|

市場調查報告書

商品編碼

2043973

南美洲塑膠瓶蓋和封蓋:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)South America Plastic Caps And Closures - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

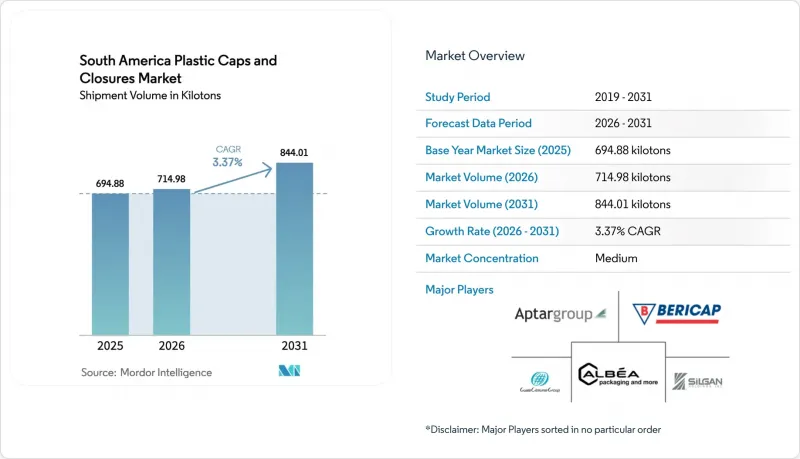

2025 年南美洲塑膠瓶蓋和封蓋市場價值為 694.88 千噸,預計到 2031 年將從 2026 年的 714.98 千噸成長至 844.01 千噸,預測期(2026-2031 年)複合年成長率為 3.37%。

關於再生材料含量的有利法規、電子商務履約的快速發展以及出口商對歐盟瓶蓋法規的回應,正促使人們重新評估產品規格和籌資策略。區域樹脂製造商 Braskem 正在加速向機械和化學回收等級的樹脂轉型,而高階個人護理和酒類品牌則開始採用智慧瓶蓋,以便在消費點驗證產品的真偽。能夠混合原生樹脂和廢棄樹脂、整合防篡改功能並處理促銷宣傳活動小批量生產的加工商正在獲得新契約。同時,隨著品牌所有者追求碳減排目標並尋求減輕聚丙烯價格波動的影響,更輕的瓶蓋正成為降低進入門檻的必要條件。

南美洲塑膠瓶蓋及封口件市場趨勢及洞察

行程途中飲料消費量激增

都市區通勤者更傾向於選擇單份寶特瓶飲料方便攜帶飲用,這迫使品牌商必須設計出能夠保持碳酸氣、防止洩漏且易於開啟的瓶蓋。零售數據顯示,巴西和哥倫比亞的軟性飲料和能量飲料銷量成長,其中運動飲料系列採用了翻蓋式和推拉式設計,方便單手操作。加工商也積極響應,推出了防篡改封條、洩壓閥和更堅固的鉸鏈設計,這些措施雖然使單價上漲了高達8%,但有助於零售商減少庫存損耗。對多腔壓縮模具的投資支撐了銷售量的激增,而重量減輕則抵消了部分新增功能帶來的成本。因此,一種良性循環正在形成:瓶蓋的細分市場不斷擴大,價值更高的瓶蓋不斷湧現,推高了平均售價。

寶特瓶乳類飲料的廣泛應用

巴西和阿根廷的乳製品生產商正從紙盒包裝轉向冷藏寶特瓶,這推動了對能夠保持風味並彰顯高階定位的瓶蓋的需求。利樂公司以甘蔗為原料的繫繩式瓶蓋表明,生物基材料既能滿足永續性目標,又能滿足性能需求。結合鋁箔內襯和防篡改環的雙層密封設計正日益受到關注,但其共射出成型成型工藝要求限制了其生產,目前只有大規模加工商才能生產。秘魯和哥倫比亞低溫運輸的擴建預計將在基礎設施完善後進一步刺激需求,使PET包裝的乳類飲料成為長期成長的關鍵領域。能夠共注塑不同樹脂並處理小批量彩色生產的瓶蓋製造商具有戰略優勢。

家用清潔劑包裝過渡到立式袋

在巴西和智利,軟包裝填充用裝如今已成為商店清潔劑和衣物柔順劑區的主流,硬質瓶蓋的需求正在下降。聯合利華在南美的銷售額在2024年成長了6.0%,這主要得益於軟包裝補充裝的流行,這種包裝重量減輕了70%,且每次使用成本更低。瓶蓋供應商正在探索帶有翻蓋式吸嘴的軟包裝補充裝,但這種子包裝形式目前僅佔所有軟包裝的不到5%。隨著濃縮洗衣凝珠的日益普及,除非加工商轉型為補充站的分配器頭,或設計出與薄膜層壓工藝相容的可重複密封吸嘴,否則瓶蓋的重要性可能會進一步下降。

細分市場分析

其他材料(主要包括再生PET、生物基聚乙烯和先進生質塑膠)預計將以4.33%的複合年成長率成長,超過南美塑膠瓶蓋和封口整體市場的表現,這主要得益於巴西從2026年起強制要求PET包裝中含有22%的再生材料。聚丙烯在2025年保持了44.20%的市場佔有率,但由於供應價格波動較大,高達每噸840美元,加工商為了滿足客戶的永續發展要求並維持利潤率,不得不摻入20-30%的消費後再生樹脂。

2025年6月,Braschem公司符合FDA標準的PCR PP產品掃清了食品接觸瓶蓋中使用再生PP的最後一道技術障礙。同時,生物基甘蔗PE產品符合Bonsucro認證要求,並在其生命週期內減少70%的碳排放。然而,秘魯和哥倫比亞食品級rPET產能有限,限制了PET瓶蓋市場的成長。目前,全部區域四種樹脂流進行驗證:原生樹脂、機械回收樹脂、化學回收樹脂和生物基樹脂,從而確保了供應的穩定性,但庫存成本也在上升。

到2025年,飲料瓶蓋將佔總出貨量的49.32%,主要得益於Ambev的啤酒廠和可口可樂FEMSA的裝瓶廠。然而,化妝品和洗漱用品瓶蓋預計將以更快的速度成長,複合年成長率達到4.52%,因為高階護膚和護髮產品正在採用軟壓泵和無氣泵來提高分裝精度。儘管銷量較低,但南美化妝品塑膠瓶蓋和封蓋市場的平均售價較高,抵消了部分成長。

隨著人均收入的成長,食品瓶蓋和封口市場也在擴張,而家用化學品瓶蓋和封口市場則因填充用包裝的普及而面臨盈利。醫藥保健品領域雖然仍屬於小眾市場,但由於巴西國家衛生監督局 (ANVISA) 和阿根廷國家藥品和醫療設備監管局 (ANMAT) 等機構要求的兒童安全鎖和乾燥劑等特性,該領域仍保持著較高的利潤率。在智利和巴西等品質監管更為嚴格的市場,品牌商為這些先進的瓶蓋設計支付的價格已經是普通螺旋蓋的三到五倍。

《南美塑膠瓶蓋及封蓋市場報告》按材料(PET、PP、LDPE 及其他)、終端用戶行業(飲料、食品及其他)、瓶蓋類型(螺旋蓋、繫繩蓋、兒童安全蓋及其他)、製造程序(射出成型、壓縮成型及其他)和地區(巴西、阿根廷、哥倫比亞及其他)進行細分。市場預測以銷售量(千噸)為單位。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 外出時飲料消費量激增

- 寶特瓶乳類飲料的日益普及

- 電子商務對防篡改包裝的需求激增

- 區域快速消費品公司自有品牌(PB)的擴張

- 主要飲料品牌進行填充和重複使用試點項目

- 南美出口商採納歐盟關於「捆綁銷售上限」的指令

- 市場限制因素

- 家用清潔劑市場向立式袋的轉變

- 加強太平洋聯盟的塑膠監管

- 原生聚丙烯的價格波動

- 消費者偏好高級啤酒的金屬皇冠蓋

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的競爭

- 宏觀經濟因素對市場的影響

第5章 市場規模與成長預測

- 材料

- 聚對苯二甲酸乙二醇酯(PET)

- 聚丙烯(PP)

- 低密度聚乙烯(LDPE)

- 高密度聚苯乙烯(HDPE)

- 其他

- 按最終用戶行業分類

- 飲料

- 食物

- 製藥和醫療保健

- 化妝品和盥洗用品

- 家用化學品

- 其他

- 按帽型

- 螺帽

- 繫繩帽

- 翻蓋式按扣帽

- 兒童安全蓋

- 豪華/高級裝飾帽

- 分配蓋

- 透過製造技術

- 射出成型

- 壓縮成型

- 三件式直列組裝

- 數位印刷智慧帽

- 國家

- 巴西

- 阿根廷

- 哥倫比亞

- 智利

- 秘魯

- 南美洲其他地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Silgan Holdings Inc.

- Albea SA

- Guala Closures SpA

- Bericap GmbH & Co. KG

- AptarGroup, Inc.

- Amcor plc

- Crown Holdings, Inc.

- Closure Systems International, Inc.

- Plastivaloire SE

- Tecnocap SpA

- Pano Cap (Canada) Limited

- Mold-Tek Packaging Limited

- RPC M& H Plastics Ltd.

- Oben Holding Group SAC

- Universal Closures Ltd.

- Paccor Packaging GmbH

- Weener Plastics Group BV

- Freudenberg Home and Cleaning Solutions GmbH

- Comar, LLC

第7章 市場機會與未來展望

The South America plastic caps and closures market size was valued at 694.88 kilotons in 2025 and estimated to grow from 714.98 kilotons in 2026 to reach 844.01 kilotons by 2031, at a CAGR of 3.37% during the forecast period (2026-2031).

Favorable recycled-content mandates, the rapid uptick in e-commerce fulfillment, and exporter alignment with the European Union tethered-cap rule are redefining product specifications and sourcing strategies. Regional resin producer Braskem has accelerated the shift toward mechanically and chemically recycled grades, while premium personal-care and spirits brands are installing smart closures that validate authenticity at the point of consumption. Converters able to blend virgin and post-consumer resin, integrate tamper-evident functionality, and offer short print runs for promotional campaigns are winning new contracts. At the same time, closure lightweighting is becoming a cost-of-entry requirement as brand owners pursue carbon-reduction targets and seek relief from volatile polypropylene prices.

South America Plastic Caps And Closures Market Trends and Insights

Surging On-The-Go Beverage Consumption

Urban commuters are favoring single-serve PET bottles that can be consumed on the move, pushing brands to specify closures that maintain carbonation, resist leakage, and open smoothly. Retail data show soft-drink and energy-drink volumes rising in Brazil and Colombia, and sports-drink lines are adopting flip-top and push-pull designs that enable one-handed use. Converters are responding with tamper-evident bands, pressure-relief vents, and stronger hinge designs that add up to 8% to unit cost yet reduce shrinkage for retailers. Investment in high-cavity compression molds supports the volume surge, while lightweighting offsets part of the added feature cost. The net effect is a positive mix shift toward value-added closures that lift average selling prices.

Rising Penetration of PET Bottled Dairy Drinks

Dairy processors in Brazil and Argentina are switching from cartons to chilled PET bottles, driving demand for closures that protect flavor and signal premium positioning. Sugarcane-based tethered caps introduced by Tetra Pak demonstrate that bio-attributed materials can meet both sustainability targets and performance needs. Dual-seal designs combining foil liners with tamper rings are gaining traction, though their co-injection tooling requirements limit production to larger converters. Cold-chain expansion in Peru and Colombia will unlock additional volume once infrastructure matures, making PET dairy drinks a key long-term growth pocket. Closure makers able to co-mold dissimilar resins and manage small color runs hold a strategic edge.

Shift Toward Stand-Up Pouches In Household Cleaners

Flexible refill pouches now dominate detergent and fabric-softener aisles in Brazil and Chile, reducing demand for rigid-bottle closures. Unilever's South America revenue rose 6.0% in 2024, helped by pouch formats that weigh 70% less and sell at a lower cost-per-use. Closure suppliers are exploring spouted pouches with flip-tops, yet the subformat still accounts for less than 5% of flexible-pack volume. As concentrated pods gain traction, closures could lose further relevance unless converters pivot to dispensing heads for refill stations or design resealable spouts compatible with film laminates.

Other drivers and restraints analyzed in the detailed report include:

- Booming E-Commerce Demand For Tamper-Evident Packaging

- Private-Label Expansion Among Regional FMCG Players

- Growing Anti-Plastic Regulations In Pacific Alliance

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Other Materials, mainly recycled PET, bio-based polyethylene, and advanced bioplastics, are forecast to outpace the overall South America plastic caps and closures market at a 4.33% CAGR, benefiting from Brazil's 22% mandatory recycled content in PET packaging beginning in 2026. Polypropylene retained 44.20% volume share in 2025, but volatile offer prices at USD 840 per tonne have prompted converters to blend in 20-30% post-consumer resin, safeguarding margins while meeting client sustainability commitments.

Braskem's FDA-compliant PCR PP launched in June 2025 removed the last technical barrier to using recycled PP in food-contact closures. Meanwhile, bio-attributed sugarcane PE qualifies for Bonsucro certification and cuts life-cycle carbon emissions by 70%. Limited food-grade rPET capacity in Peru and Colombia, however, constrains PET closure growth. Across the region, converters now qualify four resin streams, virgin, mechanically recycled, chemically recycled, and bio-based, raising inventory costs yet providing supply resilience..

Beverage closures delivered 49.32% of volume in 2025 thanks to Ambev's breweries and Coca-Cola FEMSA's bottling footprint. Even so, cosmetics and toiletries closures will grow faster at 4.52% CAGR as premium skincare and hair-care lines adopt soft-squeeze and airless pumps that improve dosing precision. The South America plastic caps and closures market size for cosmetics commands higher average selling prices, offsetting lower tonnage.

Food closures advance in lockstep with rising per-capita income, while household-chemical closures suffer from refill pouches. Pharmaceutical and healthcare remain niche but highly profitable because of child-resistant and desiccant-integrated features demanded by ANVISA and ANMAT. Brand owners in Chile and Brazil, markets with stricter quality regulation, already pay 3-5 times the price of commodity screw caps for these advanced formats.

The South America Plastic Caps and Closures Market Report is Segmented by Material (PET, PP, LDPE, and More), End-User Industry (Beverage, Food, and More), Cap Type (Screw Closures, Tethered Caps, Child-Resistant Closures, and More), Manufacturing Technology (Injection Molding, Compression Molding, and More), and Geography (Brazil, Argentina, Colombia, and More). The Market Forecasts are Provided in Terms of Volume (Kilotons).

List of Companies Covered in this Report:

- Silgan Holdings Inc.

- Albea S.A.

- Guala Closures S.p.A.

- Bericap GmbH & Co. KG

- AptarGroup, Inc.

- Amcor plc

- Crown Holdings, Inc.

- Closure Systems International, Inc.

- Plastivaloire SE

- Tecnocap S.p.A.

- Pano Cap (Canada) Limited

- Mold-Tek Packaging Limited

- RPC M&H Plastics Ltd.

- Oben Holding Group S.A.C.

- Universal Closures Ltd.

- Paccor Packaging GmbH

- Weener Plastics Group BV

- Freudenberg Home and Cleaning Solutions GmbH

- Comar, LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging On-The-Go Beverage Consumption

- 4.2.2 Rising Penetration Of Pet Bottled Dairy Drinks

- 4.2.3 Booming E-Commerce Demand For Tamper-Evident Packaging

- 4.2.4 Private-Label Expansion Among Regional Fmcg Players

- 4.2.5 Refill-And-Reuse Pilots By Large Beverage Brands

- 4.2.6 Adoption Of Tethered-Cap Eu Directive By Sa Exporters

- 4.3 Market Restraints

- 4.3.1 Shift Toward Stand-Up Pouches In Household Cleaners

- 4.3.2 Growing Anti-Plastic Regulations In Pacific Alliance

- 4.3.3 Price Volatility Of Virgin Polypropylene

- 4.3.4 Consumer Preference For Metal Crowns In Premium Beer

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 The Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VOLUME)

- 5.1 By Material

- 5.1.1 Polyethylene Terephthalate (PET)

- 5.1.2 Polypropylene (PP)

- 5.1.3 Low Density Polyethylene (LDPE)

- 5.1.4 High-Density Polyethylene (HDPE)

- 5.1.5 Other Materials

- 5.2 By End-user Industry

- 5.2.1 Beverage

- 5.2.2 Food

- 5.2.3 Pharmaceutical and Healthcare

- 5.2.4 Cosmetics and Toiletries

- 5.2.5 Household Chemicals

- 5.2.6 Other End-user Industries

- 5.3 By Cap Type

- 5.3.1 Screw Closures

- 5.3.2 Tethered Caps

- 5.3.3 Flip-top and Snap-on Caps

- 5.3.4 Child-resistant Closures

- 5.3.5 Luxury/Premium Decorative Closures

- 5.3.6 Dispensing Caps

- 5.4 By Manufacturing Technology

- 5.4.1 Injection Molding

- 5.4.2 Compression Molding

- 5.4.3 3-Piece and In-line Assembly

- 5.4.4 Digitally Printed Smart Closures

- 5.5 By Country

- 5.5.1 Brazil

- 5.5.2 Argentina

- 5.5.3 Colombia

- 5.5.4 Chile

- 5.5.5 Peru

- 5.5.6 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Silgan Holdings Inc.

- 6.4.2 Albea S.A.

- 6.4.3 Guala Closures S.p.A.

- 6.4.4 Bericap GmbH & Co. KG

- 6.4.5 AptarGroup, Inc.

- 6.4.6 Amcor plc

- 6.4.7 Crown Holdings, Inc.

- 6.4.8 Closure Systems International, Inc.

- 6.4.9 Plastivaloire SE

- 6.4.10 Tecnocap S.p.A.

- 6.4.11 Pano Cap (Canada) Limited

- 6.4.12 Mold-Tek Packaging Limited

- 6.4.13 RPC M&H Plastics Ltd.

- 6.4.14 Oben Holding Group S.A.C.

- 6.4.15 Universal Closures Ltd.

- 6.4.16 Paccor Packaging GmbH

- 6.4.17 Weener Plastics Group BV

- 6.4.18 Freudenberg Home and Cleaning Solutions GmbH

- 6.4.19 Comar, LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

塑膠蓋子與封口裝置市場:2026-2032年全球市場預測(按產品類型、材料、最終用途和分銷管道分類)

塑膠蓋子與封口裝置市場:2026-2032年全球市場預測(按產品類型、材料、最終用途和分銷管道分類) 美國塑膠瓶蓋和封蓋:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)

美國塑膠瓶蓋和封蓋:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年) 全球塑膠瓶蓋和封蓋市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球塑膠瓶蓋和封蓋市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球塑膠瓶蓋和封蓋市場報告

2026年全球塑膠瓶蓋和封蓋市場報告 塑膠瓶蓋和封蓋市場 - 全球產業規模、佔有率、趨勢、機會和預測(按產品類型、容器類型、原料、技術、最終用途行業、地區和競爭格局分類,2021-2031年)

塑膠瓶蓋和封蓋市場 - 全球產業規模、佔有率、趨勢、機會和預測(按產品類型、容器類型、原料、技術、最終用途行業、地區和競爭格局分類,2021-2031年) 70mm塑膠瓶蓋市場規模、佔有率和趨勢分析報告:按材料、應用、地區和細分市場預測,2026-2033年北美塑膠瓶蓋及封蓋市場:市佔率分析、產業趨勢、統計及成長預測(2026-2031)歐洲塑膠瓶蓋和封蓋:市場佔有率分析、行業趨勢、統計數據和成長預測(2026-2031 年)

70mm塑膠瓶蓋市場規模、佔有率和趨勢分析報告:按材料、應用、地區和細分市場預測,2026-2033年北美塑膠瓶蓋及封蓋市場:市佔率分析、產業趨勢、統計及成長預測(2026-2031)歐洲塑膠瓶蓋和封蓋:市場佔有率分析、行業趨勢、統計數據和成長預測(2026-2031 年) 塑膠瓶蓋和封蓋:全球市場佔有率和排名、總銷售額和需求預測(2025-2031 年)

塑膠瓶蓋和封蓋:全球市場佔有率和排名、總銷售額和需求預測(2025-2031 年) 2032年塑膠瓶蓋和封口市場預測:依產品類型、原料、製造流程、應用和地區分析

2032年塑膠瓶蓋和封口市場預測:依產品類型、原料、製造流程、應用和地區分析