|

市場調查報告書

商品編碼

2044211

列印貼標及貼標設備:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Print And Apply Labeling And Labeling Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

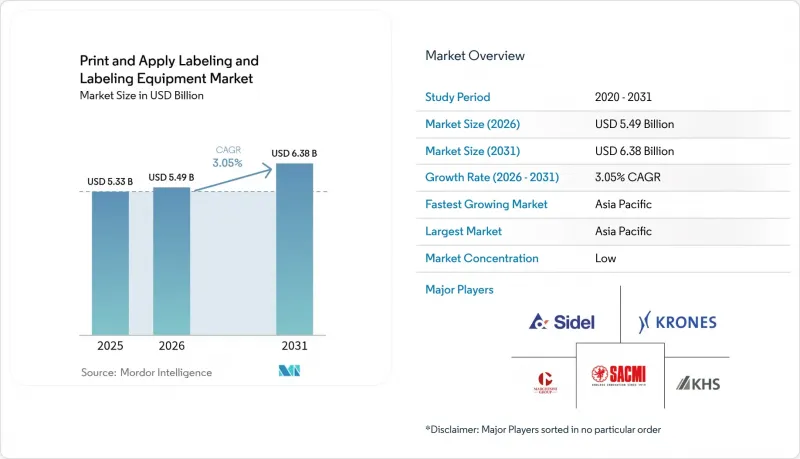

預計到 2025 年,列印貼上標籤和貼標設備的市場規模將達到 53.3 億美元,到 2026 年將達到 54.9 億美元,到 2031 年將達到 63.8 億美元。

預計從 2026 年到 2031 年,年複合成長率將達到 3.05%。

高速食品飲料包裝、藥品序列化專案以及電子商務履約流程等需求推動了按需可變資料印刷的發展。邊緣人工智慧驅動的缺陷檢測縮短了換線時間,而數位噴墨模組實現了「單批量」經濟效益,使品牌所有者能夠開展短期促銷宣傳活動,而無需持有數週的預印庫存。亞太地區仍然是量化成長的主要驅動力,中國小包裹量的成長和印度RFID投資與工廠車間自動化預算融合。同時,北美和歐洲仍然專注於遵守永續性和可追溯性法規,正在評估具有整合視覺檢測功能的全自動系統。競爭對手之間的競爭仍然較低。五家全球原始設備製造商(OEM)仍佔據近一半的裝置容量,但價格極具競爭力的中國整合商正在擴大模組化單元的規模,其價格比歐美製造商的標價低40%,迫使現有製造商依賴物聯網服務合約來保障其利潤率。

全球列印貼標及貼標設備市場趨勢與洞察

數位印刷和全自動覆膜機的演變

數位噴墨和UV-LED模組不僅在速度上可與柔版印刷媲美,而且無需印版,使飲料OEM廠商能夠將標籤庫存週期從12週縮短至3天,從而節省營運資金。達美樂披薩於2025年11月推出的Dx1060i雷射打碼機,可在紙板和冷凍水產品紙盒上以每分鐘200公尺的速度進行列印,同時降低40%的能耗。Konica Minolta的AccurioLabel 400具備線上分光光度計功能,即使對於擁有數百個SKU的品牌,也能將色差控制在Delta-E 0.5以內。配備視覺系統的伺服控制施用器可校正紙板錯位,將缺陷率控制在0.05%以下。艾丁格魏斯布勞啤酒公司於2026年1月實施了人工智慧列印引擎,並驗證了這項數據。高解析度列印頭與閉合迴路機器人技術的結合,正推動列印貼標和貼標設備市場朝向無人生產和「單件生產」個人化方向發展。

嚴格的可追溯性和序列化規定

美國《藥品供應鏈安全法案》強制要求在2024年11月前實現單元級2D資料矩陣編碼,這將使列印貼標站從單純的列印後附加功能轉變為符合法規要求的必要設備。在歐洲,防篡改封條的引入,以及《反假冒藥品指令》的規定,已經推動採購轉向結合收縮套標和噴墨序列化模組的解決方案。 ForgeStop計劃於2026年1月發布的支援NFC功能的標籤,整合了序列化和溫度追蹤功能,旨在解決低溫運輸每年高達350億美元的浪費問題。巴西和沙烏地阿拉伯也在同步實施相關法規,進一步擴大了全部區域的需求。這些要求解釋了為什麼儘管序列化平台價格更高,但在列印貼標和貼標設備市場,它們的表現卻優於傳統的半自動生產線。

高速列印貼合系統的資本投資強度

整合雙面編碼、視覺檢測和資料庫序列化的下一代生產線成本高達25萬至50萬美元,其投資回收期遠超中小企業的承受能力。一項2025年的北美調查發現,62%的合約包裝公司推遲了自動化進程,轉而增加傳統設備的班次。儘管租賃方案在歐洲逐漸興起,但由於兩位數的利率,南美和非洲的使用率仍然很低。 2023年至2025年間印字頭解析度的翻倍進一步加劇了設備快速過時的風險。除非「設備即服務(EaaS)」模式在全球廣泛應用,否則高資本密集度將繼續拖累列印貼標和貼標設備市場的成長速度。

細分市場分析

到2025年,全自動平台將佔據列印貼標和貼標設備市場89.51%的佔有率,預計到2031年將以4.51%的複合年成長率成長。這些系統以封閉回路型機器人取代人工干預,可將單位人事費用降低高達70%。在艾丁格魏斯啤酒廠,經過2026年1月的維修,得益於人工智慧控制的列印引擎,缺陷率降至0.05%以下。半自動化設備仍適用於SKU頻繁更換的代工包裝場所,而手動操作工位則仍應用於手工食品生產和臨床試驗標籤貼標等領域。

人們對物聯網連接日益成長的興趣正在進一步拉大差距。 SATO在2025年7月於泰國擴建的生產線中新增了一條配備眾多感測器並透過雲端監控的專用生產線。此生產線能夠在停機前檢測列印頭磨損情況。半自動設備現在配備了觸控螢幕設定嚮導,在熟練技術人員短缺的情況下,這使得培訓更加便利。隨著模組化、低成本的「列印貼標」單元(售價低於3萬美元)進入列印貼標和貼標設備市場,手動工具的使用正在穩步減少。這擴大了自動化應用的普及範圍,即使是精釀啤酒廠和利基化妝品品牌也能從中受益。

區域分析

預計到2025年,亞太地區將佔全球銷售額的37.89%,並以4.92%的複合年成長率成長,這主要得益於中國2024年處理的1750億小包裹以及印度RFID產能的擴張。艾利丹尼森位於浦那的嵌體工廠(投資3,000萬美元)將於2025年4月投產,屆時年產能將達到50億個標籤,以滿足全通路零售的激增需求。OMRON位於班加羅爾的自動化中心將進一步解決熟練技術人員短缺的問題,這原本可能成為實施過程中的瓶頸。

北美和歐洲的成長率接近3.05%的全球平均水平,但重點在於利潤豐厚、完全自動化且符合序列化和永續性相關法規的系統。歐盟委員會的《包裝和包裝廢棄物法規》設定了2030年將包裝減少15%的目標,這推動了人們對無底紙技術和數位印刷的興趣。在美國,FDA的可追溯性法規要求2027年40%的食品生產線進行升級改造,這將增加對現有設備維修的需求。

在南美,由於巴西計畫在2027年前分階段推行藥品序列化,以及大量外商直接投資湧入自動化領域,市場正蓬勃發展。DAIFUKU CO. LTD.於2025年4月宣佈在特倫甘納邦投資2,400萬美元建設工廠,凸顯了該地區物流樞紐的潛力。儘管中東和非洲仍處於發展中,但沙烏地阿拉伯將於2024年實施的藥品序列化法規以及阿拉伯聯合大公國的航空貨運RFID計畫預示著未來五年內列印貼標和貼標設備市場將持續擴張。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 數位印刷和全自動塗佈機的演變

- 強制性嚴格可追溯性和序列化

- 食品飲料產業對高速包裝線自動化的需求

- 電子商務低溫運輸中雙溫標籤的必要性

- 推廣無底紙標籤形式的永續性

- 物聯網邊緣預測性維護在標籤生產線的應用

- 市場限制因素

- 高速列印貼合系統的資本投資強度

- 高濕度環境/冷卻隧道內的耐久性問題

- 綜合維修工程師短缺

- 由於RFID嵌體供應波動,原料成本上漲。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模與成長預測

- 透過技術

- 全自動

- 半自動

- 手動的

- 標籤類型

- 壓敏膠/黏合劑

- 收縮套

- 黏合劑底座

- 套模

- 無底紙標籤貼標機

- 智慧標籤(RFID/QR)系統

- 最終用戶

- 食品/飲料

- 製藥

- 個人護理和家居用品

- 工業與物流

- 其他終端用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 智利

- 南美洲其他地區

- 歐洲

- 德國

- 英國

- 法國

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 亞太其他地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲地區

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Avery Dennison Corporation

- Axon LLC

- BW Packaging(Barry-Wehmiller Group, Inc)

- Domino Printing Sciences PLC

- Videojet Technologies

- Fuji Seal International, Inc.

- Heuft Systemtechnik GmbH

- HERMA GmbH

- ID Technology, LLC

- KHS GmbH

- Krones AG

- Shenzhen Shuangcheng Automation Co., Ltd

- Marchesini Group SpA

- MARKEM-IMAJE(DOVER CORPORATION)

- Novexx Solutions GmbH

- PDC International Corp.

- Quadrel Labeling Systems

- FoxJet

- SATO Holdings Corporation

- SIDEL(Tetra Laval)

- Weber Marking Systems GmbH

- ProMach

- Wuxi Sici Auto Co, Ltd.

第7章 市場機會與未來展望

The print and apply labeling and labeling equipment market size is projected to be USD 5.33 billion in 2025, USD 5.49 billion in 2026, and reach USD 6.38 billion by 2031, growing at a CAGR of 3.05% from 2026 to 2031.

Demand is anchored in high-speed food and beverage packaging, pharmaceutical serialization programs, and e-commerce fulfillment workflows that favor on-demand variable data printing. Edge-AI defect detection is shortening changeover windows while digital inkjet modules deliver lot-size-of-one economics, encouraging brand owners to run short promotional campaigns without holding weeks of pre-printed inventory. Asia-Pacific remains the volume growth engine as China's parcel throughput and India's RFID investments translate into factory-floor automation budgets, whereas North America and Europe continue to target sustainability and traceability mandates that reward fully automatic systems with integrated vision inspection. Competitive rivalry is moderate: five global OEMs still control nearly half of installed capacity, yet price-aggressive Chinese integrators are scaling modular cells that undercut Western list prices by up to 40%, forcing incumbents to lean on IoT-enabled service contracts for margin defense.

Global Print And Apply Labeling And Labeling Equipment Market Trends and Insights

Evolution Of Digital Printing And Fully Automatic Applicators

Digital inkjet and UV-LED modules now rival flexography on speed while eliminating plates, enabling beverage co-packers to slash label inventory from twelve weeks to three days and unlock working-capital savings. Domino's Dx1060i laser coder, released in November 2025, prints 200 meters per minute on corrugated and frozen seafood cartons while cutting energy use by 40%. Konica Minolta's AccurioLabel 400 adds inline spectrophotometry, keeping color drift within 0.5 Delta-E for brands juggling hundreds of SKUs. Servo-guided applicators equipped with vision systems compensate for carton misalignment and drive defect rates below 0.05%, a metric validated by Erdinger Weissbrau's January 2026 installation of AI-enabled print engines. Together, high-resolution printheads and closed-loop robotics move the print and apply labeling and labeling equipment market toward lights-out production and lot-size-of-one personalization.

Stringent Trace And Trace And Serialization Mandates

The U.S. Drug Supply Chain Security Act requires unit-level 2D DataMatrix coding by November 2024, converting print-and-apply stations into compliance assets rather than post-printing niceties. In Europe, Falsified Medicines Directive rules plus tamper-evident seals have already shifted procurement toward combination shrink-sleeve and inkjet serialization modules. ForgeStop's January 2026 NFC-enabled label merges serialization with temperature tracking to combat USD 35 billion of annual cold-chain spoilage. Brazil and Saudi Arabia are phasing in parallel mandates that extend addressable demand across emerging regions. These requirements explain why serialization-ready platforms command premium pricing yet still outgrow legacy semi-automatic lines in the print and apply labeling and labeling equipment market.

Cap-Ex Intensity Of High-Speed Print-And-Apply Systems

Next-generation lines integrating dual-sided coding, vision inspection, and database serialization cost USD 250,000-500,000, pushing payback horizons beyond the comfort level of small and medium enterprises. North American surveys in 2025 showed 62% of contract packagers delaying automation, instead adding shifts to legacy gear. Leasing options have emerged in Europe, yet double-digit interest rates in South America and Africa keep utilization low. Rapid obsolescence compounds the risk, as printhead resolution doubled between 2023 and 2025. Unless equipment-as-a-service models proliferate globally, capital intensity will continue to shave growth points from the print and apply labeling and labeling equipment market.

Other drivers and restraints analyzed in the detailed report include:

- Automation Demand In Food And Beverage High-Speed Packaging Lines

- E-Commerce Cold-Chain Dual-Temperature Label Needs

- Shortage Of Integration And Maintenance Technicians

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fully automatic platforms captured 89.51% share of the print and apply labeling and labeling equipment market in 2025 and are projected to advance at a 4.51% CAGR to 2031. These systems replace operator intervention with closed-loop robotics, trimming labor cost per unit by up to 70%. At Erdinger Weissbrau, AI-guided print engines pushed defect rates below 0.05% after a January 2026 retrofit. Semi-automatic equipment still fits co-packing sites handling frequent SKU swaps, while manual stations linger in artisanal food production and clinical trial labeling.

Interest in IoT connectivity widens the gulf. SATO's July 2025 Thailand expansion added a line dedicated to sensor-rich, cloud-monitored machines that flag printhead wear before downtime occurs. Semi-automatic units now ship with touchscreen setup wizards, making training accessible during the technician shortage. Manual tools decline steadily as modular low-cost print-and-apply cells often below USD 30,000 enter the print and apply labeling and labeling equipment market, broadening automation access for micro-breweries and niche cosmetic brands.

The Print and Apply Labeling and Labeling Equipment Market Report is Segmented by Technology (Fully Automatic, Semi-Automatic, and Manual), Label Type (Pressure-Sensitive, Shrink-Sleeve, Glue-Based, In-Mold, Linerless, and Smart-Label RFID and QR), End-User Vertical (Food and Beverage, Pharmaceutical, Personal Care and Household, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 37.89% of 2025 revenue and is expected to expand at a 4.92% CAGR, underpinned by China's 175 billion parcel throughput in 2024 and India's RFID capacity build-outs. Avery Dennison's USD 30 million Pune inlay plant, inaugurated in April 2025, can output 5 billion tags per year to satisfy surging omnichannel retail demand. OMRON's Bengaluru Automation Center further addresses technician shortages that might otherwise bottleneck adoption.

North America and Europe grow near the global average of 3.05% yet focus on higher-margin fully automatic systems that comply with serialization and sustainability statutes. The European Commission's Packaging and Packaging Waste Regulation sets a 15% packaging-reduction target by 2030, boosting linerless and digital print interest. In the United States, FDA traceability rules mean 40% of food lines require upgrades by 2027, feeding retrofit demand.

South America gains traction as Brazil phases pharmaceutical serialization in by 2027 and as foreign direct investment pours into automation. Daifuku's USD 24 million Telangana facility, announced April 2025, underscores interest in the region's logistics hubs. The Middle East and Africa remain nascent, yet Saudi Arabia's 2024 serialization rules and United Arab Emirates air-cargo RFID projects foreshadow a lift in the print and apply labeling and labeling equipment market over the next five years.

- Avery Dennison Corporation

- Axon LLC

- BW Packaging (Barry-Wehmiller Group, Inc)

- Domino Printing Sciences PLC

- Videojet Technologies

- Fuji Seal International, Inc.

- Heuft Systemtechnik GmbH

- HERMA GmbH

- ID Technology, LLC

- KHS GmbH

- Krones AG

- Shenzhen Shuangcheng Automation Co., Ltd

- Marchesini Group S.p.A.

- MARKEM-IMAJE (DOVER CORPORATION)

- Novexx Solutions GmbH

- PDC International Corp.

- Quadrel Labeling Systems

- FoxJet

- SATO Holdings Corporation

- SIDEL (Tetra Laval)

- Weber Marking Systems GmbH

- ProMach

- Wuxi Sici Auto Co, Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Evolution of Digital Printing and Fully-Automatic Applicators

- 4.2.2 Stringent Trace-and-Trace and Serialization Mandates

- 4.2.3 Automation Demand in Food and Beverage High-Speed Packaging Lines

- 4.2.4 E-Commerce Cold-Chain Dual-Temperature Label Needs

- 4.2.5 Sustainability Push Toward Liner-Less Label Formats

- 4.2.6 IoT-Edge Predictive Maintenance for Labeling Lines

- 4.3 Market Restraints

- 4.3.1 Cap-Ex Intensity of High-Speed Print-and-Apply Systems

- 4.3.2 Durability Issues in Extreme Humidity / Freezer Tunnels

- 4.3.3 Shortage of Integration and Maintenance Technicians

- 4.3.4 RFID Inlay Supply Volatility Inflating Raw-Material Cost

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology

- 5.1.1 Fully Automatic

- 5.1.2 Semi-Automatic

- 5.1.3 Manual

- 5.2 By Label Type

- 5.2.1 Pressure-Sensitive / Self-Adhesive

- 5.2.2 Shrink-Sleeve

- 5.2.3 Glue-Based

- 5.2.4 In-Mold

- 5.2.5 Liner less Label Applicators

- 5.2.6 Smart-Label (RFID / QR) Systems

- 5.3 By End-User Vertical

- 5.3.1 Food and Beverage

- 5.3.2 Pharmaceutical

- 5.3.3 Personal Care and Household

- 5.3.4 Industrial and Logistics

- 5.3.5 Others End-User Verticals

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Chile

- 5.4.2.4 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 India

- 5.4.4.4 South Korea

- 5.4.4.5 Australia

- 5.4.4.6 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 Middle East

- 5.4.5.1.1 Saudi Arabia

- 5.4.5.1.2 United Arab Emirates

- 5.4.5.1.3 Turkey

- 5.4.5.1.4 Rest of Middle East

- 5.4.5.2 Africa

- 5.4.5.2.1 South Africa

- 5.4.5.2.2 Nigeria

- 5.4.5.2.3 Rest of Africa

- 5.4.5.1 Middle East

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 Avery Dennison Corporation

- 6.4.2 Axon LLC

- 6.4.3 BW Packaging (Barry-Wehmiller Group, Inc)

- 6.4.4 Domino Printing Sciences PLC

- 6.4.5 Videojet Technologies

- 6.4.6 Fuji Seal International, Inc.

- 6.4.7 Heuft Systemtechnik GmbH

- 6.4.8 HERMA GmbH

- 6.4.9 ID Technology, LLC

- 6.4.10 KHS GmbH

- 6.4.11 Krones AG

- 6.4.12 Shenzhen Shuangcheng Automation Co., Ltd

- 6.4.13 Marchesini Group S.p.A.

- 6.4.14 MARKEM-IMAJE (DOVER CORPORATION)

- 6.4.15 Novexx Solutions GmbH

- 6.4.16 PDC International Corp.

- 6.4.17 Quadrel Labeling Systems

- 6.4.18 FoxJet

- 6.4.19 SATO Holdings Corporation

- 6.4.20 SIDEL (Tetra Laval)

- 6.4.21 Weber Marking Systems GmbH

- 6.4.22 ProMach

- 6.4.23 Wuxi Sici Auto Co, Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

標籤印刷市場:按標籤格式、印刷過程、終端用戶產業和地區分類

標籤印刷市場:按標籤格式、印刷過程、終端用戶產業和地區分類 印刷標籤:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)美國印刷標籤:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)

印刷標籤:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)美國印刷標籤:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年) 印刷標籤市場報告:按原料、印刷過程、標籤格式、最終用途行業和地區分類(2026-2034年)

印刷標籤市場報告:按原料、印刷過程、標籤格式、最終用途行業和地區分類(2026-2034年) 2026年全球印刷標籤市場報告北美印刷標籤市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

2026年全球印刷標籤市場報告北美印刷標籤市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 印刷組件和標籤(熱轉印、數位印刷、網版印刷):全球市場佔有率和排名、總收入和需求預測(2025-2031 年)日本印刷標籤市場規模、佔有率、趨勢及預測(按原料、印刷過程、標籤格式、最終用途行業和地區),2025 年至 2033 年

印刷組件和標籤(熱轉印、數位印刷、網版印刷):全球市場佔有率和排名、總收入和需求預測(2025-2031 年)日本印刷標籤市場規模、佔有率、趨勢及預測(按原料、印刷過程、標籤格式、最終用途行業和地區),2025 年至 2033 年 印刷標籤市場規模、佔有率及成長分析(依印刷製程、標籤格式、原料、最終用途產業、地區及細分市場預測),2025 年至 2032 年

印刷標籤市場規模、佔有率及成長分析(依印刷製程、標籤格式、原料、最終用途產業、地區及細分市場預測),2025 年至 2032 年 2025-2029年全球印刷標籤市場

2025-2029年全球印刷標籤市場