|

市場調查報告書

商品編碼

2044260

亞太地區丙烯酸黏合劑:市場佔有率分析、產業趨勢和統計數據以及成長預測(2026-2031 年)Asia-Pacific Acrylic Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

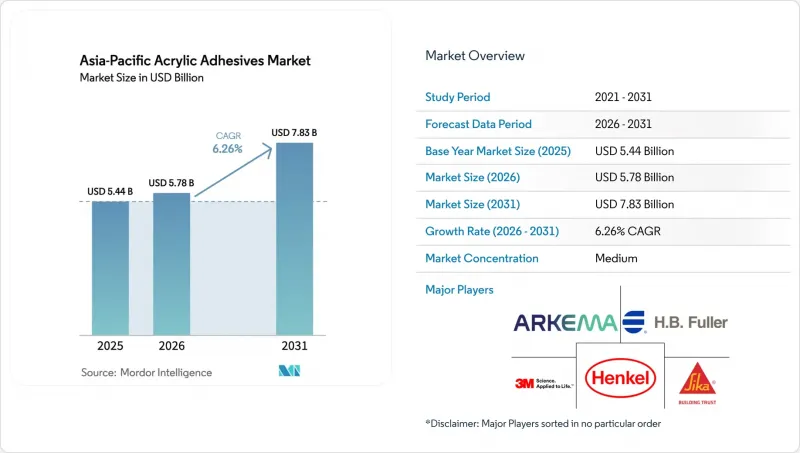

預計亞太地區丙烯酸黏合劑市場將從 2025 年的 54.4 億美元和 2026 年的 57.8 億美元成長到 2031 年的 78.3 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 6.26%。

電子商務包裝的擴張、電動車 (EV) 零件組裝的加速以及更嚴格的區域性揮發性有機化合物 (VOC) 法規,都支撐著包裝銷量的穩定成長。水性丙烯酸類化學品繼續應用於包裝生產線,以滿足回收目標並提供快速剝離和密封性能。同時,電池製造商正在採用導熱丙烯酸混合材料,以在電池單體封裝設計中實現散熱。製造商還將產能轉移到泰國、馬來西亞和越南,以利用兩位數的稅收優惠來降低新建反應器的巨額資本投資成本。然而,原料成本的波動仍然對利潤率構成壓力,預計在中東供應衝擊之後,甲基丙烯酸甲酯的價格將在 2025 年下降 21%,然後在 2026 年初反彈。

亞太地區丙烯酸黏合劑市場趨勢及洞察

電動車和電子產品製造業的激增

電池生產仍然是特殊丙烯酸酯需求的主要驅動力。寧德時代(CATL)預計到2025年將出貨661GWh的鋰離子電池,運轉率高達96.9%,這促使黏合劑開發商提供導熱且抗震的丙烯酸酯混合材料,用於將電池直接黏合到電池組機殼。湖北匯天將於2025年投資9,768萬元人民幣(約1,359萬美元)新建一條乳膠黏合劑生產線,並與台蘭新能源合作開發固態電池黏合劑,該產品將於2027年後實現商業化生產。半導體國產化過程進一步擴大了需求。南工集團於2025年成立了一家合資企業,旨在開發適用於先進製程節點的超低釋氣晶片封裝黏合劑。受奈米銀和丙烯酸酯晶片黏接解決方案的持續需求驅動,預計到2030年,韓國碳化矽功率晶片黏合劑市場規模將成長三倍,達到8,500億韓元(約5.984億美元)。

推廣低揮發性有機化合物(VOC)水基系統的相關法規

中國標準GB 33372-2020將溶劑型丙烯酸樹脂的VOC含量限制在510 g/L以內,而用於室內的水性產品的VOC含量必須低於50 g/L。這促使生產線廣泛改造為乳化工藝,並擴大乾燥區域。新加坡的「超低能耗建築計畫」和馬來西亞的「綠色技術投資信貸」也同樣強化了相關標準,鼓勵複合材料生產商獲得ISO 14024生態標籤認證。歐盟的「包裝和包裝廢棄物法規」將於2025年生效,其中新增一項要求:到2030年,亞洲生產的軟包裝材料中必須含有30%的再生材料,這進一步加大了外部合規壓力。BASF在2025年中國國際塑膠橡膠工業展(CHINAPLAS 2025)上展出的Acrodur樹脂正是這項商業性轉變的體現。該樹脂是一種可熱交聯、不含甲醛的水性丙烯酸樹脂,可與75%的再生纖維相容。

丙烯酸單體價格波動與原物料風險

到2025年12月,甲基丙烯酸甲酯的價格跌至每噸1,275美元,較1月下降了21%。然而,由於中東地區緊張局勢升級,導致石腦油(該地區60%以上的裂解原料由石腦油供應)供應中斷,三菱化學宣布將於2026年3月上調價格。BASF隨後也宣布,將於2026年3月將丙烯酸酯的價格上調每噸100美元,理由是物流和能源成本飆升。這種價格波動削弱了期貨價格的可預測性,迫使化合物生產商採取重複供貨和增加安全庫存的措施。

細分市場分析

2025年,包裝產業在亞太地區丙烯酸黏合劑市場中佔據59.56%的佔有率。跨境電商的蓬勃發展以及零售商為減少一次性塑膠的使用而採取的措施,推動了小包裹處理量的增加,進而帶動了水性黏合劑在瓦楞紙板封口和軟性複合應用領域的持續高需求。在預測期(2026-2031年)內,亞太地區丙烯酸黏合劑在汽車應用領域的市場規模將以6.72%的複合年成長率(CAGR)高速成長。這主要得益於輕量化多材料車身和碳化矽逆變器對耐熱接頭的需求。建築業的需求呈現兩極化。儘管中國住宅開工量增加了1.8%,但黏合劑需求卻放緩。同時,由於資料中心和半導體製造廠的建設,印度、越南和馬來西亞的膠合劑需求實現了中等個位數的成長。印度鞋類出口商受益於歐盟自由貿易協定(FTA)的關稅減免政策,從而增加了用於PU襯裡皮革鞋面的丙烯酸黏合劑的採購量。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 中國主導的電動車和電子產品製造中心快速發展

- 推廣低揮發性有機化合物(VOC)水基系統的相關法規

- 履約的擴展

- 印度和東協的大型建設項目

- 東協的免稅措施將促進區域黏合劑生產。

- 市場限制因素

- 丙烯酸單體價格波動與原物料風險

- 加速高強度接頭中聚氨酯和環氧樹脂的推廣應用

- 減少溶劑型揮發性有機化合物的合規成本

- 價值鏈分析

- 分銷通路分析

- 監理情勢

- 波特五力模型

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模與成長預測

- 按最終用戶行業分類

- 航太

- 車

- 建築/施工

- 鞋類皮革

- 衛生保健

- 包裝

- 其他

- 透過技術

- 反應性

- 溶劑型

- 紫外線固化型

- 水溶液

- 國家

- 澳洲

- 中國

- 印度

- 印尼

- 日本

- 馬來西亞

- 新加坡

- 韓國

- 泰國

- 亞太其他地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率/排名分析

- 公司簡介

- 3M

- Arkema

- artience Co., Ltd.

- Avery Dennison Corporation

- BASF

- Dow Inc.

- Dymax Corporation

- HB Fuller Company

- Henkel AG & Co. KGaA

- Hubei Huitian New Materials Co., Ltd.

- Huntsman Corporation

- ITW Performance Polymers

- Jowat SE

- Kangda New Materials(Group)Co., Ltd.

- NANPAO RESINS CHEMICAL GROUP

- Permabond LLC

- Pidilite Industries Ltd.

- Sika AG

第7章 市場機會與未來展望

The Asia-Pacific Acrylic Adhesives Market size is projected to expand from USD 5.44 billion in 2025 and USD 5.78 billion in 2026 to USD 7.83 billion by 2031, registering a CAGR of 6.26% between 2026 and 2031. Expanding e-commerce packaging, accelerating electric-vehicle component assembly, and tighter regional VOC (Volatile Organic Compound) regulations underpin steady volume growth. Packaging lines continue to specify water-borne acrylic chemistries because they meet recyclability targets and deliver rapid peel-seal performance, while battery makers adopt thermally conductive acrylic hybrids that dissipate heat in cell-to-pack designs. Producers are also relocating capacity toward Thailand, Malaysia, and Vietnam to capture double-digit tax incentives that lower effective capex on new reactors. Feedstock cost swings, however, still compress margins, with 2025 methyl methacrylate prices falling 21% before rebounding in early 2026 on Middle-East supply shocks.

Asia-Pacific Acrylic Adhesives Market Trends and Insights

Surge in Electric Vehicle and Electronics Manufacturing

Battery-cell production remains the principal catalyst for specialty acrylic demand. CATL shipped 661 GWh of lithium-ion batteries in 2025 at 96.9% utilization, prompting adhesive developers to supply thermally conductive, vibration-resistant acrylic hybrids that bond cells directly to pack enclosures. Hubei Huitian invested RMB 97.68 million (USD 13.59 million) in 2025 for a new latex binder line and partnered with Tailan New Energy on solid-state battery adhesives that will reach commercial scale after 2027. Semiconductor localization amplifies the pull; NANPAO formed a 2025 joint venture to formulate ultra-low outgassing chip-package adhesives suited to advanced nodes. South Korea's market for silicon-carbide power-chip adhesives is projected to triple to KRW 850 billion (USD 598.4 million) by 2030, sustaining demand for nano-silver and acrylic-based die attach solutions.

Regulatory Push Toward Low-VOC, Water-Borne Systems

China's GB 33372-2020 limits solvent-borne acrylics to 510 g/L VOC, whereas water-borne analogs must stay below 50 g/L in indoor uses, forcing widespread line conversions to emulsion polymerization and longer oven zones. Singapore's Super Low-Energy building program and Malaysia's Green Technology Investment Allowance reinforce similar thresholds, encouraging formulators to certify products under ISO 14024 ecolabels. The European Union Packaging and Packaging Waste Regulation, effective 2025, adds an external compliance lever because Asia-made flexible packs must hit 30% recycled content by 2030. BASF's Acrodur resins showcased at CHINAPLAS 2025 demonstrate the commercial pivot, offering thermally crosslinkable, formaldehyde-free water-borne acrylics compatible with 75% regenerated fibers.

Acrylic-Monomer Price Volatility and Feedstock Risk

Methyl methacrylate prices fell to USD 1,275 per ton by December 2025, 21% below January, before Mitsubishi Chemical announced a price rise in March 2026 as Middle-East tensions disrupted naphtha flows that supply over 60% of regional cracker feedstock. BASF followed with USD 100 per ton acrylate increases in March 2026, citing higher logistics and energy outlays. Such whipsaw movements erode forward-pricing visibility and drive formulators toward dual sourcing and higher safety stocks.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Flexible Packaging for E-Commerce Fulfillment

- Mega Construction Projects Across India and ASEAN

- Intensifying PU and Epoxy Substitution in High-Strength Joints

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Packaging commanded 59.56% of the Asia-Pacific acrylic adhesives market share in 2025. Rising parcel volumes from cross-border e-commerce and retailer commitments to curb single-use plastics sustain high-volume water-borne consumption in carton sealing and flexible laminations. The Asia-Pacific Acrylic Adhesives market size tied to automotive uses is expanding at the fastest CAGR of 6.72% duirng the forecast period (2026-2031) because lightweight multi-material bodies and silicon-carbide inverters need heat-resistant joints. Building and construction demand is diverging: China's adhesive volumes soften with its 1.8% uptick in residential starts, but India, Vietnam, and Malaysia deliver mid-single-digit gains through data-center and semiconductor-fab work. Footwear exporters in India gain from the EU FTA tariff removal, spurring incremental acrylic purchases for PU-lined leather uppers.

The Asia-Pacific Acrylic Adhesives Market Report is Segmented by End-User Industry (Aerospace, Automotive, Building and Construction, Footwear and Leather, Healthcare, Packaging, and More), Technology (Reactive, Solvent-Borne, UV-Cured Adhesives, and Water-Borne), and Country (Australia, China, India, Indonesia, Malaysia, Singapore, South Korea, and Rest of Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- 3M

- Arkema

- artience Co., Ltd.

- Avery Dennison Corporation

- BASF

- Dow Inc.

- Dymax Corporation

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Hubei Huitian New Materials Co., Ltd.

- Huntsman Corporation

- ITW Performance Polymers

- Jowat SE

- Kangda New Materials (Group) Co., Ltd.

- NANPAO RESINS CHEMICAL GROUP

- Permabond LLC

- Pidilite Industries Ltd.

- Sika AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in Electric Vehicle and electronics manufacturing in China-led hubs

- 4.2.2 Regulatory push toward low-VOC, water-borne systems

- 4.2.3 Expansion of flexible packaging for e-commerce fulfilment

- 4.2.4 Mega construction projects across India and ASEAN

- 4.2.5 ASEAN tax-holiday schemes catalysing local adhesive output

- 4.3 Market Restraints

- 4.3.1 Acrylic-monomer price volatility and feedstock risk

- 4.3.2 Intensifying PU and epoxy substitution in high-strength joints

- 4.3.3 Compliance cost of solvent-borne VOC abatement

- 4.4 Value Chain Analysis

- 4.5 Distribution Channel Analysis

- 4.6 Regulatory Landscape

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By End-user Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Footwear and Leather

- 5.1.5 Healthcare

- 5.1.6 Packaging

- 5.1.7 Other End-user Industries

- 5.2 By Technology

- 5.2.1 Reactive

- 5.2.2 Solvent-borne

- 5.2.3 UV-Cured Adhesives

- 5.2.4 Water-borne

- 5.3 By Country

- 5.3.1 Australia

- 5.3.2 China

- 5.3.3 India

- 5.3.4 Indonesia

- 5.3.5 Japan

- 5.3.6 Malaysia

- 5.3.7 Singapore

- 5.3.8 South Korea

- 5.3.9 Thailand

- 5.3.10 Rest of Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share/Raking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)}

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 artience Co., Ltd.

- 6.4.4 Avery Dennison Corporation

- 6.4.5 BASF

- 6.4.6 Dow Inc.

- 6.4.7 Dymax Corporation

- 6.4.8 H.B. Fuller Company

- 6.4.9 Henkel AG & Co. KGaA

- 6.4.10 Hubei Huitian New Materials Co., Ltd.

- 6.4.11 Huntsman Corporation

- 6.4.12 ITW Performance Polymers

- 6.4.13 Jowat SE

- 6.4.14 Kangda New Materials (Group) Co., Ltd.

- 6.4.15 NANPAO RESINS CHEMICAL GROUP

- 6.4.16 Permabond LLC

- 6.4.17 Pidilite Industries Ltd.

- 6.4.18 Sika AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

丙烯酸密封劑市場:全球市場預測,2026-2032年丙烯酸黏合劑市場:2026-2032年全球市場預測(按產品類型、形態、固化方法、應用、終端用戶產業和分銷管道分類)

丙烯酸密封劑市場:全球市場預測,2026-2032年丙烯酸黏合劑市場:2026-2032年全球市場預測(按產品類型、形態、固化方法、應用、終端用戶產業和分銷管道分類) 歐洲丙烯酸黏合劑:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

歐洲丙烯酸黏合劑:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 全球丙烯酸黏合劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球丙烯酸黏合劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球高強度丙烯酸黏合劑市場報告

2026年全球高強度丙烯酸黏合劑市場報告 丙烯酸黏合劑市場規模、佔有率和成長分析(按類型、技術、應用和地區分類)—產業預測,2026-2033年

丙烯酸黏合劑市場規模、佔有率和成長分析(按類型、技術、應用和地區分類)—產業預測,2026-2033年 丙烯酸黏合劑市場-全球產業規模、佔有率、趨勢、機會與預測(按技術、應用、地區和競爭細分,2020-2030 年)丙烯酸密封膠市場-全球產業規模、佔有率、趨勢、機會及預測,按類型(彩色、無色)、按應用(建築、汽車、其他)、按地區及競爭情況細分,2020-2030 年丙烯酸黏合劑:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)

丙烯酸黏合劑市場-全球產業規模、佔有率、趨勢、機會與預測(按技術、應用、地區和競爭細分,2020-2030 年)丙烯酸密封膠市場-全球產業規模、佔有率、趨勢、機會及預測,按類型(彩色、無色)、按應用(建築、汽車、其他)、按地區及競爭情況細分,2020-2030 年丙烯酸黏合劑:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030) 2030 年丙烯酸黏合劑市場預測:按類型、技術、應用、最終用戶和地區進行的全球分析

2030 年丙烯酸黏合劑市場預測:按類型、技術、應用、最終用戶和地區進行的全球分析