|

市場調查報告書

商品編碼

2044261

歐洲丙烯酸黏合劑:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Europe Acrylic Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

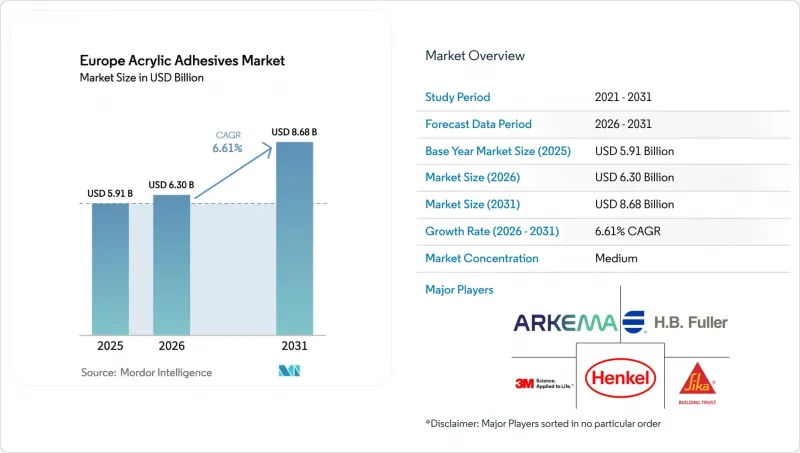

歐洲丙烯酸黏合劑市場預計將從 2025 年的 59.1 億美元成長到 2026 年的 63 億美元,到 2031 年達到 86.8 億美元,2026 年至 2031 年的複合年成長率預計為 6.61%。

電子商務包裝、汽車輕量化以及維修項目獎勵等因素正推動產品需求成長,這些因素共同促進了銷售成長並提高了平均售價。監管政策的收緊,尤其是對揮發性有機化合物 (VOC) 的基準值,加速了向低 VOC 水性化學品的轉型,迫使供應商重組供應鏈,以確保獲得符合規定的單體和乳化劑。擁有與甲基丙烯酸甲酯和丙烯酸丁酯等原料後端連接的一體化製造商保持著成本優勢,而中型加工商則透過為特定基材定製配方來提高產量。隨著買家整合供應商以確保按時交貨和合規文件,精簡產品系列、技術服務支援和快速產能擴張仍然是關鍵的競爭因素。

歐洲丙烯酸黏合劑市場的趨勢與洞察

根據歐盟揮發性有機化合物 (VOC) 法規,過渡到水性丙烯酸酯。

歐盟修訂後的VOC排放上限規定於2025年底公佈,並於2026年中期生效。該規定要求化合物生產商審核所有溶劑型SKU(庫存管理單元),加快符合規定的水性等級產品的試點生產,並為新的原料供應鏈獲得認證。已發布第三方生命週期評估(LCA)的領先者在公共競標和酒店業維修項目中獲得了優先評分,因為這些項目更重視低排放產品。乳液產品由於開放時間較長且流變性能發生變化,需要對施工人員進行再培訓,但其近乎無味的特性縮短了室內空氣重新利用前的等待時間。包裝製造商已經在測試符合生產效率和法規要求的混合丙烯酸UV乳液化學成分。總體而言,這些法規的推進預計將使歐洲丙烯酸黏合劑市場的複合年成長率(CAGR)提高1.8個百分點。

電子商務包裝的快速成長正在推動對PSA(產品安全劑)產品的需求。

向線上零售的轉型推動了對瓦楞紙板標籤、軟性薄膜和可重複密封袋的需求,這些產品需要使用壓敏丙烯酸乳液,以確保在瓦楞紙板、聚乙烯和金屬沉澱基材上實現穩定的粘合。低遷移丙烯酸酯膠黏劑擴大被指定用於RFID標籤和智慧標籤感測器,以在多溫物流循環中保持穩定性。品牌擁有者更傾向符合歐盟循環經濟指令的水性膠合劑,這類膠合劑便於纖維間回收,並可減少脫墨工序。歐洲加工商報告稱,改用新一代乳液壓敏膠後,生產線速度提高了12%,這使得歐洲丙烯酸黏合劑市場的整體成長率提高了1.5個百分點。

丙烯酸單體價格波動

裂解裝置的定期維護以及丙酮現貨市場供應緊張歷來導致甲基丙烯酸甲酯價格出現兩位數的以季度為基礎波動。儘管由於2025年下半年供應過剩,價格趨於穩定,但買家仍然保持謹慎,並轉向基本契約以及從完全一體化的供應商處進行雙重採購。原料價格±10%的波動正在擠壓配方生產商的利潤空間,推遲可自由支配的投資,並在短期內使歐洲丙烯酸黏合劑市場的成長潛力降低0.8個百分點。

細分市場分析

2025年,包裝領域佔據了歐洲丙烯酸黏合劑市場佔有率的59.56%。這主要得益於小包裹處理量的成長以及軟性薄膜複合生產線運作紀錄的運轉率。隨著品牌商轉向採用高透明度丙烯酸乳液的單一材料結構,預計該領域將保持主導地位直至2031年。阿科瑪於2024年底收購陶氏的軟性包裝黏合劑業務,立即擴大了博斯蒂克在歐洲的業務規模,並確保了其在高性能樹脂領域的後向整合。醫療包裝和藥品泡殼標籤進一步支撐了基本需求,預計在整個預測期內,包裝領域在歐洲丙烯酸黏合劑市場的規模將穩步成長。

儘管汽車領域目前市場佔有率較小,但預計其成長速度將最快,複合年成長率 (CAGR) 為 6.72%,組裝電池模組組裝、輕量化素車黏合以及對電氣化領域的投資。為了延長續航里程,汽車平臺正在進行大規模的減重,而原始設備製造商 (OEM) 正在檢驗使用丙烯酸膠帶進行混合金屬接頭連接,以應對熱膨脹係數的差異。一家德國汽車製造商簽署的一項策略採購協議確保了多年的產能,為歐洲丙烯酸黏合劑市場在移動出行價值鏈中開闢了清晰的成長路徑。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 向水性丙烯酸產品的轉變是由歐盟的 VOC 法規所推動的。

- 電子商務包裝需求的激增帶動了對壓敏膠的需求。

- 汽車輕量化和複合材料粘合

- 歐盟的「翻新浪潮」正在推動對用於外牆保溫的黏合劑的需求。

- 使用結構丙烯酸樹脂對風力發電機葉片維修

- 市場限制因素

- 丙烯酸單體價格波動

- 遵守溶劑型產品VOC法規的成本

- 利用生物基聚氨酯分散體爭奪市場佔有率

- 價值鏈分析

- 監理情勢

- 分銷通路分析

- 波特五力模型

- 買方的議價能力

- 供應商的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模與成長預測

- 按最終用戶行業分類

- 航太

- 車

- 建築/施工

- 鞋類皮革

- 衛生保健

- 包裝

- 其他

- 透過技術

- 反應性

- 溶劑型

- 紫外線固化型

- 水溶液

- 國家

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- 3M

- Arkema

- Avery Dennison Corporation

- Dow

- HB Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC

- MAPEI SpA

- Sika AG

- Soudal Holding NV

- BASF

- Dymax Corporation

- ITW Performance Polymers

- PARKER HANNIFIN CORP

- Lohmann

- Hoenle AG

- Parson Adhesives, Inc.

- Novatech International

第7章 市場機會與未來展望

The Europe Acrylic Adhesives Market size is expected to increase from USD 5.91 billion in 2025 to USD 6.30 billion in 2026 and reach USD 8.68 billion by 2031, growing at a CAGR of 6.61% over 2026-2031. Product demand benefits from e-commerce packaging, vehicle lightweighting, and retrofit construction incentives that collectively lift volumes and improve average selling prices. Regulatory changes that tighten volatile-organic-compound (VOC) thresholds accelerate the switch to low-VOC water-borne chemistries, prompting suppliers to re-engineer supply chains for compliant monomers and emulsifiers. Integrated producers with backward linkages into methyl-methacrylate and butyl-acrylate feedstocks retain a cost edge, while mid-tier converters win volume with tailored formulations for niche substrates. Portfolio rationalization, technical-service support, and rapid scale-up capacity remain decisive competitive factors as buyers consolidate supplier bases to secure on-time deliveries and regulatory documentation.

Europe Acrylic Adhesives Market Trends and Insights

Shift Toward Water-Borne Acrylics Under European Union VOC Limits

Revised EU VOC ceilings, announced late 2025 and effective mid-2026, compel formulators to audit every solvent-borne stock-keeping unit, accelerate pilot runs of compliant water-borne grades, and certify new raw-material supply chains. Early movers that publish third-party life-cycle assessments secure preferential scores in public tenders and hospitality refurbishments that weight low-emission products higher. Installers need retraining because emulsion systems exhibit longer open time and altered rheology, yet their near-zero odor profile reduces indoor-air re-occupancy delays. Packaging groups have already trialed hybrid acrylic UV-emulsion chemistries that meet both productivity and compliance targets. Collectively, the legislative push adds a visible 1.8 percentage-point uplift to the forecast CAGR of the Europe Acrylic Adhesives market.

E-Commerce Packaging Boom Driving PSA Demand

Online retail migration propels demand for corrugated labels, flexible films, and resealable pouches that rely on pressure-sensitive acrylic emulsions for consistent tack across cardboard, polyethylene, and metallized substrates. RFID tags and smart-label sensors increasingly specify low-migration acrylics that remain stable through multi-temperature logistics cycles. Brand owners favor water-borne grades that facilitate fiber-to-fiber recycling and reduce de-inking steps, aligning with EU circular-economy directives. European converters report line-speed gains of up to 12% after switching to next-generation emulsion PSAs, supporting a 1.5 percentage-point boost to overall growth in the Europe Acrylic Adhesives market.

Acrylic-Monomer Price Volatility

Scheduled cracker turnarounds and spot acetone tightness have historically triggered double-digit quarterly swings in methyl-methacrylate pricing. Although late-2025 oversupply cooled quotations, buyers remain wary and shift toward formula-based contracts or dual sourcing from fully integrated suppliers. Feedstock swings of +-10% compress formulators' margins, delaying discretionary investments and shaving 0.8 percentage-points off the Europe acrylic adhesives market growth potential in the near term.

Other drivers and restraints analyzed in the detailed report include:

- Automotive Lightweighting and Mixed-Material Bonding

- EU Renovation Wave Spurring Facade-Insulation Adhesives

- VOC-Compliance Costs for Solvent Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Packaging accounted for 59.56% of the Europe Acrylic Adhesives market share in 2025, supported by escalating parcel volumes and flexible-film lamination lines running at record utilization. The segment is expected to retain leadership through 2031 as brand owners migrate to mono-material structures that rely on high-clarity acrylic emulsions. Arkema's late-2024 acquisition of Dow's flexible-packaging adhesive assets immediately lifted Bostik's European footprint and secured backward integration into performance resins. Medical packaging and pharmaceutical blister labels further reinforce baseline demand, ensuring the Europe Acrylic Adhesives market size for packaging expands steadily across the forecast years.

Automotive, while contributing a smaller base, is forecast to grow fastest at 6.72% CAGR on the back of battery module assembly, lightweight body-in-white bonding, and electromobility investments. Vehicle platforms aggressively cut weight to extend driving range, and OEMs (Original Equipment Manufacturers) validate acrylic tapes for mixed-metal joints that tolerate differential thermal expansion. Strategic sourcing arrangements signed by German automakers secure multi-year capacity reservations, creating a visible growth pipeline for the Europe acrylic adhesives market within the mobility value chain.

The Europe Acrylic Adhesives Market Report is Segmented by End-User Industry (Aerospace, Automotive, Building and Construction, Footwear and Leather, Healthcare, Packaging, and More), Technology (Reactive, Solvent-Borne, UV-Cured Adhesives, and Water-Borne), and Country (Australia, China, India, Indonesia, Malaysia, Singapore, South Korea, and Rest of Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- 3M

- Arkema

- Avery Dennison Corporation

- Dow

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC

- MAPEI S.p.A.

- Sika AG

- Soudal Holding N.V.

- BASF

- Dymax Corporation

- ITW Performance Polymers

- PARKER HANNIFIN CORP

- Lohmann

- Hoenle AG

- Parson Adhesives, Inc.

- Novatech International

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shift toward water-borne acrylics under European Union VOC limits

- 4.2.2 E-commerce packaging boom driving PSA demand

- 4.2.3 Automotive lightweighting and mixed-material bonding

- 4.2.4 European Union "Renovation Wave" spurring facade-insulation adhesives

- 4.2.5 Wind-turbine blade refurbishment using structural acrylics

- 4.3 Market Restraints

- 4.3.1 Acrylic-monomer price volatility

- 4.3.2 VOC-compliance costs for solvent systems

- 4.3.3 Bio-based polyurethane dispersions cannibalising share

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Distribution Channel Analysis

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By End-user Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Footwear and Leather

- 5.1.5 Healthcare

- 5.1.6 Packaging

- 5.1.7 Other End-user Industries

- 5.2 By Technology

- 5.2.1 Reactive

- 5.2.2 Solvent-borne

- 5.2.3 UV-cured

- 5.2.4 Water-borne

- 5.3 By Country

- 5.3.1 Germany

- 5.3.2 United Kingdom

- 5.3.3 France

- 5.3.4 Italy

- 5.3.5 Spain

- 5.3.6 Russia

- 5.3.7 NORDIC Countries

- 5.3.8 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 Avery Dennison Corporation

- 6.4.4 Dow

- 6.4.5 H.B. Fuller Company

- 6.4.6 Henkel AG & Co. KGaA

- 6.4.7 Huntsman International LLC

- 6.4.8 MAPEI S.p.A.

- 6.4.9 Sika AG

- 6.4.10 Soudal Holding N.V.

- 6.4.11 BASF

- 6.4.12 Dymax Corporation

- 6.4.13 ITW Performance Polymers

- 6.4.14 PARKER HANNIFIN CORP

- 6.4.15 Lohmann

- 6.4.16 Hoenle AG

- 6.4.17 Parson Adhesives, Inc.

- 6.4.18 Novatech International

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

丙烯酸密封劑市場:全球市場預測,2026-2032年丙烯酸黏合劑市場:2026-2032年全球市場預測(按產品類型、形態、固化方法、應用、終端用戶產業和分銷管道分類)

丙烯酸密封劑市場:全球市場預測,2026-2032年丙烯酸黏合劑市場:2026-2032年全球市場預測(按產品類型、形態、固化方法、應用、終端用戶產業和分銷管道分類) 亞太地區丙烯酸黏合劑:市場佔有率分析、產業趨勢和統計數據以及成長預測(2026-2031 年)

亞太地區丙烯酸黏合劑:市場佔有率分析、產業趨勢和統計數據以及成長預測(2026-2031 年) 全球丙烯酸黏合劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球丙烯酸黏合劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球高強度丙烯酸黏合劑市場報告

2026年全球高強度丙烯酸黏合劑市場報告 丙烯酸黏合劑市場規模、佔有率和成長分析(按類型、技術、應用和地區分類)—產業預測,2026-2033年

丙烯酸黏合劑市場規模、佔有率和成長分析(按類型、技術、應用和地區分類)—產業預測,2026-2033年 丙烯酸黏合劑市場-全球產業規模、佔有率、趨勢、機會與預測(按技術、應用、地區和競爭細分,2020-2030 年)丙烯酸密封膠市場-全球產業規模、佔有率、趨勢、機會及預測,按類型(彩色、無色)、按應用(建築、汽車、其他)、按地區及競爭情況細分,2020-2030 年丙烯酸黏合劑:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)

丙烯酸黏合劑市場-全球產業規模、佔有率、趨勢、機會與預測(按技術、應用、地區和競爭細分,2020-2030 年)丙烯酸密封膠市場-全球產業規模、佔有率、趨勢、機會及預測,按類型(彩色、無色)、按應用(建築、汽車、其他)、按地區及競爭情況細分,2020-2030 年丙烯酸黏合劑:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030) 2030 年丙烯酸黏合劑市場預測:按類型、技術、應用、最終用戶和地區進行的全球分析

2030 年丙烯酸黏合劑市場預測:按類型、技術、應用、最終用戶和地區進行的全球分析