|

市場調查報告書

商品編碼

2044071

美國平板玻璃:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)United States Flat Glass - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

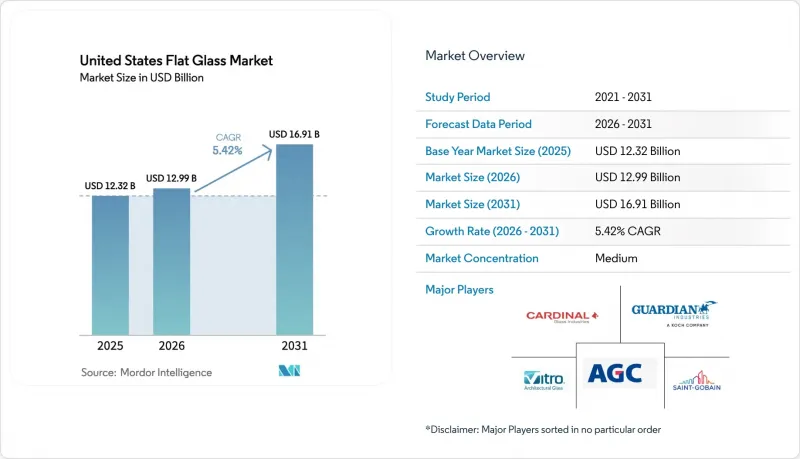

美國平板玻璃市場預計將從 2025 年的 123.2 億美元成長到 2026 年的 129.9 億美元,到 2031 年將達到 169.1 億美元,2026 年至 2031 年的複合年成長率為 5.42%。

隨著太陽能發電安裝激勵措施、強制性節能維修以及電動車對玻璃的需求重塑籌資策略,市場需求正從通用浮法玻璃轉向利潤更高的鍍膜和加工產品。美國平板玻璃市場也面臨技術純熟勞工短缺和日益嚴格的碳排放法規,這些因素推高了營運成本,促使生產商轉向高附加價值領域,以期透過定價權抵消遵循成本。垂直整合的太陽能玻璃生產商已經確保了永續的利潤率,而傳統的建築玻璃供應商即使在最近的反傾銷措施之後,仍然面臨日益激烈的進口競爭。七家美國本土浮法玻璃製造商之間的整合正在推進,而下游加工產業蓬勃發展,導致供應鏈上各企業的議價能力有顯著差異。整體而言,美國平板玻璃市場現在更重視那些不僅能提供產量,還能提供多層夾膠、動態著色或超低低輻射濺鍍技術的公司。

美國平板玻璃市場的趨勢與洞察

透過IRA激勵措施擴大國內太陽能板製造業

根據《聯邦稅法》第45X條,平方公尺太陽能玻璃可享有12美元的稅額扣抵,從而支持數十億美元的待開發區案。這使得垂直整合的生產線不易受到消費級浮法玻璃價格波動的影響。 First Solar公司將於2025年在路易斯安那州和阿拉巴馬州新增3.5吉瓦的生產線,使其在美國的產能達到14吉瓦。 Pilkington公司已將其位於俄亥俄州羅斯福的浮法玻璃廠改造為透明導電氧化物(TCO)的供應基地。這表明,在美國平板玻璃市場,出現了具有各自成本因素的平行太陽能基板供應鏈。貸款專案辦公室的指南進一步降低了資金籌措門檻,並鼓勵新參與企業將目標鎖定在太陽能玻璃而非建築浮法玻璃領域。

節能建築的建造和維修活動活性化

根據《通膨控制法案》(IRA) 資助的聯邦服務管理局 (GSA) 採購要求,頂級平板玻璃的碳含量上限為每噸 1331 公斤二氧化碳當量 (CO2e),這促使市場需求轉向玻璃屑比例更高的熔爐以及採用電力輔助加熱的熔爐。伯克利實驗室的研究表明,低輻射 (Low-E) 塗層已應用於美國 80% 的住宅,但 U 值低於 0.20 的三層玻璃正逐漸成為新的維修標準。這一趨勢正在推動美國平板玻璃市場的發展,因為加工商可以實現間隔條和邊緣密封生產線的自動化,從而獲得每平方英尺價值的提升。

加強美國浮動反應器碳排放法規

除了美國環保署N子部分規定的報告義務外,CC子部分規定的顆粒物和硫氧化物排放限制也要求進行成本高昂的排放維修。 Guardian公司於2024年關閉位於加州金斯堡的浮法玻璃廠,凸顯了其對當地能源和碳政策的脆弱性。生產商被迫在投資提升電壓、搬遷或退出通用浮法玻璃業務之間做出選擇,這將使美國平板玻璃市場轉向高價值塗層,因為合規成本可以透過利潤來抵消。

細分市場分析

2025年,退火玻璃佔總銷售額的62.33%,但隨著颶風、爆炸以及更嚴格的建築規範等因素導致更多應用轉向強化玻璃和夾層玻璃,其市場佔有率正在下降。在預測期(2026-2031年)內,加工玻璃的複合年成長率(CAGR)為6.78%,超過了美國平板玻璃市場的整體成長率。隨著建築規範的日益普及,美國加工平板玻璃市場規模不斷擴大,這有利於那些能夠快速完成從切割、鋼化到封邊等所有工序的一體化工廠。

將強化、層壓、充氣和品質檢測整合到一條生產線上的加工商,其每平方英尺的收入比銷售單一鋼化玻璃產品的競爭對手高出約30%至40%。格拉斯頓和芬齊的E-Coat電泳塗裝平台的廣泛應用,凸顯了資本投資向下游自動化領域的轉變,進一步鞏固了加工產品在美國平板玻璃市場的主導地位。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 電子顯示器需求不斷成長

- 增加旨在提高建築能源效率的維修工程

- 透過IRA獎勵擴大國內太陽能板製造業

- 關於輕型汽車和安全玻璃的法規

- 商業地產中動態智慧玻璃的興起

- 市場限制因素

- 加強美國浮動反應器碳排放法規

- 先進玻璃加工業技術純熟勞工短缺

- 與進口低成本加工玻璃的競爭。

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 依產品類型

- 退火玻璃(包括彩色玻璃)

- 鍍膜玻璃

- 花紋玻璃

- 加工玻璃

- 鏡子

- 按塗層類型

- 低輻射(硬地)

- 隔熱(軟塗層)

- 自清潔

- 防反射

- 其他

- 按最終用戶行業分類

- 建築/施工

- 車

- 太陽能玻璃

- 其他終端用戶產業(電子、航太等)

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- AGC Inc.

- CARDINAL GLASS INDUSTRIES, INC

- Central Glass Co., Ltd.

- China CSG Group Co., Ltd.

- Corning Incorporated

- First Solar

- Fuyao Group

- Guardian Industries

- Nippon Sheet Glass Co., Ltd

- Saint-Gobain

- SCHOTT

- Sisecam

- Specialty Glass Products

- Swift Glass

- Vitro

- Xinyi Glass Holdings Limited

第7章 市場機會與未來展望

The United States Flat Glass Market size is expected to grow from USD 12.32 billion in 2025 to USD 12.99 billion in 2026 and is forecast to reach USD 16.91 billion by 2031 at a 5.42% CAGR over 2026-2031.

Demand is pivoting from commodity float toward higher-margin coated and processed products as solar-manufacturing incentives, energy-efficient retrofit mandates, and electric-vehicle glazing needs reshape procurement strategies. The United States flat glass market is also contending with skilled-labor shortages and tightening carbon rules that raise operating costs, nudging producers toward value-added segments where pricing power offsets compliance outlays. Vertically integrated solar-glass producers are already securing sustainable margins, while traditional architectural suppliers face intensified import competition even after recent anti-dumping actions. Consolidation among the seven domestic float operators co-exists with a vibrant downstream fabricator base, so customer leverage varies sharply along the chain. Overall, the United States flat glass market now rewards firms that can deliver multi-layer lamination, dynamic tinting, or ultra-low-emissivity sputtering rather than raw tonnage alone.

United States Flat Glass Market Trends and Insights

Expansion of Domestic Solar-Panel Manufacturing Under IRA Incentives

Federal Section 45X credits pay USD 12 per m2 of solar glass, underpinning multi-billion-dollar greenfield projects that insulate vertically integrated lines from merchant-float volatility. First Solar added 3.5 GW lines in Louisiana and Alabama in 2025, bringing the United States' capacity to 14 GW. Pilkington converted its Rossford, Ohio float into a transparent-conductive-oxide supply, illustrating how the United States flat glass market is birthing a parallel solar substrate chain with distinct cost drivers. Loan Programs Office guidance further lowers financing barriers, encouraging new entrants to target solar rather than architectural float.

Rising Construction-Retrofit Activity for Energy-Efficient Buildings

IRA-funded General Services Administration procurement now specifies low-embodied-carbon limits of 1,331 kg CO2e (carbon dioxide-equivalent)/ton for top-tier flat glass, shifting demand toward furnaces with high cullet ratios or electric boosting. Berkeley Lab finds Low-E coatings already cover 80% of United States homes, yet triple-pane units with U-factors below 0.20 are emerging as the next retrofit standard. That dynamic elevates the United States flat glass market as fabricators are able to automate spacer-bar and edge-seal lines, capturing rising per-square-foot values.

Tightening US Carbon-Emission Rules on Float Furnaces

EPA Subpart N reporting plus particulate and SOx limits under Subpart CC compel costly abatement retrofits; Guardian's 2024 closure of its Kingsburg, California float underscores vulnerability to regional energy and carbon policies. Producers must decide whether to invest in electric boosting, relocate, or exit commodity float, pushing the United States flat glass market toward high-value coatings where margins can absorb compliance premiums.

Other drivers and restraints analyzed in the detailed report include:

- Automotive Lightweighting and Safety-Glazing Mandates

- Growing Demand for Electronic Displays

- Skilled-Labor Shortages in Advanced Glass Processing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Annealed Glass retained 62.33% of 2025 revenue, yet its share is slipping as hurricanes, blasts, and overhead codes move more applications to tempered or laminated forms. Processed Glass expanded at a 6.78% CAGR during the forecast period (2026-2031), outstripping the overall United States Flat Glass market. The United States flat glass market size for processed offerings rose in tandem with code adoption, rewarding integrated shops able to move quickly from cutting to tempering to edge-sealing.

Fabricators that consolidate tempering, laminating, gas filling, and quality inspection on one line earn roughly 30-40% higher revenue per square foot than peers selling stand-alone annealed sheets. New installs from Glaston and Fenzi's E-Coat printing platform validate the capital shift toward downstream automation, reinforcing the momentum behind processed product leadership inside the United States Flat Glass market.

The United States Flat Glass Market Report is Segmented by Product Type (Annealed Glass (Including Tinted Glass), Coater Glass, Patterned Glass, and More), Coating Type (Low-E (Hard-Coat), Solar-Control (Soft-Coat), and More), End-User Industry (Building and Construction, Automotive, Solar Glass, and Other End-User Industries (Electronics, Aerospace, and More)). The Market Size and Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- AGC Inc.

- CARDINAL GLASS INDUSTRIES, INC

- Central Glass Co., Ltd.

- China CSG Group Co., Ltd.

- Corning Incorporated

- First Solar

- Fuyao Group

- Guardian Industries

- Nippon Sheet Glass Co., Ltd

- Saint-Gobain

- SCHOTT

- Sisecam

- Specialty Glass Products

- Swift Glass

- Vitro

- Xinyi Glass Holdings Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand for electronic displays

- 4.2.2 Rising construction-retrofit activity for energy-efficient buildings

- 4.2.3 Expansion of domestic solar-panel manufacturing under IRA incentives

- 4.2.4 Automotive lightweighting and safety-glazing mandates

- 4.2.5 Emergence of dynamic/smart glass in commercial real estate

- 4.3 Market Restraints

- 4.3.1 Tightening US carbon-emission rules on float furnaces

- 4.3.2 Skilled-labor shortages in advanced glass processing

- 4.3.3 Competition from imported low-cost processed glass

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Annealed Glass (Including Tinted Glass)

- 5.1.2 Coater Glass

- 5.1.3 Patterned Glass

- 5.1.4 Processed Glass

- 5.1.5 Mirrors

- 5.2 By Coating Type

- 5.2.1 Low-E (Hard-Coat)

- 5.2.2 Solar-Control (Soft-Coat)

- 5.2.3 Self-Cleaning

- 5.2.4 Anti-Reflective

- 5.2.5 Others

- 5.3 By End-User Industry

- 5.3.1 Building and Construction

- 5.3.2 Automotive

- 5.3.3 Solar Glass

- 5.3.4 Other End-user Industries (Electronics, Aerospace, and more)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 AGC Inc.

- 6.4.2 CARDINAL GLASS INDUSTRIES, INC

- 6.4.3 Central Glass Co., Ltd.

- 6.4.4 China CSG Group Co., Ltd.

- 6.4.5 Corning Incorporated

- 6.4.6 First Solar

- 6.4.7 Fuyao Group

- 6.4.8 Guardian Industries

- 6.4.9 Nippon Sheet Glass Co., Ltd

- 6.4.10 Saint-Gobain

- 6.4.11 SCHOTT

- 6.4.12 Sisecam

- 6.4.13 Specialty Glass Products

- 6.4.14 Swift Glass

- 6.4.15 Vitro

- 6.4.16 Xinyi Glass Holdings Limited

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

平板玻璃加工機械市場 - 全球產業規模、佔有率、趨勢、機會、預測:機器類型、終端用戶產業、玻璃類型、自動化程度、地區及競爭格局,2021-2031年平板玻璃市場-全球產業規模、佔有率、趨勢、機會和預測:按產品類型、技術、終端用戶產業、地區和競爭格局分類,2021-2031年

平板玻璃加工機械市場 - 全球產業規模、佔有率、趨勢、機會、預測:機器類型、終端用戶產業、玻璃類型、自動化程度、地區及競爭格局,2021-2031年平板玻璃市場-全球產業規模、佔有率、趨勢、機會和預測:按產品類型、技術、終端用戶產業、地區和競爭格局分類,2021-2031年 平板玻璃市場:按產品類型、鍍膜類型、應用、最終用途和分銷管道分類-全球市場預測(2026-2032 年)

平板玻璃市場:按產品類型、鍍膜類型、應用、最終用途和分銷管道分類-全球市場預測(2026-2032 年) 2026年全球平板玻璃市場報告平板玻璃製造機械市場:依產品類型、機器類型、技術、原料、產能和最終用途分類-全球預測,2026-2032年

2026年全球平板玻璃市場報告平板玻璃製造機械市場:依產品類型、機器類型、技術、原料、產能和最終用途分類-全球預測,2026-2032年 平板玻璃市場規模、佔有率、趨勢和預測:按技術、產品類型、原料、應用、類別、最終用途行業和地區分類,2026-2034年

平板玻璃市場規模、佔有率、趨勢和預測:按技術、產品類型、原料、應用、類別、最終用途行業和地區分類,2026-2034年 平板玻璃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)歐洲平板玻璃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本平板玻璃市場報告(按技術、產品類型、最終用途行業和地區分類,2026-2034年)

平板玻璃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)歐洲平板玻璃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本平板玻璃市場報告(按技術、產品類型、最終用途行業和地區分類,2026-2034年) 平板玻璃市場規模、佔有率和成長分析(按產品類型、技術、終端用戶產業和地區分類)-2026-2033年產業預測

平板玻璃市場規模、佔有率和成長分析(按產品類型、技術、終端用戶產業和地區分類)-2026-2033年產業預測