|

市場調查報告書

商品編碼

2044138

汽車自我調整照明系統:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)Automotive Adaptive Lighting System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

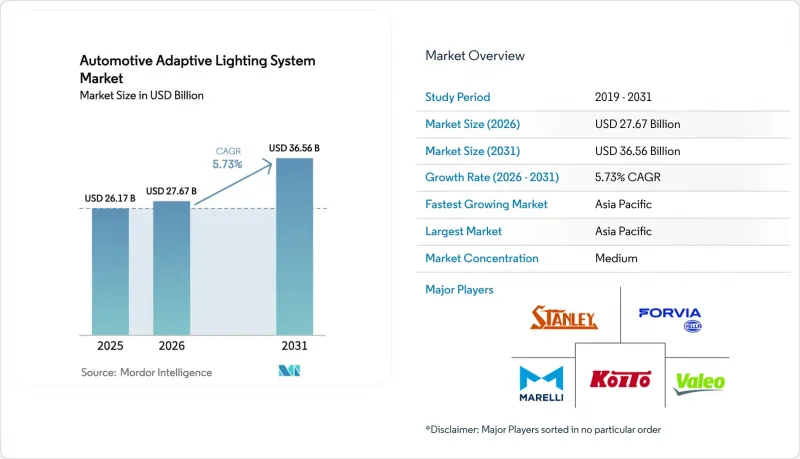

預計汽車自我調整照明系統市場將從 2025 年的 261.7 億美元成長到 2026 年的 276.7 億美元,到 2031 年達到 365.6 億美元,2026 年至 2031 年的複合年成長率為 5.73%。

歐洲和北美監管政策變化的同步進行,消除了過去阻礙先進光束技術普及的碎片化開發成本,加速了全球平台的部署。汽車製造商將高解析度頭燈與空中升級功能相結合,使其能夠在車輛的整個生命週期中持續銷售功能升級,從而建立新的、持續的收入來源。供應商正在墨西哥、波蘭、土耳其和泰國等地快速實現LED、雷射和微型LED模組的本地化生產,以降低外匯風險和運輸延誤的影響。軟體定義照明技術正從豪華汽車品牌擴展到普通車輛的安全功能,其整合的感測器和人工智慧演算法能夠根據交通狀況、地形和天氣狀況即時調整光束模式。

全球汽車自我調整照明系統市場趨勢及洞察

全球更嚴格的照明法規(亞洲開發銀行、歐洲經濟委員會 R123)

美國於2022年將自我調整遠光燈合法化,結束了數十年來對該功能的監管,並使其符合歐洲ECE R123標準。這項監管一致性將使汽車製造商能夠透過軟體微調光束模式來滿足不同地區的亮度要求,同時使用單一硬體堆疊即可獲得多區域認證。中國的GB 4599-2024及相關法規於2025年生效,明確核准了道路投影符號,並為車道引導和行人警告鋪平了道路。印度已認證了符合歐洲光學設計的國產主動式轉向頭燈,並表示計劃在2027年前強制卡車配備該功能。這些措施將共同擴大供應商的潛在市場規模,促進規模經濟,並加速對像素化LED和晶片雷射陣列的投資。

對先進安全系統和ADAS的需求日益成長

汽車照明不再只是光源,它現在還兼具外部感測器的功能。梅賽德斯-奔馳已將自我調整光束整合到其主動煞車輔助系統中,使車燈能夠在雷達或攝影機偵測到危險時主動照亮道路上的弱勢群體。博斯正在將第三代(Gen3)多功能攝影機與重型卡車的頭燈相結合,以降低夜間事故率,這對車隊保險公司來說是一項重大利好。隨著汽車製造商將照明系統與煞車、轉向和感知ECU更深入地整合,買家實際上被束縛在擁有整套技術堆疊的一級供應商手中。此外,基於訂閱的空中下載(OTA)照明昇級方案的前景,使得自我調整照明成為未來產品規劃中的重中之重。

自我調整模組和固定燈具的初始成本差異

自我調整頭燈的成本仍然是固定式LED大燈的兩到四倍,因此汽車製造商通常會將其與高級配置或付費軟體解鎖捆綁銷售。以2026號BMW3係為例,自我調整環境照明選配會使車輛價格增加約1,850歐元(約2,135.15美元),這限制了其在價格敏感型市場的普及。經銷商提供的售後改裝維修也很少見,因為額外的線路會使電氣保固失效,從而有效地堵死了快速升級的途徑。一些供應商現在提供分級包裝方案,將昂貴的MEMS後視鏡與基本的自動遠光燈邏輯分開,使入門車型能夠在不大幅漲價的情況下滿足新的法規要求。

細分市場分析

2025年,乘用車在汽車自我調整照明市場中維持了73.76%的最大市場佔有率。這主要得益於車型年度的持續更新,例如矩陣式LED和像素式LED已成為中型跨界車的標配。由於汽車製造商將這些照明系統作為資訊娛樂系統升級的一部分進行銷售,消費者不再將其視為昂貴的獨立選配件,而是將其視為舒適性和安全性一體化解決方案的一部分。 SUV車型更大的造型自由度也為設計師提供了更多空間來安裝散熱器和感測器,這進一步推動了自適應照明技術的快速普及。隨著產量的增加,一級供應商受益於規模經濟,透過共用電子平台降低了每個模組的成本並提高了可靠性。

預計到2031年,中型和重型商用車市場將呈現最高的成長率,複合年成長率(CAGR)將達到9.62%,主要得益於法規要求長途卡車必須配備自我調整遠光燈和碰撞緩解煞車系統。車隊營運商願意承擔額外的成本,因為提高夜間能見度可以減少因事故造成的運作並降低保險費用。燈具製造商現在提供可滑入現有開口的模組化燈罩,使卡車能夠在日常維護期間進行升級,而無需重新噴漆周圍的面板。這種維修途徑將加速技術的普及,並在製造商保固期結束後為供應商提供第二個收入來源。

到2025年,外部照明系統將佔據93.22%的市場。這反映了全球法規強制要求所有新車配備防眩光光束和日行燈。汽車製造商正朝著單一的、可透過軟體調節的全球通用燈具架構發展,從而最大限度地減少區域模具的變更。這項策略縮短了開發週期,使設計團隊能夠專注於提升品牌形象的獨特設計。因此,供應商之間的競爭將不再局限於基本的法規遵循性,而是圍繞著溫度控管和光學效率。

車載自我調整照明是成長最快的細分市場,複合年成長率高達 8.27%,這主要得益於電動車和自動駕駛汽車利用顏色和亮度變化向車內乘客提供回饋,而非引擎噪音。這些以車內為中心的系統與語音助理和生物識別感測器協同工作,根據駕駛員的情緒和駕駛條件調整照明場景。軟體更新允許添加新的主題,類似於智慧型手機壁紙,從而為汽車製造商創造持續的收入來源。隨著車載螢幕數量的增加,環境LED 燈透過調整整體亮度來減輕眼睛疲勞。

區域分析

預計到2025年,亞太地區將佔汽車自我調整照明銷量的45.55%,並在2031年之前以8.91%的複合年成長率成長。這主要得益於中國快速發展的法規,這些法規認可了道路投射能力。國內品牌正將自我調整光束作為電動車車型的標配,這些車型直接與德國豪華進口車競爭。日本供應商如小糸工業株式會社和史丹利正在東協和拉丁美洲擴建工廠,以緊跟全球汽車平臺並避免外匯波動風險。印度正在崛起成為下一個轉捩點市場。印度擁有反映歐洲光學標準的照明標準,為其從2027年起強制實施卡車照明系統鋪平了道路。

歐洲保持其技術領先地位,預計到2031年將繼續以4.49%的複合年成長率穩定成長。 ECE R123標準對無眩光性能設定了高標準,促使所有新平台採用矩陣式LED和雷射照明。德國豪華汽車製造商正逐步在售價低於4萬歐元(約4,6178.20美元)的車型中採用高解析度車燈,這意味著大眾汽車品牌必須採用類似技術,要麼將面臨市場佔有率流失的風險。隨著供應商將組裝廠轉移到工資水平較低的波蘭、匈牙利和摩洛哥,生產成本正在降低,但在物流方面,嚴格遵守向歐盟工廠交付的期限仍然是重中之重。

在北美,隨著美國國家公路交通安全管理局 (NHTSA)核准自我調整遠光燈,積壓已久的市場需求終於得以釋放。儘管 2031 年 4.78% 的複合年成長率 (CAGR) 看起來並不高,但考慮到數十年的禁令,其基數仍然很小。特斯拉主導透過空中下載 (OTA) 功能推送至現有車輛,顯示潛在的用戶群體已經相當龐大。供應商正在墨西哥本地化微型 LED 生產線,以縮短交貨前置作業時間,並利用美墨加協定 (USMCA) 的原產地規則。南美和中東地區也正在效法。此次銷售成長主要來自以 SUV 為主的產品線,消費者願意為這些功能支付溢價,但照明法規的不嚴格性仍然限制了全矩陣大燈系統的全面普及。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 全球更嚴格的照明法規(亞洲開發銀行、歐洲經濟委員會 R123)

- 對先進安全系統和ADAS的需求日益成長

- 高檔轎車和SUV銷量的成長推高了裝備率。

- LED成本快速降低和效能提升

- 售後可透過OTA升級波束模式。

- V2X行人用通訊照明

- 市場限制因素

- 自我調整模組和固定燈具的初始成本比較

- 高流明LED/雷射單元的溫度控管局限性

- 透過 CAN-FD 閘道器傳輸的 ECU 的網路安全風險(一個被忽視的問題)

- 雷射二極體用氮化鎵基板供應瓶頸(一個被忽視的趨勢)

- 價值/供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的競爭

第5章:市場規模及成長預測(價值(美元)及數量(單位))

- 按車輛類型

- 搭乘用車

- 輕型商用車(LCV)

- 中型重型商用車(MHCV)

- 透過使用

- 外部照明

- 室內照明

- 依組件類型

- 控制器

- 感應器/攝影機

- 燈具組件

- 執行器

- 其他

- 透過技術

- LED

- 氙氣燈/HID燈

- 鹵素

- 雷射照明

- 透過分銷管道

- OEM

- 售後市場

- 按功能

- 自動遠光燈

- 動態彎曲燈光

- 彎道照明燈

- 主動式轉向頭燈

- 按地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 亞太其他地區

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 土耳其

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Hella GmbH & Co. KGaA

- Valeo SA

- Koito Manufacturing Co., Ltd.

- Stanley Electric Co., Ltd.

- OSRAM Continental GmbH

- Marelli Automotive Lighting

- Lumileds Holding BV

- Hyundai Mobis Co., Ltd.

- Panasonic Automotive Systems

- ZKW Group

- JW Speaker Corporation

- Denso Corporation

- Varroc Lighting Systems

- Signify NV(Philips Automotive)

- Renesas Electronics Corporation

- Texas Instruments Incorporated

- Aptiv PLC

- Bosch Mobility

- Continental AG

- Lear Corporation

- Infineon Technologies AG

第7章 市場機會與未來展望

The automotive adaptive lighting market size is expected to increase from USD 26.17 billion in 2025 to USD 27.67 billion in 2026 and reach USD 36.56 billion by 2031, growing at a CAGR of 5.73% over 2026-2031.

Near-synchronous regulatory changes in Europe and North America are erasing the split-engineering costs that once slowed the rollout of advanced beams, enabling global platforms to scale faster. Automakers are pairing high-resolution headlamps with over-the-air functionality so that feature upgrades can be sold long after the initial vehicle purchase, supporting new recurring-revenue streams. Suppliers are racing to localize production of LED, laser, and micro-LED modules in Mexico, Poland, Turkiye, and Thailand to blunt currency risk and shipping delays. Software-defined lighting is moving from luxury branding to mainstream safety, with embedded sensors and AI algorithms constantly adjusting beam shape in real time based on traffic, terrain, and weather.

Global Automotive Adaptive Lighting System Market Trends and Insights

Stringent Global Lighting Regulations (ADB, ECE R123)

The United States legalized adaptive driving beams in 2022, aligning with Europe's ECE R123 and ending decades of suppression of the feature. This convergence lets automakers certify one hardware stack for multiple regions while fine-tuning beam patterns in software to satisfy each local photometric clause. China's GB 4599-2024 and companion rules came into force in 2025 with explicit approval for road-projection symbols, opening the door for lane guidance and pedestrian alerts. India validated a home-grown adaptive front lighting design that mirrors European optics, signaling an intent to mandate the feature on trucks by 2027. Together, these moves increase the addressable volume for suppliers, spur economies of scale, and accelerate investments in pixelated LEDs and laser-on-chip arrays.

Growing Demand for Advanced Safety Systems and ADAS

Automotive lighting now serves as an outward-facing sensor, not just illumination. Mercedes-Benz embedded adaptive beams into Active Brake Assist so the lamps actively highlight vulnerable road users when radar or camera flags a threat. Bosch pairs its Gen3 multi-purpose camera with headlamps on heavy trucks to shrink nighttime crash rates, a big win for fleet insurers. As OEMs deeply couple lighting with braking, steering, and perception ECUs, buyers are effectively locked into the tier-1 supplier that owns the entire stack. That establishment, and the prospect of subscription-based light upgrades delivered over-the-air, make adaptive lighting a priority line item on future product plans.

High Upfront Cost of Adaptive Modules vs. Fixed Lamps

Adaptive headlamps still cost 2-4 times as much as fixed LEDs, so OEMs usually bundle them with premium trim lines or paid software unlocks. On the 2026 BMW 3 Series, an adaptive ambient option adds nearly EUR 1,850 (~USD 2,135.15) to the sticker, limiting uptake in cost-sensitive markets. Dealership retrofits are scarce because extra harnesses void electrical warranties, cutting off a quick aftermarket path. Some suppliers now offer tiered packages that separate the expensive MEMS mirrors from basic auto-high-beam logic so that entry cars can at least comply with emerging regulations without big price jumps.

Other drivers and restraints analyzed in the detailed report include:

- Rising Premium and SUV Sales Lifting Feature-Take Rates

- Rapid LED Cost Reduction and Performance Gains

- Thermal Management Limits in High-Lumen LED/Laser Units

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Passenger vehicles retained the largest 73.76% share of the automotive adaptive lighting market in 2025, helped by steady model-year refreshes that make matrix and pixel LEDs standard on mid-trim crossovers. Carmakers bundle the lamps with infotainment upgrades so buyers view them as part of a single comfort-and-safety package rather than a costly stand-alone option. Styling freedom in SUVs also gives designers more space for heatsinks and sensors, which further encourages rapid rollout. As volume rises, tier-1 suppliers gain scale economies that lower per-module costs and improve reliability through shared electronics platforms.

Medium and heavy commercial vehicles are expected to post the fastest 9.62% CAGR through 2031, driven by regulations that pair adaptive beams with collision-mitigation braking on long-haul rigs. Fleet operators accept the added expense because better nighttime visibility cuts accident downtime and insurance premiums. Lamp makers now offer modular housings that slide into existing apertures, letting trucks upgrade during scheduled maintenance without repainting surrounding panels. The resulting retrofit path accelerates adoption and provides suppliers with a second revenue cycle once factory warranties expire.

Exterior systems held a commanding 93.22% share in 2025, reflecting global laws that require glare-free beams and daytime running lamps on every new vehicle. Automakers migrate to single global lamp architectures that can be recalibrated in software, limiting tooling changes across regions. That strategy shortens development cycles and lets design teams focus on signature graphics that reinforce brand identity. Suppliers, in turn, compete on thermal management and optical efficiency rather than on basic compliance.

Interior adaptive lighting is rising fastest at an 8.27% CAGR, largely because electric and autonomous models use color and intensity shifts to substitute for engine sound as feedback to occupants. Cabin-centric systems integrate with voice assistants and biometric sensors so light scenes match the driver's mood or route conditions. Software updates can add new themes just like smartphone wallpapers, giving OEMs an ongoing revenue stream. As screens proliferate inside vehicles, ambient LEDs also cut eye strain by balancing overall luminance.

The Automotive Adaptive Lighting Market Report is Segmented by Vehicle Type (Passenger Vehicles, Light Commercial Vehicles, and More), Application (Exterior Lighting and Interior Lighting), Component Type (Controllers and More), Technology (LED and More), Sales Channel (OEM and Aftermarket), Functionality (Automatic High Beam and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Geography Analysis

Asia-Pacific captured 45.55% of the automotive adaptive lighting market revenue in 2025 and is growing at an 8.91% CAGR through 2031, driven by China's rapidly evolving rules that allow road-projection features. Domestic brands deploy adaptive beams as a status symbol in electric models competing head-to-head with German luxury imports. Japanese suppliers such as Koito and Stanley are expanding factories across ASEAN and Latin America to hedge against currency shifts while staying close to global vehicle platforms. India is shaping up as the next inflection market; an indigenous lighting standard mirroring Europe's optics clears the path for a mandate covering trucks from 2027 onward.

Europe maintains technology leadership and will advance at a measured 4.49% CAGR to 2031. ECE R123 sets a high bar for glare-free performance, nudging all new platforms toward matrix LEDs or lasers. German premium OEMs continue to trickle down high-resolution lamps into sub-EUR 40,000 (~USD 46,178.20) models, forcing volume brands to adopt similar tech or risk market share erosion. Production costs are being squeezed as suppliers shift assembly to Poland, Hungary, and Morocco, where wages are lower, but logistics still favor on-time delivery to EU plants.

North America is finally unlocking pent-up demand now that the NHTSA green-lit adaptive beams. Growth of 4.78% CAGR through 2031 may seem modest, yet the base is small after decades of prohibition. Over-the-air activations on existing vehicles, led by Tesla, prove that a latent install base already waits in the driveway. Suppliers are localizing micro-LED lines in Mexico to capitalize on the United States-Mexico-Canada Agreement's rules-of-origin credits, all while trimming shipping lead times. South America and the Middle East follow in tandem; revenue lifts come from SUV-heavy lineups where buyers accept feature premiums, but the lack of stringent lighting rules still limits full matrix rollouts.

- Hella GmbH & Co. KGaA

- Valeo SA

- Koito Manufacturing Co., Ltd.

- Stanley Electric Co., Ltd.

- OSRAM Continental GmbH

- Marelli Automotive Lighting

- Lumileds Holding B.V.

- Hyundai Mobis Co., Ltd.

- Panasonic Automotive Systems

- ZKW Group

- J.W. Speaker Corporation

- Denso Corporation

- Varroc Lighting Systems

- Signify N.V. (Philips Automotive)

- Renesas Electronics Corporation

- Texas Instruments Incorporated

- Aptiv PLC

- Bosch Mobility

- Continental AG

- Lear Corporation

- Infineon Technologies AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent Global Lighting Regulations (ADB, ECE R123)

- 4.2.2 Growing Demand for Advanced Safety Systems and ADAS

- 4.2.3 Rising Premium and SUV Sales Lifting Feature-Take Rates

- 4.2.4 Rapid LED Cost Reduction and Performance Gains

- 4.2.5 OTA-Enabled Beam-Pattern Upgrades Post-Sale

- 4.2.6 V2X-Triggered Pedestrian-Communication Lighting

- 4.3 Market Restraints

- 4.3.1 High Upfront Cost of Adaptive Modules Vs. Fixed Lamps

- 4.3.2 Thermal Management Limits in High-Lumen LED/Laser Units

- 4.3.3 ECU Cybersecurity Risks Via CAN-FD Gateways (Under-Radar)

- 4.3.4 GaN Substrate Supply Bottlenecks for Laser Diodes (Under-Radar)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Vehicle Type

- 5.1.1 Passenger Vehicles

- 5.1.2 Light Commercial Vehicles (LCV)

- 5.1.3 Medium and Heavy Commercial Vehicles (MHCV)

- 5.2 By Application

- 5.2.1 Exterior Lighting

- 5.2.2 Interior Lighting

- 5.3 By Component Type

- 5.3.1 Controllers

- 5.3.2 Sensors / Cameras

- 5.3.3 Lamp Assemblies

- 5.3.4 Actuators

- 5.3.5 Others

- 5.4 By Technology

- 5.4.1 LED

- 5.4.2 Xenon / HID

- 5.4.3 Halogen

- 5.4.4 Laser Lighting

- 5.5 By Sales Channel

- 5.5.1 OEM

- 5.5.2 Aftermarket

- 5.6 By Functionality

- 5.6.1 Automatic High Beam

- 5.6.2 Dynamic Bending Light

- 5.6.3 Cornering Lights

- 5.6.4 Adaptive Front Lighting

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Rest of North America

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 Germany

- 5.7.3.2 United Kingdom

- 5.7.3.3 France

- 5.7.3.4 Italy

- 5.7.3.5 Spain

- 5.7.3.6 Rest of Europe

- 5.7.4 Asia-Pacific

- 5.7.4.1 China

- 5.7.4.2 India

- 5.7.4.3 Japan

- 5.7.4.4 South Korea

- 5.7.4.5 Rest of Asia-Pacific

- 5.7.5 Middle East and Africa

- 5.7.5.1 United Arab Emirates

- 5.7.5.2 Saudi Arabia

- 5.7.5.3 South Africa

- 5.7.5.4 Turkey

- 5.7.5.5 Rest of Middle East and Africa

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Hella GmbH & Co. KGaA

- 6.4.2 Valeo SA

- 6.4.3 Koito Manufacturing Co., Ltd.

- 6.4.4 Stanley Electric Co., Ltd.

- 6.4.5 OSRAM Continental GmbH

- 6.4.6 Marelli Automotive Lighting

- 6.4.7 Lumileds Holding B.V.

- 6.4.8 Hyundai Mobis Co., Ltd.

- 6.4.9 Panasonic Automotive Systems

- 6.4.10 ZKW Group

- 6.4.11 J.W. Speaker Corporation

- 6.4.12 Denso Corporation

- 6.4.13 Varroc Lighting Systems

- 6.4.14 Signify N.V. (Philips Automotive)

- 6.4.15 Renesas Electronics Corporation

- 6.4.16 Texas Instruments Incorporated

- 6.4.17 Aptiv PLC

- 6.4.18 Bosch Mobility

- 6.4.19 Continental AG

- 6.4.20 Lear Corporation

- 6.4.21 Infineon Technologies AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

汽車自我調整頭燈系統市場:按組件、技術、系統類型、車輛類型、銷售管道和最終用戶分類-2026-2032年全球市場預測

汽車自我調整頭燈系統市場:按組件、技術、系統類型、車輛類型、銷售管道和最終用戶分類-2026-2032年全球市場預測 自動遠光燈控制:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

自動遠光燈控制:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 主動式轉向頭燈市場分析及預測(至2035年):類型、產品、技術、組件、應用、最終用戶、功能、安裝類型、解決方案、模式

主動式轉向頭燈市場分析及預測(至2035年):類型、產品、技術、組件、應用、最終用戶、功能、安裝類型、解決方案、模式 自適應頭燈市場 - 全球產業規模、佔有率、趨勢、機會、預測:按車輛類型、技術、地區和競爭格局分類,2021-2031年自適應照明系統市場分析與預測(至2035年):類型、產品類型、服務、技術、組件、應用、形式、功能、安裝方式、解決方案印度汽車自我調整照明系統:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

自適應頭燈市場 - 全球產業規模、佔有率、趨勢、機會、預測:按車輛類型、技術、地區和競爭格局分類,2021-2031年自適應照明系統市場分析與預測(至2035年):類型、產品類型、服務、技術、組件、應用、形式、功能、安裝方式、解決方案印度汽車自我調整照明系統:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 汽車自我調整頭燈系統市場報告(按產品類型、應用和地區分類,2026-2034年)自動遠光燈控制市場 - 全球產業規模、佔有率、趨勢、機會及預測(按車輛類型、動力類型、銷售管道、技術、地區和競爭格局分類,2021-2031年)

汽車自我調整頭燈系統市場報告(按產品類型、應用和地區分類,2026-2034年)自動遠光燈控制市場 - 全球產業規模、佔有率、趨勢、機會及預測(按車輛類型、動力類型、銷售管道、技術、地區和競爭格局分類,2021-2031年) 自動遠光燈控制市場規模、佔有率和成長分析(按技術、車輛類型、推進系統、通路和地區分類)—產業預測(2026-2033 年)

自動遠光燈控制市場規模、佔有率和成長分析(按技術、車輛類型、推進系統、通路和地區分類)—產業預測(2026-2033 年) 汽車自我調整頭燈市場規模、佔有率和成長分析(按技術、車輛類型、銷售管道和地區分類)-2026-2033年產業預測

汽車自我調整頭燈市場規模、佔有率和成長分析(按技術、車輛類型、銷售管道和地區分類)-2026-2033年產業預測