|

市場調查報告書

商品編碼

2044028

通訊網路永續性:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031 年)Telecom Network Sustainability - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

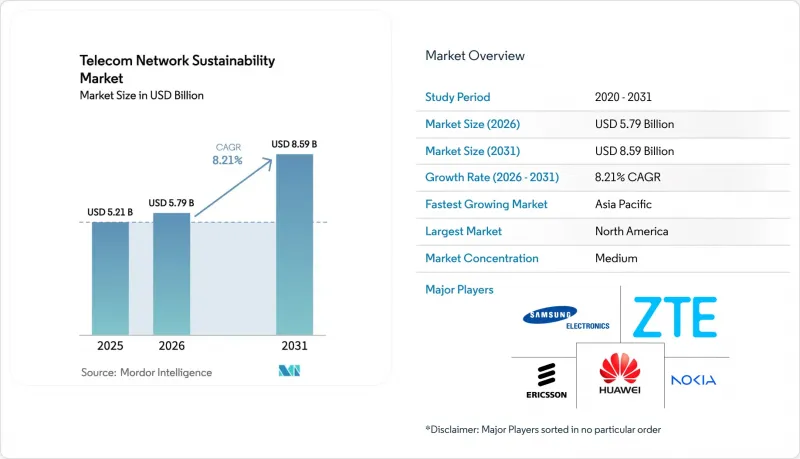

預計電信網路永續性市場將從 2025 年的 52.1 億美元成長到 2026 年的 57.9 億美元,然後在 2031 年達到 85.9 億美元,2026 年至 2031 年的複合年成長率為 8.21%。

5G普及導致電費飆升、碳中和要求日益嚴格以及ESG相關融資的出現,使得永續發展成為董事會層面的優先事項。通訊業者正投資於人工智慧驅動的無線接取網路(RAN)休眠模式軟體、模組化開放式RAN硬體以及現場可再生能源微電網,以減少範圍1和範圍2的排放並獲得優惠利率。超大規模雲端服務供應商要求託管合作夥伴配合其全天候無碳能源部署計劃,從而推動了市場發展;與此同時,鐵塔公司正透過高價租賃,從覆蓋多個租戶的綠色基礎設施中獲得收益。

全球電信網路永續性市場趨勢及洞察

淨零排放承諾和ESG法規

投資人不再重視那些將碳排放報告僅視為附註的通訊業者。隨著歐盟《企業永續性報告指令》的生效,沃達豐和西班牙電信的採購團隊開始將生命週期排放納入評估標準,而那些沒有經過檢驗數據的供應商則被直接淘汰出最終候選名單。中國工業和資訊化部也設定了類似的2030年排放上限,促使中國移動在一年內為120萬個基地台部署了人工智慧能源管理軟體。這項轉變意味著,所有電信網路永續發展市場的參與企業現在都必須公佈可審計的碳排放數據,才能進入2025年發行的5,000億美元ESG債券市場。

5G網路普及導致能源成本快速成長。

從廣域4G基地台向高密度5G叢集的轉變導致每月電費加倍,在某些情況下甚至翻了兩番,尤其是在電力公司幾乎沒有或根本沒有提前通知就提高電價的地區。根據愛立信的研究,典型的5G宏基地台耗電量為4-5千瓦,而4G硬體的耗電量為2-3千瓦,電價飆升導致許多地方市場虧損運作。鐵塔營運商已透過部署太陽能和電池儲能混合系統來應對這項挑戰。美國鐵塔公司在非洲和拉丁美洲的3000個站點項目中,柴油消耗量減少了60%,二氧化碳排放每年減少了約5萬噸。這種成本降低的幅度正促使規模較小的業者也開始共用離網電源,進而擴大電信網路永續發展市場的規模。

維修現有基礎設施需要大量資金投入。

為了實現永續性,對現有網路進行升級需要大量資本投入,這往往與短期投資報酬率目標相衝突。對於一家管理著5萬個基地台的一級通訊業者,這筆費用高達7.5億至12.5億美元,佔年度資本支出的15%至25%,而此時市場收入成長卻十分緩慢。在歐洲,像Orange和德國電信這樣的通訊業者仍然依賴無法透過人工智慧進行能源最佳化的過時3G基地台,這迫使它們必須採取兩階段的升級模式。優先升級都市區站點進一步擴大了城鄉之間的能源效率差距。鐵塔公司採用租賃模式來支付升級成本,並透過提高租金來收回成本,這只是轉移了資本投資的負擔,而沒有真正消除它。

細分市場分析

到2025年,解決方案將佔據68.45%的市場佔有率,這主要得益於對節能無線設備、人工智慧驅動的網路平台以及可再生能源驅動的微電網的投資。服務業預計到2031年將以每年8.98%的速度成長。儘管通訊業者將近70%的2025年預算用於硬體,但他們很快就意識到,採購高效無線設備相對容易。由於計算數千家供應商、容器和廢棄物處理流程的範圍3排放十分困難,通訊業者目前正聘請Accenture、Capgemini SA和愛立信等顧問公司來分析這些數據。因此,由於監管機構每年更新資訊揭露規則並維持諮詢契約,電信網路永續發展市場的業務收益成長速度超過了任何打包產品,年成長率約為9%。能源監控儀錶板清晰地展現了其吸引力。諾基亞的NetGuard平台透過識別可在夜間安全運作的過剩容量基地台,在部署後的18個月內就收回了成本。

同樣重要的是,這項服務使通訊業者能夠將與永續發展相關的支出從資本支出 (Capex) 轉移到營運支出 (OpEx)。許多通訊業者更傾向於根據網路規模支付可變的月費,而不是購買自己的碳計量工具。這有助於平衡現金流,使成本與使用量相符。這種轉變正在吸引那些無法承擔七位數軟體授權費用的規模較小的虛擬行動服務業者(MVNO)。隨著越來越多的國家強制要求揭露經審計的範圍 3 數據,電信網路永續發展市場的服務業很可能會逐漸形成訂閱模式,為供應商和顧問公司帶來可預測且利潤豐厚的收入。

截至2025年,接取網路將佔調查市場的37.89%,這主要得益於5G密度提升宣傳活動中大量無線單元的部署。然而,資料中心和邊緣設施預計將以9.12%的年均成長率成長至2031年,成為網路層中成長率最高的。儘管由於每次5G升級都需要新的無線設備,無線存取網(RAN)仍然佔據最大的市場佔有率,但邊緣節點和資料中心節點才是真正的明星。谷歌雲端計畫在2025年在五個地區實現全天候無碳能源供應,微軟也獲得100億美元的投資,計畫在2030年實現同樣的目標。隨著超大規模資料中心業者推動在託管設施中使用綠色能源,如果本地通訊業者不跟進,它們將失去託管多接入邊緣運算(MAEC)的合約。這種壓力推動了邊緣設施9%的成長率,輕鬆超過了電信網路永續發展市場中核心網路和傳輸網路升級的成長速度。

除了簡單的電力採購,邊緣節點正在開闢新的創收途徑,例如餘熱回收和需量反應。一家北歐通訊業者正在利用微型資料中心的廢熱為區域供熱網路提供燃料,從而獲得積分,縮短投資回收期。在美國,Verizon 透過在基地台安裝電池進一步實現永續設備的商業化,這些電池不僅用於備用電源,還用於參與當地電力市場的頻率調節容量競標。這些創新正在將邊緣層從單純的成本中心轉變為多元化的收入來源,從而增強其未來資本投資的動力。

區域分析

在北美,與大規模風電場簽訂購電協議仍是減少碳排放最經濟的方式,但也導致單站支出最高。 Verizon 和 AT&T 正利用這些協議來對沖電力市場波動風險,並向華爾街展示一份可靠的藍圖,以實現 2035 年淨零排放的目標。各州,特別是德克薩斯州和中大西洋地區的獎勵,進一步提升了大規模風能和太陽能發電工程的吸引力,使該地區在通訊網路永續發展市場中的佔有率達到 26.78%。

然而,亞太地區預計到2031年將以10.19%的年均成長率成長,在所有地區中增速最高,這主要得益於政府監管和5G部署的快速發展。印度通訊部強制要求5G基站在2027年前採用可再生能源,促使Reliance Jio和Bharti Airtel在其基地台屋頂安裝太陽能薄膜和電池組。中國移動響應北京市政府2030年碳排放達峰的號召,於2025年在120萬台無線電台上部署了AI睡眠控制器,在一個預算週期內將網路總功耗降低了兩位數百分比。隨著亞太地區網路的持續擴張,新站點從一開始就採用環保設備,使得資本支出(CAPEX)累計用於成長預算,而非維修成本。這對該地區電信網路永續發展市場而言是一個結構性的利多因素。

在歐洲,網路已趨於成熟,更換老舊設備成本高昂,但歐洲綠色交易仍促使通訊業者積極回應。從橘子到Vodafone,營運商們正在利用與環境、社會和治理(ESG)掛鉤的融資模式,即如果能源相關關鍵績效指標(KPI)有所改善,利率就會降低。這種模式既能起到“維修”的“鞭策”,又能起到“優惠利率”的“激勵”。在斯堪的納維亞半島和比荷盧經濟聯盟等小規模的市場,熱能再利用方案正在試點中,旨在將邊緣伺服器的排放輸送到當地的區域供熱管道。這是一項創新舉措,如果能源公司核准長期契約,則有望廣泛應用。南美洲、中東和非洲的支出合計約佔15%,但這些地區的成長取決於鐵塔公司在離網通訊塔中以太陽能發電取代柴油發電的發電工程。將電力服務納入長期租賃的資金籌措模式將有助於克服高昂的主權借貸成本,並加速這些地區的普及。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 淨零排放承諾和ESG法規

- 5G網路密度不斷增加,導致能源成本飆升。

- 綠色金融和ESG掛鉤債券的可用性

- 供應商生態設計與生命週期評估標準

- AI驅動的RAN睡眠模式最佳化

- 從廢舊設備中回收金屬所得收入

- 市場限制因素

- 維修現有基礎設施需要大量資金投入。

- 缺乏統一的永續發展關鍵績效指標

- 可再生能源微電網建設延誤

- 低碳鋼和再生塑膠供不應求

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭公司之間的競爭

- 永續發展優先領域分析

- 能源效率和減碳

- 循環經濟與電子廢棄物管理

- 可再生能源的整合

- 水資源管理

第5章 市場規模與成長預測

- 按組件

- 解決方案

- 服務

- 網路層

- 接取網路

- 運輸/回程傳輸

- 核心網路

- 資料中心和邊緣設施

- 按部署模式

- 現場

- 雲/SaaS

- 網路技術獨立

- 5G

- 4G/LTE

- 光纖(FTTx)

- 邊緣運算/MEC

- 開放式無線接取網

- 衛星(低地球軌道)

- 按業務類型分類

- 行動通訊業者(MNO)

- 固定電話和網際網路服務供應商

- 超大規模雲端和內容提供者

- 中立主機和塔成本

- 私人網路公司

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 亞太其他地區

- 中東和非洲

- 中東

- 海灣合作理事會國家

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲地區

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Telefonaktiebolaget LM Ericsson

- Nokia Corporation

- Huawei Technologies Co., Ltd.

- ZTE Corporation

- Cisco Systems, Inc.

- Samsung Electronics Co., Ltd.

- NEC Corporation

- Fujitsu Limited

- Dell Technologies Inc.

- International Business Machines Corporation(IBM)

- Juniper Networks, Inc.

- Mavenir Systems, Inc.

- Parallel Wireless, Inc.

- Capgemini Engineering(Capgemini SE)

- Accenture plc

- Orange SA

- Vodafone Group Plc

- American Tower Corporation

- Crown Castle Inc.

- Digital Realty Trust, Inc.

第7章 市場機會與未來展望

The Telecom Network Sustainability Market size is expected to grow from USD 5.21 billion in 2025 to USD 5.79 billion in 2026 and is forecast to reach USD 8.59 billion by 2031 at 8.21% CAGR over 2026-2031.

Escalating electricity bills from 5G densification, binding carbon-neutrality mandates, and the availability of ESG-linked financing are together raising sustainability to a board-level priority. Operators are directing capital toward AI-driven radio access network (RAN) sleep-mode software, modular Open RAN hardware, and on-site renewable microgrids to curb Scope 1 and 2 emissions and secure preferential lending rates. Market momentum is reinforced by hyperscale cloud providers that insist colocation partners match their 24/7 carbon-free energy timelines, while tower companies monetize green infrastructure across multiple tenants through premium leases.

Global Telecom Network Sustainability Market Trends and Insights

Net-Zero Commitments and ESG Regulation

Investors no longer reward telecom operators that treat carbon reporting as a footnote. When the European Union's Corporate Sustainability Reporting Directive took effect, procurement teams at Vodafone and Telefonica began scoring bids partly on life-cycle emissions, and vendors that lacked verified data suddenly fell off short lists. China's Ministry of Industry and Information Technology set a matching 2030 ceiling, prompting China Mobile to wire 1.2 million base stations with AI energy software in a single year. This pivot forces every participant in the telecom network sustainability market to publish auditable carbon numbers to access the USD 500 billion ESG-bond pool priced in 2025.

Escalating Energy Costs From 5G Densification

Moving from wide-area 4G sites to dense 5G clusters doubled, and sometimes tripled, monthly electricity bills, especially in markets where utilities raise tariffs with little notice. Ericsson recorded 4-5 kW draws for a typical 5G macro site, compared with 2-3 kW for 4G hardware, pushing many rural markets into negative-margin territory when grid prices spike. Tower operators answered by rolling out hybrid solar-battery kits; American Tower's 3,000-site program in Africa and Latin America cut diesel burn by 60% and saved roughly 50,000 t of CO2 each year. Cost relief of that scale is nudging smaller carriers toward shared off-grid power, expanding the addressable slice of the telecom network sustainability market.

High Capex to Retrofit Legacy Infrastructure

Upgrading brownfield networks for sustainability requires significant capital, often at odds with short-term ROI goals. For a tier-1 operator managing 50,000 sites, this equates to USD 750 million-1.25 billion, or 15-25% of annual capex in stagnant revenue markets. In Europe, operators like Orange and Deutsche Telekom still rely on outdated 3G base stations incapable of AI-driven energy optimization, forcing a two-tiered upgrade cycle. Urban sites are prioritized, widening the energy-efficiency gap with rural areas. Leasing models from tower companies, which finance upgrades and recover costs via higher rents, shift rather than eliminate the capex burden.

Other drivers and restraints analyzed in the detailed report include:

- AI-Driven RAN Sleep-Mode Optimization

- Vendor Eco-Design and Life-Cycle Standards

- Absence of Unified Sustainability KPIs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions comprised 68.45% of market share in 2025, driven by investments in energy-efficient radios, AI-powered network platforms, and renewable microgrids. Services, growing at 8.98% through 2031. Operators poured almost 70% of their 2025 budgets into hardware but quickly discovered that buying an efficient radio is the easy part. Calculating Scope 3 footprints across thousands of suppliers, containers, and disposal streams is tougher, so carriers now hire consulting arms at Accenture, Capgemini, and Ericsson to crunch that data. Services revenue inside the telecom network sustainability market therefore rises nearly 9% a year, faster than any boxed product, because regulators refresh disclosure rules annually, keeping advisory contracts alive. Energy-monitoring dashboards illustrate the appeal: Nokia's NetGuard platform paid for itself in 18 months after highlighting over-provisioned cell sites that could safely cycle down at night.

Just as important, services let operators move sustainability spending from capex to opex. Instead of buying their own carbon-accounting tools, many carriers prefer paying a monthly fee that scales with network size, smoothing cash flow and aligning costs with usage. This shift attracts smaller mobile virtual network operators that could never justify a seven-figure software license. As more countries mandate audited Scope 3 data, the service slice of the telecom network sustainability market should harden into a subscription model that delivers predictable, high-margin revenue to vendors and consultants alike.

The access network held 37.89% of the studied market in 2025, driven by the sheer volume of radio units deployed in 5G densification campaigns. Yet data center and edge facilities are growing at 9.12% through 2031, the fastest rate among network layers. RAN still commands the biggest dollar share because every 5G upgrade needs new radios, yet edge and data-center nodes are the real head-turners. Google Cloud matched 24/7 carbon-free energy for five regions in 2025, and Microsoft reserved USD 10 billion to hit the same goal by 2030. Those promises ripple outward when hyperscalers insist that a colocation hall run on green power, and the local telecom operator hosting multi-access edge compute must follow suit or lose the contract. That pressure fuels a 9% growth rate for edge facilities, easily outpacing core and transport upgrades inside the telecom network sustainability market.

Beyond raw power sourcing, edge nodes open new levers for heat reuse and demand-response revenue. Operators in Northern Europe now pipe waste heat from micro-data centers into district-heating grids, earning credits that shorten the payback period. In the United States, Verizon installs batteries at cell sites not only for backup but also to bid for frequency-regulation capacity in regional power markets, further monetizing sustainability installations. These tweaks elevate the edge layer from a cost center to a diversified earnings engine, strengthening its pull on future capex.

The Telecom Network Sustainability Market Report is Segmented by Component (Solutions and Services), Network Layer (Access Network, Transport/Backhaul, Core Network, and More), Deployment Model (On-Premise and Cloud/SaaS), Network Technology (5G, 4G/LTE, and More), Operator Type (Mobile Network Operators (MNOs), Fixed-Line and ISPs, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America continues to spend the most per site because power purchase agreements with large wind farms remain the cheapest path to carbon cuts. Verizon and AT&T use those contracts to shield themselves from utility volatility and to show Wall Street credible net-zero roadmaps by 2035. State-level incentives, especially in Texas and the Mid-Atlantic, make large wind or solar blocks even more attractive, reinforcing the region's 26.78% share of the telecom network sustainability market.

However, Asia-Pacific is expanding at 10.19% through 2031, the fastest regional growth rate, propelled by government mandates and the sheer scale of 5G deployments. India's Department of Telecommunications mandated renewable-ready 5G base stations by 2027, prompting Reliance Jio and Bharti Airtel to line cell-site rooftops with solar film and battery packs. China Mobile, under Beijing's 2030 carbon-peaking directive, wired 1.2 million radios with AI sleep controllers in 2025, saving a double-digit slice of total network power in a single budget cycle. Because APAC networks are still expanding, new sites ship with green kit baked in, so capex falls into growth budgets rather than retrofit buckets, a structural tailwind for the regional telecom network sustainability market.

In the European region, networks are mature, and swapping old gear is expensive, yet the European Green Deal still pressures carriers to move. Operators from Orange to Vodafone tap ESG-linked loans that shave interest rates if energy KPIs improve, creating financial carrots to balance the retrofit stick. Smaller markets, Nordics, Benelux, experiment with heat-reuse schemes, feeding waste warmth from edge servers into municipal district-heating pipes, an innovation that may spread once energy utilities verify long-term contracts. South America and the Middle East and Africa together account for a mid-teens share of spending, but their growth curves hinge on tower-company solar projects that replace diesel in off-grid towers. Financing models that bundle power services into long leases help overcome high sovereign borrowing costs and accelerate adoption in these regions.

- Telefonaktiebolaget LM Ericsson

- Nokia Corporation

- Huawei Technologies Co., Ltd.

- ZTE Corporation

- Cisco Systems, Inc.

- Samsung Electronics Co., Ltd.

- NEC Corporation

- Fujitsu Limited

- Dell Technologies Inc.

- International Business Machines Corporation (IBM)

- Juniper Networks, Inc.

- Mavenir Systems, Inc.

- Parallel Wireless, Inc.

- Capgemini Engineering (Capgemini SE)

- Accenture plc

- Orange S.A.

- Vodafone Group Plc

- American Tower Corporation

- Crown Castle Inc.

- Digital Realty Trust, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Net-Zero Commitments and ESG Regulation

- 4.2.2 Escalating Energy Costs From 5G Densification

- 4.2.3 Availability of Green Financing and ESG-Linked Bonds

- 4.2.4 Vendor Eco-Design and Lifecycle-Assessment Standards

- 4.2.5 AI-Driven RAN Sleep-Mode Optimization

- 4.2.6 Metal Recovery Revenue From Decommissioned Gear

- 4.3 Market Restraints

- 4.3.1 High Capex to Retrofit Legacy Infrastructure

- 4.3.2 Absence of Unified Sustainability KPIs

- 4.3.3 Site Delays for Renewable Micro-Grids

- 4.3.4 Scarcity of Low-Carbon Steel and Recycled Plastics

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Sustainability Focus Area Analysis

- 4.8.1 Energy Efficiency and Carbon Reduction

- 4.8.2 Circular Economy and E-waste Management

- 4.8.3 Renewable Energy Integration

- 4.8.4 Water Stewardship

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.2 Services

- 5.2 By Network Layer

- 5.2.1 Access Network

- 5.2.2 Transport/Backhaul

- 5.2.3 Core Network

- 5.2.4 Data Center and Edge Facilities

- 5.3 By Deployment Model

- 5.3.1 On-premise

- 5.3.2 Cloud/SaaS

- 5.4 By Network Technology

- 5.4.1 5G

- 5.4.2 4G/LTE

- 5.4.3 Fiber (FTTx)

- 5.4.4 Edge Computing/MEC

- 5.4.5 Open RAN

- 5.4.6 Satellite (LEO)

- 5.5 By Operator Type

- 5.5.1 Mobile Network Operators (MNOs)

- 5.5.2 Fixed-line and ISPs

- 5.5.3 Hyperscale Cloud and Content Providers

- 5.5.4 Neutral Hosts and TowerCos

- 5.5.5 Private-Network Enterprises

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 GCC Countries

- 5.6.5.1.2 Turkey

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Telefonaktiebolaget LM Ericsson

- 6.4.2 Nokia Corporation

- 6.4.3 Huawei Technologies Co., Ltd.

- 6.4.4 ZTE Corporation

- 6.4.5 Cisco Systems, Inc.

- 6.4.6 Samsung Electronics Co., Ltd.

- 6.4.7 NEC Corporation

- 6.4.8 Fujitsu Limited

- 6.4.9 Dell Technologies Inc.

- 6.4.10 International Business Machines Corporation (IBM)

- 6.4.11 Juniper Networks, Inc.

- 6.4.12 Mavenir Systems, Inc.

- 6.4.13 Parallel Wireless, Inc.

- 6.4.14 Capgemini Engineering (Capgemini SE)

- 6.4.15 Accenture plc

- 6.4.16 Orange S.A.

- 6.4.17 Vodafone Group Plc

- 6.4.18 American Tower Corporation

- 6.4.19 Crown Castle Inc.

- 6.4.20 Digital Realty Trust, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

- 7.2 Analyst Recommendations and Suggestions

ReclaimX永續發展市場預測至2034年-按服務類型、策略類型、技術、應用、最終用戶和地區分類的全球分析永續工業資源管理市場預測至2034年-按解決方案類型、部署模式、技術、應用、最終用戶和地區分類的全球分析

ReclaimX永續發展市場預測至2034年-按服務類型、策略類型、技術、應用、最終用戶和地區分類的全球分析永續工業資源管理市場預測至2034年-按解決方案類型、部署模式、技術、應用、最終用戶和地區分類的全球分析 永續發展市場規模、佔有率和成長分析:按解決方案類別、重點領域、最終用途產業和地區分類-2026-2033年產業預測永續原料市場預測至2034年-全球原料類型、來源、功能、形態、永續性屬性、應用、通路和區域分析

永續發展市場規模、佔有率和成長分析:按解決方案類別、重點領域、最終用途產業和地區分類-2026-2033年產業預測永續原料市場預測至2034年-全球原料類型、來源、功能、形態、永續性屬性、應用、通路和區域分析 2026年全球永續諮詢市場報告

2026年全球永續諮詢市場報告 水力發電的連結:資料中心如何重塑美國水資源格局

水力發電的連結:資料中心如何重塑美國水資源格局 全球水燃料市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球水燃料市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2025-2029年全球水燃料市場

2025-2029年全球水燃料市場 永續性:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)2032年食品廢棄物減量技術市場預測:按食品類型、技術、應用、最終用戶和地區分類的全球分析

永續性:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)2032年食品廢棄物減量技術市場預測:按食品類型、技術、應用、最終用戶和地區分類的全球分析