|

市場調查報告書

商品編碼

2029871

全球OCP機架市場:依最終用戶、應用程式和地區分類-預測至2030年OCP Rack Market By Application (AI, High-performance computing, Data Management, Enterprise Apps & Others), End User (Retail Colocation, Enterprise, Neocloud Providers, Others - Hyperscalers/Wholesale Colocation) - Global Forecast to 2030 |

||||||

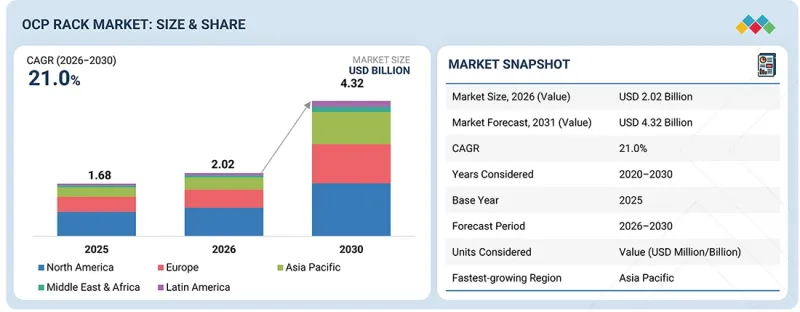

OCP機架市場正在快速擴張,預計將從2025年的16.8億美元成長到2030年的43.2億美元,複合年成長率為21.0%。

隨著資料處理越來越靠近終端用戶和設備,邊緣運算的擴展正成為OCP機架市場的重要驅動力。邊緣設施通常空間有限,需要緊湊、高效且易於部署的基礎設施。 OCP機架設計由開放式運算專案(Open Compute Project)開發,透過簡化的機械結構、模組化配置和高效的配電來滿足這些需求。

| 調查範圍 | |

|---|---|

| 調查期 | 2020-2030 |

| 基準年 | 2025 |

| 預測期 | 2026-2030 |

| 目標單元 | 金額(100萬/10億美元) |

| 部分 | 按應用程式、最終用戶、區域 |

| 目標區域 | 北美、歐洲、亞太地區、中東和非洲以及拉丁美洲 |

與大規模超大規模環境不同,邊緣環境部署通常優先考慮快速部署和跨多個分散位置的運作一致性。基於 OCP 的機架提供標準化設計,只需極少的客製化即可複製,從而縮短部署時間並降低整合複雜性。此外,它們能夠在更小的面積內提供高運算密度,滿足空間和電力資源有限的邊緣環境的需求。隨著邊緣應用場景的擴展,包括通訊、內容傳送和工業應用,對靈活且可擴展的機架解決方案的需求預計將會增加,從而推動 OCP 架構的日益普及。

“從應用領域來看,高效能運算(HPC)預計在預測期內將呈現市場第二高的成長率。”

高效能運算 (HPC) 預計將成為 OCP 機架市場中成長速度第二快的應用領域,這主要得益於科研、企業和工業應用場景中對運算密集型工作負載日益成長的需求。 HPC 環境需要高度整合的系統,具備高功率密度、低延遲網路和高效率的溫度控管。 OCP 機架架構透過支援更高的機架功率容量和先進的冷卻解決方案(包括液冷)來滿足這些需求。這使得營運商能夠在不超出設施限制的情況下部署高密度運算叢集。此外,HPC 工作負載通常需要可複製且擴充性的基礎設施設計,這與 OCP 機架的標準化方法相契合。隨著各組織機構在模擬、建模和人工智慧輔助運算方面能力的不斷提升,對高效且擴充性的HPC 基礎設施的需求也日益成長,從而加速了基於 OCP 的機架系統的普及。

“按最終用戶分類,預計在預測期內,‘其他’細分市場將佔據最大的市場佔有率。”

由大規模資料中心超大規模資料中心業者和批發託管服務提供者組成的「其他」細分市場預計將佔據OCP機架市場最大的佔有率,這主要得益於其基礎設施部署的規模和標準化程度。這些業者基於統一且可重複的架構建構和營運大型資料中心園區,而符合開放運算專案(OCP)標準的OCP機架在效率和可擴展性方面具有顯著優勢。超大規模資料中心超大規模資料中心業者正在部署基於OCP的系統來支援高密度工作負載,尤其是在人工智慧和雲端服務領域;而批發託管服務供應商則採用類似的設計來滿足大規模租戶的需求。投資客製化設施設計(包括高容量電源和液冷基礎設施)的能力進一步推動了OCP的普及。此外,這些營運商通常擁有長期規劃和充足的資本預算,這使他們能夠儘早採用新的機架架構。規模、標準化和基礎設施發展三者之間的協同作用,使得該細分市場成為OCP機架需求的最大驅動力。

“在預測期內,北美將引領OCP機架市場。”

由於北美地區超大規模容量的集中、對開放硬體標準的早期採用以及對人工智慧基礎設施的持續投資,預計該地區將在OCP機架市場佔據最大的市場佔有率。該地區匯集了大規模雲端服務供應商以及開放運算專案(OCP)生態系統的其他關鍵貢獻者,他們正在大規模地設計和部署基於OCP的架構。這些營運商已將其大部分基礎設施遷移到21英寸開放式機架設計,從而實現了高功率密度、高效的溫度控管以及跨多個園區的標準化部署。

人工智慧訓練和推理叢集的快速擴張正在推動市場發展。這主要是由於對機架級電源和冷卻進行最佳化的需求日益成長,尤其是在液冷和高容量匯流排系統應用日益普及的情況下。同時,北美批發託管服務供應商正在根據OCP(開放式資料中心)要求建造新設施,以支援超大規模租戶,這進一步刺激了市場需求。該地區在「機架級整合」方面也取得了持續進展,即將計算、網路和冷卻作為預整合系統而非獨立組件進行部署。這縮短了部署時間並圖了維運複雜性。再加上涵蓋OEM、ODM和基礎設施供應商的強大供應鏈,這些因素共同促成了北美成為OCP機架部署的領先市場。

本報告對OCP機架市場的主要參與者進行了詳細研究。本研究涵蓋的主要市場參與企業包括:Rittal(德國)、戴爾科技(美國)、Sanmina Corporation(美國)、Legrand(法國)、Vertiv(美國)、Eaton(愛爾蘭)、Belden(美國)、Wiwynn Corporation(台灣)、Lite-on Cloud Infrastructure(台灣)、Cheval Group、技技法(台灣)和Chat Product(台灣)。

調查範圍

本研究報告根據應用(人工智慧(訓練和推理)、高效能運算(HPC)、資料管理、企業應用程式等)、最終用戶(零售主機供應商、企業、雲端供應商等(超大規模資料中心業者/批發託管供應商))和地區(北美、歐洲、亞太地區、中東和非洲以及拉丁美洲)對 OCP 機架市場進行細分。

本報告深入分析了影響 OCP 機架市場的關鍵因素,包括促進因素、限制因素、挑戰和機會。該報告還全面分析了領先供應商的產品系列、機架級容量以及對開放計算項目 (OCP) 標準的合規性。此外,報告還探討了策略性舉措,例如與超大規模資料中心業者和原始設計製造商 ( 檢驗 ) 的夥伴關係、整個 OCP 生態系統的協作、機架設計的產品創新以及電源和冷卻整合,以及影響 OCP 機架市場格局的併購和最新發展動態。

購買本報告的理由

本報告為市場領導和新參與企業提供OCP機架市場及其細分市場最精確的銷售估計值。這有助於相關人員了解競爭格局,更有效地定位其產品和服務,並制定有效的打入市場策略。此外,本報告還透過對影響OCP機架市場的關鍵促進因素、限制因素、挑戰和機會進行詳細分析,幫助相關人員評估市場趨勢和動態。

本報告深入分析了以下幾點:

- 本報告深入分析了影響 OCP 機架市場的關鍵促進因素、阻礙因素、機會和挑戰。關鍵促進因素包括:人工智慧機架功率密度的提升推動了 OCP 的普及;機架級整合基礎設施取代了組件級部署;以及超大規模資料中心業者主導的標準化進程加速了 OCP 在全球範圍內的普及。阻礙因素包括:與傳統 19 吋機架基礎設施的兼容性較差,以及機房電源和冷卻系統初始改造成本較高。機會包括:將液冷(D2C 和浸沒式冷卻)整合到機架設計中,以及為超大規模和新雲端供應商提供支援人工智慧的預配置機架解決方案。關鍵挑戰包括:多廠商 OCP 生態系統中的互通性問題,以及舊有系統的複雜性影響了部署效率。

- 服務開發與創新:深入了解 OCP 機架市場的未來技術、研發活動以及新產品/服務發布。

- 市場發展:盈利市場的全面資訊-本報告分析了各個地區的OCP機架市場。

- 市場多元化:OCP機架市場新服務、未開發地區、近期趨勢和投資的全面訊息

- 競爭格局分析:本報告針對主要廠商(如Rittal(德國)、戴爾科技(美國)、Sanmina Corporation(美國)、Legrand(法國)、Vertiv(美國)、Eaton(愛爾蘭)、Belden(美國)、Wiwynn Corporation(台灣)、Lite-on Cloud Infrastructure(台灣)、Chevalstructure(台灣)、Cheval Group、sworth(台灣)、Cheval! Product(美國))的市場佔有率、成長策略和OCP機架產品進行了詳細評估。此外,本報告還提供了有關關鍵市場促進因素、限制、挑戰和機會的信息,幫助相關人員了解OCP機架市場。

目錄

第1章:引言

第2章 市場概覽

- 市場動態

- 促進因素

- 抑制因子

- 機會

- 任務

- 案例研究分析

- 分析:提高機架的功率密度能否從結構上減少所需的機架數量?

- 2030 年前 21 吋 OCP 機架千瓦演變分析

- 影響客戶業務的趨勢/顛覆性因素

- 價格分析

第3章:21吋OCP機架市場(依最終用戶分類)

- 零售商店託管服務提供者

- 企業版(本地部署)

- 新雲端提供者

- 其他

第4章:21吋OCP機架市場(依應用領域分類)

- 人工智慧(訓練和推理)

- 高效能運算(HPC)

- 資料管理

- 企業應用及其他

第5章:21吋OCP機架市場(依地區分類)

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 其他

- 亞太地區

- 中國

- 日本

- 印度

- 其他

- 中東和非洲

- GCC

- 南非

- 其他

- 拉丁美洲

- 巴西

- 墨西哥

- 其他

第6章:公司簡介

- 主要參與企業

- SANMINA CORPORATION

- DELL TECHNOLOGIES

- WIWYNN

- GIGABYTE

- EATON

- RITTAL

- LEGRAND

- RACK RENEW

- BELDEN

- CHEVAL GROUP

The OCP rack market is expanding rapidly, with the market projected to grow from USD 1.68 billion in 2025 to USD 4.32 billion by 2030, at a CAGR of 21.0%. The expansion of edge computing is emerging as a distinct driver for the OCP rack market, as data processing increasingly shifts closer to end users and devices. Edge facilities are typically space-constrained and require compact, efficient, and easily deployable infrastructure. OCP rack designs, developed under the Open Compute Project, support these requirements through simplified mechanical structures, modular configurations, and efficient power distribution.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2020-2030 |

| Base Year | 2025 |

| Forecast Period | 2026-2030 |

| Units Considered | Value (USD Million/Billion) |

| Segments | By Application, End User, Region |

| Regions covered | North America, Europe, Asia Pacific, the Middle East & Africa, and Latin America |

Unlike large hyperscale environments, edge deployments often prioritize rapid installation and operational consistency across multiple distributed sites. OCP-based racks enable standardized designs that can be replicated with minimal customization, reducing deployment time and integration complexity. In addition, the ability to support higher compute density within a smaller footprint aligns with edge requirements where real estate and power availability are limited. As edge use cases expand across telecom, content delivery, and industrial applications, demand for flexible and scalable rack solutions is expected to support increased adoption of OCP architectures.

"By application, the high-performance computing (HPC) is projected to be the second-fastest-growing in the market during the forecast period."

High-performance computing (HPC) is projected to be the second fastest-growing application in the OCP rack market, supported by increasing demand for compute-intensive workloads across research, enterprise, and industrial use cases. HPC environments require tightly integrated systems with high power density, low-latency networking, and efficient thermal management. OCP rack architectures address these requirements by supporting higher rack power capacities and enabling advanced cooling solutions, including liquid cooling. This allows operators to deploy dense compute clusters without exceeding facility constraints. In addition, HPC workloads often require repeatable and scalable infrastructure designs, which aligns with the standardized approach of OCP racks. As organizations expand simulation, modeling, and AI-assisted computing capabilities, the need for efficient and scalable HPC infrastructure is increasing, contributing to the accelerated adoption of OCP-based rack systems.

"By end user, the others segment is expected to hold the largest market value during the forecast period."

The "others" segment, comprising hyperscalers and wholesale colocation providers, is expected to hold the largest market value in the OCP rack market due to the scale and standardization of their infrastructure deployments. These operators build and operate large data center campuses designed for uniform, repeatable architectures, where OCP racks aligned with Open Compute Project standards provide clear advantages in terms of efficiency and scalability. Hyperscalers deploy OCP-based systems to support high-density workloads, particularly for AI and cloud services, while wholesale colocation providers adopt similar designs to meet the requirements of large tenants. Their ability to invest in custom facility design, including high-capacity power and liquid cooling infrastructure, further supports OCP adoption. Additionally, these players typically operate with long planning horizons and large capital budgets, enabling early adoption of new rack architectures. This combination of scale, standardization, and infrastructure readiness positions the segment as the largest contributor to OCP rack demand.

"North America leads the OCP rack market during the forecast."

North America is expected to hold the largest market value in the OCP rack market due to its concentration of hyperscale capacity, early adoption of open hardware standards, and continued investment in AI infrastructure. The region hosts major contributors to the Open Compute Project ecosystem, including large cloud providers that design and deploy OCP-based architectures at scale. These operators have already transitioned significant portions of their infrastructure to 21-inch Open Rack designs, enabling higher power density, efficient thermal management, and standardized deployments across multiple campuses.

The rapid expansion of AI training and inference clusters is driving the market as it requires rack-level optimization for power delivery and cooling, particularly with the increasing adoption of liquid cooling and high-capacity busbar systems. In parallel, wholesale colocation providers in North America are aligning new facility builds with OCP requirements to support hyperscale tenants, further reinforcing demand. The region is also seeing continued advancement in rack-scale integration, where compute, networking, and cooling are deployed as pre-integrated systems rather than discrete components. This reduces deployment timelines and operational complexity. Combined with strong supply chain presence across OEMs, ODMs, and infrastructure vendors, these factors position North America as the leading market for OCP rack deployments.

Breakdown of Primaries

In-depth interviews were conducted with Chief Executive Officers (CEOs), innovation and technology directors, system integrators, and executives from various key organizations operating in the OCP rack market.

- By Company: Tier 1 - 35%, Tier 2 - 45%, and Tier 3 - 20%

- By Designation: Directors - 35%, Managers - 25%, and Others - 40%

- By Region: North America - 25%, Europe - 45%, Asia Pacific - 25%, Middle East & Africa - 3%, and Latin America - 2%.

The report includes a detailed study of key players operating in the OCP rack market. The major market participants covered in the study include Rittal (Germany), Dell Technologies (US), Sanmina Corporation (US), Legrand (France), Vertiv (US), Eaton (Ireland), Belden (US), Wiwynn Corporation (Taiwan), Lite-on Cloud Infrastructure (Taiwan), Cheval Group, Gigabyte (Taiwan), and Chatsworth Product (US).

Research Coverage

This research report categorizes the OCP rack market based on applications By Applications (AI (training & inference), high performance computing (HPC), data management and enterprise apps & others)), By end users (retail colocation providers, enterprise, necloud providers and others (hyperscalers/ wholesale colocation providers) and Region (North America, Europe, Asia Pacific, Middle East & Africa, and Latin America).

The report's scope encompasses detailed insights into the key factors influencing the OCP rack market, including drivers, restraints, challenges, and opportunities shaping its growth. It provides a comprehensive analysis of leading vendors, covering their product portfolios, rack-scale capabilities, and alignment with standards defined by the Open Compute Project. The report also examines strategic initiatives such as partnerships with hyperscalers and ODMs, collaborations across the OCP ecosystem, product innovations in rack design, power and cooling integration, as well as mergers, acquisitions, and recent developments impacting the OCP rack market landscape.

Reason to Buy this Report

The report provides market leaders and new entrants with insights into the closest estimations of revenue for the overall OCP rack market and its subsegments. It enables stakeholders to understand the competitive landscape and gain actionable insights to better position their offerings and develop effective go-to-market strategies. Additionally, the report helps stakeholders assess market trends and dynamics by providing a detailed analysis of key drivers, restraints, challenges, and opportunities shaping the OCP rack market.

The report provides insights into the following points:

- The report provides insights into key drivers, restraints, opportunities, and challenges shaping the OCP rack market. Major drivers include AI rack power density exceeding driving OCP adoption, rack-scale integrated infrastructure replacing component-level deployments, and hyperscaler-led standardization accelerating global OCP adoption. Restraints include limited compatibility with legacy 19-inch rack infrastructure and high upfront redesign costs for facility power and cooling systems. Opportunities include integration of liquid cooling (D2C and immersion) within rack designs, pre-configured AI-ready rack solutions for hyperscale and neo-cloud players. Key challenges include interoperability issues in multi-vendor OCP ecosystems and legacy system complexity impacting deployment efficiency.

- Services Development/Innovation: Detailed insight into upcoming technologies, research & development activities, and new product & service launches in the OCP rack market

- Market Development: Comprehensive information about lucrative markets - the report analyses the OCP rack market across varied regions

- Market Diversification: Exhaustive information about new services, untapped geographies, recent developments, and investments in the OCP rack market

- Competitive Assessment: In-depth assessment of market shares, growth strategies and OCP rack offerings of leading players such as Rittal (Germany), Dell Technologies (US), Sanmina Corporation (US), Legrand (France), Vertiv (US), Eaton (Ireland), Belden (US), Wiwynn Corporation (Taiwan), Lite-on Cloud Infrastructure (Taiwan), Cheval Group, Gigabyte (Taiwan), and Chatsworth Product (US). The report also helps stakeholders understand the OCP rack market by providing information on key drivers, restraints, challenges, and opportunities.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.4 STAKEHOLDERS

2 MARKET OVERVIEW

- 2.1 INTRODUCTION

- 2.2 MARKET DYNAMICS

- 2.2.1 DRIVERS

- 2.2.1.1 Adoption in high-density data center environments driven by AI rack power density

- 2.2.1.2 Rack-scale integration across high-density deployments

- 2.2.1.3 Hyperscale standardization

- 2.2.2 RESTRAINTS

- 2.2.2.1 Legacy 19-inch infrastructure limits broader OCP rack adoption in existing data centers

- 2.2.2.2 High facility redesign costs constrain OCP rack adoption in retrofit data center environments

- 2.2.3 OPPORTUNITIES

- 2.2.3.1 Liquid cooling integration to improve adoption opportunity in high-density AI infrastructure

- 2.2.3.2 Pre-configured AI rack systems among hyperscale and neocloud operators

- 2.2.4 CHALLENGES

- 2.2.4.1 Multi-vendor interoperability gaps increase deployment complexity in OCP environments

- 2.2.4.2 Thermal constraints at ultra-high rack densities challenge OCP scalability

- 2.2.1 DRIVERS

- 2.3 CASE STUDY ANALYSIS

- 2.3.1 MODERNIZED ENTERPRISE INFRASTRUCTURE WITH OCP-BASED PRIVATE CLOUD DEPLOYMENT

- 2.3.2 REDUCED DATA CENTER COST AND IMPROVED FLEXIBILITY WITH OPEN BRIDGE RACK ADOPTION

- 2.3.3 STRENGTHENED SCALABLE PRIVATE CLOUD DELIVERY WITH OCP-BASED INTEGRATED INFRASTRUCTURE

- 2.4 ANALYSIS: DOES RISING RACK POWER DENSITY STRUCTURALLY REDUCE RACK COUNTS?

- 2.5 ANALYSIS OF KW EVOLUTION OF 21" OCP RACKS BY 2030

- 2.5.1 LEGACY TO EARLY OCP FOUNDATION (PRE-2015 -> 2020 | 5-15 KW)

- 2.5.2 PHASE 2: CLOUD SCALING & EARLY AI TRANSITION (2020 -> 2023 | 15-40 KW)

- 2.5.3 PHASE 3: STANDARDIZED HIGH-DENSITY ORV3 ERA (2023 -> 2025 | 50-130 KW)

- 2.5.4 PHASE 4: ORV3 STRETCH PHASE (2025 -> 2026 | 130-200 KW+)

- 2.5.5 PHASE 5: TRANSITION TO HIGH-VOLTAGE ARCHITECTURES (2027 -> 2028 | 200-500 KW)

- 2.5.6 PHASE 6: ULTRA-HIGH-DENSITY AI RACKS (2028 -> 2030 | 500 KW-1 MW)

- 2.6 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 2.7 PRICING ANALYSIS

- 2.7.1 AVERAGE SELLING PRICE

- 2.7.2 INDICATIVE PRICING, BY VENDOR

3 21-INCH OCP RACK MARKET, BY END USER

- 3.1 INTRODUCTION

- 3.1.1 21 INCH OCP RACK, BY END USER: MARKET DRIVERS

- 3.2 RETAIL COLOCATION PROVIDERS

- 3.2.1 ABILITY TO SUPPORT HIGH-DENSITY DEPLOYMENTS IN SHARED DATA CENTER ENVIRONMENTS TO PROPEL GROWTH

- 3.3 ENTERPRISE (ON-PREMISES)

- 3.3.1 DRIVING ENTERPRISE INFRASTRUCTURE TRANSFORMATION THROUGH OCP ADOPTION TO FUEL GROWTH

- 3.4 NEOCLOUD PROVIDERS

- 3.4.1 ACCELERATING NEOCLOUD GROWTH THROUGH MODULAR OCP INFRASTRUCTURE TO DRIVE ADOPTION

- 3.5 OTHER END USERS

4 21-INCH OCP RACK MARKET, BY APPLICATION

- 4.1 INTRODUCTION

- 4.1.1 21 INCH OCP RACK, BY APPLICATION: MARKET DRIVERS

- 4.2 AI (TRAINING & INFERENCES)

- 4.2.1 ENABLING AI-SCALE TRAINING WITH HIGH-DENSITY OCP RACK ARCHITECTURES TO DRIVE GROWTH

- 4.3 HIGH-PERFORMANCE COMPUTING (HPC)

- 4.3.1 ENHANCING HPC EFFICIENCY WITH ADVANCED COOLING AND POWER SYSTEMS TO PROPEL GROWTH

- 4.4 DATA MANAGEMENT

- 4.4.1 SUPPORTING REAL-TIME DATA PROCESSING WITH OCP RACK SOLUTIONS TO DRIVE ADOPTION

- 4.5 ENTERPRISE APPS AND OTHERS

5 21-INCH OCP RACK MARKET, BY REGION

- 5.1 INTRODUCTION

- 5.2 NORTH AMERICA

- 5.2.1 US

- 5.2.1.1 Accelerating OCP rack adoption through hyperscale and AI expansion to boost market growth

- 5.2.2 CANADA

- 5.2.2.1 Growing emphasis on building scalable AI infrastructure through ecosystem collaboration to support market growth

- 5.2.1 US

- 5.3 EUROPE

- 5.3.1 UK

- 5.3.1.1 Enabling high-density AI workloads through 21-inch OCP rack deployments to propel growth

- 5.3.2 GERMANY

- 5.3.2.1 Leveraging OCP architectures to support liquid cooling and higher rack powers

- 5.3.3 FRANCE

- 5.3.3.1 Supporting gigawatt-scale AI data centers with high-density rack architectures to fuel growth

- 5.3.4 ITALY

- 5.3.4.1 Expanding data center investments to support OCP rack adoption in Italy

- 5.3.5 SPAIN

- 5.3.5.1 Increase in hyperscale activity, including large AI-focused deployments, to drive demand for high-density and scalable infrastructure

- 5.3.6 REST OF EUROPE

- 5.3.1 UK

- 5.4 ASIA PACIFIC

- 5.4.1 CHINA

- 5.4.1.1 Public cloud expansion supporting open rack deployment to propel growth

- 5.4.2 JAPAN

- 5.4.2.1 Japan strengthens OCP rack adoption through AI infrastructure design

- 5.4.3 INDIA

- 5.4.3.1 India supports OCP rack adoption through local infrastructure demand

- 5.4.4 REST OF ASIA PACIFIC

- 5.4.1 CHINA

- 5.5 MIDDLE EAST & AFRICA

- 5.5.1 GCC

- 5.5.1.1 Saudi Arabia

- 5.5.1.1.1 Saudi data center expansion to drive OCP rack demand

- 5.5.1.2 UAE

- 5.5.1.2.1 UAE hyperscale growth to increase OCP adoption potential

- 5.5.1.3 Rest of GCC

- 5.5.1.1 Saudi Arabia

- 5.5.2 SOUTH AFRICA

- 5.5.2.1 Improving rack power density and cooling efficiency with OCP designs to drive growth

- 5.5.3 REST OF MIDDLE EAST & AFRICA

- 5.5.1 GCC

- 5.6 LATIN AMERICA

- 5.6.1 BRAZIL

- 5.6.1.1 Brazil to strengthen open infrastructure with domestic OCP manufacturing

- 5.6.2 MEXICO

- 5.6.2.1 Mexico to standardize next-generation rack infrastructure for AI workloads

- 5.6.3 REST OF LATIN AMERICA

- 5.6.1 BRAZIL

6 COMPANY PROFILES

- 6.1 INTRODUCTION

- 6.2 KEY PLAYERS

- 6.2.1 SANMINA CORPORATION

- 6.2.1.1 Business overview

- 6.2.1.2 Products/Solutions/Services offered

- 6.2.1.3 Recent developments

- 6.2.1.3.1 Product launches and enhancements

- 6.2.1.3.2 Deals

- 6.2.1.4 MnM view

- 6.2.1.4.1 Right to win

- 6.2.1.4.2 Strategic choices

- 6.2.1.4.3 Weaknesses and competitive threats

- 6.2.2 DELL TECHNOLOGIES

- 6.2.2.1 Business overview

- 6.2.2.2 Products/Solutions/Services offered

- 6.2.2.2.1 Product launches and enhancements

- 6.2.2.3 MnM view

- 6.2.2.3.1 Right to win

- 6.2.2.3.2 Strategic choices

- 6.2.2.3.3 Weaknesses and competitive threats

- 6.2.3 WIWYNN

- 6.2.3.1 Business overview

- 6.2.3.2 Products/Solutions/Services offered

- 6.2.3.3 Recent developments

- 6.2.3.3.1 Product launches and enhancements

- 6.2.3.3.2 Deals

- 6.2.3.4 MnM view

- 6.2.3.4.1 Right to win

- 6.2.3.4.2 Strategic choices

- 6.2.3.4.3 Weaknesses and competitive threats

- 6.2.4 GIGABYTE

- 6.2.4.1 Business overview

- 6.2.4.2 Products/Solutions/Services offered

- 6.2.4.3 Recent developments

- 6.2.4.3.1 Product launches and enhancements

- 6.2.4.4 MnM view

- 6.2.4.4.1 Right to win

- 6.2.4.4.2 Strategic choices

- 6.2.4.4.3 Weaknesses and competitive threats

- 6.2.5 EATON

- 6.2.5.1 Business overview

- 6.2.5.2 Products/Solutions/Services offered

- 6.2.5.3 Recent developments

- 6.2.5.3.1 Product launches and enhancements

- 6.2.5.4 MnM view

- 6.2.5.4.1 Right to win

- 6.2.5.4.2 Strategic choices

- 6.2.5.4.3 Weaknesses and competitive threats

- 6.2.6 RITTAL

- 6.2.6.1 Business overview

- 6.2.6.2 Products/Solutions/Services offered

- 6.2.6.3 Recent developments

- 6.2.6.3.1 Product launches and enhancements

- 6.2.6.3.2 Deals

- 6.2.7 LEGRAND

- 6.2.7.1 Business overview

- 6.2.7.2 Products/Solutions/Services offered

- 6.2.7.3 Recent developments

- 6.2.7.3.1 Product launches and enhancements

- 6.2.8 RACK RENEW

- 6.2.8.1 Business overview

- 6.2.8.2 Products/Solutions/Services offered

- 6.2.8.3 Recent developments

- 6.2.8.3.1 Product launches and enhancements

- 6.2.9 BELDEN

- 6.2.9.1 Business overview

- 6.2.9.2 Products/Solutions/Services offered

- 6.2.10 CHEVAL GROUP

- 6.2.10.1 Business overview

- 6.2.10.2 Products/Solutions/Services offered

- 6.2.1 SANMINA CORPORATION

List of Tables

- TABLE 1 INCLUSIONS AND EXCLUSIONS

- TABLE 2 USD EXCHANGE RATES, 2020-2025

- TABLE 3 INDICATIVE PRICING, BY VENDOR, 2025 (USD)

- TABLE 4 21-INCH OCP RACK MARKET, BY END USER, 2020-2025 (USD MILLION)

- TABLE 5 21-INCH OCP RACK MARKET, BY END USER, 2026-2030 (USD MILLION)

- TABLE 6 21-INCH OCP RACK MARKET, BY END USER, 2020-2025 (THOUSAND UNITS)

- TABLE 7 21-INCH OCP RACK MARKET, BY END USER, 2026-2030 (THOUSAND UNITS)

- TABLE 8 21-INCH OCP RACK MARKET FOR RETAIL COLOCATION PROVIDERS, BY REGION, 2020-2025 (USD MILLION)

- TABLE 9 21-INCH OCP RACK MARKET FOR RETAIL COLOCATION PROVIDERS, BY REGION, 2026-2030 (USD MILLION)

- TABLE 10 21-INCH OCP RACK MARKET FOR ENTERPRISE (ON-PREMISES), BY REGION, 2020-2025 (USD MILLION)

- TABLE 11 21-INCH OCP RACK MARKET FOR ENTERPRISE (ON-PREMISES), BY REGION, 2026-2030 (USD MILLION)

- TABLE 12 21-INCH OCP RACK MARKET FOR NEOCLOUD, BY REGION, 2020-2025 (USD MILLION)

- TABLE 13 21-INCH OCP RACK MARKET FOR NEOCLOUD, BY REGION, 2026-2030 (USD MILLION)

- TABLE 14 21-INCH OCP RACK MARKET FOR OTHERS, BY REGION, 2020-2025 (USD MILLION)

- TABLE 15 21-INCH OCP RACK MARKET FOR OTHERS, BY REGION, 2026-2030 (USD MILLION)

- TABLE 16 21-INCH OCP RACK MARKET, BY APPLICATION, 2020-2025 (USD MILLION)

- TABLE 17 21-INCH OCP RACK MARKET, BY APPLICATIONS, 2026-2030 (USD MILLION)

- TABLE 18 21-INCH OCP RACK MARKET FOR AI (TRAINING & INFERENCE), BY REGION, 2020-2025 (USD MILLION)

- TABLE 19 21-INCH OCP RACK MARKET FOR AI (TRAINING & INFERENCE), BY REGION, 2026-2030 (USD MILLION)

- TABLE 20 21-INCH OCP RACK MARKET FOR HIGH-PERFORMANCE COMPUTING (HPC), BY REGION, 2020-2025 (USD MILLION)

- TABLE 21 21-INCH OCP RACK MARKET FOR HIGH-PERFORMANCE COMPUTING (HPC), BY REGION, 2026-2030 (USD MILLION)

- TABLE 22 21-INCH OCP RACK MARKET FOR DATA MANAGEMENT, BY REGION, 2020-2025 (USD MILLION)

- TABLE 23 21-INCH OCP RACK MARKET FOR DATA MANAGEMENT, BY REGION, 2026-2030 (USD MILLION)

- TABLE 24 21-INCH OCP RACK MARKET FOR ENTERPRISE APPS & OTHERS, BY REGION, 2020-2025 (USD MILLION)

- TABLE 25 21-INCH OCP RACK MARKET FOR ENTERPRISE APPS & OTHERS, 2026-2030 (USD MILLION)

- TABLE 26 21-INCH OCP RACK MARKET, BY REGION, 2020-2025 (USD MILLION)

- TABLE 27 21-INCH OCP RACK MARKET, BY REGION, 2026-2030 (USD MILLION)

- TABLE 28 NORTH AMERICA: 21-INCH OCP RACK MARKET, BY END USER, 2020-2025 (USD MILLION)

- TABLE 29 NORTH AMERICA: 21-INCH OCP RACK MARKET, BY END USER, 2026-2030 (USD MILLION)

- TABLE 30 NORTH AMERICA: 21-INCH OCP RACK MARKET, BY APPLICATION, 2020-2025 (USD MILLION)

- TABLE 31 NORTH AMERICA: 21-INCH OCP RACK MARKET, BY APPLICATION, 2026-2030 (USD MILLION)

- TABLE 32 NORTH AMERICA: 21-INCH OCP RACK MARKET, BY COUNTRY, 2020-2025 (USD MILLION)

- TABLE 33 NORTH AMERICA: 21-INCH OCP RACK MARKET, BY COUNTRY, 2026-2030 (USD MILLION)

- TABLE 34 US: 21-INCH OCP RACK MARKET, BY END USER, 2020-2025 (USD MILLION)

- TABLE 35 US: 21-INCH OCP RACK MARKET, BY END USER, 2026-2030 (USD MILLION)

- TABLE 36 CANADA: 21-INCH OCP RACK MARKET, BY END USER, 2020-2025 (USD MILLION)

- TABLE 37 CANADA: 21-INCH OCP RACK MARKET, BY END USER, 2026-2030 (USD MILLION)

- TABLE 38 EUROPE: 21-INCH OCP RACK MARKET, BY END USER, 2020-2025 (USD MILLION)

- TABLE 39 EUROPE: 21-INCH OCP RACK MARKET, BY END USER, 2026-2030 (USD MILLION)

- TABLE 40 EUROPE: 21-INCH OCP RACK MARKET, BY APPLICATION, 2020-2025 (USD MILLION)

- TABLE 41 EUROPE: 21-INCH OCP RACK MARKET, BY APPLICATION, 2026-2030 (USD MILLION)

- TABLE 42 EUROPE: 21-INCH OCP RACK MARKET, BY COUNTRY, 2020-2025 (USD MILLION)

- TABLE 43 EUROPE: 21-INCH OCP RACK MARKET, BY COUNTRY, 2026-2030 (USD MILLION)

- TABLE 44 UK: 21-INCH OCP RACK MARKET, BY END USER, 2020-2025 (USD MILLION)

- TABLE 45 UK: 21-INCH OCP RACK MARKET, BY END USER, 2026-2030 (USD MILLION)

- TABLE 46 GERMANY: 21-INCH OCP RACK MARKET, BY END USER, 2020-2025 (USD MILLION)

- TABLE 47 GERMANY: 21-INCH OCP RACK MARKET, BY END USER, 2026-2030 (USD MILLION)

- TABLE 48 FRANCE: 21-INCH OCP RACK MARKET, BY END USER, 2020-2025 (USD MILLION)

- TABLE 49 FRANCE: 21-INCH OCP RACK MARKET, BY END USER, 2026-2030 (USD MILLION)

- TABLE 50 ITALY: 21-INCH OCP RACK MARKET, BY END USER, 2020-2025 (USD MILLION)

- TABLE 51 ITALY: 21-INCH OCP RACK MARKET, BY END USER, 2026-2030 (USD MILLION)

- TABLE 52 SPAIN: 21-INCH OCP RACK MARKET, BY END USER, 2020-2025 (USD MILLION)

- TABLE 53 SPAIN: 21-INCH OCP RACK MARKET, BY END USER, 2026-2030 (USD MILLION)

- TABLE 54 REST OF EUROPE: 21-INCH OCP RACK MARKET, BY END USER, 2020-2025 (USD MILLION)

- TABLE 55 REST OF EUROPE: 21-INCH OCP RACK MARKET, BY END USER, 2026-2030 (USD MILLION)

- TABLE 56 ASIA PACIFIC: 21-INCH OCP RACK MARKET, BY END USER, 2020-2025 (USD MILLION)

- TABLE 57 ASIA PACIFIC: 21-INCH OCP RACK MARKET, BY END USER, 2026-2030 (USD MILLION)

- TABLE 58 ASIA PACIFIC: 21-INCH OCP RACK MARKET, BY APPLICATION, 2020-2025 (USD MILLION)

- TABLE 59 ASIA PACIFIC: 21-INCH OCP RACK MARKET, BY APPLICATION, 2026-2030 (USD MILLION)

- TABLE 60 ASIA PACIFIC: 21-INCH OCP RACK MARKET, BY COUNTRY, 2020-2025 (USD MILLION)

- TABLE 61 ASIA PACIFIC: 21-INCH OCP RACK MARKET, BY COUNTRY, 2026-2030 (USD MILLION)

- TABLE 62 CHINA: 21-INCH OCP RACK MARKET, BY END USER, 2020-2025 (USD MILLION)

- TABLE 63 CHINA: 21-INCH OCP RACK MARKET, BY END USER, 2026-2030 (USD MILLION)

- TABLE 64 JAPAN: 21-INCH OCP RACK MARKET, BY END USER, 2020-2025 (USD MILLION)

- TABLE 65 JAPAN: 21-INCH OCP RACK MARKET, BY END USER, 2026-2030 (USD MILLION)

- TABLE 66 INDIA: 21-INCH OCP RACK MARKET, BY END USER, 2020-2025 (USD MILLION)

- TABLE 67 INDIA: 21-INCH OCP RACK MARKET, BY END USER, 2026-2030 (USD MILLION)

- TABLE 68 REST OF ASIA PACIFIC: 21-INCH OCP RACK MARKET, BY END USER, 2020-2025 (USD MILLION)

- TABLE 69 REST OF ASIA PACIFIC: 21-INCH OCP RACK MARKET, BY END USER, 2026-2030 (USD MILLION)

- TABLE 70 MIDDLE EAST & AFRICA: 21-INCH OCP RACK MARKET, BY END USER, 2020-2025 (USD MILLION)

- TABLE 71 MIDDLE EAST & AFRICA: 21-INCH OCP RACK MARKET, BY END USER, 2026-2030 (USD MILLION)

- TABLE 72 MIDDLE EAST & AFRICA: 21-INCH OCP RACK MARKET, BY APPLICATION, 2020-2025 (USD MILLION)

- TABLE 73 MIDDLE EAST & AFRICA: 21-INCH OCP RACK MARKET, BY APPLICATION, 2026-2030 (USD MILLION)

- TABLE 74 MIDDLE EAST & AFRICA: 21-INCH OCP RACK MARKET, BY COUNTRY, 2020-2025 (USD MILLION)

- TABLE 75 MIDDLE EAST & AFRICA: 21-INCH OCP RACK MARKET, BY COUNTRY, 2026-2030 (USD MILLION)

- TABLE 76 GCC: 21 INCH OCP RACK MARKET, BY COUNTRY, 2020-2025 (USD MILLION)

- TABLE 77 GCC: 21 INCH OCP RACK MARKET, BY COUNTRY, 2026-2030 (USD MILLION)

- TABLE 78 GCC: 21-INCH OCP RACK MARKET, BY END USER, 2020-2025 (USD MILLION)

- TABLE 79 GCC: 21-INCH OCP RACK MARKET, BY END USER, 2026-2030 (USD MILLION)

- TABLE 80 SAUDI ARABIA: 21-INCH OCP RACK MARKET, BY END USER, 2020-2025 (USD MILLION)

- TABLE 81 SAUDI ARABIA: 21-INCH OCP RACK MARKET, BY END USER, 2026-2030 (USD MILLION)

- TABLE 82 UAE: 21-INCH OCP RACK MARKET, BY END USER, 2020-2025 (USD MILLION)

- TABLE 83 UAE: 21-INCH OCP RACK MARKET, BY END USER, 2026-2030 (USD MILLION)

- TABLE 84 REST OF GCC: 21-INCH OCP RACK MARKET, BY END USER, 2020-2025 (USD MILLION)

- TABLE 85 REST OF GCC: 21-INCH OCP RACK MARKET, BY END USER, 2026-2030 (USD MILLION)

- TABLE 86 SOUTH AFRICA: 21-INCH OCP RACK MARKET, BY END USER, 2020-2025 (USD MILLION)

- TABLE 87 SOUTH AFRICA: 21-INCH OCP RACK MARKET, BY END USER, 2026-2030 (USD MILLION)

- TABLE 88 REST OF MIDDLE EAST & AFRICA: 21-INCH OCP RACK MARKET, BY END USER, 2020-2025 (USD MILLION)

- TABLE 89 REST OF MIDDLE EAST & AFRICA: 21-INCH OCP RACK MARKET, BY END USER, 2026-2030 (USD MILLION)

- TABLE 90 LATIN AMERICA: 21-INCH OCP RACK MARKET, BY END USER, 2020-2025 (USD MILLION)

- TABLE 91 LATIN AMERICA: 21-INCH OCP RACK MARKET, BY END USER, 2026-2030 (USD MILLION)

- TABLE 92 LATIN AMERICA: 21-INCH OCP RACK MARKET, BY APPLICATIONS, 2020-2025 (USD MILLION)

- TABLE 93 LATIN AMERICA: 21-INCH OCP RACK MARKET, BY APPLICATIONS, 2026-2030 (USD MILLION)

- TABLE 94 LATIN AMERICA: 21-INCH OCP RACK MARKET, BY COUNTRY, 2020-2025 (USD MILLION)

- TABLE 95 LATIN AMERICA: 21-INCH OCP RACK MARKET, BY COUNTRY, 2026-2030 (USD MILLION)

- TABLE 96 BRAZIL: 21-INCH OCP RACK MARKET, BY END USER, 2020-2025 (USD MILLION)

- TABLE 97 BRAZIL: 21-INCH OCP RACK MARKET, BY END USER, 2026-2030 (USD MILLION)

- TABLE 98 MEXICO: 21-INCH OCP RACK MARKET, BY END USER, 2020-2025 (USD MILLION)

- TABLE 99 MEXICO: 21-INCH OCP RACK MARKET, BY END USER, 2026-2030 (USD MILLION)

- TABLE 100 REST OF LATIN AMERICA: 21-INCH OCP RACK MARKET, BY END USER, 2020-2025 (USD MILLION)

- TABLE 101 REST OF LATIN AMERICA: 21-INCH OCP RACK MARKET, BY END USER, 2026-2030 (USD MILLION)

- TABLE 102 SANMINA CORPORATION: COMPANY OVERVIEW

- TABLE 103 SANMINA CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 104 SANMINA CORPORATION: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 105 SANMINA CORPORATION: DEALS

- TABLE 106 DELL TECHNOLOGIES: COMPANY OVERVIEW

- TABLE 107 DELL TECHNOLOGIES: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 108 DELL TECHNOLOGIES: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 109 WIWYNN: COMPANY OVERVIEW

- TABLE 110 WIWYNN: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 111 WIWYNN: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 112 WIWYNN: DEALS

- TABLE 113 GIGABYTE: COMPANY OVERVIEW

- TABLE 114 GIGABYTE: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 115 GIGABYTE: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 116 EATON: COMPANY OVERVIEW

- TABLE 117 EATON: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 118 EATON: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 119 RITTAL: COMPANY OVERVIEW

- TABLE 120 RITTAL: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 121 RITTAL: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 122 RITTAL: DEALS

- TABLE 123 LEGRAND: COMPANY OVERVIEW

- TABLE 124 LEGRAND: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 125 LEGRAND: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 126 RACK RENEW: COMPANY OVERVIEW

- TABLE 127 RACK RENEW: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 128 RACK RENEW: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 129 BELDEN: COMPANY OVERVIEW

- TABLE 130 BELDEN: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 131 CHEVAL GROUP: COMPANY OVERVIEW

- TABLE 132 CHEVAL GROUP: PRODUCTS/SOLUTIONS/SERVICES OFFERED

List of Figures

- FIGURE 1 OCP RACK MARKET SEGMENTATION

- FIGURE 2 STUDY YEARS CONSIDERED

- FIGURE 3 OCP RACK MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- FIGURE 4 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- FIGURE 5 AVERAGE SELLING PRICE, 2020-2025 (USD)

- FIGURE 6 OTHERS TO ACCOUNT FOR LARGEST MARKET SHARE DURING FORECAST PERIOD

- FIGURE 7 AI (TRAINING & INFERENCE) TO BE LARGEST APPLICATION OF OCP RACKS DURING FORECAST PERIOD

- FIGURE 8 NORTH AMERICA TO DOMINATE MARKET DURING FORECAST PERIOD

- FIGURE 9 NORTH AMERICA: OCP RACK MARKET SNAPSHOT

- FIGURE 10 ASIA PACIFIC: OCP RACK MARKET SNAPSHOT

- FIGURE 11 SANMINA CORPORATION: COMPANY SNAPSHOT

- FIGURE 12 DELL TECHNOLOGIES: COMPANY SNAPSHOT

- FIGURE 13 WIWYNN: COMPANY SNAPSHOT

- FIGURE 14 GIGABYTE: COMPANY SNAPSHOT

- FIGURE 15 EATON: COMPANY SNAPSHOT

- FIGURE 16 LEGRAND: COMPANY SNAPSHOT

- FIGURE 17 BELDEN: COMPANY SNAPSHOT

資料中心機架市場-2026-2032年全球市場預測

資料中心機架市場-2026-2032年全球市場預測 資料中心機櫃市場規模及預測(2021-2034),全球及區域佔有率、趨勢及成長機會分析報告:按類型、資料中心規模、機架高度、最終用戶及地區分類

資料中心機櫃市場規模及預測(2021-2034),全球及區域佔有率、趨勢及成長機會分析報告:按類型、資料中心規模、機架高度、最終用戶及地區分類 資料中心機櫃市場 - 全球產業規模、佔有率、趨勢、機會、預測:按組件、機架類型、資料中心規模、機架高度、產業垂直領域、地區和競爭格局分類,2021-2031年

資料中心機櫃市場 - 全球產業規模、佔有率、趨勢、機會、預測:按組件、機架類型、資料中心規模、機架高度、產業垂直領域、地區和競爭格局分類,2021-2031年 資料中心機架市場:按機架類型、資料中心類型、最終用戶和地區分類

資料中心機架市場:按機架類型、資料中心類型、最終用戶和地區分類 資料中心機架及機櫃市場:按組件、應用、安裝類型、國家及地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測

資料中心機架及機櫃市場:按組件、應用、安裝類型、國家及地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測 資料中心機架式配電單元市場規模、佔有率和成長分析:按類型、相數、安裝方式、額定功率、資料中心類型、應用和地區分類-2026年至2033年產業預測

資料中心機架式配電單元市場規模、佔有率和成長分析:按類型、相數、安裝方式、額定功率、資料中心類型、應用和地區分類-2026年至2033年產業預測 資料中心機櫃市場分析及預測(至2035年):類型、產品類型、服務、技術、應用、材質、最終用戶、安裝配置

資料中心機櫃市場分析及預測(至2035年):類型、產品類型、服務、技術、應用、材質、最終用戶、安裝配置 資料中心機架市場規模、佔有率、趨勢和預測:按類型、框架單位、機架尺寸、框架尺寸、框架設計、服務、應用、最終用戶和地區分類,2026-2034 年

資料中心機架市場規模、佔有率、趨勢和預測:按類型、框架單位、機架尺寸、框架尺寸、框架設計、服務、應用、最終用戶和地區分類,2026-2034 年 全球資料中心機櫃市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球資料中心機櫃市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球資料中心機櫃與機櫃市場報告

2026年全球資料中心機櫃與機櫃市場報告