|

市場調查報告書

商品編碼

2044022

電子商務ERP整合:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)E-commerce ERP Integration - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

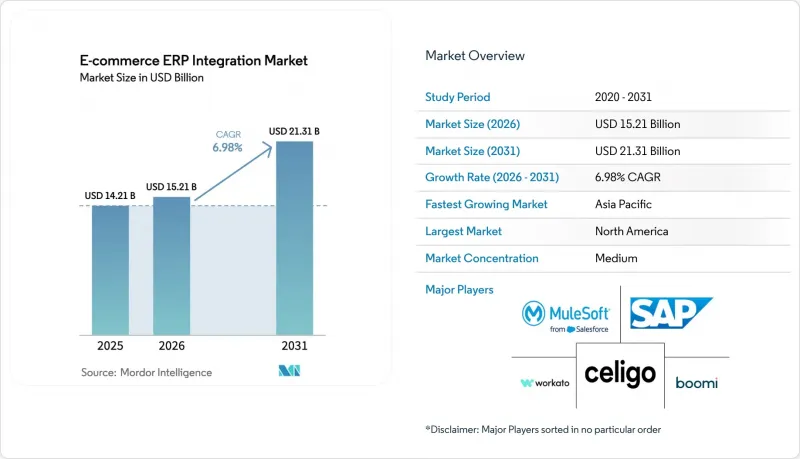

預計電子商務 ERP 整合市場將從 2025 年的 142.1 億美元和 2026 年的 152.1 億美元成長到 2031 年的 213.1 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 6.98%。

對全通路零售、符合稅務法規的即時發票以及可組合式數位商務日益成長的需求,正將整合從後勤部門IT營運提升至首要任務。歐盟和印度強制推行電子帳單、無頭電商平台的迅速普及以及全球市場對經營團隊水平違規行為日益嚴厲的處罰,都促使零售商需要能夠處理每秒數千次API調用的低延遲中間件。訂閱模式推動了雲端技術的普及,因為整合支出與交易高峰期相符。同時,低程式碼iPaaS工具正在為資源受限的團隊提供更方便的連接方式。供應商將整合功能捆綁到ERP套件中,而專業供應商則透過為特定應用提供現成的連接器來凸顯自身優勢,加劇了市場競爭。

全球電子商務ERP整合市場趨勢與洞察

無頭商業架構的傳播

無頭電商透過解耦前端和後端邏輯,使品牌能夠同時部署多個接點,例如網頁、語音和物聯網介面。這種架構顯著增加了 API 端點的數量,因此需要中間件來處理比傳統單體平台多三到五倍的單筆交易呼叫。採用無頭框架的零售商通常更傾向於整合平台即服務 (iPaaS) 解決方案,包括 Shopify Plus 和 BigCommerce 等平台的認證連接器。 API 呼叫量的增加帶來了資料一致性方面的挑戰,尤其是在不同管道的購物車內容或配送時間出現不一致時。為了解決這些問題,整合供應商正在引入即時監控功能,並採用基於交易量的績效定價模式,從而確保零售商的無縫營運和更高的可靠性。

中階零售市場對以SaaS為基礎的ERP套件的採用率不斷提高

中型零售商正加速從傳統的本地企業資源規劃 (ERP) 系統遷移到 SAP S/4HANA Cloud、Oracle NetSuite 和 Microsoft Dynamics 365 等現代雲端套件。這些雲端解決方案提供原生商務連接器,使零售商能夠在數週而非數月內同步各個網店和市場平台的訂單,從而顯著縮短專案週期。透過將基礎設施成本轉移給供應商,這些解決方案還有助於最佳化公司的營運支出。此外,這些平台的持續更新確保了連接器的長期相容性。然而,雲端部署的多租戶結構在資料儲存和合規性方面帶來了挑戰,尤其對於在資料保護條例嚴格的地區營運的公司而言更是如此。這推動了對特定區域部署方案的需求,這些方案既能解決合規性問題,又能維持雲端 ERP 系統的效率和擴充性。

在本地部署的 ERP 系統中遺留的客製化設計阻礙了標準化連接器的採用。

多年來在本地ERP環境中開發的專有程式碼會形成脆弱且高度客製化的資料模型,而現成的連接器難以輕鬆處理這些模型。零售商常常面臨巨大的挑戰,並需要承擔大量的諮詢費用,才能將這些自訂欄位、工作流程和流程映射到現代系統所需的標準化模式。這種複雜性通常會導致雲端遷移專案延長約6至12個月,因為企業需要採取措施確保相容性並最大限度地減少對業務的影響。當多個ERP實例部署在不同區域時,這種困難會進一步加劇,因為整合平台必須並行維護和管理連接器,而理想情況下,這些連接器應該作為一個統一的系統運作。這些挑戰凸顯了製定穩健的規劃和執行策略以簡化遷移流程並確保業務連續性的迫切需求。

細分市場分析

到2025年,基於雲端的解決方案將佔銷售額的54.23%,因為零售商優先考慮在假期季節實現彈性擴展,並避免硬體升級週期。混合部署方案預計將以7.58%的複合年成長率成長,在本地控制敏感財務模組的同時,兼顧雲端面向客戶的商務服務的速度。混合部署中的電子商務ERP整合市場預計將持續成長,因為店內邊緣運行時支援本地訂單處理,並與中央ERP系統同步以減少連接故障。第二代混合平台能夠根據即時延遲和合規性閾值動態路由數據,將邊緣設備、私有雲端和公有SaaS端點統一到一個策略域。

仍完全依賴本地部署中間件的組織將資料主權法規和現有伺服器較長的折舊週期列為主要原因。然而,不斷上漲的維護成本和熟練人員的短缺正在加速向託管服務的轉型。為了促進這一轉變,供應商現在將持續安全更新、微隔離網路控制和人工智慧驅動的異常檢測功能捆綁在一起。這些附加價值,加上訂閱定價模式,使得雲端服務和混合雲端服務越來越有吸引力,尤其對於那些跨多個稅務和支付生態系統運營的企業而言更是如此。

預計到2025年,中小企業將佔總收入的62.14%,這表明低代碼iPaaS訂閱服務(每月300美元起)即使在預算有限的情況下也能提供企業級功能。範本庫可將部署時間縮短至最短六週,從而實現向新銷售管道和履約合作夥伴的快速過渡。大型零售商雖然數量較少,但他們正在推動高價值的客製化項目,這些項目將全通路編配與獨特的定價演算法相結合。然而,這兩類企業都在採取雙管齊下的策略:使用現成的連接器處理通用流程,並針對差異化工作流程進行客製化編碼。

供應商格局也反映了這種兩極化。純粹的 iPaaS 公司正在添加企業管治模組、基於角色的存取控制、版本控制的 API 閘道和 SOC 2 認證,以進軍更高層級市場。同時,傳統的中間件套件正在引入拖放式設計器,以維持其在中層市場的佔有率。這種趨同的發展藍圖正在縮小技術差距,價格、支援和行業專業知識正成為主要的購買標準。因此,市場在不犧牲複雜部署深度的前提下,持續擴大對各種規模企業的吸引力。

區域分析

到2025年,亞太地區將佔全球整體收入的29.37%。這主要得益於中國、印度和東南亞地區以數位優先的消費者,他們期望透過超級應用、聊天和社交視訊獲得不間斷的購物體驗。諸如印度統一支付介面(UPI)等本地支付基礎設施每月處理數十億筆交易,從而催生了對能夠近乎即時匹配小額支付的ERP連接器的需求。在市場不斷擴張的非洲,對M-Pesa等行動支付系統的依賴迫使供應商開發支援基於USSD的驗證以及在行動電話覆蓋範圍之外進行離線同步的適配器。

北美和歐洲的絕對支出最高。零售商正從簡單的訂單同步轉向更高級的應用場景,例如即時碳足跡追蹤和人工智慧驅動的配送路線最佳化。歐盟分階段實施的ViDA強制令正在加速對符合稅務規定的發票資料橋接的投資。同時,美國商家正在將州級銷售稅引擎與其「先買後付」服務整合。中東國家,特別是沙烏地阿拉伯和阿拉伯聯合大公國,正在投入公共資金建設全通路基礎設施,這產生了對能夠將本地閘道器與全球物流API整合的連接器的需求。

區域資料隱私法導致架構選擇分散。歐盟-美國資料隱私框架於2023年生效,使跨大西洋資料傳輸合法化。然而,持續不斷的法律挑戰使其能否繼續有效存疑。為防患於未然,零售商正在建立混合架構,並準備在框架失效時遷移到本地處理。中國的本地化法規強制要求ERP系統在國內託管,歐洲根據GDPR實施嚴格的同意追蹤,俄羅斯則強制要求資料儲存在國內。整合平台透過位置感知路由來應對這些挑戰,在不影響效能的前提下,尊重居住地。新興市場也需要「離線優先」的運行時環境,以便在邊緣端對交易進行排隊,而目前缺乏在該領域擁有豐富經驗的供應商,這表明該領域存在尚未開發的成長機會。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 無頭商業架構的傳播

- 中階零售市場對以SaaS為基礎的ERP套件的採用率不斷提高

- 強制性電子帳單和綜合稅務合規

- 隨著全通路零售的成長,整合化的庫存可見性變得至關重要。

- 市場經銷商正在整合 ERP 系統,以避免因違反服務等級協定 (SLA) 而受到處罰。

- 低程式碼 iPaaS 平台降低了整合複雜性和成本。

- 市場限制因素

- 對傳統本地部署 ERP 系統的客製化阻礙了標準化連接器的採用。

- 跨境資料流相關的資料安全和合規性問題

- 新興市場複雜的多站點部署往往伴隨著高昂的總擁有成本

- 熟練的整合架構師和中間件開發人員短缺

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模與成長預測

- 部署模式

- 基於雲端的

- 現場

- 混合

- 按組織規模

- 大公司

- 小型企業

- 按行業

- 零售和消費品

- 製造業

- 衛生保健

- 物流/運輸

- 其他行業

- 透過整合方法

- API整合

- 中介軟體/ESB

- 客製化/專屬整合

- 整合平台即服務 (iPaaS)

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 亞太其他地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲地區

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Celigo, Inc.

- Boomi, Inc.

- MuleSoft LLC

- Jitterbit, Inc.

- Workato, Inc.

- SnapLogic, Inc.

- Microsoft Corporation

- SAP SE

- Oracle Corporation

- IBM Corporation

- SPS Commerce, Inc.

- TrueCommerce, Inc.

- Magic Software Enterprises Ltd.

- nChannel, Inc.

- Patchworks Integration Ltd.

- Adeptia, Inc.

- Cleo Communcations, Inc.

- HighJump Software Inc.(Korber AG)

- Dscartes Systems Group Inc.

- Flowgear(Pty)Ltd.

第7章 市場機會與未來展望

The E-commerce enterprise resource planning integration market size is projected to expand from USD 14.21 billion in 2025 and USD 15.21 billion in 2026 to USD 21.31 billion by 2031, registering a CAGR of 6.98% between 2026 and 2031.

Rising omnichannel retail expectations, real-time tax-compliant invoicing, and the shift toward composable digital commerce are reshaping integration from a back-office IT task into a board-level priority. Mandatory e-invoicing rules across the European Union and India, the rapid spread of headless commerce storefronts, and mounting service-level penalties on global marketplaces are driving retailers to seek low-latency middleware capable of orchestrating thousands of API calls per second. Cloud deployments dominate as subscription economics align integration spending with transaction peaks, while low-code iPaaS tools democratize connectivity for resource-constrained teams. Competitive intensity stems from vendors that bundle integration with ERP suites and from specialists that differentiate through pre-built connectors for niche applications.

Global E-commerce ERP Integration Market Trends and Insights

Proliferation of Headless Commerce Architectures

Headless commerce decouples the storefront from back-end logic, allowing brands to deploy multiple touchpoints, such as web, voice, and IoT interfaces, simultaneously. This architecture significantly increases the number of API endpoints, requiring middleware to handle three to five times as many calls per transaction as traditional monolithic platforms. Retailers adopting headless frameworks often prefer Integration Platform as a Service (iPaaS) solutions that include certified connectors for platforms such as Shopify Plus, BigCommerce, and others. The increased volume of API calls introduces data-consistency challenges, particularly when discrepancies arise in cart contents or delivery estimates across different channels. To address these issues, integration vendors are incorporating real-time monitoring capabilities and adopting outcome-based pricing models that align with transaction throughput, ensuring seamless operations and improved reliability for retailers.

Rising Adoption of SaaS-Based ERP Suites Among Mid-Market Retailers

Mid-market merchants are increasingly transitioning from outdated on-premise Enterprise Resource Planning (ERP) systems to modern cloud-based suites such as SAP S/4HANA Cloud, Oracle NetSuite, and Microsoft Dynamics 365. These cloud solutions offer native commerce connectors that significantly reduce project timelines by enabling retailers to synchronize orders across various web stores and marketplaces in a matter of weeks rather than months. By shifting infrastructure costs to vendors, these solutions also help businesses optimize their operational expenses. Additionally, continuous updates provided by these platforms ensure that connector compatibility is maintained over time. However, the multi-tenant nature of cloud deployments introduces data residency and compliance challenges, particularly for businesses operating in regions with stringent data protection regulations. This has led to a growing demand for region-specific deployment options that address these compliance concerns while maintaining the efficiency and scalability of cloud-based ERP systems.

Legacy On-Premise ERP Customizations Hindering Standardized Connectors

Years of bespoke code in on-premise ERP landscapes create brittle and highly customized data models that off-the-shelf connectors cannot easily accommodate. Retailers often face significant challenges and incur substantial consulting fees to map these custom fields, workflows, and processes to normalized schemas required for modern systems. This complexity frequently delays cloud migration projects by an estimated 6 to 12 months, as businesses work to ensure compatibility and minimize disruptions. The difficulty is further compounded when multiple ERP instances are deployed across different regions, requiring integration platforms to maintain and manage parallel connectors for what ideally should function as a unified system. These challenges highlight the critical need for robust planning and execution strategies to streamline the migration process and ensure operational continuity.

Other drivers and restraints analyzed in the detailed report include:

- Mandatory E-Invoicing and Taxation Compliance Integrations

- Growth of Omnichannel Retail Requiring Unified Inventory Visibility

- Data Security and Compliance Concerns Around Cross-Border Flows

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud-based solutions accounted for 54.23% of 2025 revenue as retailers gravitated toward elastic scaling during holiday peaks and avoided hardware refresh cycles. The hybrid approach is forecast to rise at a 7.58% CAGR, balancing on-premise control for sensitive finance modules with cloud speed for customer-facing commerce services. The E-commerce enterprise resource planning integration market size for hybrid deployments is projected to widen as edge runtimes in stores support local order processing and later synchronize with central ERPs, mitigating connectivity outages. Second-generation hybrid platforms route data dynamically based on real-time latency and compliance thresholds, integrating edge devices, private clouds, and public SaaS endpoints in a single policy domain.

Organizations still running fully on-premises middleware cite data sovereignty rules and long depreciation cycles for existing servers. Yet, rising maintenance costs and limited talent pools accelerate the pivot toward managed services. Vendors now bundle continuous security updates, micro-segmented network controls, and AI-driven anomaly detection to ease the transition. These value-adds, combined with subscription pricing, make cloud and hybrid offerings increasingly attractive, especially for merchants operating across multiple tax regimes and payment ecosystems.

SMEs accounted for 62.14% of 2025 revenue, underscoring how low-code iPaaS subscriptions starting at USD 300 per month unlock enterprise-grade capabilities for smaller budgets. Template libraries compress deployment to as little as 6 weeks, enabling rapid pivots to new sales channels and fulfillment partners. Larger retailers, while fewer in number, drive high-value custom projects that fuse omnichannel orchestration with proprietary pricing algorithms. Both cohorts, however, pursue a bimodal strategy: pre-built connectors for commodity processes and bespoke coding for differentiating workflows.

The vendor landscape mirrors this dichotomy. Pure-play iPaaS firms add enterprise governance modules, role-based access, versioned API gateways, and SOC 2 attestations to penetrate the upper tier, while traditional middleware suites introduce drag-and-drop designers to defend mid-market share. These converging roadmaps reduce technology gaps, making pricing, support, and vertical expertise the main buying criteria. Consequently, the market continues to broaden its appeal across company sizes without sacrificing depth for complex rollouts.

The E-Commerce Enterprise Resource Planning Integration Market Report is Segmented by Deployment Mode (Cloud-Based, On-Premise, and Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), Industry Vertical (Retail and Consumer Goods, and More), Integration Approach (API Integration, Custom / Bespoke Integration, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific accounted for 29.37% of global revenue in 2025, driven by digital-first consumers in China, India, and Southeast Asia who expect uninterrupted commerce across super-apps, chat, and social video. Local payment rails like India's Unified Payments Interface process billions of monthly transactions, requiring ERP connectors that reconcile micro-payments in near real time. Africa, expanding its market, relies on mobile money systems such as M-Pesa, prompting vendors to build adapters for USSD-based confirmations and offline synchronization when cellular coverage lapses.

North America and Europe generate the largest absolute spend. Retailers are moving beyond order synchronization to advanced use cases such as real-time carbon footprint tracking and AI-driven delivery routing. The European Union's phased ViDA mandate accelerates investment in tax-compliant invoice data bridges, while U.S. merchants integrate state-level sales tax engines alongside Buy Now Pay Later services. Middle Eastern economies, especially Saudi Arabia and the United Arab Emirates, channel public funds into omnichannel infrastructure, demanding connectors that blend local gateways with global logistics APIs.

Geography-specific data privacy laws fragment architecture choices. . The EU-US Data Privacy Framework, enacted in 2023, legitimizes transatlantic data transfers. However, ongoing legal challenges cast doubt on its longevity. As a precaution, retailers are crafting hybrid architectures, ready to shift to on-premise processing should the framework face invalidation. China's localization rules compel in-country ERP hosting, Europe enforces rigorous consent tracking under GDPR, and Russia mandates domestic data storage. Integration platforms answer with location-aware routing that respects residency without compromising performance. Emerging markets also push for offline-first runtimes capable of queuing transactions at the edge, an area where only a few vendors currently excel, signaling untapped growth opportunities.

- Celigo, Inc.

- Boomi, Inc.

- MuleSoft LLC

- Jitterbit, Inc.

- Workato, Inc.

- SnapLogic, Inc.

- Microsoft Corporation

- SAP SE

- Oracle Corporation

- IBM Corporation

- SPS Commerce, Inc.

- TrueCommerce, Inc.

- Magic Software Enterprises Ltd.

- nChannel, Inc.

- Patchworks Integration Ltd.

- Adeptia, Inc.

- Cleo Communcations, Inc.

- HighJump Software Inc. (Korber AG)

- Dscartes Systems Group Inc.

- Flowgear (Pty) Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of Headless Commerce Architectures

- 4.2.2 Rising Adoption of SaaS-Based ERP Suites Among Mid-Market Retailers

- 4.2.3 Mandatory E-Invoicing and Taxation Compliance Integrations

- 4.2.4 Growth of Omnichannel Retail Requiring Unified Inventory Visibility

- 4.2.5 Surge in Marketplace Sellers Integrating ERP to Meet SLA Penalties

- 4.2.6 Low-Code iPaaS Platforms Lowering Integration Complexity and Cost

- 4.3 Market Restraints

- 4.3.1 Legacy On-Premise ERP Customizations Hindering Standardized Connectors

- 4.3.2 Data Security and Compliance Concerns Around Cross-Border Flows

- 4.3.3 High TCO for Complex Multi-Site Rollouts in Emerging Markets

- 4.3.4 Shortage of Skilled Integration Architects and Middleware Developers

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Mode

- 5.1.1 Cloud-Based

- 5.1.2 On-Premise

- 5.1.3 Hybrid

- 5.2 By Organization Size

- 5.2.1 Large Enterprises

- 5.2.2 Small and Medium Enterprises

- 5.3 By Industry Vertical

- 5.3.1 Retail and Consumer Goods

- 5.3.2 Manufacturing

- 5.3.3 Healthcare

- 5.3.4 Logisitcs and Transportation

- 5.3.5 Other Industry Verticals

- 5.4 By Integration Approach

- 5.4.1 API Integration

- 5.4.2 Middleware / ESB

- 5.4.3 Custom / Bespoke Integration

- 5.4.4 Integration Platform as a Service (iPaaS)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Celigo, Inc.

- 6.4.2 Boomi, Inc.

- 6.4.3 MuleSoft LLC

- 6.4.4 Jitterbit, Inc.

- 6.4.5 Workato, Inc.

- 6.4.6 SnapLogic, Inc.

- 6.4.7 Microsoft Corporation

- 6.4.8 SAP SE

- 6.4.9 Oracle Corporation

- 6.4.10 IBM Corporation

- 6.4.11 SPS Commerce, Inc.

- 6.4.12 TrueCommerce, Inc.

- 6.4.13 Magic Software Enterprises Ltd.

- 6.4.14 nChannel, Inc.

- 6.4.15 Patchworks Integration Ltd.

- 6.4.16 Adeptia, Inc.

- 6.4.17 Cleo Communcations, Inc.

- 6.4.18 HighJump Software Inc. (Korber AG)

- 6.4.19 Dscartes Systems Group Inc.

- 6.4.20 Flowgear (Pty) Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

企業資源計畫 (ERP) 市場 - 全球產業規模、佔有率、趨勢、機會和預測:按組件、部署模式、業務功能、最終用戶、行業、地區和競爭對手分類,2021-2031 年

企業資源計畫 (ERP) 市場 - 全球產業規模、佔有率、趨勢、機會和預測:按組件、部署模式、業務功能、最終用戶、行業、地區和競爭對手分類,2021-2031 年 企業資源計畫 (ERP) 市場:按部署類型、組件、組織規模和產業分類-2026-2032 年全球市場預測

企業資源計畫 (ERP) 市場:按部署類型、組件、組織規模和產業分類-2026-2032 年全球市場預測 企業資源規劃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

企業資源規劃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 2026年全球產品實施服務市場報告2026年全球開放原始碼企業資源規劃(ERP)市場報告

2026年全球產品實施服務市場報告2026年全球開放原始碼企業資源規劃(ERP)市場報告 物聯網資源最佳化解決方案市場預測至2034年-按解決方案類型、元件、部署模式、應用、最終用戶和地區分類的全球分析2026年全球ERP和ECM整合市場報告2026年企業資源規劃(ERP)區塊鏈全球市場報告亞太地區企業資源規劃(ERP):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

物聯網資源最佳化解決方案市場預測至2034年-按解決方案類型、元件、部署模式、應用、最終用戶和地區分類的全球分析2026年全球ERP和ECM整合市場報告2026年企業資源規劃(ERP)區塊鏈全球市場報告亞太地區企業資源規劃(ERP):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 2026-2030年全球企業資源規劃系統整合與諮詢市場

2026-2030年全球企業資源規劃系統整合與諮詢市場