|

市場調查報告書

商品編碼

2044201

商用廚房設備:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Commercial Kitchen Appliances - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

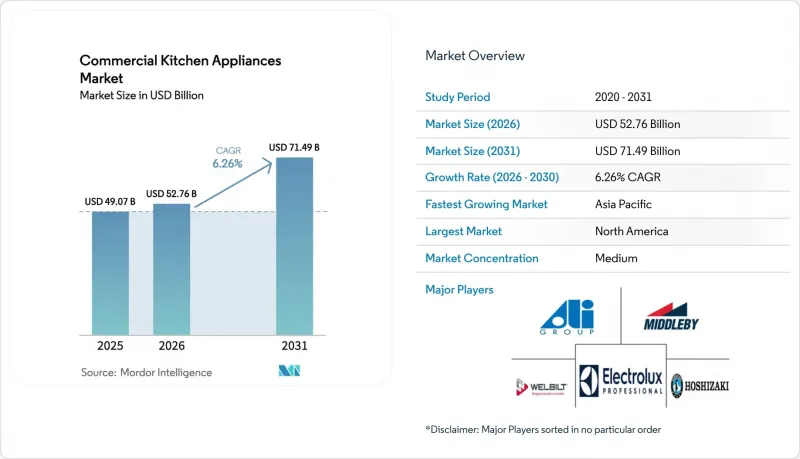

2025 年商用廚房設備市場價值為 490.7 億美元,預計到 2031 年將達到 714.9 億美元,而 2026 年為 527.6 億美元,預測期(2026-2031 年)複合年成長率為 6.26%。

企業正以多功能連網設備取代傳統設備,這些設備不僅節省空間、降低能耗,還能與集中式訂購和服務平台整合,從而減少對單一功能設備的資本投入。大型快餐連鎖店的擴張計劃持續推動強勁的需求,因為它們正在擴展標準化的、支援物聯網的後勤部門系統,從而提高處理能力並降低每筆交易的人事費用。同時,成長最快的應用領域是雲端廚房和虛擬廚房,預計到2031年將以10.32%的複合年成長率成長,因為以配送為先的企業更傾向於緊湊型、高容量的烹飪、保溫和冷藏平台。隨著大型連鎖店轉向直接採購,透過大量採購和捆綁式生命週期服務來獲得價格優勢,從而增強其應對監管和供應鏈變化的能力,分銷模式也在不斷演變。

全球商用廚房設備市場趨勢與洞察

快餐連鎖店和餐飲業正在擴張。

大型快餐公司正積極開設和整修新店,從而帶動了對烹飪、冷凍和洗碗等商用廚房設備的需求。麥當勞已增加資本支出,並制定了到2025年開設約2200家門市的計畫。為此,麥當勞計畫投入30億至32億美元的資本支出,並制定了到2027年將門市數量擴展至5萬家的多年目標,這將直接提升成熟市場和新興市場對標準化、高容量設備的需求。百勝餐飲集團(Yum! Brands)報告稱,2025年第三季度其數位銷售額達到100億美元(其中60%來自數位管道),並在同一時期創下了季度新店分店數量1131家的紀錄,這刺激了對聯網炸鍋、烤箱和廚房顯示系統(KDS)整合平台的需求。隨著營運商對更快交易速度和更低人事費用的需求不斷成長,以及跨國連鎖企業需要在其龐大的門市網路中實現一致的業績,互聯互通和自動化正在創造更高的價值。在印度和亞太地區,都市區收入的成長和人口密度的增加正推動快餐店(QSR)業態的快速擴張,這也導致商用廚房設備市場出現多年一次的設備更新週期。隨著菜單在地化進程的推進和數位化點餐趨勢的持續強勁,設備規格的製定更加注重一致性、快速恢復時間和遠端診斷功能,以最大限度地減少服務停機時間,這反過來又加強了營運商在部署新店分店對平台的選擇。

酒店業正經歷建設熱潮。

隨著飯店、度假村和服務式公寓建造的廚房不斷滿足賓客和活動的多樣化需求,飯店業的投資持續推動未來多年的設備需求。中東地區的專案活動仍然活躍,包括沙烏地阿拉伯的迪里耶開發項目,該項目正在製定大規模、分階段的烤箱、冷藏庫和大容量洗碗機採購計劃,這些計劃將與施工階段相配合,持續數年。在長期住宿設施中,廚房和共享烹飪空間的支出不斷增加,帶動了對台下式冷藏庫、小型電磁爐和高效能洗碗機的需求。在印度,國內旅遊和商務旅行的新建和整修飯店持續採用具有檢驗性能指標的節能電器,這與優先考慮使用壽命長、易於獲得零件和服務的設備的採購框架相一致。對於經營多家物業的集團公司而言,集中採購系統和標準化的廚房設計正在降低單位成本並簡化安裝流程,使供應商能夠獲得大規模的合規文件和試運行支援。在持續嚴峻的通膨和資金籌措環境下,營運商優先考慮能夠大幅降低公用事業和維護成本的設備,並且對經 ENERGY STAR 認證且具有可衡量投資回報的型號有著持續的需求。

中小企業面臨高昂的初始設備投資難題。

對於無法協商企業級折扣或優惠貸款條款的中小型企業 (SME) 而言,資金籌措管道和成本上漲仍然是限制其發展的結構性因素。加拿大的一項調查數據顯示,69% 的中小型企業表示設備成本是其資本投資的限制因素,50% 的企業表示現金流緊張,47% 的企業表示借貸成本高。此外,65% 的企業仍背負著平均 10.8 萬美元的疫情相關債務,這給新設備的預算帶來了壓力。貸款標準的提高和嚴格使得企業更難購買投資回報明確的設備,以及需要大量前期投入的節能型和物聯網設備。印度的獨立餐廳和雲端廚房新創公司也面臨類似的預算調整,因為它們的設備需求已從基本的烹飪設備擴展到包括冷凍、洗碗和溫度記錄硬體等,以滿足食品安全標準。因此,企業通常會根據設備的重要性和投資回收期分階段進行升級,導致升級週期延長。未來,降低初始成本的創新資金籌措方式和供應商服務方案可能會加速商用廚房設備市場的普及。

細分市場分析

預計到2025年,冷藏庫將佔據34.36%的市場佔有率,成為產品組合中的領頭羊。這反映了餐飲服務業多年來對步入冷藏庫、延伸式冷藏庫和台下式冷藏庫的持續更換需求。烹飪設備預計到2031年將以8.24%的複合年成長率成長,這主要得益於市場對高效炸鍋、煎鍋和多功能組合烤箱的需求,這些設備面積小巧,功能齊全。對於商用蒸氣烹飪鍋和洗碗機等設備而言,高效能仍然是採購的關鍵因素,因為它們能夠顯著降低年度能源和用水量,並改善門市的經濟效益。由於電氣化措施和建築規範的推動,後廚新計畫紛紛採用全電動配置,因此電磁加熱烤箱和先進烤箱更受青睞。在空氣品質和安全至關重要的印度大都會圈,這種做法正日益受到支持。此外,基於感測器和雲端連接的產品生態系統支援多地點企業監控溫度曲線、庫存管理和維護週期,有助於提高商用廚房設備市場中所有設備的合規性和運轉率。

產品選擇越來越取決於具體情況,麵包店、餐飲服務、快餐店和商用廚房對加工能力、一致性和易維護性的重點各不相同。結合微波和衝擊式加熱技術的高速烤箱滿足了外帶需求的激增,而強大的對流式烤箱已成為批量加工的必備設備。獲得能源之星認證的洗碗機能夠降低能源和水的消耗,這對於水資源匱乏地區的設施至關重要,因為這些地區的收費系統會因用水量的激增而增加成本。在預測期內,隨著整合控制系統縮短培訓時間並提高可重複性,烹飪設備預計將在商用廚房設備市場中獲得更大的市場佔有率。在印度,同時提供店內飲食和外賣服務的連鎖餐廳正在標準化相容的製冷和加熱設備組合,從而實現了商用廚房設備行業不同業態之間零件、培訓和服務流程的通用。

區域分析

2025年,北美地區佔全球銷售額的26.38%。這反映了該地區在多地點餐飲系統方面的雄厚基礎,以及互聯節能設備的廣泛應用。政策因素將持續影響採購模式至2026年,因為美國《AIM法案》限制了高全球暖化潛勢(GWP)冷媒的使用,並強制要求對大容量系統實施更嚴格的洩漏偵測和維修規程。這推動了餐飲服務業對冰箱和步入式冷藏庫設備更換需求的成長。在加拿大,中小企業持續面臨融資困難和疫情帶來的債務負擔,這降低了它們進行大額前期投資的意願。因此,它們對融資和服務主導模式的興趣仍然濃厚。該地區的法規結構和食品安全標準也在推動性能成熟、具備日誌記錄功能的設備的普及。中期來看,這些因素將持續支撐商用廚房設備市場穩定的更換和升級需求。

亞太地區是成長最快的地區,預計到2031年複合年成長率將達到6.87%。這主要得益於中國、印度和東南亞地區對設備需求的不斷成長,而這種成長又都市化、收入成長以及快餐店(QSR)和外賣模式擴張的推動。全球連鎖擴張勢頭依然強勁,百勝餐飲集團(Yum! Brands)報告稱,全球新增門市數以千計,其中許多集中在亞太地區。不斷成長的線上訂單量也推動了對大容量設備的需求。在印度,二、三線城市的快速發展帶動了對符合食品安全標準的標準化烹飪設備套裝以及具備溫度記錄功能的可靠冷凍設備的需求。設備的選擇也反映了當地法規和電氣化的發展趨勢,電磁爐因其安裝快速、控溫穩定等優勢,在都市區廚房中越來越受歡迎。這些趨勢為提高單店設備採用率和最佳化整個商用廚房設備市場的更新換代週期奠定了基礎。

歐洲、中東和非洲的變革步伐各不相同。歐洲營運商正在適應能源成本上漲和修訂後的氟化氣體法規,這些法規鼓勵在新系統和維修系統中過渡到天然冷媒。歐洲零售冷凍產業已經普遍採用二氧化碳和碳氫化合物解決方案,飯店業者正在利用這些專業知識,為食品服務提供冷藏和延伸式冷藏庫。在中東,沙烏地阿拉伯的迪里耶專案等大型開發案正在形成多年的採購週期和密集的安裝計劃,這些計劃將大量廚房設備引入酒店和綜合用途設施。雖然非洲的需求基礎仍然不均衡,但一些關鍵地區正在發展分銷基礎設施,以支持區域擴張。在整個歐洲、中東和非洲地區,永續性、合規性和全生命週期的可維護性是商用廚房設備市場供應商選擇的核心,這些因素將繼續影響設備更換時間和產品組合的選擇。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 速食連鎖店和餐飲服務業的擴張

- 飯店業的建設熱潮

- 節能型物聯網廚房

- 雲端廚房/幽靈廚房的興起

- 維修天然冷媒

- 對多功能緊湊型單元的需求

- 市場限制因素

- 中小企業 (SME) 面臨著高額初始資本支出 (CAPEX) 的困境。

- 處理複雜的安全和消防安全認證工作充滿挑戰。

- 電子元件供應鏈正受到供不應求。

- 能源價格波動劇烈。

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的競爭

- 洞察最新市場趨勢與創新

- 洞察近期市場趨勢(新產品發布、策略性舉措、投資、合作、合資、業務擴張、併購等)

第5章 市場規模與成長預測

- 按類型

- 冷藏庫

- 無需預約

- 伸手進去

- 台下式及備餐檯

- 烹飪用具

- 傳單

- 煎板和木炭烤架

- 汽船

- 爐灶/烹飪爐灶

- 氣體

- 電

- 就職

- 烤箱

- 對流

- 合成的

- 高速

- 洗碗機

- 櫃檯下

- 輸送機

- 隔熱/宴會設備

- 食品烹飪設備

- 智慧型互聯設備

- 冷藏庫

- 透過使用

- 速食店(QSR)

- 全方位服務餐廳 (FSR)

- 雲端廚房/幽靈廚房

- 公司食堂

- 度假村和飯店

- 醫院和醫療保健

- 鐵路餐廳

- 餐飲服務

- 透過分銷管道

- 直接從製造商購買

- 銷售代理/銷售公司

- 按地區

- 北美洲

- 加拿大

- 美國

- 墨西哥

- 南美洲

- 巴西

- 秘魯

- 智利

- 阿根廷

- 南美洲其他地區

- 亞太地區

- 印度

- 中國

- 日本

- 澳洲

- 韓國

- 東南亞(新加坡、馬來西亞、泰國、印尼、越南、菲律賓)

- 亞太其他地區

- 歐洲

- 英國

- 德國

- 法國

- 西班牙

- 義大利

- 比荷盧經濟聯盟(比利時、荷蘭、盧森堡)

- 北歐國家(丹麥、芬蘭、冰島、挪威、瑞典)

- 其他歐洲國家

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 奈及利亞

- 其他中東和非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Ali Group

- Electrolux Professional

- Middleby Corporation

- Hoshizaki Corporation

- Welbilt(Manitowoc)

- Carrier Commercial Refrigeration

- Rational AG

- Meiko International

- Duke Manufacturing Co.

- Vulcan

- Hobart

- Hamilton Beach Commercial

- Alto-Shaam

- True Manufacturing

- Turbo Air

- Southbend

- Fagor Group

- Falcon Foodservice Equipment

- Interlevin Refrigeration Ltd

- The Vollrath Company

- Panasonic Commercial

- Garland(Welbilt)

- Blodgett

第7章 市場機會與未來展望

The commercial kitchen appliances market size was valued at USD 49.07 billion in 2025 and is estimated to grow from USD 52.76 billion in 2026 to reach USD 71.49 billion by 2031, at a CAGR of 6.26% during the forecast period (2026-2031).

Operators continue to replace legacy setups with multifunctional, connected appliances that reduce space, lower energy costs, and sync with centralized order and service platforms, which is shifting capital allocation away from single-function equipment. Expansion programs by leading quick-service chains remain a strong demand anchor as chains scale standardized, IoT-ready back-of-house systems that raise throughput and compress labor per transaction. In parallel, the fastest-growing application segment is cloud and ghost kitchens, which are on track for a 10.32% CAGR through 2031 as delivery-first formats favor compact, high-throughput cooking, holding, and refrigeration platforms. Distribution models are also evolving as large chains shift to direct procurement to secure volume pricing and bundled lifecycle services, supporting higher resilience to regulatory and supply changes.

Global Commercial Kitchen Appliances Market Trends and Insights

QSR Chains and Out-of-Home Dining are Expanding

Large quick-service companies are executing aggressive new-unit builds and remodels that sustain commercial kitchen purchasing across cooking, refrigeration, and warewashing categories. McDonald's lifted capital expenditures and outlined plans consistent with the opening of around 2,200 restaurants in 2025, supported by a USD 3.0-3.2 billion capex range and a multi-year goal of scaling to 50,000 locations by 2027, which directly raises demand for standardized, high-throughput equipment in both mature and developing markets. Yum! Brands reported USD 10 billion in digital sales for Q3 2025 with a 60% digital mix, while achieving a quarterly record of 1,131 gross new units in the period, creating procurement momentum for connected fryers, ovens, and KDS-integrated platforms. Connectivity and automation now command a premium as operators seek faster throughput and lower labor per transaction, and as multi-country chains require uniform outcomes across a broad store base. In India and across the Asia-Pacific, rising urban incomes and dense catchment areas enable QSR formats to scale unit counts quickly, which anchors multi-year equipment replacement cycles within the commercial kitchen appliances market. As menus localize and digital order flows remain elevated, equipment specifications prioritize consistency, rapid recovery times, and remote diagnostics that reduce service downtimes, reinforcing platform choices that operators carry into successive waves of openings.

Hospitality Sector Is Witnessing a Construction Boom

Hospitality capital expenditure continues to create multi-year equipment demand as hotels, resorts, and serviced apartments build kitchens suited to varied guest and event needs. Project flows in the Middle East, including Saudi Arabia's Diriyah development, remain significant and translate into large, staged procurement schedules for ovens, refrigerators, and high-capacity dishwashers across several years to match construction phasing. Extended-stay properties allocate proportionally higher spend on kitchenettes and communal prep spaces, increasing demand for undercounter refrigeration, compact induction hobs, and efficient warewashing. In India, new and upgraded hotel properties tied to domestic tourism and business travel continue to specify energy-saving appliances with verified performance metrics, aligning with procurement frameworks that favor long-life equipment with ready access to parts and service. For multi-property groups, centralized purchasing and template kitchen designs compress unit costs and tighten installation schedules, which benefits vendors able to deliver compliance documentation and commissioning support at scale. As inflation and financing conditions remain tight, operators prioritize equipment choices with clear utility and maintenance savings, maintaining a steady preference for ENERGY STAR-qualified models that demonstrate measurable paybacks.

SMEs Grapple with High Upfront Capex

Capital access and cost inflation remain structural constraints for small and midsize operators that cannot negotiate enterprise-level discounts or favorable lending terms. Survey data in Canada indicate that 69% of SMEs identify equipment costs as a deterrent to capital investment, 50% cite cash-flow constraints, and 47% point to high borrowing costs, while 65% continue to manage pandemic-related debt that averages USD 108,000, which crowds out new-equipment budgets. Higher funding thresholds and stricter underwriting standards elevate the hurdle for energy-efficient or IoT-enabled equipment purchases that offer clear paybacks but require upfront cash. Independent restaurants and cloud-kitchen start-ups in India face similar budget balancing as equipment needs expand beyond basic cooking to include refrigeration, warewashing, and temperature-logging hardware that satisfies food-safety practices. As a result, operators often phase equipment upgrades based on criticality and return horizon, which elongates replacement cycles. Over time, financing innovations and vendor service bundles that reduce upfront payments can improve adoption within the commercial kitchen appliances market.

Other drivers and restraints analyzed in the detailed report include:

- Kitchens are Becoming Energy-Efficient And Iot-Enabled

- Cloud And Ghost Kitchens are on the Rise

- Navigating Complex Safety and Fire Certifications Proves Challenging

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Refrigerators led the type mix with 34.36% market share in 2025, reflecting the sustained replacement needs for walk-ins, reach-ins, and undercounter units in longstanding foodservice operations. Cooking appliances are forecast to advance at 8.24% CAGR through 2031 on the strength of high-efficiency fryers, griddles, and combi platforms that concentrate multi-function capability within smaller footprints. Verified efficiency remains central to procurement, as equipment like commercial steam cookers and dishwashers delivers measurable annual energy and water savings that improve site-level economics. Induction and advanced ovens are prioritized where electrification agendas and building codes steer new projects toward all-electric back-of-house configurations, an approach that is gaining traction in dense Indian metros that prioritize air quality and safety. Product ecosystems built around sensors and cloud connectivity also help multi-unit operators monitor temperature profiles, cycle counts, and service intervals, tightening compliance and uptime across fleets within the commercial kitchen appliances market.

Product choice is increasingly context-specific, with bakery, catering, QSR, and institutional kitchens placing different weights on throughput, consistency, and maintenance access. High-speed oven variants that combine microwave and impingement technologies support delivery surges, while robust convection units remain staples for batch processes. ENERGY STAR-qualified dishwashers reduce both energy and water, which is relevant for facilities in water-stressed regions where tariff structures penalize usage spikes. Over the forecast period, cooking appliances are positioned to capture a rising share of the commercial kitchen appliances market as integrated controls shorten training time and improve repeatability. In India, chains that balance dine-in and delivery channels increasingly standardize on compatible refrigeration and hot-side packages so parts, training, and service procedures remain common across formats in the commercial kitchen appliances industry.

The Commercial Kitchen Appliances Market Report is Segmented by Type (Refrigerators, Cooking Appliances, Cooktops & Cooking Ranges, and More), Application (QSR, FSR, Cloud/Ghost Kitchens, and More), Distribution Channel (Direct From the Manufacturers and Dealers/Distributors), and Geography (North America, South America, Asia-Pacific, Europe, Middle East, and Africa). Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America accounted for 26.38% of global revenue in 2025, reflecting the region's strong base of multi-unit restaurant systems and broad adoption of connected, energy-efficient equipment. Policy drivers will continue to influence purchasing patterns through 2026, as the U.S. AIM Act limits high-GWP refrigerants and mandates stricter leak detection and repair protocols for large-charge systems, which increases replacement activity in foodservice cold rooms and walk-ins. In Canada, small and midsize enterprises report ongoing capital constraints and pandemic-era debt burdens that reduce appetite for large upfront purchases, which keeps interest in financing and service-led models elevated. The region's regulatory frameworks and food-safety codes also reinforce the adoption of equipment with verified performance and logging features. Over the medium term, these factors sustain a steady base of replacements and upgrades within the commercial kitchen appliances market.

Asia-Pacific is the fastest-growing region with a projected 6.87% CAGR through 2031 as urbanization, rising incomes, and expanding QSR and delivery-first formats deepen equipment demand across China, India, and Southeast Asia. Expansion by global chains has been robust, with Yum! Brands reporting thousands of net new units globally, many in Asia-Pacific, alongside rising digital order volumes that require throughput-focused equipment. In India, growth in Tier-2 and Tier-3 cities is elevating demand for standardized hot-side packages and reliable cold storage with temperature logging to meet food-safety practices. Equipment selection also reflects local codes and electrification trajectories, with induction gaining exposure in urban kitchens that benefit from faster installs and consistent heat control. These trends underpin increasing equipment penetration per site and steadier replacement cycles across the commercial kitchen appliances market.

Europe, the Middle East, and Africa show mixed momentum, with European operators adapting to energy costs and updated F-gas rules that push toward natural refrigerants in new and retrofit systems. The shift to CO2 and hydrocarbon solutions is now well established in European retail refrigeration, and hospitality operators are drawing on those learnings for foodservice cold rooms and reach-ins. In the Middle East, mega-developments such as Saudi Arabia's Diriyah project are shaping multi-year procurement cycles and concentrated installation programs that absorb large volumes of kitchen equipment across hotels and mixed-use venues. Africa's demand base remains uneven, though key hubs are developing distribution infrastructure that supports regional rollouts. Across EMEA, sustainability, compliance, and lifecycle serviceability remain central to supplier selection in the commercial kitchen appliances market and will continue to drive replacement timing and product mix choices.

- Ali Group

- Electrolux Professional

- Middleby Corporation

- Hoshizaki Corporation

- Welbilt (Manitowoc)

- Carrier Commercial Refrigeration

- Rational AG

- Meiko International

- Duke Manufacturing Co.

- Vulcan

- Hobart

- Hamilton Beach Commercial

- Alto-Shaam

- True Manufacturing

- Turbo Air

- Southbend

- Fagor Group

- Falcon Foodservice Equipment

- Interlevin Refrigeration Ltd

- The Vollrath Company

- Panasonic Commercial

- Garland (Welbilt)

- Blodgett

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of QSR chains & out-of-home dining

- 4.2.2 Hospitality construction boom

- 4.2.3 Energy-efficient & IoT-enabled kitchens

- 4.2.4 Rise of cloud/ghost kitchens

- 4.2.5 Natural-refrigerant retrofits

- 4.2.6 Demand for multi-function compact units

- 4.3 Market Restraints

- 4.3.1 Smes Grapple with High Upfront CAPEX

- 4.3.2 Navigating Complex Safety and Fire Certifications Proves Challenging

- 4.3.3 Shortages Plague the Electronics Supply Chain

- 4.3.4 Energy Prices Experience Notable Volatility

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Insights into the Latest Trends and Innovations in the Market

- 4.7 Insights on Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, etc.) in the Market

5 Market Size & Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Refrigerators

- 5.1.1.1 Walk-in

- 5.1.1.2 Reach-in

- 5.1.1.3 Undercounter & Prep-table

- 5.1.2 Cooking Appliances

- 5.1.2.1 Fryers

- 5.1.2.2 Griddles & Charbroilers

- 5.1.2.3 Steamers

- 5.1.3 Cooktops & Cooking Ranges

- 5.1.3.1 Gas

- 5.1.3.2 Electric

- 5.1.3.3 Induction

- 5.1.4 Ovens

- 5.1.4.1 Convection

- 5.1.4.2 Combi

- 5.1.4.3 High-speed

- 5.1.5 Dishwashers

- 5.1.5.1 Undercounter

- 5.1.5.2 Conveyor

- 5.1.6 Heated Holding & Banquet Equipment

- 5.1.7 Food-Preparation Equipment

- 5.1.8 Smart Connected Equipment

- 5.1.1 Refrigerators

- 5.2 By Application

- 5.2.1 Quick-Service Restaurants (QSR)

- 5.2.2 Full-Service Restaurants (FSR)

- 5.2.3 Cloud / Ghost Kitchens

- 5.2.4 Institutional Canteens

- 5.2.5 Resorts & Hotels

- 5.2.6 Hospitals & Healthcare

- 5.2.7 Railway Dining

- 5.2.8 Catering Services

- 5.3 By Distribution Channel

- 5.3.1 Direct from the Manufacturers

- 5.3.2 Dealers/Distributors

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 Canada

- 5.4.1.2 United States

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Peru

- 5.4.2.3 Chile

- 5.4.2.4 Argentina

- 5.4.2.5 Rest of South America

- 5.4.3 Asia-Pacific

- 5.4.3.1 India

- 5.4.3.2 China

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- 5.4.3.7 Rest of Asia Pacific

- 5.4.4 Europe

- 5.4.4.1 United Kingdom

- 5.4.4.2 Germany

- 5.4.4.3 France

- 5.4.4.4 Spain

- 5.4.4.5 Italy

- 5.4.4.6 BENELUX (Belgium, Netherlands, Luxembourg)

- 5.4.4.7 NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- 5.4.4.8 Rest of Europe

- 5.4.5 Middle East and Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 South Africa

- 5.4.5.4 Nigeria

- 5.4.5.5 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Ali Group

- 6.4.2 Electrolux Professional

- 6.4.3 Middleby Corporation

- 6.4.4 Hoshizaki Corporation

- 6.4.5 Welbilt (Manitowoc)

- 6.4.6 Carrier Commercial Refrigeration

- 6.4.7 Rational AG

- 6.4.8 Meiko International

- 6.4.9 Duke Manufacturing Co.

- 6.4.10 Vulcan

- 6.4.11 Hobart

- 6.4.12 Hamilton Beach Commercial

- 6.4.13 Alto-Shaam

- 6.4.14 True Manufacturing

- 6.4.15 Turbo Air

- 6.4.16 Southbend

- 6.4.17 Fagor Group

- 6.4.18 Falcon Foodservice Equipment

- 6.4.19 Interlevin Refrigeration Ltd

- 6.4.20 The Vollrath Company

- 6.4.21 Panasonic Commercial

- 6.4.22 Garland (Welbilt)

- 6.4.23 Blodgett

7 Market Opportunities & Future Outlook

- 7.1 Rapid expansion of quick-service restaurants (QSRs)

商用廚房設備及設施市場:2026-2032年全球市場預測(依產品類型、技術、動力來源、最終用戶及銷售管道)

商用廚房設備及設施市場:2026-2032年全球市場預測(依產品類型、技術、動力來源、最終用戶及銷售管道) 商用廚房刀具市場:市場規模、佔有率和趨勢分析(按刀片類型、類別、應用和地區分類),基於細分市場的預測(2026-2033 年)

商用廚房刀具市場:市場規模、佔有率和趨勢分析(按刀片類型、類別、應用和地區分類),基於細分市場的預測(2026-2033 年) 客製化單元市場報告:按類型、最終用戶和地區分類(2026-2034 年)

客製化單元市場報告:按類型、最終用戶和地區分類(2026-2034 年) 二手二手設備市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、最終用途、分銷管道、地區和競爭格局分類,2021-2031年客製化單元市場:按單元類型、客製化程度、材料類型、設計風格、最終用戶和分銷管道分類-2026-2032年全球市場預測商用麵包切片機市場:依動力來源、類型、最終用戶和分銷管道分類-2026-2032年全球市場預測超超臨界壓力裝置市場:依壓力等級、燃料類型、容量、裝置類型、計劃狀態和應用分類-全球預測,2026-2032年

二手二手設備市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、最終用途、分銷管道、地區和競爭格局分類,2021-2031年客製化單元市場:按單元類型、客製化程度、材料類型、設計風格、最終用戶和分銷管道分類-2026-2032年全球市場預測商用麵包切片機市場:依動力來源、類型、最終用戶和分銷管道分類-2026-2032年全球市場預測超超臨界壓力裝置市場:依壓力等級、燃料類型、容量、裝置類型、計劃狀態和應用分類-全球預測,2026-2032年 2026-2030年全球商用廚房刀具市場商用廚房設備市場規模、佔有率、趨勢及預測(按類型、通路、應用及地區分類),2026-2034年

2026-2030年全球商用廚房刀具市場商用廚房設備市場規模、佔有率、趨勢及預測(按類型、通路、應用及地區分類),2026-2034年 2026年全球二手餐飲設備市場報告

2026年全球二手餐飲設備市場報告