|

市場調查報告書

商品編碼

2043989

南美紡織品:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)South America Textile - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

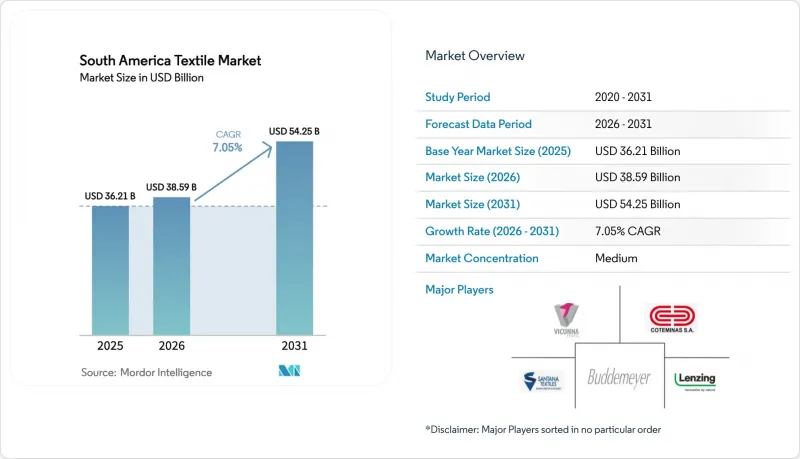

預計南美紡織品市場將從 2025 年的 362.1 億美元和 2026 年的 385.9 億美元成長到 2031 年的 542.5 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 7.05%。

巴西和阿根廷服裝需求的成長,加上地工織物、衛生不織布和再生聚酯纖維等產業的結構性成長,正推動收入來源向時尚產業以外的領域拓展。歐洲循環經濟標準的加強,加速了對可追溯供應鏈和「數位產品護照」試點計畫的投資,使符合標準的出口商能夠免稅進入歐盟市場。蘭精集團和Indorama等公司的外國直接投資,在確保本地原料供應、加強回收基礎設施建設以及保護跨國公司免受棉花價格波動的影響方面發揮著重要作用。同時,聖保羅的非正規紡織中心已將設計到商店的周期縮短至14天以內,迫使正規紡紗廠在採用按需生產模式和承擔市場佔有率下降的風險之間做出選擇。能源價格的波動,特別是巴西計畫在2025年將電費提高12%,持續對印染整理產業的利潤率構成壓力。

南美洲紡織品市場趨勢與考量

技術紡織品在地方交通基礎設施的普及

巴西2024-2030年基礎建設計畫撥款560億美元用於交通網路建設,其中大部分需要符合ASTM標準的不織布地工織物。阿根廷瓦卡穆埃爾塔頁岩計畫對高強度聚酯織物的需求在2025年增加了19%,反映出該國環境法規的日益嚴格。在秘魯採礦業,尾礦壩加固織物已被列入規範,歐洲供應商正透過利馬的經銷商進入秘魯市場。隨著巴西ABNT NBR 12553等技術標準的實施,採購正轉向經認證的本地製造商。持續的檢驗仍然至關重要,因為先前監管不力導致不合格的進口產品以低於合格產品的價格出售。

快時尚週期和按需生產

在聖保羅的布拉斯區和布宜諾斯艾利斯的拉薩拉達市場,一些非正式的產業叢集正在將社群媒體上的流行趨勢在兩週內轉化為成品。這些微型工廠將裁剪、縫紉和後整理工序整合於一處,無需透過批發商,即可在Instagram和WhatsApp上直接銷售。預計到2025年,這些非正式企業將佔巴西國內服裝產量的38%,凸顯了其龐大的規模。正規工廠正透過數位印花和模組化生產線來應對,並將最低訂購量降低至50件,但它們仍然難以在不影響可追溯性的前提下,保持與非正式企業同等的靈活性。隨著歐盟買家對勞動標準的檢驗日益嚴格,速度與合規之間的矛盾也愈發尖銳,迫使非正式企業要麼合法化,要麼縮減出口規模。

能源和原物料價格波動

巴西2025年電費上漲12%,進一步推高了高耗能染色和支架加工產業的利潤率。在阿根廷,查科地區的乾旱導致棉花價格在2024年飆升18%,迫使工廠以高價進口棉花。聚酯纖維成本與原油價格波動有60天的滯後效應,使得簽訂固定價格服飾合約的工廠面臨風險。像Indorama位於聖保羅的rPET工廠這樣垂直整合回收業務的生產商,正在對沖原生樹脂價格波動帶來的風險。而那些沒有這些緩衝措施的公司則推遲了資本投資,但隨著買家轉向價格更穩定的供應商,它們將面臨設備過時的風險。

細分市場分析

在南美紡織品市場,時尚服裝業仍佔據主導地位,市場佔有率高達55.55%,但由於自由裁量權支配支出下降和二手商品進口增加,其成長速度正在放緩。工業和技術紡織品領域正以6.15%的複合年成長率快速擴張,成長率超過其他任何應用領域。需求來源包括巴西一項價值560億美元的交通基礎設施維修所需的地工織物,以及秘魯採礦業所需的過濾織物。服裝公司仍在投資阿根廷的近岸外包專案以規避關稅,但用於石油、天然氣和建築行業的功能性織物在採購預算中所佔的佔有率越來越大。

技術紡織品生產商正尋求公共採購,以強制要求ASTM和ABNT認證,這使得擁有內部測試實驗室的製造商更具優勢。像Ober這樣的本土巨頭已經實施了ISO 9001體系,而新興參與企業則與德國專業公司HUESKER合作,提供承包侵蝕防護解決方案。成功的關鍵在於快速實現符合歐盟買家所重視的永續性標準的再生聚酯地工格網的商業化。服裝製造商則透過引入QR碼追溯功能來應對這項挑戰,以證明更高的價格是合理的。這表明,儘管這兩個領域將共存,但技術平台終將融合。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 快時尚週期和按需生產

- 27個歐盟國家強制實施紡織品廢棄物分類收集(2025年)

- 透過電子商務和社交商務縮短從設計到商店銷售的前置作業時間。

- 技術紡織品在區域內交通基礎設施領域的普及。

- 投資者對來自南美洲、環境影響較小的天然纖維越來越感興趣。

- 南方共同市場基於區塊鏈的「數位產品護照」試點項目

- 市場限制因素

- 能源和原物料價格波動

- 先進的回收和分類能力需要大量資金投入。

- 熟練工人短缺(染色、整理、自動化)

- 中小企業分散化及遵守新的ESG實質審查

- 價值/供應鏈分析

- 監理情勢

- 技術展望

- 產業吸引力:五力分析

- 買方的議價能力

- 供應商議價能力

- 新參與企業的威脅

- 替代品的威脅

- 競爭公司之間的競爭關係

- 地緣政治對紡織品市場的影響

第5章:市場規模及成長率預測(以金額為準:10億美元)

- 透過使用

- 時尚與服裝

- 工業和技術用紡織品

- 家用及家用紡織品

- 用於醫療保健領域的紡織品

- 汽車和運輸紡織品

- 其他(防護和運動紡織品等)

- 按成分

- 天然纖維

- 棉布

- 羊毛

- 絲綢

- 合成纖維

- 聚酯纖維

- 尼龍

- 人造絲/粘膠纖維

- 丙烯酸纖維

- 聚丙烯

- 再生纖維

- 其他(特殊高性能纖維(芳香聚醯胺、碳纖維、超高分子量聚乙烯))

- 天然纖維

- 透過製造程序和技術

- 織物

- 針織

- 不織布

- 紡絲成網(紡粘/熔噴)

- 乾式突襲水力纏繞

- 濕法成網

- 針刺機

- 立體編織織物/間隔織物

- 按地區

- 巴西

- 阿根廷

- 秘魯

- 南美洲其他地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Vicunha Textil

- Coteminas SA

- Santana Textiles Group

- Buddemeyer SA

- Springs Global

- Lenzing AG

- Freudenberg Performance Materials

- Indorama Ventures(PET Brazil)

- Ahlstrom-Munksjo

- Beaulieu Technical Textiles

- HUESKER Synthetic GmbH

- TWE Group

- PFNonwovens

- DuPont de Nemours

- Berry Global Group

- Toray Industries

- Schoeller Textil AG

- Borgers SE & Co. KG

- Kaltex Textiles

- Albini Group

第7章 市場機會與未來展望

The South America Textile Market size is projected to expand from USD 36.21 billion in 2025 and USD 38.59 billion in 2026 to USD 54.25 billion by 2031, registering a CAGR of 7.05% between 2026 to 2031.

Benefits from apparel demand in Brazil and Argentina now overlap with structural gains in geotextiles, hygiene nonwovens, and recycled-polyester fiber, broadening the revenue base beyond fashion. Higher European circular-economy standards accelerated investment in traceable supply chains and Digital Product Passport pilots, positioning compliant exporters for tariff-free access to the EU. Foreign direct investment from Lenzing and Indorama secures regional feedstock, strengthens recycling infrastructure, and shields multinationals from cotton-price swings. At the same time, Sao Paulo's informal hubs cut design-to-shelf cycles to under 14 days, forcing formal mills to adopt on-demand manufacturing or risk erosion of their share. Energy-price volatility, especially Brazil's 12% electricity hike in 2025, continues to pressure dyeing and finishing margins.

South America Textile Market Trends and Insights

Uptake of Technical Textiles in Regional Mobility & Infrastructure

Brazil's 2024-2030 infrastructure plan earmarks USD 56 billion for transport upgrades, many of which require nonwoven geotextiles that meet ASTM standards. Demand for high-tenacity polyester fabrics in Argentina's Vaca Muerta shale projects rose 19% in 2025, reflecting stricter environmental protocols. Peru's mining sector is now specifying tailings-dam reinforcement fabrics, attracting European suppliers through Lima distributors. Enforcement of engineering standards, such as Brazil's ABNT NBR 12553, tilts procurement toward certified local producers. Consistent inspection remains critical, as lax oversight previously let substandard imports undercut compliant products.

Fast-Fashion Cycles and On-Demand Manufacturing

Informal clusters in Sao Paulo's Bras district and Buenos Aires' La Salada market turn social-media trends into finished garments within two weeks. Micro-factories combine cutting, sewing, and finishing on a single site, bypassing wholesalers and selling on Instagram or WhatsApp. By 2025, these informal operations produced 38% of Brazil's domestic apparel volume, underscoring their scale. Formal mills answer with digital printing and modular lines that trim minimum orders to 50 units, yet still struggle to match the agility without compromising traceability. Tension between speed and compliance will rise as EU buyers demand verified labor standards, pushing informal players either toward legalization or toward shrinking export avenues.

Volatile Energy and Raw-Material Prices

A 12% rise in Brazilian electricity tariffs during 2025 deepened margin pressure for energy-intensive dyeing and stentering operations. Cotton prices in Argentina spiked 18% in 2024 after the Chaco droughts, forcing mills to import at a premium. Polyester costs mirror crude-oil swings with a 60-day lag, leaving mills exposed under fixed-price apparel contracts. Producers with vertically integrated recycling, such as Indorama's Sao Paulo rPET facility, hedge against volatility in virgin resin prices. Firms lacking such buffers delay capex, risking obsolescence as buyers gravitate toward price-stable suppliers.

Other drivers and restraints analyzed in the detailed report include:

- E-Commerce and Social-Commerce Compressing Design-to-Shelf Time

- Mandatory EU-27 Separate Textile-Waste Collection (2025)

- High Capex for Advanced Recycling / Sorting Capacity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The South America textile market share of Fashion & Apparel remains dominant at 55.55% yet slowing discretionary spend and mounting second-hand imports temper its pace. The industrial/Technical Textiles segment is advancing at a 6.15% CAGR, faster than any other application. Demand originates from civil-engineering geotextiles for Brazil's USD 56 billion transport overhaul and filtration fabrics keyed to Peru's mining sector. Apparel houses still invest in near-shoring to Argentina to avoid tariffs, but performance fabrics for oil, gas, and construction now capture a growing share of procurement budgets.

Technical textile producers bank on public procurement that mandates ASTM and ABNT certification, favouring mills with in-house labs. Local champions like Ober add ISO 9001 systems, while newcomers partner with German specialist HUESKER to deliver turnkey erosion-control solutions. Success hinges on the rapid commercialization of recycled-polyester geogrids that align with EU buyers' sustainability scorecards. Apparel mills counter by embedding QR-coded traceability to justify higher price points, signalling that both segments will coexist but with converging technology platforms.

The South America Textile Market Report is Segmented by Application (Fashion & Apparel, Industrial/Technical, and More), by Raw Material (Natural Fibers, Synthetic Fibers, Recycled Fibers, Specialty High-Performance Fibers), by Process/Technology (Woven, Knitted, Non-Woven, 3D Weaving & Spacer Fabrics), and by Geography (Brazil, Argentina, Peru, Rest of South America). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Vicunha Textil

- Coteminas S.A.

- Santana Textiles Group

- Buddemeyer S.A.

- Springs Global

- Lenzing AG

- Freudenberg Performance Materials

- Indorama Ventures (PET Brazil)

- Ahlstrom-Munksjo

- Beaulieu Technical Textiles

- HUESKER Synthetic GmbH

- TWE Group

- PFNonwovens

- DuPont de Nemours

- Berry Global Group

- Toray Industries

- Schoeller Textil AG

- Borgers SE & Co. KG

- Kaltex Textiles

- Albini Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Fast-fashion cycles & on-demand manufacturing

- 4.2.2 Mandatory EU-27 separate textile-waste collection (2025)

- 4.2.3 E-commerce & social-commerce compressing design-to-shelf time

- 4.2.4 Uptake of technical textiles in regional mobility & infrastructure

- 4.2.5 Surging investor interest in low-impact South-American natural fibres

- 4.2.6 Blockchain-enabled "Digital Product Passport" pilots in MERCOSUR

- 4.3 Market Restraints

- 4.3.1 Volatile energy & raw-material prices

- 4.3.2 High capex for advanced recycling / sorting capacity

- 4.3.3 Skilled-labour shortages (dyeing, finishing, automation)

- 4.3.4 SME fragmentation vs. new ESG / due-diligence compliance

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Impact of Geopolitics on Textile Market

5 Market Size & Growth Forecasts (Value, In USD Billion)

- 5.1 By Application

- 5.1.1 Fashion & Apparel

- 5.1.2 Industrial/Technical Textiles

- 5.1.3 Household & Home Textiles

- 5.1.4 Medical & Healthcare Textiles

- 5.1.5 Automotive & Transport Textiles

- 5.1.6 Others (Protective, Sports Textiles, etc.)

- 5.2 By Raw Material

- 5.2.1 Natural Fibers

- 5.2.1.1 Cotton

- 5.2.1.2 Wool

- 5.2.1.3 Silk

- 5.2.2 Synthetic Fibers

- 5.2.2.1 Polyester

- 5.2.2.2 Nylon

- 5.2.2.3 Rayon / Viscose

- 5.2.2.4 Acrylic

- 5.2.2.5 Polypropylene

- 5.2.3 Recycled Fibers

- 5.2.4 Others (Speciality High-Performance Fibers (Aramid, Carbon, UHMWPE))

- 5.2.1 Natural Fibers

- 5.3 By Process / Technology

- 5.3.1 Woven

- 5.3.2 Knitted

- 5.3.3 Non-woven

- 5.3.3.1 Spunlaid (Spunbond / Melt-blown)

- 5.3.3.2 Dry-laid Hydro-entangled

- 5.3.3.3 Wet-Laid

- 5.3.3.4 Needle-punched

- 5.3.4 3-D Weaving & Spacer Fabrics

- 5.4 By Geography

- 5.4.1 Brazil

- 5.4.2 Argentina

- 5.4.3 Peru

- 5.4.4 Rest of South America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)}

- 6.4.1 Vicunha Textil

- 6.4.2 Coteminas S.A.

- 6.4.3 Santana Textiles Group

- 6.4.4 Buddemeyer S.A.

- 6.4.5 Springs Global

- 6.4.6 Lenzing AG

- 6.4.7 Freudenberg Performance Materials

- 6.4.8 Indorama Ventures (PET Brazil)

- 6.4.9 Ahlstrom-Munksjo

- 6.4.10 Beaulieu Technical Textiles

- 6.4.11 HUESKER Synthetic GmbH

- 6.4.12 TWE Group

- 6.4.13 PFNonwovens

- 6.4.14 DuPont de Nemours

- 6.4.15 Berry Global Group

- 6.4.16 Toray Industries

- 6.4.17 Schoeller Textil AG

- 6.4.18 Borgers SE & Co. KG

- 6.4.19 Kaltex Textiles

- 6.4.20 Albini Group

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

綠色紡織品市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、原料、應用、地區和競爭格局分類,2021-2031年

綠色紡織品市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、原料、應用、地區和競爭格局分類,2021-2031年 防護紡織品市場:按類型、產品類型、最終用途和分銷管道分類 - 2026-2032年全球市場預測動物源性紡織品市場:2026-2032年全球市場按形態、產品類型、通路和應用分類的預測紡織品市場:按材料、應用和分銷管道分類-2026-2032年全球市場預測

防護紡織品市場:按類型、產品類型、最終用途和分銷管道分類 - 2026-2032年全球市場預測動物源性紡織品市場:2026-2032年全球市場按形態、產品類型、通路和應用分類的預測紡織品市場:按材料、應用和分銷管道分類-2026-2032年全球市場預測 2026-2034年全球服飾市場規模、佔有率、趨勢和成長分析報告紗線、纖維和線材市場:按產品類型、原料、製造流程、撚度、應用、分銷通路和最終用途產業分類-全球預測,2026-2032年

2026-2034年全球服飾市場規模、佔有率、趨勢和成長分析報告紗線、纖維和線材市場:按產品類型、原料、製造流程、撚度、應用、分銷通路和最終用途產業分類-全球預測,2026-2032年 紡織品市場分析及預測(至2035年):依類型、產品類型、技術、應用、材料類型、最終用戶、製程、組件及採用度分類

紡織品市場分析及預測(至2035年):依類型、產品類型、技術、應用、材料類型、最終用戶、製程、組件及採用度分類 亞太地區紡織品:市佔率分析、產業趨勢與統計、成長預測(2026-2031)紡織品市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並預測至2026-2034年

亞太地區紡織品:市佔率分析、產業趨勢與統計、成長預測(2026-2031)紡織品市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並預測至2026-2034年 日本紡織品市場:規模、佔有率、趨勢和預測:按原料、產品、應用和地區分類,2026-2034年

日本紡織品市場:規模、佔有率、趨勢和預測:按原料、產品、應用和地區分類,2026-2034年