|

市場調查報告書

商品編碼

2044024

中小企業的雲端ERP:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)SMBs Cloud ERP - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

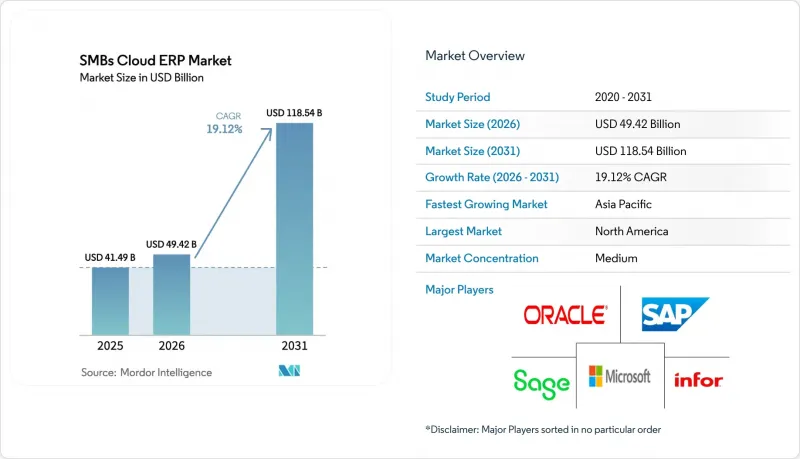

2025年,中小企業雲ERP市值為414.9億美元,預計到2031年將達到1185.4億美元,而2026年為494.2億美元,預測期(2026-2031年)複合年成長率為19.12%。

訂閱式定價、即時合規要求和嵌入式人工智慧 (AI) 正在共同作用,消除先前阻礙中小企業 (SME) 採用人工智慧技術的預算和技能障礙。儘管公共雲端仍佔據市場主導地位,但隨著中國、印度和中東等地的資料主權法規將工作負載轉移到本地基礎設施,混合部署正在加速發展。醫療保健、製造業和零售業的垂直整合模組因其部署時間短和標準化的合規模板而持續受到歡迎。供應商在人工智慧代理編配和低程式碼整合方面的激烈競爭,進一步加快了價值實現速度,並創造了與更高採用率相關的新獲利途徑。

全球雲端ERP市場趨勢及對中小企業的洞察

中小企業對公共雲端的採用率快速成長

憑藉便捷的配置和可隨使用量擴展的靈活收費模式,83% 的中型企業和 61% 的中小企業正在將其大部分工作負載遷移到公共雲端。每月更新、自動修補程式和近乎瞬時的擴展能力,提供了本地 ERP 系統無法實現的營運敏捷性。超大規模資料中心超大規模資料中心業者正在部署新的區域資料中心以滿足資料居住要求。 Oracle 和Oracle已宣布計劃在 2025 年前擴展其在亞洲的資料中心,旨在透過滿足中國、印度和中東地區的主權雲端要求,降低延遲並減少合規性方面的摩擦。隨著可用區的擴展,面向中小企業的雲端 ERP 市場正受益於良性循環:對本地合規性的信心增強,從而加速了工作負載的進一步遷移。供應商藍圖現在專注於主權雲端藍圖和零信任安全功能,使公共雲端成為新部署的預設選擇。

加速後疫情時代的數位轉型

疫情封鎖暴露了傳統會計和庫存管理系統的脆弱性,這些系統缺乏電子商務和行動存取所需的API介面。小型企業主不再將數位化工作流程視為緊急措施,而是視為標準業務流程。雲端ERP供應商已將電子商務連接器、嵌入式分析和行動應用程式捆綁到其基礎套餐中,從而消除了曾經阻礙小規模買家的整合成本。以前需要額外購買的CRM和供應鏈模組現在已成為標準功能,這反映了客戶對從報價到付款全程可視性的期望。即使疫情的影響逐漸消退,這些變化也推動了市場持續強勁成長。

中小企業缺乏資訊科技技能

儘管許多技術領導者都在努力招募雲端ERP專家,但只有35%的員工接受過與人工智慧相關的技能培訓。人才短缺在農村和小城市尤其嚴重,迫使中小企業依賴託管服務,但這會增加成本並降低客製化靈活性。雖然供應商推出了設定精靈和無程式碼擴充程序,但這些工具無法完全取代專業知識。技術進步的快速發展加劇了熟練人才的短缺,因為技術進步的速度超過了訓練有素的人才的供應速度。由此造成的技能差距導致部署延遲和投資回報率降低,從而在中小企業雲端ERP市場中形成結構性瓶頸。

細分市場分析

到2025年,公共雲端的市佔率將達到71.87%,這主要得益於小規模企業優先考慮即時可擴展性和最低維護成本。然而,由於監管壓力要求在保持公共雲端分析柔軟性的同時實現本地數據存儲,預計混合架構在2026年至2031年間的複合年成長率將達到15.87%。主權雲端服務和整合管理主機允許財務和人力資源工作負載保留在私有實例上,而人工智慧驅動的預測分析和開發/測試環境可以根據需要擴展到公共基礎設施。 SAP已與先正達合作部署SAP Cloud ERP私有解決方案。這些私有版本不僅保證了專用租戶和客戶管理的加密金鑰,而且還能與SAP廣泛的雲端生態系無縫整合。

第二代混合部署方案也著眼於新興市場網路不穩定的問題,在這些市場中,穩定可靠的網路連線仍然是一大挑戰。這些部署方案利用本地快取技術,確保即使在網路故障期間,關鍵業務交易也能不間斷地進行。一旦網路連線恢復,系統會將本地快取的資料與雲端帳本進行核對,從而確保資料完整性和業務連續性。這種容錯能力使得中小企業的雲端ERP市場能夠拓展到先前受制於不可靠寬頻基礎設施的地區。

區域分析

預計到2025年,北美將維持36.12%的收入佔有率,這得益於其對SaaS的成熟態度、強大的合作夥伴生態系統以及大規模公共部門計畫。儘管持續的投資,例如Workday的10億加元(約7.1億美元)擴張計劃,有望進一步推動薪資核算和安全管理的本地化,但隨著市場普及率接近飽和,整體成長速度正在放緩。目前,北美中小企業雲端ERP市場的收入成長更依賴於提升銷售機會,特別是人工智慧代理模組和產業特定附加元件,而非新客戶的取得。

亞太地區預計將成為成長最快的地區,複合年成長率 (CAGR) 將達到 15.19%。諸如「數位印度」和沙烏地阿拉伯「2030 願景」等國家數位化目標,透過稅收優惠和強制電子帳單等措施,有效推動了該地區的成長,迫使企業採用雲端財務系統。包括主要雲端服務供應商在內的超大規模資料中心業者正在持續推進運算區域的在地化,圖延遲並確保符合資料主權法規,而資料主權法規先前一直是企業採用雲端技術的障礙。 Zoho 等本土供應商和一些知名的全球公司正在建立研發中心,並部署本地語言版本的軟體包。這些舉措顯著縮短了該地區中小企業採用雲端技術的週期,加速了市場擴張和雲端 ERP 解決方案的普及。

在歐洲,由於符合GDPR標準的架構以及歐盟旨在抵消中小企業實施成本的財政援助計劃,市場呈現穩定成長態勢。斯洛維尼亞的數位化基金和英國的中小企業數位化工作小組等舉措,便是協調一致的政策舉措,旨在促進中小企業的數位轉型。同時,在中東和非洲地區,沙烏地阿拉伯ZATCA第二階段的即時發票等監管進步,以及沿岸地區正在實施的類似法規,都為市場發展提供了助力。這些進展正在加速雲端ERP系統的轉型。南美洲的整體市場規模雖然落後,但隨著巴西和阿根廷等國實施激進的增值稅(增值稅)方案,其發展勢頭正在增強。這些變革推動了雲端平台支援的自動化報稅流程,進一步加速了該地區的採用。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 中小企業對公共雲端的採用率快速成長

- 加速後疫情時代的數位轉型

- 訂閱定價模式的日益普及

- 政府獎勵中小企業數位轉型

- 產業專用雲端ERP解決方案的興起

- 與低程式碼平台整合

- 市場限制因素

- 中小企業缺乏資訊科技技能

- 資料安全和合規性問題

- 整合舊有系統的複雜性

- 雲端運算成本不斷上漲

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭強度

第5章 市場規模與成長預測

- 按部署模式

- 公共雲端

- 私有雲端

- 混合雲端

- 模組特定

- 財務管理

- 庫存和訂單管理

- 人力資本管理

- 客戶關係管理

- 供應鏈管理

- 其他模組

- 按行業

- 製造業

- 零售與電子商務

- 專業服務

- 衛生保健

- 建造

- 其他行業部門

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 亞太其他地區

- 中東和非洲

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲地區

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- SAP SE

- Oracle Corporation

- Microsoft Corporation

- Sage Group Plc

- Infor Inc.

- Epicor Software Corporation

- Acumatica, Inc.

- Workday, Inc.

- Priority Software Ltd.

- Odoo SA

- Zoho Corporation Pvt. Ltd.

- Xero Limited

- Exact Holdin BV

- SYSPRO(Pty)Ltd.

- Intuit Inc.

- Deltek, Inc.

- Certinia Inc.

- Brrightpeearl Limited

- Abas Software GmbH

- IFS AB

- Unite4 NV

- MYOB Group Pty Ltd.

第7章 市場機會與未來展望

The SMBs Cloud Enterprise Resource Planning market size was valued at USD 41.49 billion in 2025 and estimated to grow from USD 49.42 billion in 2026 to reach USD 118.54 billion by 2031, at a CAGR of 19.12% during the forecast period (2026-2031).

Subscription pricing, real-time compliance mandates, and embedded artificial intelligence are converging to remove historic budget and skills barriers that slowed adoption among smaller businesses. Public cloud deployments still dominate the market, yet hybrid deployments are accelerating as sovereign-data rules in China, India, and the Middle East push workloads toward localized infrastructure. Vertically tailored modules for healthcare, manufacturing, and retail continue to gain traction because they shorten implementation timelines and embed regulatory templates out of the box. Intense vendor competition around AI-agent orchestration and low-code integration is further compressing time-to-value while creating new monetization pathways tied to consumption expansion.

Global SMBs Cloud ERP Market Trends and Insights

Surge in Public Cloud Adoption Among SMBs

Low-touch provisioning and pay-as-you-grow elasticity have pushed 83% of mid-sized businesses and 61% of small businesses to migrate the majority of workloads to public cloud. Monthly release cycles, automated patching, and near-instant scaling deliver operational agility that on-premise ERP cannot match. Hyperscalers are responding with new regional data centers that satisfy data-residency mandates. Oracle and SAP announced plans to expand their data centers in Asia by 2025, aiming to meet sovereign-cloud requirements in China, India, and the Middle East, thereby reducing latency and easing compliance friction. As availability zones proliferate, the SMBs cloud enterprise resource planning market benefits from a feedback loop in which local compliance confidence accelerates additional workload migration. Vendor roadmaps now center on sovereign cloud blueprints and zero-trust security features, making the public cloud the default choice for new deployments.

Accelerating Digital Transformation Post-COVID-19

Lockdowns exposed the fragility of legacy accounting and inventory systems that lacked APIs for ecommerce and mobile access. SMB leaders continue to treat digital workflows as standard operating procedure rather than contingency planning. Cloud ERP vendors have bundled ecommerce connectors, embedded analytics, and mobile apps into base tiers, removing the integration cost that once deterred smaller buyers. CRM and supply-chain modules that previously required bolt-on purchases now ship standard, reflecting the expectation of end-to-end visibility from quote to cash. These shifts sustain premium growth in the market even as pandemic shocks recede.

Limited IT Skills Within Small Businesses

Many technology leaders struggle to recruit cloud-ERP specialists, while only 35% of employees receive AI-related upskilling. Rural and tier-2 cities face the steepest shortages, forcing SMBs to rely on managed services that add cost and dilute customization freedom. Vendors have introduced guided setup wizards and no-code extensions, yet these tools cannot fully replace domain expertise. This shortage of skilled professionals is further exacerbated by the rapid pace of technological advancements, which outpaces the availability of trained personnel. The resulting skills gap slows rollouts and dampens ROI, placing a structural drag on the SMBs' cloud enterprise resource planning market.

Other drivers and restraints analyzed in the detailed report include:

- Growing Affordability of Subscription Pricing Models

- Government Incentives for SME Digitization

- Data Security and Compliance Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Public cloud retained 71.87% of the market share in 2025 as smaller firms gravitated toward instant scalability and minimal maintenance. Hybrid architectures, however, are projected to deliver a 15.87% CAGR over 2026-2031, reflecting regulatory pressures that compel local data storage while preserving the analytic flexibility of the public cloud. Sovereign-cloud offerings and unified management consoles let finance and HR workloads remain on private instances, with AI-driven forecasting and dev-test environments burst to public infrastructure on demand. SAP has teamed up with Syngenta to roll out its SAP Cloud ERP Private solutions. These private editions not only ensure dedicated tenancy and customer-controlled encryption keys but also seamlessly integrate with SAP's expansive cloud ecosystem.

Second-generation hybrid deployments also hedge against network instability in emerging markets, where consistent and reliable internet connectivity remains a challenge. These deployments use local caching to ensure mission-critical transactions continue uninterrupted during network outages. Once connectivity is restored, the system reconciles the locally cached data with cloud-based ledgers, ensuring data integrity and operational continuity. This level of resilience is enabling the SMBs cloud enterprise resource planning market to expand into regions previously constrained by unreliable broadband infrastructure.

The SMBs Cloud Enterprise Resource Planning Market Report is Segmented by Deployment Model (Public Cloud, Private Cloud, and Hybrid Cloud), Module (Financial Management, Inventory and Order Management, Human Capital Management, Customer Relationship Management, and More), Industry Vertical (Manufacturing, Retail and E-Commerce, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 36.12% revenue share in 2025, buoyed by mature SaaS mindsets, dense partner ecosystems, and large public-sector projects. Continued investments, such as Workday's CAD 1 billion (USD 0.71 billion approximately) expansion, will deepen payroll and security localization, but overall growth is moderating as penetration approaches saturation. Upsell opportunities around AI-agent modules and industry add-ons now outpace net-new logos in driving North American revenue for the SMBs cloud ERP market.

Asia-Pacific is projected to be the fastest-growing region, with a 15.19% CAGR. National digitization targets, such as Digital India and Saudi Arabia's Vision 2030, are driving growth by combining tax incentives with e-invoicing mandates that effectively require businesses to adopt cloud-ready finance systems. Hyperscalers, including major cloud service providers, are continuing to localize compute regions, which helps reduce latency and ensures compliance with data-sovereignty statutes that previously hindered adoption. Domestic vendors, such as Zoho, as well as global incumbents, are establishing R&D hubs and introducing local-language packs. These efforts are significantly compressing deployment timelines for regional SMBs, thereby fueling market expansion and adoption of cloud ERP solutions.

Europe is experiencing steady growth, supported by GDPR-compliant architectures and EU funding programs designed to offset the adoption costs for smaller firms. Initiatives such as Slovenia's digitization fund and the UK's SME Digital Adoption Taskforce exemplify a coordinated policy push to encourage digital transformation among SMBs. Meanwhile, the Middle East and Africa are benefiting from regulatory advancements, such as ZATCA Phase 2 real-time invoicing in Saudi Arabia, along with similar rules emerging across the Gulf region. These developments are prompting accelerated migrations to cloud ERP systems. South America, while trailing in total market value, is gaining momentum as countries like Brazil and Argentina implement overhauls to their VAT frameworks. These changes favor automated tax-filing processes enabled by cloud platforms, further driving adoption in the region.

- SAP SE

- Oracle Corporation

- Microsoft Corporation

- Sage Group Plc

- Infor Inc.

- Epicor Software Corporation

- Acumatica, Inc.

- Workday, Inc.

- Priority Software Ltd.

- Odoo SA

- Zoho Corporation Pvt. Ltd.

- Xero Limited

- Exact Holdin B.V.

- SYSPRO (Pty) Ltd.

- Intuit Inc.

- Deltek, Inc.

- Certinia Inc.

- Brrightpeearl Limited

- Abas Software GmbH

- IFS AB

- Unite4 N.V.

- MYOB Group Pty Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in Public Cloud Adoption Among SMBs

- 4.2.2 Accelerating Digital Transformation Post COVID-19

- 4.2.3 Growing Affordability of Subscription Pricing Models

- 4.2.4 Government Incentives for SME Digitization

- 4.2.5 Emergence of Vertical-Specific Cloud ERP Solutions

- 4.2.6 Integration Capabilities with Low-Code Platforms

- 4.3 Market Restraints

- 4.3.1 Limited IT Skills Within Small Businesses

- 4.3.2 Data Security and Compliance Concerns

- 4.3.3 Legacy System Integration Complexities

- 4.3.4 Rising Cloud Computing Cost Inflation

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Comptitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Model

- 5.1.1 Public Cloud

- 5.1.2 Private Cloud

- 5.1.3 Hybrid Cloud

- 5.2 By Module

- 5.2.1 Financial Management

- 5.2.2 Inventory and Order Management

- 5.2.3 Human Capital Management

- 5.2.4 Customer Relationship Management

- 5.2.5 Supply Chain Management

- 5.2.6 Other Modules

- 5.3 By Industry Vertical

- 5.3.1 Manufacturing

- 5.3.2 Retail and E-commerce

- 5.3.3 Professional Services

- 5.3.4 Healthcare

- 5.3.5 Construction

- 5.3.6 Other Industry Verticals

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 United Kingdom

- 5.4.3.2 Germany

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 India

- 5.4.4.4 South Korea

- 5.4.4.5 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 Middle East

- 5.4.5.1.1 United Arab Emirates

- 5.4.5.1.2 Saudi Arabia

- 5.4.5.1.3 Rest of Middle East

- 5.4.5.2 Africa

- 5.4.5.2.1 South Africa

- 5.4.5.2.2 Egypt

- 5.4.5.2.3 Rest of Africa

- 5.4.5.1 Middle East

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Oracle Corporation

- 6.4.3 Microsoft Corporation

- 6.4.4 Sage Group Plc

- 6.4.5 Infor Inc.

- 6.4.6 Epicor Software Corporation

- 6.4.7 Acumatica, Inc.

- 6.4.8 Workday, Inc.

- 6.4.9 Priority Software Ltd.

- 6.4.10 Odoo SA

- 6.4.11 Zoho Corporation Pvt. Ltd.

- 6.4.12 Xero Limited

- 6.4.13 Exact Holdin B.V.

- 6.4.14 SYSPRO (Pty) Ltd.

- 6.4.15 Intuit Inc.

- 6.4.16 Deltek, Inc.

- 6.4.17 Certinia Inc.

- 6.4.18 Brrightpeearl Limited

- 6.4.19 Abas Software GmbH

- 6.4.20 IFS AB

- 6.4.21 Unite4 N.V.

- 6.4.22 MYOB Group Pty Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

CRM整合ERP:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)基於雲端的企業資源規劃(ERP):市場佔有率分析、產業趨勢和統計數據以及成長預測(2026-2031 年)

CRM整合ERP:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)基於雲端的企業資源規劃(ERP):市場佔有率分析、產業趨勢和統計數據以及成長預測(2026-2031 年) 雲端ERP市場規模、佔有率和成長分析:按組件、部署類型、組織規模、業務職能、產業和地區分類-2026年至2033年產業預測

雲端ERP市場規模、佔有率和成長分析:按組件、部署類型、組織規模、業務職能、產業和地區分類-2026年至2033年產業預測 基於雲端的企業資源計畫 (ERP) 市場:按組件、部署類型、應用程式和產業分類-2026-2032 年全球市場預測

基於雲端的企業資源計畫 (ERP) 市場:按組件、部署類型、應用程式和產業分類-2026-2032 年全球市場預測 雲ERP市場規模、佔有率、成長率和全球產業分析:按類型、應用和地區分類的洞察,2026-2034年預測

雲ERP市場規模、佔有率、成長率和全球產業分析:按類型、應用和地區分類的洞察,2026-2034年預測 2026年全球雲端ERP市場報告2026年全球雲端ERP市場報告

2026年全球雲端ERP市場報告2026年全球雲端ERP市場報告 雲端ERP市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、模組及功能分類全球雲端ERP市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

雲端ERP市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、模組及功能分類全球雲端ERP市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 雲端ERP的全球市場的評估:各部署,各用途,各組織規模,各最終用途產業,各地區,機會,預測(2018年~2032年)

雲端ERP的全球市場的評估:各部署,各用途,各組織規模,各最終用途產業,各地區,機會,預測(2018年~2032年)