|

市場調查報告書

商品編碼

2043847

印度汽車自我調整照明系統:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)India Automotive Adaptive Lighting System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

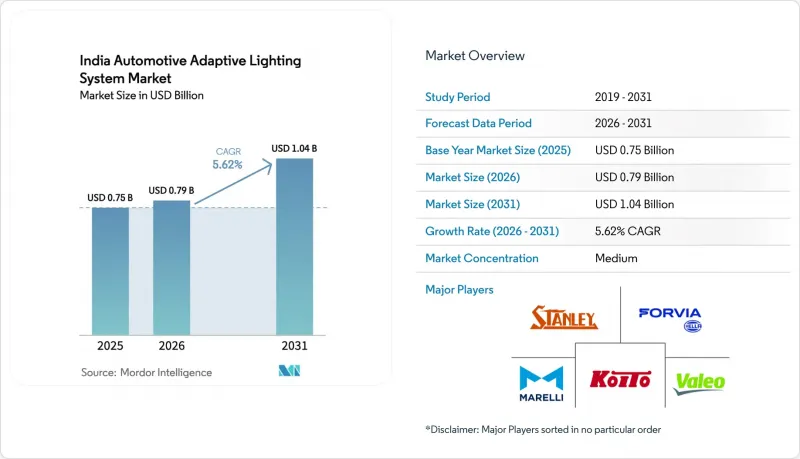

印度汽車自我調整照明系統市場預計將從 2025 年的 7.5 億美元成長到 2026 年的 7.9 億美元,到 2031 年達到 10.4 億美元,2026 年至 2031 年的複合年成長率為 5.62%。

近期監管政策的進展,特別是AIS-199光度標準草案,促使汽車製造商(OEM)將自我調整頭燈視為合規要求,而非僅將其視為一項豪華配置。同時,持續的價格壓力限制了全功能系統在高階和中高階車型上的應用,儘管由於LED晶圓成本的下降,價格差距正在逐步縮小。供應商正在實現關鍵感測器和相機模組的本地化生產,以滿足生產連結獎勵計畫(PLI)的要求,從而縮短前置作業時間並降低外匯風險。由於節能照明有助於最大限度地提高實際行駛里程,並且在充電基礎設施不斷擴展的背景下,節能照明已成為購車者關注的關鍵因素,因此市場成長前景仍然取決於OEM的電氣化藍圖。市場競爭較為溫和,五家全球一級供應商憑藉與OEM建立的穩固關係及其專有的軟體技術,維持各自的市場佔有率。

印度汽車自我調整照明系統市場趨勢與洞察。

LED成本的快速下降使其在中階市場普及。

最佳化的晶片尺寸提高了良率,顯著降低了LED大燈的價格,使汽車製造商能夠在不超出價格上限的情況下,將自我調整功能整合到車輛中。印度汽車研究協會 (ARAI)檢驗的本地開發原型表明,本地設計的LED自我調整模組能夠以具有競爭力的成本滿足AIS-127標準。中階車型需求的增加正在提升感測器和執行器供應商的規模經濟效益。價格仍然是印度乘用車買家關注的關鍵因素,因此,任何微小的成本降低都能幫助企業拓展更廣泛的客戶群。因此,自動遠光燈正擴大被中端電動車型作為標準配備。

AIS-199 法規(2024 年草案)規定了 AFS(空氣聚焦系統)的亮度標準。

2024 年草案統一了照明標準,並參考了聯合國 R-123 標準。該草案要求汽車製造商將眩光控制邏輯、攝影機輸入和自適應光學系統整合到 2026 年及以後推出的新平台中。已獲得歐洲市場產品認證的一級供應商將更容易獲得型式認證,因為他們可以重複使用檢驗的設計。由於該規則適用於所有車輛類別,到 2020 年代末,合規壓力將擴展到商用車領域。出口型原始設備製造商 (OEM) 對此統一表示歡迎,因為它使他們能夠使用單一模組滿足多個地區的要求,從而減輕工程負擔。短期內,AIS-199 將有效強制大多數新型乘用車配備自我調整照明系統。

高昂的單位成本阻礙了其在大規模生產車輛的廣泛應用。

功能齊全的自我調整頭燈組件價格昂貴,對佔銷量大多數的低價位車型構成了重大准入門檻。感測器依賴進口專用積體電路(ASIC)推高了零件成本,而原始設備製造商(OEM)也面臨外匯波動的風險。一級供應商正在測試模組化方案,根據配置等級調整功能,但由於生產規模分散,成本節約效果有限。在控制器和攝影機價格透過本地化生產降低之前,自我調整照明系統很可能仍將是高階車型的象徵,而非主流安全標準。

細分市場分析

預計到2025年,乘用車將佔印度汽車自我調整照明系統市場的55.67%,複合年成長率達8.47%。這主要是因為個人消費者優先考慮自我調整頭燈所提供的安全性能和時尚外觀。由於AIS-199相關法規的最後期限要求汽車製造商先推出符合標準的乘用車平台,卡車和巴士仍沿用傳統規格。電動乘用車的普及進一步推動了自適應照明系統的採用,因為低功率LED有助於延長續航里程。

因此,供應商的研發藍圖將工程資源集中在專為乘用車設計的波束成形演算法和緊湊型感測器叢集。由於車隊營運商更加關注投資報酬率,商用車領域的應用相對落後。然而,夜間運輸量的增加和更嚴格的保險標準可能會促使一些輕型商用車車隊在重型卡車之前率先採用自我調整遠光燈。未來,乘用車領域實現的規模經濟可望降低成本門檻,進而逐步推廣至貨運車輛和城際巴士。

在印度汽車自我調整照明系統市場,外部照明佔據主導地位。這是因為頭燈既符合安全法規,又滿足消費者可見的需求。到2025年,該類別將佔整個市場的72.87%,預計成長速度最快,到2031年複合年成長率將達到9.77%,這主要得益於自我調整頭燈和動態彎道照明模組向低階車型的擴展。車內照明應用,例如車內環境燈,主要應用於高階車型,這些車型更注重個人化而非嚴格的安全標準,且其市場基數較低。因此,供應商將工程預算的很大一部分用於頭燈的光學元件、感測器和光束成形軟體。

對外部照明的重視體現在整個頭燈總成(整合了致動器、ECU 和 LED)的高單價。雖然內部照明模組對於品牌差異化仍然至關重要,但由於缺乏監管支持,其應用受到限制。未來,車身域控制器的集中化有望透過同步車廂和外部照明序列進一步推動市場需求。然而,在整個預測期內,外部頭燈仍將是自適應照明產品組合中銷售和收入的主要驅動力。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- LED成本的快速下降使得中階市場採用LED技術成為可能。

- AIS-199 法規(2024 年草案)強制規定了 AFS 亮度標準。

- 原始設備製造商對低成本車輛中整合ADAS功能的需求

- 電動車的日益普及推高了對節能照明的需求。

- 根據PLI汽車零件計劃,一級供應商本地化獎勵

- 將用於 V2X 的嵌入式感測器與 microLED/像素 ADB 整合

- 市場限制因素

- 高昂的單價阻礙了其在普通市場上的廣泛應用。

- 半導體供應鏈的波動性

- 售後市場多元化以及因改裝而導致保固失效的風險。

- 車隊所有者對防眩光技術的優勢認知不足。

- 價值/供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

- 競爭公司之間的競爭

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

第5章 市場規模與成長預測

- 車輛類型

- 搭乘用車

- 輕型商用車(LCV)

- 中型和重型商用車輛(MHCV)

- 透過使用

- 外部照明

- 室內照明

- 依組件類型

- 控制器

- 感應器/攝影機

- 燈具組件

- 執行器

- 其他

- 透過技術

- LED

- 氙氣/HID燈

- 鹵素

- 雷射照明

- 按銷售管道

- OEM

- 售後市場

- 功能性別

- 自動遠光燈

- 動態彎曲燈光

- 彎道照明燈

- 自我調整頭燈

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Koito Manufacturing Co. Ltd.

- Valeo SA

- HELLA GmbH & Co KGaA(FORVIA)

- Magneti Marelli SpA

- Stanley Electric Co. Ltd.

- Varroc Engineering Ltd.

- Lumax Industries Ltd.

- Hyundai Mobis Co. Ltd.

- OSRAM Continental GmbH

- Texas Instruments Inc.

- Philips Automotive Lighting

- Continental AG

- Denso Corporation

- Robert Bosch GmbH

- Uno Minda Ltd.

- Neolite ZKW Lighting Pvt. Ltd.

- LG Innotek Co. Ltd.

- ZKW Group GmbH

- SL Corporation

- Yazaki Corp.

第7章 市場機會與未來展望

The Indian automotive adaptive lighting system market size is expected to increase from USD 0.75 billion in 2025 to USD 0.79 billion in 2026, reaching USD 1.04 billion by 2031, growing at a CAGR of 5.62% over 2026-2031.

Recent rule-making, notably the draft AIS-199 photometric standard, is nudging original equipment manufacturers (OEMs) to treat adaptive front lighting as a compliance feature rather than a luxury add-on. Meanwhile, persistent unit-cost pressures confine full-feature systems to premium and upper-mid trims, even as LED die-cost declines slowly narrow the affordability gap. Suppliers are localizing critical sensors and camera modules to qualify for production-linked incentives (PLI) and thereby shorten lead times and mitigate currency exposure. Growth prospects remain tied to OEM electrification roadmaps because energy-efficient lighting helps maximize real-world range, an attribute buyers value as charging infrastructure scales. Competitive intensity is moderate, with five global tier-1 suppliers leveraging established OEM relationships and in-house software stacks to defend share.

India Automotive Adaptive Lighting System Market Trends and Insights

Rapid LED Cost Declines Enabling Mid-Segment Adoption

ED headlamp prices have come down sharply as die-size optimization improves yield, allowing OEMs to equip cars with adaptive functions without breaching price ceilings. Indigenous prototypes validated by the Automotive Research Association of India prove that locally engineered LED adaptive modules can meet AIS-127 benchmarks at competitive costs. Added volumes from mid-segment trims improve scale economics for sensor and actuator suppliers. As price sensitivity remains a defining feature of India's passenger-vehicle buyers, each incremental cost reduction unlocks a broader customer pool. Consequently, mid-segment electrified platforms increasingly specify automatic high-beam as standard.

AIS-199 Regulation Mandating AFS Photometric Standards (2024 Draft)

The 2024 draft standard consolidates illumination norms and references UN R-123, pushing carmakers to add glare-control logic, camera inputs, and adaptive optics to new platforms launched after 2026. Tier-1 suppliers that already certify products for Europe can repurpose validated designs, easing homologation. Because the rule applies across vehicle classes, compliance pressure trickles into commercial-vehicle segments by the decade's end. Export-oriented OEMs value this alignment because a single module can serve multiple regions, reducing engineering overhead. In the short term, AIS-199 effectively makes adaptive lighting mandatory for most new passenger models.

High Unit-Cost Limits Mass-Market Penetration

Full adaptive front-lighting assemblies cost well, forming a steep barrier for budget vehicles that dominate sales. Import dependence for sensor ASICs keeps bills of materials elevated, exposing OEMs to currency swings. Tier-1 suppliers are testing modular approaches that scale features with trim level, but fragmented volumes dilute cost savings. Until controller and camera prices drop through local fabrication, adaptive lighting remains a premium signifier rather than a mainstream safety norm.

Other drivers and restraints analyzed in the detailed report include:

- OEM Demand for ADAS Bundle-Features in Low-Budget Vehicles

- Growing EV Penetration Raising Demand for Energy-Efficient Lighting

- Semiconductor Supply-Chain Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Passenger cars dominated the Indian automotive adaptive lighting system market share in 2025, holding 55.67% and growing at an 8.47% CAGR, largely because private buyers value the safety features and styling cues that adaptive headlamps offer. Regulatory deadlines tied to AIS-199 spur OEMs to launch compliant passenger platforms first, leaving trucks and buses on legacy setups. Electrified passenger cars further reinforce uptake, as low-wattage LEDs help extend driving range.

Supplier roadmaps, therefore, concentrate engineering resources on car-specific beam-shaping algorithms and compact sensor clusters. Commercial vehicles trail because fleet operators scrutinize return on investment more tightly. Nonetheless, rising night-haul logistics and stricter insurance norms may pull adaptive high beam into select LCV fleets sooner than heavy trucks. Over time, economies of scale achieved in the passenger domain are expected to lower cost barriers, enabling a gradual spill-over into goods carriers and intercity buses.

Exterior lighting accounts for the majority of the Indian automotive adaptive lighting system market because headlamps sit at the intersection of safety regulations and consumer visibility needs. In 2025, the category accounted for 72.87% of total value and is set to post the fastest expansion, clocking a 9.77% CAGR through 2031 as adaptive front lighting and dynamic bending modules move down-segment. Interior applications such as ambient cabin lighting grow from a lower base, anchored mostly in premium vehicles where personalization outweighs strict safety calculus. Suppliers, therefore, direct most engineering budgets into forward-lighting optics, sensors, and beam-forming software.

The exterior focus also reflects higher per-unit revenue, as complete headlamp assemblies integrate actuators, ECUs, and LEDs. Interior modules remain important for brand differentiation, yet they lack regulatory tailwinds, limiting their penetration. Over time, synchronized cabin-exterior light sequences may spur incremental demand once centralized body-domain controllers become common. For the forecast period, however, exterior headlamps remain the clear volume and value driver within adaptive lighting portfolios.

The India Automotive Adaptive Lighting System Market Report is Segmented by Vehicle Type (Passenger Vehicles, Light Commercial Vehicles, and More), Application (Exterior Lighting and Interior Lighting), Component Type (Controllers, Sensors/Cameras, and More), Technology (LED and More), Sales Channel (OEM and Aftermarket), and Functionality (Automatic High Beam and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Koito Manufacturing Co. Ltd.

- Valeo SA

- HELLA GmbH & Co KGaA (FORVIA)

- Magneti Marelli SpA

- Stanley Electric Co. Ltd.

- Varroc Engineering Ltd.

- Lumax Industries Ltd.

- Hyundai Mobis Co. Ltd.

- OSRAM Continental GmbH

- Texas Instruments Inc.

- Philips Automotive Lighting

- Continental AG

- Denso Corporation

- Robert Bosch GmbH

- Uno Minda Ltd.

- Neolite ZKW Lighting Pvt. Ltd.

- LG Innotek Co. Ltd.

- ZKW Group GmbH

- SL Corporation

- Yazaki Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid LED Cost Declines Enabling Mid-Segment Adoption

- 4.2.2 AIS-199 Regulation Mandating AFS Photometric Standards (2024 Draft)

- 4.2.3 OEM Demand for ADAS Bundle-Features in Low-Budget Vehicles

- 4.2.4 Growing EV Penetration Raising Demand for Energy-Efficient Lighting

- 4.2.5 Tier-1 Localisation Incentives Under PLI Auto Components Scheme

- 4.2.6 Integration of Micro-LED/Pixel ADB With Embedded Sensors for V2X

- 4.3 Market Restraints

- 4.3.1 High Unit-Cost Limits Mass-Market Penetration

- 4.3.2 Semiconductor Supply-Chain Volatility

- 4.3.3 Fragmented Aftermarket and Warranty-Void Risk for Retrofits

- 4.3.4 Low Awareness of Glare-Free Benefits Among Fleet Owners

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Competitive Rivalry

- 4.7.2 Threat of New Entrants

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Bargaining Power of Buyers

- 4.7.5 Threat of Substitutes

5 Market Size and Growth Forecasts (Value)

- 5.1 By Vehicle Type

- 5.1.1 Passenger Vehicles

- 5.1.2 Light Commercial Vehicles (LCV)

- 5.1.3 Medium and Heavy Commercial Vehicles (MHCV)

- 5.2 By Application

- 5.2.1 Exterior Lighting

- 5.2.2 Interior Lighting

- 5.3 By Component Type

- 5.3.1 Controllers

- 5.3.2 Sensors / Cameras

- 5.3.3 Lamp Assemblies

- 5.3.4 Actuators

- 5.3.5 Others

- 5.4 By Technology

- 5.4.1 LED

- 5.4.2 Xenon / HID

- 5.4.3 Halogen

- 5.4.4 Laser Lighting

- 5.5 By Sales Channel

- 5.5.1 OEM

- 5.5.2 Aftermarket

- 5.6 By Functionality

- 5.6.1 Automatic High Beam

- 5.6.2 Dynamic Bending Light

- 5.6.3 Cornering Lights

- 5.6.4 Adaptive Front Lighting

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Koito Manufacturing Co. Ltd.

- 6.4.2 Valeo SA

- 6.4.3 HELLA GmbH & Co KGaA (FORVIA)

- 6.4.4 Magneti Marelli SpA

- 6.4.5 Stanley Electric Co. Ltd.

- 6.4.6 Varroc Engineering Ltd.

- 6.4.7 Lumax Industries Ltd.

- 6.4.8 Hyundai Mobis Co. Ltd.

- 6.4.9 OSRAM Continental GmbH

- 6.4.10 Texas Instruments Inc.

- 6.4.11 Philips Automotive Lighting

- 6.4.12 Continental AG

- 6.4.13 Denso Corporation

- 6.4.14 Robert Bosch GmbH

- 6.4.15 Uno Minda Ltd.

- 6.4.16 Neolite ZKW Lighting Pvt. Ltd.

- 6.4.17 LG Innotek Co. Ltd.

- 6.4.18 ZKW Group GmbH

- 6.4.19 SL Corporation

- 6.4.20 Yazaki Corp.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

汽車自我調整頭燈系統市場:按組件、技術、系統類型、車輛類型、銷售管道和最終用戶分類-2026-2032年全球市場預測

汽車自我調整頭燈系統市場:按組件、技術、系統類型、車輛類型、銷售管道和最終用戶分類-2026-2032年全球市場預測 自動遠光燈控制:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

自動遠光燈控制:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 主動式轉向頭燈市場分析及預測(至2035年):類型、產品、技術、組件、應用、最終用戶、功能、安裝類型、解決方案、模式

主動式轉向頭燈市場分析及預測(至2035年):類型、產品、技術、組件、應用、最終用戶、功能、安裝類型、解決方案、模式 自適應頭燈市場 - 全球產業規模、佔有率、趨勢、機會、預測:按車輛類型、技術、地區和競爭格局分類,2021-2031年汽車自我調整照明系統:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)自適應照明系統市場分析與預測(至2035年):類型、產品類型、服務、技術、組件、應用、形式、功能、安裝方式、解決方案

自適應頭燈市場 - 全球產業規模、佔有率、趨勢、機會、預測:按車輛類型、技術、地區和競爭格局分類,2021-2031年汽車自我調整照明系統:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)自適應照明系統市場分析與預測(至2035年):類型、產品類型、服務、技術、組件、應用、形式、功能、安裝方式、解決方案 汽車自我調整頭燈系統市場報告(按產品類型、應用和地區分類,2026-2034年)自動遠光燈控制市場 - 全球產業規模、佔有率、趨勢、機會及預測(按車輛類型、動力類型、銷售管道、技術、地區和競爭格局分類,2021-2031年)

汽車自我調整頭燈系統市場報告(按產品類型、應用和地區分類,2026-2034年)自動遠光燈控制市場 - 全球產業規模、佔有率、趨勢、機會及預測(按車輛類型、動力類型、銷售管道、技術、地區和競爭格局分類,2021-2031年) 自動遠光燈控制市場規模、佔有率和成長分析(按技術、車輛類型、推進系統、通路和地區分類)—產業預測(2026-2033 年)

自動遠光燈控制市場規模、佔有率和成長分析(按技術、車輛類型、推進系統、通路和地區分類)—產業預測(2026-2033 年) 汽車自我調整頭燈市場規模、佔有率和成長分析(按技術、車輛類型、銷售管道和地區分類)-2026-2033年產業預測

汽車自我調整頭燈市場規模、佔有率和成長分析(按技術、車輛類型、銷售管道和地區分類)-2026-2033年產業預測