|

市場調查報告書

商品編碼

2044064

中國資料中心機櫃:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)China Data Center Rack - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

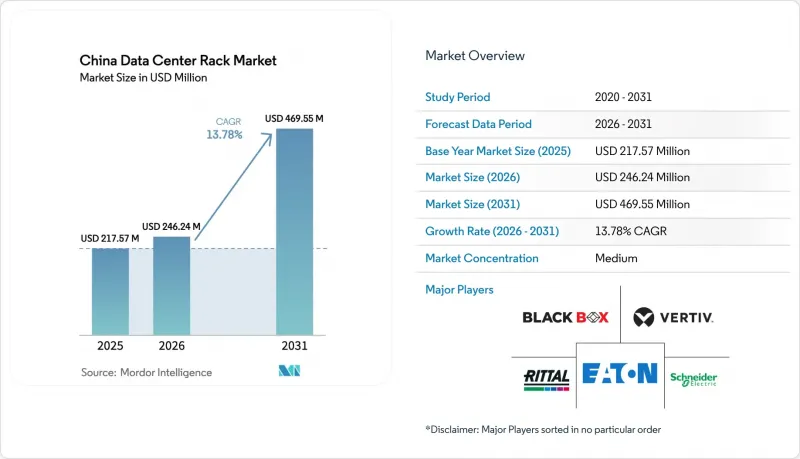

中國資料中心機架市場預計將從 2025 年的 2.1757 億美元成長到 2026 年的 2.4624 億美元,然後從 2026 年到 2031 年以 13.78% 的複合年成長,到 2031 年達到 4.6955 億美元成長率。

「東方數據,西方運算」政策正在加速需求成長,因為超大規模工作負載正向內陸轉移,這些地區擁有更便宜的可再生能源和適宜自然冷卻的氣候。液冷機櫃曾經是小眾產品,如今已成為主流,因為人工智慧(AI)叢集的機架功率密度已超過30千瓦。國營通訊業者正在標準化採用母線槽配電和工廠封閉式的全高機櫃,以縮短安裝時間並提高區域統一性。同時,中型企業和5G營運商更傾向於為安裝空間有限的邊緣節點選擇緊湊的半高配置。在此背景下,能夠提供預先試運行機架(整合式電源、遙測和冷卻迴路)的供應商正受到超大規模資料中心業者和託管服務供應商的青睞。

中國資料中心機櫃市場趨勢及洞察。

雲端運算和人工智慧工作負載的激增正在推動對高密度機架的需求。

人工智慧 (AI)叢集目前每個機架的功耗超過 30 千瓦,迫使營運商改造原有的機櫃,加裝原本設計用於 8-12 千瓦的液冷歧管。華為的 CloudMatrix 384 測試平台表明,每台伺服器搭載 8 個 H100 級加速器需要將電源供給能力提升至 50 千瓦。預計到 2025 年,國內 AI 相關收入將超過 410 億美元,到 2028 年將達到 960 億美元。雖然金融和醫療保健等敏感行業僅佔伺服器需求的 5%,但它們對具備防篡改功能的本地機櫃需求旺盛,這就要求機架配備主動冷卻和安全功能。根據 Dell'Oro Group 的一份報告,2026 年第一季液冷產品的直接銷售量將成長一倍以上,這反映出 600 千瓦機架所需的母線槽電源軌的需求將激增 40%。這些因素共同推動中國資料中心機架市場朝向更高功率容量、更先進的遙測技術和工廠整合冷卻迴路發展。

擴大超大規模和託管設施的採用

GDS Holdings在2024年第三季獲得了8.8萬平方公尺的新增閒置頻段,而BroadNet計劃到2025年中期運營7.2萬個機櫃,併計劃再增加23萬個機櫃。領先的託管企業正在採用標配匯流排、PDU和機櫃的Scorpio機架,從而減少60%的現場人力成本。甘肅國家電網的雲端節點已投資1.37億美元購置了3,000個機架,凸顯了承包機架部署的資本密集特性。超大規模資料中心業者營運商現在透過與製造商簽訂多年合約直接採購機架,繞過分銷商,這種做法使不具備協同設計能力的小規模供應商處於不利地位。 VNET 集團 2024 年第三季的營收年增 14.3%,這主要得益於強勁的託管需求,凸顯了營運商按季度供應數千個相同機櫃所帶來的規模經濟效益。

刀片式和整合系統減少了傳統機架的數量。

超融合設備將運算、儲存和網路功能整合到單一底盤中,從而減少了銀行、金融和保險 (BFSI) 行業及其分店的機架面積。雖然出貨量有所下降,但由於融合機櫃需要更堅固的框架、雙匯流排和加固腳輪,平均售價卻在上漲。維修到三級網路的企業通常會將機櫃尺寸從 42U 升級到 48U,這在一定程度上緩解了出貨量下降的影響。因此,供應商面臨一個微妙的挑戰:機櫃數量正在減少,而每個機櫃的容量卻在增加。競爭優勢在於能夠提供可承受 1500 公斤靜態負載且不影響氣流的加固機殼。

細分市場分析

在中國,半機架的複合年成長率高達14.54%,遠超過整體資料中心機櫃市場。這主要得益於微型邊緣站點和5G無線節點對緊湊型、高可靠性機架的需求。隨著通訊業者在路邊基地台附近部署能夠抵禦灰塵和潮濕環境的IP65防護等級機櫃,中國資料中心機櫃市場半機架的尺寸也不斷擴大。儘管邊緣部署的功耗很少超過3-4千瓦,但仍需要生物識別鎖和遠端遙測技術來防止人為破壞。相較之下,預計到2025年,全機架的市佔率將達到71.32%,這主要得益於超大規模資料中心合約對42U和48U Scorpio機架的標準化。這些更大的機殼能夠最佳化氣流和佈線路徑,縮短組裝時間,並提高多個園區之間的一致性。

全高機櫃仍將是超大規模資料中心的標配。這是因為,雖然業者批量採購貨櫃單元會壓縮利潤空間,但工廠的產量卻變得可預測。四分之一機架和壁掛式微型機櫃仍然在零售連鎖店和分店中使用,這些場所更注重美觀而非密度。浪潮專為沙漠環境打造的「沙漠之舟」系列機櫃,能夠承受各種溫度環境並配備防塵過濾器,象徵資料中心向機櫃的轉變,目前正在中國西部風電帶重新推出。此系列機櫃交付預先佈線的快速部署設計,可將安裝時間縮短高達 40%,為急於運作新機房的託管服務提供者帶來顯著的生產力優勢。

到2025年,封閉式機櫃將佔據75.33%的市場。這反映了銀行、金融和保險(BFSI)行業在防篡改檢測、電磁干擾屏蔽和抗震加固方面的嚴格監管。受網路風險監管力度加大的推動,預計該細分市場將以14.76%的複合年成長率成長,超過中國整體資料中心機櫃市場的成長速度。對於訪問受限且氣流效率至關重要的超超大規模資料中心業者資料中心而言,開放式機櫃仍然很受歡迎。然而,超大規模資料中心業者正在增加網狀門和盲點攝影機的部署,從而縮小成本差距。

壁掛式和微邊框機架在物聯網閘道器、零售POS中心和智慧工廠單元中越來越受歡迎。因此,封閉式機櫃仍然主導中國資料中心機櫃市場,因為企業仍然優先考慮實體合規性而非降低初始成本。Schneider Electric和Vertiv透過模組化配件(垂直PDU、帶刷條的入侵面板、環境探頭等)直接展開競爭,這些配件可以無縫整合到各自的EcoStruxure和Vertiv Life平台中,使用戶能夠存取集中管理電源和熱數據的儀表板。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 擴大超大規模和託管設施的採用

- 雲端運算和人工智慧工作負載的激增正在推動對高密度機架的需求。

- 政府的「東方數據,西方計算」舉措正在加速建設。

- 碳中和法規正在推動水冷機架的普及。

- 建造 5G 邊緣網路需要在基地台採用緊湊型微型機架。

- 隨著 BFSI(以建構為中心的安全整合商)產業對數位核心升級的需求不斷成長,需要安全的本地機架。

- 市場限制因素

- 刀片式和整合系統減少了傳統機架的數量。

- 由於主要城市的土地和電力分配受到限制,資料中心的許可批准變得更加嚴格。

- 美國對高性能晶片的出口限制正在減緩超高密度機架的普及。

- 先進機架整合和維護方面的技術純熟勞工短缺

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 買方的議價能力

- 供應商的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模與成長預測

- 按機架尺寸

- 四分之一機架(11U 或更大)

- 半機架(12-22U)

- 整機架(42U 或以上)

- 按機架類型

- 密封櫃

- 開放式框架

- 壁掛式和微邊框外殼

- 層級類型

- 一級和二級

- 三級

- 第四級

- 按資料中心規模

- 小規模資料中心

- 中型資料中心

- 大型資料中心

- 超大規模資料中心

- 依資料中心類型

- 託管資料中心

- 超大規模資料中心業者資料中心/雲端服務供應商

- 企業和邊緣資料中心

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Eaton Corporation

- Black Box Corporation

- Rittal GmbH and Co. KG

- Schneider Electric SE

- Vertiv Group Corp.

- Dell Technologies Inc.

- nVent Electric PLC

- Hewlett Packard Enterprise

- Legrand SA

- Fujitsu Corporation

- Huawei Technologies Co. Ltd.

- Inspur Group

- Sugon Information Industry

- ZTE Corporation

- GreatIoT(Shenzhen)Technology

- Tripp Lite by Eaton

- Panduit Corp.

- Belden Inc.

- CyberPower Systems

- StarTech.com

第7章 市場機會與未來展望

The China data center rack market size is expected to grow from USD 217.57 million in 2025 to USD 246.24 million in 2026 and is forecast to reach USD 469.55 million by 2031 at a 13.78% CAGR over 2026-2031.

Demand is accelerating as the Eastern Data, Western Computing policy moves hyperscale workloads toward inland hubs that offer inexpensive renewable energy and free-cooling climates. Liquid-cooling cabinets, once niche, now command mainstream adoption because rack power densities have climbed past 30 kilowatts in artificial-intelligence clusters. State-owned carriers are standardizing on full-height cabinets with busway distribution and factory-installed containment, thereby reducing installation time and improving consistency across regions. Mid-sized enterprises and 5G operators, meanwhile, favor compact half-height formats for edge nodes where floor space is constrained. Against this backdrop, vendors able to ship pre-commissioned rows with integrated power, telemetry, and coolant loops capture growing preference from both hyperscalers and colocation providers.

China Data Center Rack Market Trends and Insights

Surge in Cloud and AI Workloads Driving High-Density Rack Demand

Artificial-intelligence clusters now exceed 30 kilowatts per rack, forcing operators to retrofit old cabinets with liquid manifolds designed for only 8-12 kilowatts. Huawei's CloudMatrix 384 testbed showed that power delivery must scale to 50 kilowatts to host eight H100-class accelerators per server. Domestic AI revenues surpassed USD 41 billion in 2025 and could top USD 96 billion by 2028. Sensitive sectors such as finance and healthcare account for only 5% of server demand but insist on on-prem cabinets with tamper detection, nudging racks toward active cooling and security functions. Dell'Oro Group reported that direct liquid-cooling revenue more than doubled in Q1 2026, mirroring a 40% surge in busway power rails needed for 600-kilowatt rows. Together, these forces propel the China data center rack market toward higher wattages, richer telemetry, and factory-integrated coolant loops.

Increasing Deployment of Hyperscale and Colocation Facilities

GDS Holdings committed 88,000 square meters of new white space in Q3 2024, while BroadNet operated 72,000 cabinets by mid-2025 with another 230,000 in pipeline. Colocation leaders standardize on Scorpio frames that arrive with busbars, PDUs, and containment, cutting on-site labor by 60%. Gansu State Grid's cloud node invested USD 137 million for 3,000 racks, underscoring the capital intensity of turnkey rows. Hyperscalers now bypass distributors, locking multi-year rack contracts directly with manufacturers, a practice that disadvantages small vendors lacking co-engineering capacity. VNET Group's Q3 2024 revenue climbed 14.3% year-over-year on persistent colocation demand, spotlighting the scale dividends accruing to players that can deliver thousands of identical cabinets each quarter.

Blade and Converged Systems Reducing Traditional Rack Counts

Hyper-converged appliances pack compute, storage, and networking into a single chassis, trimming rack footprints for BFSI and branch sites. Although unit shipments decline, average selling prices rise because converged cabinets need heavier frames, dual busbars, and reinforced casters. Enterprises retrofitting three-tier networks often upsize from 42U to 48U formats, partially cushioning unit erosion. Vendors therefore face a nuanced threat; fewer cabinets but richer content per cabinet. Competitive positioning hinges on supplying reinforced enclosures that can handle 1,500-kilogram static loads without sacrificing airflow.

Other drivers and restraints analyzed in the detailed report include:

- Government Eastern Data, Western Computing Initiative Accelerating Build-Outs

- Carbon-Neutral Mandates Fostering Liquid-Cooling-Ready Rack Adoption

- Land and Power Quota Caps in Tier-1 Cities Tightening Data-Center Approvals

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Half racks will outpace the broader China data center rack market with a 14.54% CAGR because micro edge sites and 5G radio nodes need compact, rugged formats. The China data center rack market size for half racks is expanding as operators install cabinets rated IP65 to handle dust and moisture near street-level base stations. Edge deployments seldom exceed 3-4 kilowatts, yet still demand biometric locks and remote telemetry to deter vandalism. In contrast, full racks secured 71.32% of share in 2025 thanks to hyperscale contracts that standardize on 42U and 48U Scorpio frames. These larger enclosures streamline airflow and cable routes, lowering assembly hours and boosting consistency across multiple campuses.

Full-height formats will remain the backbone inside hyperscale halls because operators buy them in container-load volumes, compressing margins but creating predictable factory throughput. Quarter racks and wall-mount micro enclosures persist in retail chains and branch offices where aesthetics trump density. Inspur's desert-rated "Desert Ship" family highlights the march toward wide-temperature, dust-filtered cabinets that are now repatriating to western China wind belts. Rapid-deploy designs that arrive pre-cabled slash installation times by up to 40%, a productivity edge valued by colocation providers racing to bring new halls online.

Enclosed cabinets held 75.33% share in 2025, reflecting strict BFSI rules for tamper detection, EMI shielding, and seismic anchoring. The segment will grow faster than the overall China data center rack market, advancing 14.76% CAGR as cyber-risk regulations tighten. Open-frame racks remain favored by hyperscalers where access is already restricted and airflow efficiency is paramount. Even so, hyperscale operators increasingly add mesh-door inserts and blind-spot cameras, narrowing the cost gap.

Wall-mount and micro-edge styles gain traction in IoT gateways, retail checkout hubs, and smart-factory cells. The China data center rack market share for enclosed cabinets therefore remains dominant because enterprises continue to prioritize physical compliance features over initial cost savings. Schneider Electric and Vertiv compete head-to-head with modular accessories vertical PDUs, brush strip ingress panels, and environmental probes that integrate seamlessly into their respective EcoStruxure and Vertiv Life platforms, giving operators unified dashboards for power and thermal data.

The China Data Center Rack Market Report is Segmented by Rack Size (Quarter Rack, Half Rack, and Full Rack), Rack Type (Enclosed Cabinet, Open-Frame, and Wall-Mount and Micro-Edge Enclosure), Tier Type (Tier 1 and 2, Tier 3, and Tier 4), Data Center Size (Small, Medium, Large, and Hyperscale), Data Center Type (Colocation, Hyperscalers/CSPs, and Enterprise and Edge). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Eaton Corporation

- Black Box Corporation

- Rittal GmbH and Co. KG

- Schneider Electric SE

- Vertiv Group Corp.

- Dell Technologies Inc.

- nVent Electric PLC

- Hewlett Packard Enterprise

- Legrand SA

- Fujitsu Corporation

- Huawei Technologies Co. Ltd.

- Inspur Group

- Sugon Information Industry

- ZTE Corporation

- GreatIoT (Shenzhen) Technology

- Tripp Lite by Eaton

- Panduit Corp.

- Belden Inc.

- CyberPower Systems

- StarTech.com

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Deployment of Hyperscale and Colocation Facilities

- 4.2.2 Surge in Cloud and AI Workloads Driving High-Density Rack Demand

- 4.2.3 Government "Eastern Data, Western Computing" Initiative Accelerating Build-Outs

- 4.2.4 Carbon-Neutral Mandates Fostering Liquid-Cooling-Ready Rack Adoption

- 4.2.5 5G Edge Build-Outs Requiring Compact Micro-Racks in Base Stations

- 4.2.6 Rising BFSI Digital-Core Upgrades Requiring Secure On-Prem Racks

- 4.3 Market Restraints

- 4.3.1 Blade and Converged Systems Reducing Traditional Rack Counts

- 4.3.2 Land and Power Quota Caps in Tier-1 Cities Tightening Data-Center Approvals

- 4.3.3 U.S. Export-Control Limits on High-End Chips Slowing Ultra-Dense Rack Roll-Outs

- 4.3.4 Skilled-Labor Shortages for Advanced Rack Integration and Maintenance

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Rack Size

- 5.1.1 Quarter Rack (More than 11U)

- 5.1.2 Half Rack (12-22U)

- 5.1.3 Full Rack (More than Equal to 42U)

- 5.2 By Rack Type

- 5.2.1 Enclosed Cabinet

- 5.2.2 Open-Frame

- 5.2.3 Wall-Mount and Micro-Edge Enclosure

- 5.3 By Tier Type

- 5.3.1 Tier 1 and 2

- 5.3.2 Tier 3

- 5.3.3 Tier 4

- 5.4 By Data Center Size

- 5.4.1 Small Data Center

- 5.4.2 Medium Data Center

- 5.4.3 Large Data Center

- 5.4.4 Hyperscale Data Center

- 5.5 By Data Center Type

- 5.5.1 Colocation Data Center

- 5.5.2 Hyperscalers Data Center/CSPs

- 5.5.3 Enterprise and Edge Data Center

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 Eaton Corporation

- 6.4.2 Black Box Corporation

- 6.4.3 Rittal GmbH and Co. KG

- 6.4.4 Schneider Electric SE

- 6.4.5 Vertiv Group Corp.

- 6.4.6 Dell Technologies Inc.

- 6.4.7 nVent Electric PLC

- 6.4.8 Hewlett Packard Enterprise

- 6.4.9 Legrand SA

- 6.4.10 Fujitsu Corporation

- 6.4.11 Huawei Technologies Co. Ltd.

- 6.4.12 Inspur Group

- 6.4.13 Sugon Information Industry

- 6.4.14 ZTE Corporation

- 6.4.15 GreatIoT (Shenzhen) Technology

- 6.4.16 Tripp Lite by Eaton

- 6.4.17 Panduit Corp.

- 6.4.18 Belden Inc.

- 6.4.19 CyberPower Systems

- 6.4.20 StarTech.com

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

資料中心機櫃市場 - 全球產業規模、佔有率、趨勢、機會、預測:按組件、機架類型、資料中心規模、機架高度、產業垂直領域、地區和競爭格局分類,2021-2031年

資料中心機櫃市場 - 全球產業規模、佔有率、趨勢、機會、預測:按組件、機架類型、資料中心規模、機架高度、產業垂直領域、地區和競爭格局分類,2021-2031年 資料中心機架式配電單元市場規模、佔有率和成長分析:按類型、相數、安裝方式、額定功率、資料中心類型、應用和地區分類-2026年至2033年產業預測

資料中心機架式配電單元市場規模、佔有率和成長分析:按類型、相數、安裝方式、額定功率、資料中心類型、應用和地區分類-2026年至2033年產業預測 全球OCP機架市場:依最終用戶、應用程式和地區分類-預測至2030年

全球OCP機架市場:依最終用戶、應用程式和地區分類-預測至2030年 資料中心機櫃市場分析及預測(至2035年):類型、產品類型、服務、技術、應用、材質、最終用戶、安裝配置

資料中心機櫃市場分析及預測(至2035年):類型、產品類型、服務、技術、應用、材質、最終用戶、安裝配置 資料中心機架市場規模、佔有率、趨勢和預測:按類型、框架單位、機架尺寸、框架尺寸、框架設計、服務、應用、最終用戶和地區分類,2026-2034 年

資料中心機架市場規模、佔有率、趨勢和預測:按類型、框架單位、機架尺寸、框架尺寸、框架設計、服務、應用、最終用戶和地區分類,2026-2034 年 全球資料中心機櫃市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球資料中心機櫃市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 資料中心機櫃市場:按機架類型、設計、承載能力、材質、應用、最終用戶和分銷管道分類-2026-2032年全球市場預測

資料中心機櫃市場:按機架類型、設計、承載能力、材質、應用、最終用戶和分銷管道分類-2026-2032年全球市場預測 2026年全球資料中心機櫃與機櫃市場報告

2026年全球資料中心機櫃與機櫃市場報告 資料中心機櫃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

資料中心機櫃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 全球資料中心機櫃用配電單元市場:市場規模、佔有率和趨勢分析(按機架類型和地區分類),細分市場預測(2026-2033 年)

全球資料中心機櫃用配電單元市場:市場規模、佔有率和趨勢分析(按機架類型和地區分類),細分市場預測(2026-2033 年)