|

市場調查報告書

商品編碼

2044009

亞太地區企業資源規劃(ERP):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Asia-Pacific Enterprise Resource Planning - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

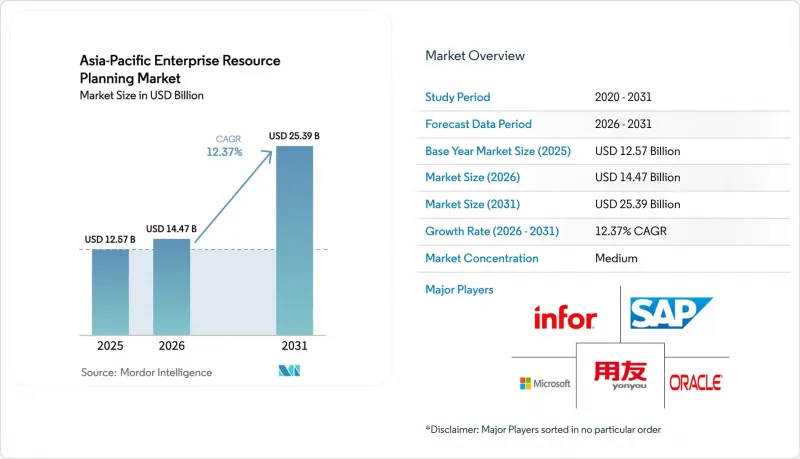

預計亞太地區的企業資源計畫 (ERP) 市場將從 2025 年的 125.7 億美元成長到 2026 年的 144.7 億美元,到 2031 年將達到 253.9 億美元,2026 年至 2031 年的複合年成長率為 12.37%。

雲端原生套件的快速普及、「雲端優先」策略的正式化以及人工智慧 (AI) 與核心工作流程的融合,正將目標市場從大型製造商擴展到監管嚴格的公共機構和小規模零售商。政府框架強制推行電子帳單、統一資料註冊表和主權雲端託管,縮短了決策週期,並將資訊技術 (IT) 預算重新導向現代企業資源規劃 (ERP) 平台。隨著供應商競相獲得本地資料中心認證、與國內身分錢包預先整合以及發布支援新創企業垂直擴展的應用程式介面 (API),競爭格局日趨激烈。人口結構變化、行動優先的工作模式以及低程式碼配置工具的融合,進一步降低了資源受限的中小型企業採用雲端原生技術的門檻。

亞太地區企業資源規劃(ERP)市場的趨勢與洞察

亞太地區企業對雲端原生架構的採用率不斷提高。

公部門的強制性要求正逐漸滲透到私人企業的採購週期。在日本政府統一規定所有機構必須剝離傳統資料中心之後,2024年至2025年間,日本政府採用雲端技術的系統數量激增335%,從671個增加到2918個。澳洲將於2026年推出一項政府範圍內的雲端政策,要求所有機構將雲端的經濟效益納入所有新的數位投資,並推廣與超大規模資料中心業者的合作認證。新加坡已將41個機構的213個系統遷移到商業雲,遷移的工作負載佔政府私有雲端的80%以上。這些案例表明,雲端技術能夠顯著縮短發布週期並降低營運成本,這鼓勵亞太地區企業資源規劃(ERP)市場的金融機構和零售商採取類似的現代化計畫。

亞洲新興經濟體政府主導的數位轉型舉措

各國發展藍圖現已將國內生產總值目標與數位經濟產出掛鉤,確保為整合資料骨幹網和人工智慧賦能的企業資源規劃(ERP)基礎設施提供永續的預算撥款。北京的《數位中國2025行動計畫》旨在將關鍵數位產業在GDP中的佔比提升至10%以上,同時將運算能力擴展至300百億億次浮點運算以上,從而為國內部署的、基於標準的平台創造可預測的需求。 2025年簽署的《印度-日本數位夥伴關係2.0》明確了數位公共基礎設施的互通性、人工智慧管治以及半導體價值鏈合作,加速了跨國系統整合專案。在新加坡的「智慧國家2.0」計畫中,數位經濟在過去五年中實現了11.2%的年均成長率,到2024年,十分之九的企業將至少採用一種數位化工具。這些政策縮短了最新套件的部署時間表,使亞太 ERP 市場中能夠驗證本地資料駐留情況並與電子採購平台和數位身分基礎設施整合的供應商獲得了競爭優勢。

亞洲區域城市缺乏熟練的ERP實施夥伴

諮詢人才仍然集中在大都會圈,迫使位於區域叢集的製造商忍受漫長的等待時間和高昂的差旅費用。一項針對越南605家中小企業的調查顯示,如果沒有內部促進者,18個月後員工留任率驟降至35%。馬來西亞的「新產業總體規劃」也指出類似的技能缺口是智慧工廠計畫的障礙,促使政府撥款用於培訓。雖然供應商提供遠端配置入口網站和模板化實施方案,但這些方案往往限制了亞太地區ERP市場的深度客製化。

細分市場分析

到2025年,雲端原生套件將佔據亞太地區企業資源規劃(ERP)市場46.1%的佔有率。隨著分散式辦公人員對智慧型手機上同等功能的需求日益成長,行動優先架構預計到2031年將以12.7%的複合年成長率成長。公共機構在SAP ECC和Oracle E-Business Suite停止支援前將其從本地部署遷移到雲端,推動了雲端原生模組市場的發展。企業正著力採用微服務架構,以避免高風險的大規模遷移,並實現分階段過渡。行動優先設計為零售商帶來了顯著優勢,例如減輕最終用戶的培訓負擔、加快核准流程以及管理全通路庫存調整。

供應商的策略也清楚地反映了這一轉變。一家日本數位代理公司透過採用可擴展的敏捷框架和自動化品質關卡,將發布週期從六個月縮短至48小時。微軟和SAP正在部署一套包含嵌入式人工智慧助理的ECC遷移解決方案,目標客戶為4萬家中型企業。 Workday在2025年12月收購Sana和Pipedream後,將提供3,000個現成的連接器,讓企業無需說明大量自訂程式碼即可整合對話代理程式。

預計到2025年,亞太地區財務會計產業將維持企業資源規劃(ERP)市場31.5%的佔有率,而人力資本管理(HCM)產業預計將以12.9%的複合年成長率成長。電子帳單,但人口結構的變化使得勞動力智慧的戰略重要性日益凸顯。由於日本My Number Card和新加坡Singpass API等技術,系統現在可以即時檢索經過驗證的身份資訊和福利數據,亞太地區薪資和人才管理模組的ERP市場正在蓬勃發展。

政府的實施案例可以作為先例。新加坡的VISION平台服務於10萬名公務員,實現了從招聘到退休的整個工作流程自動化,處理時間縮短了30%。 Infosys聲稱,透過將其人工智慧調查方法「Topaz」應用於Workday的實施,在轉換率和客戶維繫方面取得了可衡量的成果。這些案例證實,人才分析和預測性人員流動模型如今已成為董事會層級的優先事項。此外,將人工智慧洞察整合到ERP系統中,能夠幫助企業做出更明智的策略決策。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 亞太地區企業對雲端原生架構的採用率不斷提高。

- 亞洲新興經濟體政府主導的數位轉型(DX)舉措

- 後疫情時代加速向遠距辦公和行動優先工作流程的轉型

- 擴展本地 ISV 擴展的生態系統,以實現特定產業的客製化。

- 人工智慧分析功能的整合正在推動對最新ERP套件的需求。

- 亞太地區垂直產業SaaS新創創業投資資金籌措增加

- 市場限制因素

- 亞太地區垂直產業SaaS新創創業投資資金籌措增加

- 亞洲區域城市缺乏熟練的ERP實施夥伴

- 資料主權法規限制了跨境雲端技術的採用。

- 中小企業 (SME) 市場分散,IT 預算有限,這延緩了雲端 ERP 系統的採用。

- 對影響市場的宏觀經濟因素進行評估

- 產業供應鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 供應商議價能力

- 買方的議價能力

- 新參與企業的威脅

- 替代品的威脅

- 競爭公司之間的競爭關係

第5章 市場規模與成長預測

- 以建築學為例

- 雲端原生套件

- 行動優先的ERP

- 社交/協作型企業資源規劃

- 雙層/邊緣ERP

- 按業務職能

- 財會

- 供應鍊和營運

- 人力資本管理

- 客戶關係和交易

- 生產執行和品質

- 透過部署方法

- 現場

- 雲

- 按組織規模

- 大公司

- 小型企業

- 按行業

- 製造業

- 零售與電子商務

- BFSI

- 政府/公共部門

- 資訊科技/通訊

- 醫學與生命科學

- 其他行業

- 按地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲和紐西蘭

- 亞太其他地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- SAP SE

- Microsoft Corporation

- Oracle Corporation

- Unit4 NV

- IFS AB

- Infor Inc.

- Sage Group Plc

- Workday Inc.

- SYSPRO(Pty)Ltd.

- Yonyou Network Technology Co. Ltd.

- Ramco Systems Ltd.

- Kingdee International Software Group Company Limited

- Epicor Software Corporation

- Fujistu Limited

- NEC Corporation

- Zoho Corporation Pvt. Ltd.

- HashMicro Pte. Ltd.

- MYOB Group Pty. Ltd.

- Pronto Software Limited

- QAD Inc.

第7章 市場機會與未來展望

The Asia-Pacific Enterprise Resource Planning Market size is expected to grow from USD 12.57 billion in 2025 to USD 14.47 billion in 2026 and is forecast to reach USD 25.39 billion by 2031 at a 12.37% CAGR over 2026-2031.

Rapid uptake of cloud-native suites, formal cloud-first policies, and the embedding of artificial intelligence into core workflows are widening the addressable base beyond large manufacturers into highly regulated public-sector agencies and small retailers. Government frameworks that mandate e-invoicing, unified data registries, and sovereign cloud hosting have shortened decision cycles and redirected information-technology budgets toward modern enterprise resource planning platforms. Vendors are racing to certify local data centers, pre-integrate with national identity wallets, and expose application programming interfaces that enable start-ups to build vertical extensions, intensifying the competitive landscape. The convergence of demographic pressures, mobile-first workstyles, and low-code configuration tools is further lowering adoption barriers for resource-constrained small and medium enterprises.

Asia-Pacific Enterprise Resource Planning Market Trends and Insights

Rising Adoption of Cloud-Native Architectures Among Asia-Pacific Enterprises

Public-sector mandates are cascading into private procurement cycles. Japan's government cloud portfolio expanded from 671 to 2,918 systems between 2024 and 2025, a 335% surge, after centralized deadlines required agencies to vacate legacy data centers. Australia activated a whole-of-government cloud policy in 2026 that compels agencies to embed cloud economics in every new digital investment, driving hyperscaler partner certifications. Singapore migrated 213 systems to commercial clouds across 41 agencies, pushing more than 80% of eligible workloads off the government's private cloud. These exemplars demonstrate measurable reductions in release cycles and operating costs, persuading financial institutions and retailers to follow similar modernization blueprints in the APAC enterprise resource planning market.

Government-Led Digital Transformation Initiatives Across Emerging Asian Economies

National blueprints now tie gross domestic product targets to digital economy output, ensuring sustained budget allocations for unified data backbones and artificial intelligence-ready enterprise resource planning foundations. Beijing's Digital China 2025 Action Plan aims for core digital industries to exceed 10% of GDP while expanding compute capacity beyond 300 exaflops, creating predictable demand for domestically hosted, standards-based platforms. The India-Japan Digital Partnership 2.0, signed in 2025, codifies collaboration on interoperability of digital public infrastructure, artificial intelligence governance, and semiconductor value chains, accelerating cross-border system integration projects. Singapore's Smart Nation 2.0 recorded a 11.2% compound annual growth rate over the past five years in its digital economy, with 9 in 10 firms adopting at least one digital tool in 2024. Such policies compress adoption timelines for modern suites and favor vendors able to certify local data residency while integrating with e-procurement platforms and digital-identity rails in the Asia-Pacific ERP market.

Shortage of Skilled ERP Implementation Partners in Tier-2 Asian Cities

Consultancy talent remains concentrated in metro hubs, leaving manufacturers in provincial clusters with long wait times and premium travel charges. A survey of 605 Vietnamese small and medium enterprises showed sustained usage plunged to 35% after 18 months without an internal champion. Malaysia's New Industrial Master Plan flags the same skills gap as a barrier to smart-factory ambitions, prompting the government to earmark intervention funds for training. Vendors offer remote configuration portals and templated rollouts, yet these often limit deep customization in the Asia-Pacific ERP market.

Other drivers and restraints analyzed in the detailed report include:

- Accelerated Post-Pandemic Push Toward Remote Work and Mobile-First Workflows

- AI-Driven Analytics Driving Demand for Modern ERP Suites

- Data Sovereignty Regulations Limiting Cross-Border Cloud Deployments

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud-native suites owned 46.1% of the Asia-Pacific enterprise resource planning market share in 2025. Mobile-first architectures are forecast to post a 12.7% CAGR through 2031 as distributed workforces demand smartphone parity. The market for cloud-native modules is expanding as public agencies migrate from on-premises SAP ECC and Oracle E-Business Suite before their support sunsets. Enterprises value microservices that allow phased cutovers, avoiding risky big-bang switches. Mobile-first design reduces end-user training overhead and accelerates approval cycles, a boon for retailers reconciling omnichannel inventory.

Vendor strategies illustrate the shift. Japan's Digital Agency slashed release cycles from six months to 48 hours by adopting scaled agile frameworks and automated quality gates. Microsoft and SAP target 40,000 mid-market firms for ECC migrations that bundle built-in artificial intelligence co-pilots. Workday's December 2025 purchases of Sana and Pipedream deliver 3,000 pre-built connectors, enabling enterprises to embed conversational agents without heavy custom code.

Finance and accounting retained 31.5% of the Asia-Pacific enterprise resource planning market share in 2025, yet human capital management is on track for a 12.9% CAGR. Mandatory e-invoicing and real-time tax remittance keep finance at the core, but demographic headwinds make workforce intelligence equally strategic. The Asia-Pacific enterprise resource planning market for payroll and talent modules is growing as Japan's My Number Card and Singapore's Singpass APIs enable systems to pull verified identity and benefits data in real time.

Government deployments set precedents. Singapore's VISION platform, spanning 100,000 public officers, cut processing time by 30% after automating hire-to-retire workflows. Infosys applies its Topaz artificial intelligence methodology to Workday rollouts, claiming measurable gains in close rates and retention. These examples reinforce that talent analytics and predictive attrition models are now board-level priorities. Additionally, integrating AI-driven insights into ERP systems enables organizations to make more informed, strategic decisions.

The Asia-Pacific Enterprise Resource Planning Market Report is Segmented by Architecture (Cloud-Native Suite, Mobile-First ERP, and More), Business Function (Finance and Accounting, and More), Deployment Model (On-Premise, and Cloud), Organization Size (Large Enterprises, and Small and Medium Enterprises), Industry Vertical (Manufacturing, BFSI, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- SAP SE

- Microsoft Corporation

- Oracle Corporation

- Unit4 N.V.

- IFS AB

- Infor Inc.

- Sage Group Plc

- Workday Inc.

- SYSPRO (Pty) Ltd.

- Yonyou Network Technology Co. Ltd.

- Ramco Systems Ltd.

- Kingdee International Software Group Company Limited

- Epicor Software Corporation

- Fujistu Limited

- NEC Corporation

- Zoho Corporation Pvt. Ltd.

- HashMicro Pte. Ltd.

- MYOB Group Pty. Ltd.

- Pronto Software Limited

- QAD Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Adoption of Cloud-Native Architectures Among Asia-Pacific Enterprises

- 4.2.2 Government-led Digital Transformation Initiatives Across Emerging Asian Economies

- 4.2.3 Accelerated Post-pandemic Push Toward Remote Work and Mobile-first Workflows

- 4.2.4 Growing Ecosystem of Local ISV Extensions Enabling Industry-specific Customizations

- 4.2.5 Integration of AI-driven Analytics Driving Demand for Modern ERP Suites

- 4.2.6 Increasing Venture Capital Funding for Vertical SaaS Startups in Asia-Pacific

- 4.3 Market Restraints

- 4.3.1 Increasing Venture Capital Funding for Vertical SaaS Startups in Asia-Pacific

- 4.3.2 Shortage of Skilled ERP Implementation Partners in Tier-2 Asian Cities

- 4.3.3 Data Sovereignty Regulations Limiting Cross-border Cloud Deployments

- 4.3.4 Fragmented SME Market With Low IT Budgets Slowing Cloud ERP Adoption

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Architecture

- 5.1.1 Cloud-Native Suite

- 5.1.2 Mobile-First ERP

- 5.1.3 Social / Collaborative ERP

- 5.1.4 Two-Tier / Edge ERP

- 5.2 By Business Function

- 5.2.1 Finance and Accounting

- 5.2.2 Supply-Chain and Operations

- 5.2.3 Human Capital Management

- 5.2.4 Customer Relationship and Commerce

- 5.2.5 Manufacturing Execution and Quality

- 5.3 By Deployment Model

- 5.3.1 On-Premise

- 5.3.2 Cloud

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises

- 5.5 By Industry Vertical

- 5.5.1 Manufacturing

- 5.5.2 Retail and E-commerce

- 5.5.3 BFSI

- 5.5.4 Government and Public Sector

- 5.5.5 IT and Telecom

- 5.5.6 Healthcare and Life Sciences

- 5.5.7 Other Industry Verticals

- 5.6 By Geography

- 5.6.1 China

- 5.6.2 India

- 5.6.3 Japan

- 5.6.4 South Korea

- 5.6.5 Australia and New Zealand

- 5.6.6 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Microsoft Corporation

- 6.4.3 Oracle Corporation

- 6.4.4 Unit4 N.V.

- 6.4.5 IFS AB

- 6.4.6 Infor Inc.

- 6.4.7 Sage Group Plc

- 6.4.8 Workday Inc.

- 6.4.9 SYSPRO (Pty) Ltd.

- 6.4.10 Yonyou Network Technology Co. Ltd.

- 6.4.11 Ramco Systems Ltd.

- 6.4.12 Kingdee International Software Group Company Limited

- 6.4.13 Epicor Software Corporation

- 6.4.14 Fujistu Limited

- 6.4.15 NEC Corporation

- 6.4.16 Zoho Corporation Pvt. Ltd.

- 6.4.17 HashMicro Pte. Ltd.

- 6.4.18 MYOB Group Pty. Ltd.

- 6.4.19 Pronto Software Limited

- 6.4.20 QAD Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

企業資源計畫 (ERP) 市場 - 全球產業規模、佔有率、趨勢、機會和預測:按組件、部署模式、業務功能、最終用戶、行業、地區和競爭對手分類,2021-2031 年

企業資源計畫 (ERP) 市場 - 全球產業規模、佔有率、趨勢、機會和預測:按組件、部署模式、業務功能、最終用戶、行業、地區和競爭對手分類,2021-2031 年 企業資源計畫 (ERP) 市場:按部署類型、組件、組織規模和產業分類-2026-2032 年全球市場預測

企業資源計畫 (ERP) 市場:按部署類型、組件、組織規模和產業分類-2026-2032 年全球市場預測 企業資源規劃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

企業資源規劃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 2026年全球產品實施服務市場報告2026年全球開放原始碼企業資源規劃(ERP)市場報告

2026年全球產品實施服務市場報告2026年全球開放原始碼企業資源規劃(ERP)市場報告 物聯網資源最佳化解決方案市場預測至2034年-按解決方案類型、元件、部署模式、應用、最終用戶和地區分類的全球分析電子商務ERP整合:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)2026年全球ERP和ECM整合市場報告2026年企業資源規劃(ERP)區塊鏈全球市場報告

物聯網資源最佳化解決方案市場預測至2034年-按解決方案類型、元件、部署模式、應用、最終用戶和地區分類的全球分析電子商務ERP整合:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)2026年全球ERP和ECM整合市場報告2026年企業資源規劃(ERP)區塊鏈全球市場報告 2026-2030年全球企業資源規劃系統整合與諮詢市場

2026-2030年全球企業資源規劃系統整合與諮詢市場