|

市場調查報告書

商品編碼

1910925

北美印刷標籤市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)North America Print Label - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

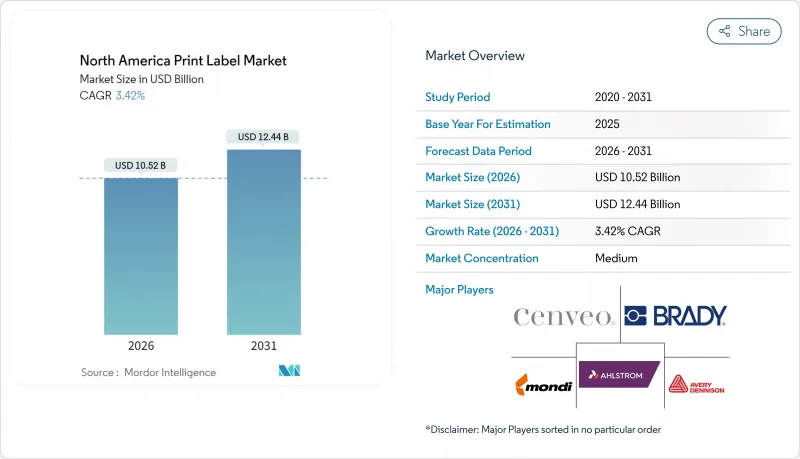

預計到 2026 年,北美印刷標籤市場規模將達到 105.2 億美元,從 2025 年的 101.7 億美元成長到 2031 年的 124.4 億美元,2026 年至 2031 年的複合年成長率為 3.42%。

這項穩定擴張反映了市場環境的日趨成熟,數位轉型、電子商務物流和永續性需求正在融合,重新定義加工商的經濟模式和終端用戶需求。可變數據工作流程的加速應用支援即時供應鏈可視性,而醫療保健產業則受美國食品藥物管理局 (FDA)主導的UDI 要求持續推動高階產品成長。墨西哥作為區域生產中心,透過製造商遷址最佳化成本結構和縮短前置作業時間,補充了美國國內市場的主導地位。儘管柔版印刷仍佔據主導地位,但噴墨技術的快速普及標誌著數位化優先營運模式的重大轉變,這種模式可以緩解勞動力短缺並減少設置廢棄物。永續性持續影響材料的選擇,隨著企業為滿足監管標準而收緊包裝目標,無底紙和生物基材越來越受歡迎。

北美印刷標籤市場趨勢與洞察

對數位印刷技術的需求日益成長

隨著原物料價格上漲和勞動力短缺導致膠印經濟效益下降,北美標籤印刷市場正在加速採用數位技術。Ricoh的數據顯示,數位排放的損益平衡點將從2010年的2000張A4紙提高到2025年的約10,000張。Canon的LabelStream LS2000(預計於2025年下半年發布)正是這一趨勢的體現,它採用高濃度水性墨水,支持FSC認證的承印物並減少VOC排放。惠普加拿大的數據顯示,在品牌對大規模客製化的需求推動下,數位印刷目前已佔感壓標籤產量的10%以上。加工商正在轉向即時生產模式,以降低庫存成本並實現高利潤的小批量訂單。這種轉變正在重塑資本配置,使模組化、可升級的噴墨平台優先於設定廢棄物高、製版成本高的類比印刷機。

電子商務物流中可變數據印刷的激增

電子商務的爆炸性成長推動了對可變資料的需求,因為配送網路需要序列化的QR碼和資料矩陣碼來實現即時追蹤。亞馬遜的包裝效率計畫推廣能夠根據庫存位置、配送路線和客戶偏好等參數動態調整的標籤。支援API的列印系統可直接與ERP和倉庫管理軟體整合,從而加快訂單到出貨的周期並降低錯誤率。品牌正在將促銷內容和會員優惠嵌入到運輸標籤中,將最後一公里配送轉變為行銷觸點。對於加工商而言,可變資料功能是其服務差異化的關鍵,並有助於在價格戰中保護其利潤。

在極低溫環境下耐久性不足

標準黏合劑在低於-40°F(約-40°C)的溫度下會發生分層,從而威脅疫苗和冷凍食品的可追溯性。採用矽膠黏合劑和PET基材的專用低溫標籤,可在低至-196 度C(約-318°F)的溫度下保持黏合力,但成本是普通替代品的2到3倍。斑馬公司的Z-Xtreme 5000T就是一個可行的解決方案,但加工商指出,運輸低利潤生鮮食品的客戶對價格非常敏感。除非價格合理的優質高性能黏合劑能夠得到更廣泛的應用,否則這項技術難題將限制低溫運輸產業在不斷成長的市場中的應用規模。

細分市場分析

到2025年,柔版印刷將佔北美印刷標籤市場37.92%的佔有率,反映出其在大批量食品飲料行業的強勢地位。同時,噴墨平台正以6.69%的複合年成長率快速成長,這標誌著隨著加工商尋求更快的換版速度、更少的印版浪費以及可變數據支持,印刷業正發生向數位化的重大轉變。受整體擁有成本(TCO)下降的推動,預計到2031年,北美噴墨印刷標籤市場規模將成長一倍以上。

混合工作流程正在興起,柔版印刷單元負責白色和局部上光,噴墨印表機頭則負責四色印刷,從而最佳化不同SKU的批量經濟性。柯達的PROSPER 7000 Turbo和FUJIFILM的Jet Press FP790均配備高速水性印刷系統,速度可達每分鐘50米,解析度為1200 dpi,縮小了與傳統模擬印刷機的生產效率差距。靜電照相印刷仍然適用於需要不透明白色和品牌標誌性金屬色的短版化妝品和保健品應用,但每平方英尺的油墨成本限制了其廣泛應用。

由於用途廣泛,到2025年,壓敏膠標籤將佔據北美印刷標籤市場36.35%的佔有率,其中無底紙標籤的複合年成長率最高,達到6.98%。電商履約中心正積極採用無底紙標籤,因為每卷標籤數量可增加40%,運輸成本降低50%;零售商也採用這種標籤形式,以支援零廢棄物的後台營運計畫。收縮和拉伸套也因創新技術的進步而發展迅速,例如CCL公司的EcoFloat聚烯套管,這種套管在標準回收過程中即可剝離,從而提高了標籤的可回收性。套模標籤在耐用消費品領域仍佔有一席之地,因為在這些領域,耐刮擦性是首要考慮因素。

帶有RFID和NFC疊加層的多聯追蹤標籤正在監管嚴格的製藥和工業領域得到應用。雖然濕膠標籤因其傳統的品牌美學而在高級啤酒和烈酒類別中繼續使用,但由於鋁罐的廣泛應用,其市場佔有率正在下降。隨著無底紙包裝的普及,壓敏膠標籤的出貨量可能在預測期中期達到峰值,這將迫使加工商拓展其應用範圍,或實施支援兩種包裝形式的自動化印刷和貼標系統。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 對數位印刷技術的需求日益成長

- 電子商務物流領域的可變資料印刷正在興起

- 轉向永續性的無襯紙和收縮套標形式

- 醫療領域強制UDI(產品識別)標籤

- 利用人工智慧實現列印工作流程自動化,以縮短交付時間

- 整合品牌保護與防偽功能

- 市場限制

- 在極低溫環境下耐久性不足

- 特殊標籤紙供應波動

- 從類比印刷機轉型為數位印刷機需要大量資金投入

- 更嚴格的VOC和油墨遷移法規將於2026年生效

- 供應鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 宏觀經濟因素如何影響市場

第5章 市場規模與成長預測

- 透過印刷技術

- 膠印

- 凹版印刷

- 柔版印刷

- 螢幕

- 凸版印刷

- 靜電照相術

- 噴墨

- 按標籤類型

- 濕膠標籤

- 壓敏膠標籤

- 無底紙標籤

- 多部分追蹤標籤

- 套模標籤

- 縮水/拉伸套

- 按基礎材料

- 紙

- 塑膠

- 金屬

- 永續生物基

- 按最終用戶行業分類

- 食物

- 飲料

- 衛生保健

- 化妝品

- 家用

- 工業的

- 物流與電子商務

- 其他終端用戶產業

- 按國家/地區

- 美國

- 加拿大

- 墨西哥

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Avery Dennison Corporation

- CCL Industries Inc.

- Multi-Color Corporation

- Brady Corporation

- Smurfit WestRock

- Mondi Group

- Ahlstrom-Munksjo Oyj

- Cenveo Worldwide Limited

- Resource Label Group

- Blue Label Packaging

- OMNI Systems Inc.

- Inovar Packaging Group

- Fort Dearborn Company

- RR Donnelley & Sons Co.

- Fortis Solutions Group

- Traco Packaging

- UPM-Raflatac

- Brook+Whittle

- Lux Global Label

- Consolidated Label Co.

第7章 市場機會與未來展望

North America print label market size in 2026 is estimated at USD 10.52 billion, growing from 2025 value of USD 10.17 billion with 2031 projections showing USD 12.44 billion, growing at 3.42% CAGR over 2026-2031.

This steady expansion reflects a maturing landscape in which digital transformation, e-commerce logistics, and sustainability mandates collectively redefine converter economics and end-user demand. Accelerating adoption of variable-data workflows supports real-time supply-chain visibility, while FDA-driven UDI requirements in healthcare sustain premium growth niches. Mexico's role as a regional production hub complements the United States' domestic dominance, as manufacturers relocate to optimize cost structures and shorten lead times. Flexography remains dominant, yet inkjet's rapid gains signal a decisive pivot toward digital-first operations that alleviate labor constraints and cut setup waste. Sustainability continues to reshape material selection, with linerless and bio-based substrates gaining traction as corporate packaging goals tighten against regulatory benchmarks.

North America Print Label Market Trends and Insights

Growing Demand for Digital Print Technologies

Digital adoption in the North America print label market accelerates as offset economics weaken under rising raw-material prices and labor shortages. Ricoh data show the digital crossover point shifting from 2,000 A4 prints in 2010 to roughly 10,000 prints in 2025. Canon's LabelStream LS2000, slated for H2 2025, exemplifies the trend with high-density aqueous inks that support FSC-compliant substrates and reduce VOC emissions. HP Canada notes digital now accounts for more than 10% of pressure-sensitive label volumes, driven by brand demand for customization at scale. Converters transition toward just-in-time models that slash inventory costs and enable premium, short-run orders with higher margins. The resulting shift restructures capital allocation, favoring modular, upgradeable inkjet platforms over analog presses with high setup waste and plate costs.

Surge in Variable Data Printing for E-commerce Logistics

Explosive e-commerce growth boosts variable-data requirements as fulfillment networks demand serialized QR and data-matrix codes for real-time tracking. Amazon's packaging-efficiency programs drive labels that adapt dynamically to inventory location, shipping route, and customer preference parameters. API-ready printing systems integrate directly with ERP and warehouse software, accelerating order-to-ship cycles and reducing error rates. Brands now embed promotional content or loyalty incentives inside shipping labels, turning the last mile into a marketing touchpoint. For converters, variable-data capability differentiates service offerings and insulates margins against commodity price competition.

Inadequate Durability in Extreme Cold-Chain Applications

Standard adhesives delaminate below -40 °F, jeopardizing traceability for vaccines and frozen food. Specialty cryogenic labels using silicone-based adhesive and PET facestocks maintain adhesion down to -196 °C but cost 2-3 times more than commodity products. Zebra's Z-Xtreme 5000T illustrates available solutions, yet converters cite price sensitivity among customers shipping low-margin perishable goods. The technical challenge limits addressable volume in cold-chain growth segments pending broader adoption of affordable, high-performance adhesives.

Other drivers and restraints analyzed in the detailed report include:

- Sustainability-Driven Switch to Linerless and Shrink-Sleeve Formats

- Healthcare UDI-Labeling Mandates

- Supply Volatility of Specialty Label-Stock Papers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Flexography captured 37.92% of the North America print label market share in 2025, reflecting its entrenched role in large-volume food and beverage lines. Inkjet platforms, however, are accelerating at a 6.69% CAGR, signaling a decisive move toward digitization as converters seek quick changeovers, reduced plate waste, and variable-data capability. The North America print label market size attached to inkjet presses is expected to more than double by 2031 as the total cost of ownership declines.

Hybrid workflows are emerging where flexo units lay white or spot varnish while inkjet heads manage four-color builds, optimizing run-length economics across SKUs. Kodak's PROSPER 7000 Turbo and Fujifilm's Jet Press FP790 exemplify high-speed, water-based systems that reach 50 m/min at 1,200 dpi, closing the productivity gap versus legacy analog machines. Electrophotography remains relevant for small-batch cosmetics and nutraceutical applications requiring opaque whites and brand-centric metallics, though ink cost per square foot limits broader adoption.

Pressure-sensitive solutions held 36.35% of the North America print label market size in 2025, owing to application versatility, but linerless alternatives are registering the fastest 6.98% CAGR. E-commerce fulfillment centers value linerless for 40% more labels per roll and 50% lower transport cost, while retailers adopt the format to meet zero-waste back-of-store initiatives. Shrink and stretch sleeves advance on recyclability innovations such as CCL's EcoFloat polyolefin sleeve, which delaminates in standard recycling processes. In-mold labels maintain a niche presence in durable consumer goods where scuff resistance is paramount.

Multi-part tracking labels supporting RFID or NFC overlays serve regulated pharma and industrial sectors. Wet-glue labels persist in premium beer and spirits categories for heritage branding aesthetics but lose share as aluminum can adoption surges. As the linerless scale improves, pressure-sensitive volumes could plateau mid-forecast, pressuring converters to diversify application portfolios or integrate print-and-apply automation that accommodates both formats.

The North America Print Label Market Report is Segmented by Printing Technology (Offset Lithography, Gravure, Flexography, Screen, and More), Label Type (Wet-Glue Labels, Pressure-Sensitive Labels, Linerless Labels, and More), Substrate Material (Paper, Plastic, and More), End-User Industry (Food, Beverage, Healthcare, Cosmetics, Household, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Avery Dennison Corporation

- CCL Industries Inc.

- Multi-Color Corporation

- Brady Corporation

- Smurfit WestRock

- Mondi Group

- Ahlstrom-Munksjo Oyj

- Cenveo Worldwide Limited

- Resource Label Group

- Blue Label Packaging

- OMNI Systems Inc.

- Inovar Packaging Group

- Fort Dearborn Company

- R.R. Donnelley & Sons Co.

- Fortis Solutions Group

- Traco Packaging

- UPM-Raflatac

- Brook + Whittle

- Lux Global Label

- Consolidated Label Co.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand for digital print technologies

- 4.2.2 Surge in variable data printing for e-commerce logistics

- 4.2.3 Sustainability-driven switch to linerless and shrink-sleeve formats

- 4.2.4 Healthcare UDI-labeling mandates

- 4.2.5 AI-enabled print workflow automation reducing turnaround time

- 4.2.6 Brand protection and anti-counterfeit features integration

- 4.3 Market Restraints

- 4.3.1 Inadequate durability in extreme cold-chain applications

- 4.3.2 Supply volatility of specialty label-stock papers

- 4.3.3 Capital-intensive transition from analog to digital presses

- 4.3.4 Stringent VOC and ink-migration regulations tightening in 2026

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Printing Technology

- 5.1.1 Offset Lithography

- 5.1.2 Gravure

- 5.1.3 Flexography

- 5.1.4 Screen

- 5.1.5 Letterpress

- 5.1.6 Electrophotography

- 5.1.7 Inkjet

- 5.2 By Label Type

- 5.2.1 Wet-glue Labels

- 5.2.2 Pressure-sensitive Labels

- 5.2.3 Linerless Labels

- 5.2.4 Multi-part Tracking Labels

- 5.2.5 In-mold Labels

- 5.2.6 Shrink and Stretch Sleeves

- 5.3 By Substrate Material

- 5.3.1 Paper

- 5.3.2 Plastic

- 5.3.3 Metallic

- 5.3.4 Sustainable bio-based

- 5.4 By End-user Industry

- 5.4.1 Food

- 5.4.2 Beverage

- 5.4.3 Healthcare

- 5.4.4 Cosmetics

- 5.4.5 Household

- 5.4.6 Industrial

- 5.4.7 Logistics and E-commerce

- 5.4.8 Other End-user Industries

- 5.5 By Country

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Avery Dennison Corporation

- 6.4.2 CCL Industries Inc.

- 6.4.3 Multi-Color Corporation

- 6.4.4 Brady Corporation

- 6.4.5 Smurfit WestRock

- 6.4.6 Mondi Group

- 6.4.7 Ahlstrom-Munksjo Oyj

- 6.4.8 Cenveo Worldwide Limited

- 6.4.9 Resource Label Group

- 6.4.10 Blue Label Packaging

- 6.4.11 OMNI Systems Inc.

- 6.4.12 Inovar Packaging Group

- 6.4.13 Fort Dearborn Company

- 6.4.14 R.R. Donnelley & Sons Co.

- 6.4.15 Fortis Solutions Group

- 6.4.16 Traco Packaging

- 6.4.17 UPM-Raflatac

- 6.4.18 Brook + Whittle

- 6.4.19 Lux Global Label

- 6.4.20 Consolidated Label Co.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

標籤印刷市場:按標籤格式、印刷過程、終端用戶產業和地區分類

標籤印刷市場:按標籤格式、印刷過程、終端用戶產業和地區分類 列印貼標及貼標設備:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印刷標籤:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)美國印刷標籤:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)

列印貼標及貼標設備:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印刷標籤:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)美國印刷標籤:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年) 印刷標籤市場報告:按原料、印刷過程、標籤格式、最終用途行業和地區分類(2026-2034年)

印刷標籤市場報告:按原料、印刷過程、標籤格式、最終用途行業和地區分類(2026-2034年) 2026年全球印刷標籤市場報告

2026年全球印刷標籤市場報告 印刷組件和標籤(熱轉印、數位印刷、網版印刷):全球市場佔有率和排名、總收入和需求預測(2025-2031 年)日本印刷標籤市場規模、佔有率、趨勢及預測(按原料、印刷過程、標籤格式、最終用途行業和地區),2025 年至 2033 年

印刷組件和標籤(熱轉印、數位印刷、網版印刷):全球市場佔有率和排名、總收入和需求預測(2025-2031 年)日本印刷標籤市場規模、佔有率、趨勢及預測(按原料、印刷過程、標籤格式、最終用途行業和地區),2025 年至 2033 年 印刷標籤市場規模、佔有率及成長分析(依印刷製程、標籤格式、原料、最終用途產業、地區及細分市場預測),2025 年至 2032 年

印刷標籤市場規模、佔有率及成長分析(依印刷製程、標籤格式、原料、最終用途產業、地區及細分市場預測),2025 年至 2032 年 2025-2029年全球印刷標籤市場

2025-2029年全球印刷標籤市場