|

市場調查報告書

商品編碼

2043977

南美軟性飲料包裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)South America Soft Drinks Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

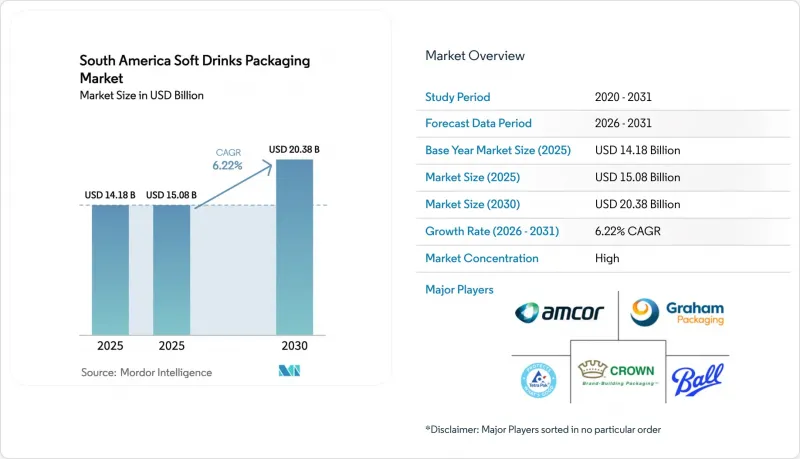

預計到 2025 年,南美軟性飲料包裝市場價值將達到 141.8 億美元,到 2026 年將成長至 150.8 億美元,到 2031 年將達到 203.8 億美元,2026 年至 2031 年的複合年成長率為 6.22%。

巴西強制再生材料法和南方共同市場關於食品接觸材料的統一法規,推動了對再生聚對苯二甲酸乙二醇酯(rPET)、輕質材料和逆向物流網路的領先投資,使先行者獲得成本優勢並與零售商建立了牢固的關係。秘魯和哥倫比亞的快速收入成長、巴西和阿根廷食品電商市場的擴張,以及對衛生一次性包裝的持續需求,即使消費者傾向於轉向價格較低的飲料,也推動了銷售的持續成長。另一方面,樹脂和鋁價格的波動、押金返還機制的區域差異以及多層複合材料的禁令,正在擠壓加工商的利潤空間,並加速產業整合。由於前五大加工商僅佔區域銷售額的約45%,競爭仍然適中,這為中型專業生產包裝袋、無菌紙盒和玻璃容器的企業留下了發展空間。

南美軟性飲料包裝市場趨勢與洞察

可支配所得增加和中產階級擴大

到了2025年,秘魯和哥倫比亞實際薪資成長4.2%,提升兩國家庭的購買力,從而形成兩極化的需求模式:大城市更青睞高階機能飲料,而小城鎮則更傾向於價格較低的碳酸飲料。在巴西,中產階級家庭增加了310萬戶,但食品雜貨和交通成本的通膨上升,促使消費者轉向購買更大容量的多份裝飲料,因為這類飲料每公升的價格更低。這種包裝規格的兩極化解釋了為什麼小包裝的單份裝飲料成長更快,而251-500毫升的規格仍然佔據主導地位。在秘魯,500毫升的等滲透壓飲料在阿雷基帕等礦業中心的輪班工人中市場佔有率有所成長,因為他們需要隨時隨地補充水分。在哥倫比亞,新的勞動法規正式承認了零工經濟,提高了課稅收入,從而刺激了對罐裝和袋裝飲料的需求,這些飲料深受送貨司機的歡迎。

寶特瓶水消費量激增

都市區供水持續不均,導致阿根廷22%的都市區家庭和秘魯31%的城市家庭無法獲得可靠的自來水供應,從而推動了瓶裝水的日常消費以及500毫升一次性瓶裝水的持續銷售。可口可樂公司預計,到2025年,其區域飲用水產品組合的銷售量將成長7%,並已在巴西容迪亞伊投資8,500萬美元用於PET瓶坯生產,以滿足市場需求。輕量化技術已將500毫升瓶裝水的重量降低至24克,樹脂用量減少了14%,但也需要更嚴格的品質檢測。在智利,更嚴格的微生物標準增加了小規模品牌的合規成本,同時也加速了產業整合。在巴西東北部,常年氣溫超過攝氏30度,人們隨時隨地飲用瓶裝水的需求推動了一次性瓶裝水的持續成長。

樹脂和鋁價格波動

2025年,原油價格波動和工廠停工導致PET價格在每噸1,050美元至1,380美元之間波動,飲料品牌抵制季節性價格上漲,擠壓了加工商的利潤空間。倫敦金屬交易所(LME)鋁的平均價格為每噸2,420美元,南美製罐製造商需支付每噸180美元的運費溢價,並面臨該地貨幣波動的風險。由於巴西諾貝麗斯(Novelis)和阿根廷阿爾阿爾(Al-Al)的運作接近滿載運轉,哥倫比亞卷材進口商被迫接受22%的成本上漲,這減緩了製罐的普及。現貨價格波動迫使加工商要麼進行避險,要麼接受更低的利潤率,這增加了再生PET(rPET)的吸引力。 rPET的價格與原生樹脂的價格相關性越來越低。

細分市場分析

2025年,塑膠製品佔銷售額的61.48%,其中寶特瓶憑藉其透明度、成本優勢和高效的配送效率脫穎而出。在塑膠產業中,rPET細分市場預計將在2031年前以6.98%的複合年成長率成長,這主要得益於對再生材料的強制性需求,以及配套的綜合供應合約和化學回收試點計畫的支持。儘管價格有所波動,金屬容器(主要是鋁罐)仍佔23%的市場佔有率。這主要歸功於其「無限循環利用」的特性,深受都市區千禧世代消費者的青睞。玻璃容器在高階果汁和精釀汽水市場保持著9%的市場佔有率。這主要得益於Verallia公司推出的新型氧氣燃燒爐,該爐使用55%的玻璃屑作為原料,與傳統熔煉製程相比,碳排放強度降低了18%。紙板基無菌包裝佔6.7%的市場佔有率,這主要得益於利樂公司大力推廣常溫物流和適用於商店展示的電商包裝設計。由於重量減輕,500毫升寶特瓶的重量將從2023年的26克減少到2025年的23克,而安姆科的氧氣吸收劑專利旨在進一步減輕12%的重量,同時不影響保存期限。

受成本壓力和永續性品牌理念的驅動,加工商的資本投資持續轉向rPET、阻隔塗層和紙塑複合結構,這些材料可提供更廣泛的處置選擇。南方共同市場統一的PET標準對沒有ISO 22000認證檢查室的小規模工廠構成合規障礙,但卻為跨國公司提供了跨境貿易便利。因此,預計南美軟性飲料塑膠包裝市場將持續擴張,而金屬和紙盒包裝預計將透過技術升級和強調可回收性的行銷,保持各自的成長動能。

到2025年,瓶裝飲料將佔44.98%的市場佔有率,其中PET瓶裝約佔四分之三。這主要歸功於PET瓶裝飲料的普及性和填充速度快。然而,受線上生鮮配送的推動,磅裝和小袋預計將以6.95%的複合年成長率成長,因為線上生鮮配送在最後一公里配送中優先考慮體積效率和重量減輕。鋁罐將佔據28%的市場佔有率,並在快餐店中佔據更多市場佔有率,因為鋁罐的單份衛生和免清洗功能優勢超過了金屬材料較高的成本。紙盒和無菌包裝將佔18%的市場佔有率,它們憑藉更長的保存期限在果汁和植物性飲料市場競爭,但在阿根廷,由於消費者普遍認為紙板質量低劣,它們面臨著形象障礙。

軟包裝袋在小規模零售店,尤其是在秘魯,優勢日益凸顯。在秘魯,300毫升的軟包裝袋每份的成本比PET瓶低35%。巴西一家連鎖餐廳為了減少飲料破損,統一使用250毫升的罐裝飲料,儘管金屬成本上漲,罐裝飲料的出貨量仍增加了9%。同時,聖地牙哥開展的一項玻璃瓶回收試點計畫顯示,回收率僅41%,凸顯了在缺乏完善的押金制度的情況下,改變消費者習慣的難度。隨著加工商大力推廣機器人裝箱機和易撕口設計,軟包裝袋有望在衝動消費和電商通路中搶佔瓶裝飲料的市場佔有率,進一步加速南美軟性飲料包裝向更輕、更靈活的形式轉變。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 可支配所得增加和中產階級擴大

- 寶特瓶水消費量激增

- 後疫情時代對衛生單份包裝的需求

- 永續性措施、再生PET和強制減重

- 電子商務推動了食品雜貨市場的成長,從而提振了對現貨配送產品的需求。

- 標準化灌裝瓶計劃

- 市場限制因素

- 嚴格禁止使用不可回收塑膠

- 樹脂和鋁價格波動

- 巴西以外地區引入存款返還制度的延遲

- 安地斯國家缺乏回收基礎設施

- 產業供應鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 供應商議價能力

- 買方的議價能力

- 新參與企業的威脅

- 替代品的威脅

- 競爭公司之間的競爭關係

- 全球軟性飲料包裝市場概覽

- 對影響市場的宏觀經濟因素進行評估

第5章 市場規模與成長預測

- 材料

- 塑膠

- 金屬

- 玻璃

- 紙張和紙板

- 按包裝類型

- 瓶子

- 能

- 紙箱及無菌包裝

- 小袋/小包

- 按飲料類型

- 碳酸飲料(CSD)

- 果汁花蜜

- 即飲飲料

- 運動飲料/等滲透壓飲料

- 其他飲料

- 按產能

- 250毫升或以下

- 251~500 ml

- 501~1000 ml

- 超過1公升

- 國家

- 巴西

- 阿根廷

- 智利

- 哥倫比亞

- 秘魯

- 南美洲其他地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Amcor plc

- Ball Corporation

- Crown Holdings, Inc.

- Tetra Pak International SA

- CAN-PACK SA

- Ardagh Group SA

- Trivium Packaging BV

- Graham Packaging Company LP

- Refresco Group NV

- Victory Packaging LP

- Plastipak Holdings, Inc.

- Owens-Illinois Inc.

- SIG Combibloc Group Ltd.

- AptarGroup, Inc.

- Envases Universales de Mexico SA de CV

- Ecolean AB

- Alpek SAB de CV

- CCL Industries Inc.

- Verallia SA

第7章 市場機會與未來展望

The South America soft drinks packaging market size was valued at USD 14.18 billion in 2025 and is estimated to grow from USD 15.08 billion in 2026 to USD 20.38 billion by 2031, at a CAGR of 6.22% over 2026-2031.

Mandatory recycled-content laws in Brazil and harmonized food-contact rules in MERCOSUR are prompting early investments in rPET, lightweighting, and reverse-logistics networks, giving first movers cost advantages and stronger retail ties. Rapid income growth in Peru and Colombia, expanding e-commerce grocery penetration in Brazil and Argentina, and persistent demand for hygienic single-serve packs continue to lift unit volumes even as consumers trade down to value beverages. At the same time, volatile resin and aluminum prices, fragmented deposit-return roll-outs, and bans on multi-material laminates are squeezing converter margins and accelerating consolidation. Competitive intensity remains moderate because the top five converters control only about 45% of regional revenue, leaving space for mid-tier specialists in pouches, aseptic cartons, and glass.

South America Soft Drinks Packaging Market Trends and Insights

Rising Disposable Income And Middle-Class Expansion

Real wage gains of 4.2% in 2025 lifted household purchasing power in Peru and Colombia, creating a two-tier demand pattern that splits premium functional drinks in large cities from value carbonated offerings in secondary towns. Brazil added 3.1 million middle-class families, yet higher food and transport inflation nudged shoppers toward larger multi-serve bottles, which lower per-liter costs. The pack-size dichotomy helps explain why 251-500 ml formats still dominate while smaller single-serve packs post faster growth. In Peru's mining hubs, such as Arequipa, 500 ml isotonic bottles gained share among shift workers seeking on-the-go hydration solutions. Colombia's new labor rules, formalizing gig-economy jobs, expanded tax-based income, boosting demand for cans and pouches popular with delivery riders.

Surge In PET Bottled-Water Consumption

Persistent gaps in municipal water supply leave 22% of Argentine and 31% of Peruvian urban households without reliable tap water, driving daily bottled-water use and consistent 500 ml single-serve purchases. Coca-Cola reported a 7% volume jump in its regional water portfolio during 2025 and invested USD 85 million in PET preform capacity at Jundiai, Brazil, to meet demand. Lightweighting cut the 500 ml bottle weight to 24 grams, saving 14% in resin but requiring stricter quality checks. Chile tightened microbiological rules, raising compliance costs for small brands yet accelerating consolidation. Out-of-home consumption in Brazil's Northeast, where temperatures exceed 30 °C year-round, underpins sustained growth in single-serve water formats.

Volatile Resin And Aluminum Prices

PET prices fluctuated between USD 1,050-1,380 per t in 2025 due to crude swings and plant outages, squeezing converter margins as beverage brands resisted mid-season price hikes. Aluminum averaged USD 2,420 per t on the LME, with South American can makers paying freight premiums of USD 180 per t and facing local currency volatility. Brazil's Novelis and Argentina's Aluar ran near full capacity, so Colombian coil importers paid a 22% cost penalty that slowed can adoption. Spot volatility forces converters to hedge or accept thinner margins, reinforcing the appeal of rPET, whose pricing increasingly decouples from virgin resin.

Other drivers and restraints analyzed in the detailed report include:

- Post-COVID Demand For Hygienic Single-Serve Packs

- Sustainability Push, rPET And Lightweighting Mandates

- Stringent Bans On Non-Recyclable Plastics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Plastic held 61.48% of 2025 revenue, anchored by PET bottles that combine clarity, cost, and distribution efficiency. Within plastics, the rPET subsegment is set to expand at a 6.98% CAGR through 2031 as mandates raise demand for recycled content, supporting integrated supply contracts and chemical-recycling pilots. Metal formats, chiefly aluminum cans, captured 23% despite price volatility because of their infinite recyclability, which resonates with urban millennial shoppers. Glass maintained a 9% niche in premium juice and craft soda, reinforced by Verallia's new oxy-combustion furnace that runs on 55% cullet feed and lowers carbon intensity by 18% versus legacy melts. Paperboard-based aseptic cartons rounded out 6.7%, benefiting from ambient logistics and shelf-ready e-commerce designs promoted by Tetra Pak. Lightweighting trimmed 500 ml PET bottles from 26 g in 2023 to 23 g in 2025, and Amcor's oxygen-scavenger patents aim to drop them another 12% without compromising shelf life.

Cost pressure and sustainability branding continue to tilt converter capex toward rPET, barrier coatings, and hybrid paper-plastic structures that broaden end-of-life options. MERCOSUR's unified PET standard adds compliance hurdles for small plants lacking ISO 22000 labs but enhances cross-border trade for multinationals. As a result, the South America soft drinks packaging market size tied to plastic is forecast to widen even while metal and carton formats defend their own growth lanes through technical upgrades and marketing that highlights recyclability.

Bottles commanded 44.98% in 2025, with PET accounting for nearly three-quarters of volume owing to familiarity and high filling speeds. Yet pouches and sachets are on track for a 6.95% CAGR, propelled by online grocery fulfillment that values cube efficiency and lighter last-mile payloads. Aluminum cans held 28% and gained share in quick-service restaurants where single-serve hygiene and no-rinse benefits outweigh metal premiums. Cartons and aseptic boxes, at 18%, leverage ambient stability to compete in juice and plant-based drinks but face perception hurdles in Argentina, where consumers regard paperboard as lower tier.

Pouches excel in informal retail, especially in Peru, where 300 ml flexible packs undercut PET by 35% per serving. Brazil's restaurant chains standardized 250 ml cans to cut breakage, boosting can volume 9% despite metal costs. Meanwhile, pilot refillable-glass programs in Santiago achieved only 41% return rates, underscoring the challenge of changing consumer habits without a robust deposit infrastructure. As converters push robotic case-packers and easy-open tear notches, pouches look poised to erode share from bottles in impulse and e-commerce channels, reinforcing the South America soft drinks packaging market's shift toward lightweight flexible formats.

The South America Soft Drinks Packaging Market Report is Segmented by Material (Plastic, Metal, and More), Packaging Format (Bottles, Cartons and Aseptic Boxes, and More), Beverage Type (Carbonated Soft Drinks, Juices and Nectars, Ready-To-Drink Beverages, Sports and Isotonic Drinks, and More), Pack Size (Less Than Equal To 250 Ml, 251-500 Ml, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Amcor plc

- Ball Corporation

- Crown Holdings, Inc.

- Tetra Pak International S.A.

- CAN-PACK S.A.

- Ardagh Group S.A.

- Trivium Packaging B.V.

- Graham Packaging Company L.P.

- Refresco Group N.V.

- Victory Packaging L.P.

- Plastipak Holdings, Inc.

- Owens-Illinois Inc.

- SIG Combibloc Group Ltd.

- AptarGroup, Inc.

- Envases Universales de Mexico S.A. de C.V.

- Ecolean AB

- Alpek S.A.B. de C.V.

- CCL Industries Inc.

- Verallia S.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Disposable Income and Middle-Class Expansion

- 4.2.2 Surge in PET Bottled-Water Consumption

- 4.2.3 Post-COVID Demand for Hygienic Single-Serve Packs

- 4.2.4 Sustainability Push, rPET and Lightweighting Mandates

- 4.2.5 E-commerce Grocery Growth Spurring Shelf-Ready Formats

- 4.2.6 Standardized Refillable Bottle Programs

- 4.3 Market Restraints

- 4.3.1 Stringent Bans on Non-Recyclable Plastics

- 4.3.2 Volatile Resin and Aluminum Prices

- 4.3.3 Slow Deposit-Return Roll-Out Outside Brazil

- 4.3.4 Limited Recycling Infrastructure in Andean Nations

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Overview of Global Soft Drinks Packaging Market

- 4.9 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Material

- 5.1.1 Plastic

- 5.1.2 Metal

- 5.1.3 Glass

- 5.1.4 Paper and Paperboard

- 5.2 By Packaging Format

- 5.2.1 Bottles

- 5.2.2 Cans

- 5.2.3 Cartons and Aseptic Boxes

- 5.2.4 Pouches and Sachets

- 5.3 By Beverage Type

- 5.3.1 Carbonated Soft Drinks (CSDs)

- 5.3.2 Juices and Nectars

- 5.3.3 Ready-to-Drink (RTD) Beverages

- 5.3.4 Sports and Isotonic Drinks

- 5.3.5 Other Beverage Types

- 5.4 By Pack Size

- 5.4.1 Less Than Equal To 250 ml

- 5.4.2 251 - 500 ml

- 5.4.3 501 - 1000 ml

- 5.4.4 More Than 1 L

- 5.5 By Country

- 5.5.1 Brazil

- 5.5.2 Argentina

- 5.5.3 Chile

- 5.5.4 Colombia

- 5.5.5 Peru

- 5.5.6 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Amcor plc

- 6.4.2 Ball Corporation

- 6.4.3 Crown Holdings, Inc.

- 6.4.4 Tetra Pak International S.A.

- 6.4.5 CAN-PACK S.A.

- 6.4.6 Ardagh Group S.A.

- 6.4.7 Trivium Packaging B.V.

- 6.4.8 Graham Packaging Company L.P.

- 6.4.9 Refresco Group N.V.

- 6.4.10 Victory Packaging L.P.

- 6.4.11 Plastipak Holdings, Inc.

- 6.4.12 Owens-Illinois Inc.

- 6.4.13 SIG Combibloc Group Ltd.

- 6.4.14 AptarGroup, Inc.

- 6.4.15 Envases Universales de Mexico S.A. de C.V.

- 6.4.16 Ecolean AB

- 6.4.17 Alpek S.A.B. de C.V.

- 6.4.18 CCL Industries Inc.

- 6.4.19 Verallia S.A.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

軟性飲料包裝市場:依包裝材料、包裝類型和最終用途產業分類-2026-2032年全球市場預測

軟性飲料包裝市場:依包裝材料、包裝類型和最終用途產業分類-2026-2032年全球市場預測 軟性飲料包裝市場機會、成長促進因素、產業趨勢分析及預測(2026-2035年)

軟性飲料包裝市場機會、成長促進因素、產業趨勢分析及預測(2026-2035年) 軟性飲料包裝市場-2026-2031年預測

軟性飲料包裝市場-2026-2031年預測 軟性飲料包裝:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)中東和非洲軟性飲料包裝:市場佔有率分析、產業趨勢、成長預測(2025-2030)北美軟性飲料包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)拉丁美洲軟性飲料包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)歐洲軟性飲料包裝:市場佔有率分析、產業趨勢、成長預測(2025-2030)美國軟性飲料包裝:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

軟性飲料包裝:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)中東和非洲軟性飲料包裝:市場佔有率分析、產業趨勢、成長預測(2025-2030)北美軟性飲料包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)拉丁美洲軟性飲料包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)歐洲軟性飲料包裝:市場佔有率分析、產業趨勢、成長預測(2025-2030)美國軟性飲料包裝:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)