|

市場調查報告書

商品編碼

2043914

美國建築外觀:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)US Facade - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

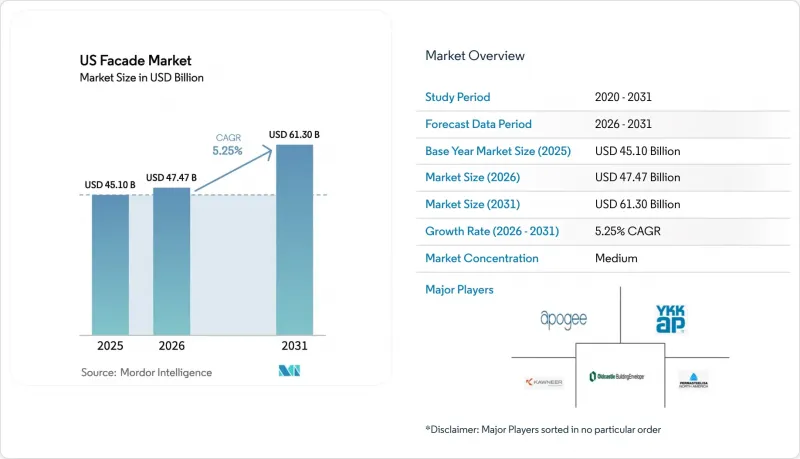

美國外牆市場預計到 2025 年將達到 451 億美元,到 2026 年將達到 474.7 億美元,到 2031 年將達到 613 億美元,2026 年至 2031 年的複合年成長率為 5.25%。

推動這項擴張的三大結構性變化是:疫情導致的非住宅建築項目在延誤後復甦;全國範圍內實施更為嚴格的2024年國際節能標準(IECC)和ASHRAE 90.1-2022建築圍護結構標準;以及對超大規模資料中心的大量投資,這些資料中心需要特殊的抗爆結構和高隔熱組裝結構。這些因素共同推動了對高性能幕牆、通風雨覆層和低碳鋁框架的需求成長。從區域來看,到2025年,南部地區將占美國幕牆市場的35.32%,但西部地區預計將成為成長最快的地區,到2031年複合年成長率將達到5.46%,這主要得益於加州的「清潔能源法案」(By-Clean Law)和抗震法規的推動。 2025 年,辦公大樓的現代化改造和資料中心園區的建設加速了對單元化系統的訂單,這些系統可以減少 25-30% 的現場勞動力,其中商業終端用戶佔需求的 67.65%。

美國帷幕牆市場趨勢與洞察

非住宅建築的復甦正在推動對先進幕牆系統的需求。

2025年全年設計訂單維持強勁,美國建築師協會(AIA)指數平均為51.2。這表明,在陽光地帶的主要都市區,辦公大樓和綜合用途項目正持續湧現。開發商傾向於採用模組化幕牆結構,這種結構可將工期縮短高達30%,從而在熟練勞動力短缺的情況下降人事費用。目前,LEED鉑金或WELL認證已成為A+級建築的常見認證標準,要求外觀U值低於0.30,可見光透射率達40%或以上。位於德克薩斯州的先鋒自然資源公司總部大樓就是一個典型的例子,該大樓佔地110萬平方英尺,外牆採用3000個單元的高性能Viracon玻璃幕牆,可見光透射率(VLT)達到44%,太陽能熱增益係數(SHGC)為0.26。這些項目共同推動了隔熱框架、低輻射隔熱玻璃和堅固錨固系統的訂單成長。隨著開發商競相應對日益嚴格的能源標準,以確保其資產的未來潛力,預計這一趨勢將持續到2027年。

IECC 和 ASHRAE 90.1 對建築圍護結構標準的收緊,促進了高性能帷幕牆的採用。

2024 年國際節能規範 (IECC) 將寒冷地區幕牆的 U 值上限收緊至 0.36–0.40,而 ASHRAE 90.1-2022 標準則將允許的空氣洩漏量減少了 25%。滿足這些要求需要使用三層隔熱玻璃、連續氣密層和先進的密封墊,這將使組裝成本增加 12%–15%。然而,加州、紐約州和馬薩諸塞州的州政府計畫為超出基準值20% 的幕牆提供每平方英尺 8–12 美元的補貼,從而將投資回收期縮短至不到九年。 Oldcastle Building Envelope 公司的「3000 XT 系列」店面帷幕牆的 U 值達到了 0.20,遠低於基準值,這表明製造商正在將重心轉向高階高性能產品。到 2026 年初,已有 38 個州採用了 2024 年版的 IECC,建立了全國統一標準,加速了先進圍護結構技術的普及。

鋁材和玻璃價格的波動推高了帷幕牆系統的專案成本。

2025年初,中國冶煉廠的產能限制導致鋁現貨價格較去年同期上漲30.5%,美國對進口金屬徵收25%的關稅更是雪上加霜。天然氣價格飆升導致浮法玻璃製造商面臨15%的成本上漲,進而推高了超大型雙層玻璃(IGU)的合約價格。幕牆承包商的利潤率下降了200-300個基點,迫使他們重新談判固定價格契約,並推遲了一些中層辦公大樓和多用戶住宅的開工。 YKK AP America透過與低碳鋁冶煉廠簽訂長期契約,滿足其80%的需求,從而降低了風險並穩定了原料價格,但這限制了其利用市場暫時低迷獲利的能力。像Apogee這樣擁有自有玻璃製造和表面處理工程的垂直整合型巨頭,比區域性獨立公司更能抵禦價格波動,從而擴大了競爭差距。

細分市場分析

預計到2025年,透氣雨幕系統將佔據美國外牆市場50.48%的佔有率,並將在2031年之前以5.01%的複合年成長率成長,因為沿海氣候地區的建築規範越來越重視濕度管理。與阻隔牆相比,這種設計透過引入0.75至1.5英吋的空腔,使水蒸氣能夠排放,從而將冷凝風險降低高達50%。在IECC 4A至5A氣候區(包括東海岸)中,這種方法的應用正在加速,因為這些地區風雨交加,使得傳統的密封外牆難以施工。如果房屋安裝了經認證的透氣空腔,保險公司將提供5%至10%的保費折扣,這進一步增強了屋主採用這種設計的經濟動力。

在乾旱的西南部地區,低濕度最大限度地降低了故障率,成本效益優先於性能,因此非通風系統仍然佔據主導地位。像金斯潘的「QuadCore」面板這樣的混合產品,將連續隔熱材料整合在排水腔內,模糊了不同類型之間的界限,使設計師能夠同時實現節能和防潮目標。隨著投資者對具有韌性和低碳性能的資產的需求日益成長,預計除最乾旱的地區外,通風設計將成為所有地區的標準配置,從而推動美國外牆市場的穩步成長。

到2025年,帷幕牆憑藉其在高層建築中的穩固地位,將佔據美國外觀市場52.40%的佔有率。然而,預計到2031年,雨幕覆層將成為成長最快的外牆材料,複合年成長率將達到5.08%。這得益於維修工程傾向於採用輕質覆層以最大限度減少對租戶的影響。透過將結構層與防水層分離,可以減少60-70%的熱橋效應,從而滿足IECC 2024對U值性能的嚴格要求。

像加州蒙特貝洛門戶大樓這樣的高層辦公大樓仍然依賴客製化幕牆來實現全景玻璃幕牆。然而,對於老舊的B級物業而言,雨幕系統正逐漸成為一種可行的維修方案,像Dextall這樣的本地公司提供的預製套件可以減少30%的現場施工量。未來,將可開啟通風口和排水腔整合到幕牆框架中的混合系統或許能夠彌補這一差距,但就目前而言,雨幕系統在美國幕牆市場仍佔據著結構性的成長優勢。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 非住宅建築的復甦增加了對先進帷幕牆系統的需求。

- IECC 和 ASHRAE 90.1 對建築圍護結構標準的收緊,促進了高性能帷幕牆的採用。

- 商業建築老化引發了大規模的外觀維修和現代化改造項目。

- 對高性能玻璃日益成長的需求正在提高建築物的能源效率。

- 超大規模資料中心的擴張導致對專用外觀結構的投資增加。

- 聯邦緊急事務管理局的抗災津貼正在加速建造抗颶風和抗災外牆。

- 市場限制因素

- 鋁材和玻璃價格的波動增加了帷幕牆系統的專案成本。

- 合格的外牆承包商短缺導致工程實施延誤,人事費用上升。

- NFPA 285 中關於易燃覆材的保險除外條款限制了材料的選擇。

- 城市層級的嵌入式碳排放法規,例如「購買清潔能源產品」政策,正在增加合規成本。

- 價值鏈/供應鏈分析

- 監理情勢

- 技術展望

- 價格分析

- 消費行為分析

- 永續發展趨勢

- 波特五力模型

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模及成長預測(價值單位:美元)

- 按類型

- 通風

- 不通風的

- 其他

- 帷幕牆系統類型

- 雨幕式覆層

- 帷幕牆系統

- 其他

- 材料

- 玻璃

- 金屬

- 塑膠和纖維

- 石材

- 其他

- 透過安裝

- 新建工程

- 維修和整修

- 最終用戶

- 商業的

- 住宅

- 其他

- 按地區

- 東北

- 中西部

- 南部

- 西

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 公司簡介

- Apogee Enterprises Inc.

- Oldcastle BuildingEnvelope

- YKK AP America

- Kawneer North America

- Permasteelisa North America

- Enclos Corp

- Walters & Wolf

- Benson Industries

- EFCO Corporation

- CENTRIA

- Kingspan Insulated Panels US

- Sto Corp.

- Clark Pacific

- CR Laurence(US Aluminum)

- National Enclosure Company

- GlassFab Tempering Services

- Technical Glass Products

- PPG Architectural Coatings

- Guardian Glass North America

- Schuco USA

第7章 市場機會與未來展望

The US Facade Market size is projected to be USD 45.10 billion in 2025, USD 47.47 billion in 2026, and reach USD 61.30 billion by 2031, growing at a CAGR of 5.25% from 2026 to 2031.

Three structural shifts propel this expansion, including the rebound in non-residential construction after pandemic-era delays, the nationwide roll-out of stricter 2024 International Energy Conservation Code (IECC) and ASHRAE 90.1-2022 building-envelope standards, and a wave of hyperscale data-center investments requiring specialized blast-resistant and thermally efficient assemblies.Together, these forces boost demand for high-performance curtain walls, ventilated rainscreen cladding, and low-carbon aluminum framing. At the regional level, the South accounted for 35.32% of the US facade market in 2025, while the West is projected to be the fastest-growing region at 5.46% CAGR through 2031, aided by California's Buy Clean Act and seismic mandates. Commercial end-users dominated with 67.65% of demand in 2025 as office-tower modernizations and data-center campuses accelerated orders for unitized systems that cut on-site labor by 25-30%.

US Facade Market Trends and Insights

Rebound in Non-Residential Construction Increases Demand for Advanced Facade Systems

Design billings strengthened throughout 2025, with the AIA Index averaging 51.2, foreshadowing a sustained pipeline of office towers and mixed-use projects across Sunbelt metros. Developers favor unitized curtain-wall assemblies that cut installation time by up to 30%, helping contain labor costs amid skilled-trade shortages. Class A+ buildings now routinely target LEED Platinum or WELL certification, which encourages facade U-factors below 0.30 and visible-light transmittance above 40%. A marquee example is the 1.1 million-sq-ft Pioneer Natural Resources headquarters in Irving, Texas, clad with 3,000 high-performance curtain-wall units featuring Viracon glass that delivers 44% VLT and 0.26 SHGC. Taken together, these projects amplify orders for thermally broken framing, low-e insulated glass, and robust anchorage systems. The trend is expected to continue through 2027 as developers race to future-proof assets against tightening energy benchmarks.

Stricter IECC and ASHRAE 90.1 Building-Envelope Codes Drive High-Performance Facade Adoption

The 2024 IECC tightened curtain-wall U-factor limits to 0.36-0.40 in colder zones, while ASHRAE 90.1-2022 cut allowable air leakage by 25%. Compliance now demands triple-glazed IGUs, continuous air barriers, and advanced gaskets that raise assembly costs by 12-15%. Yet state utility programs in California, New York, and Massachusetts rebate USD 8-12 per sq ft for facades that outperform code by 20%, shrinking payback periods to less than nine years. Oldcastle BuildingEnvelope's Series 3000 XT storefront achieves U-factors of 0.20, well below code, highlighting how fabricators are repositioning toward premium, high-performance products. As 38 states had adopted the 2024 IECC by early 2026, a uniform national baseline now accelerates widespread adoption of advanced envelope technologies.

Volatility in Aluminum and Glass Prices Raises Facade System Project Costs

Aluminum spot prices climbed 30.5% year-over-year in early 2025 due to curtailments in Chinese smelting, while a 25% U.S. tariff on imported metals added further strain. Float-glass producers faced 15% cost hikes as natural-gas prices spiked, sending contract prices for oversized IGUs sharply higher. Facade contractors lost 200-300 basis points of margin and renegotiated fixed-price deals, delaying some mid-rise office and multifamily starts. YKK AP America mitigated risk by signing long-term deals with low-carbon aluminum smelters for 80% of its demand, stabilizing input pricing yet limiting its ability to exploit short-lived market dips. Vertically integrated majors such as Apogee, with in-house glass and finishing, weathered volatility better than regional independents, widening competitive gaps.

Other drivers and restraints analyzed in the detailed report include:

- Aging Commercial Building Stock Triggers Large-Scale Facade Retrofit and Modernization Projects

- Rising Demand for High-Performance Glazing Improves Building Energy-Efficiency Outcomes

- Shortage of Certified Facade Installers Delays Project Execution and Increases Labor Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Ventilated rainscreen assemblies captured 50.48% of the US facade market share in 2025 and are projected to expand at a 5.01% CAGR through 2031 as code bodies prioritize moisture management in coastal climates. The design introduces a 0.75-1.5-inch cavity that drains vapor, cutting condensation risk by up to 50% relative to barrier walls. Adoption accelerates in IECC Climate Zones 4A-5A, covering the Eastern seaboard, where wind-driven rain challenges traditional sealed facades. Insurance carriers offer 5-10% premium discounts when ventilated cavities are documented, reinforcing financial motivation for owners.

Non-ventilated systems remain dominant in the arid Southwest, where low humidity keeps failure rates minimal, and cost efficiency trumps performance. Hybrid products, such as Kingspan's QuadCore panels that integrate continuous insulation inside a drained cavity, blur the lines between categories and allow designers to meet both energy and moisture objectives. As investors demand resilient and low-carbon assets, ventilated designs are expected to become the baseline specification in all but the driest regions, ensuring their steady ascent within the broader US facade market.

Curtain walls accounted for 52.40% of the US facade market size in 2025, owing to their stronghold in high-rise construction. However, rainscreen cladding is projected to grow fastest at 5.08% CAGR to 2031, riding a wave of retrofit projects that favor lightweight over-cladding with minimal tenant disruption. Decoupling of structural and weatherproofing layers reduces thermal bridging by 60-70%, meeting stringent IECC 2024 targets for U-factor performance.

High-rise office towers, such as Montebello Gateway in California, still depend on custom curtain walls to achieve panoramic glass facades. Yet for aging Class B stock, rainscreens offer a practical upgrade path, and regional players like Dextall provide prefabricated kits that slash on-site labor by 30%. Looking ahead, hybrid systems that merge operable vents and drainage cavities into curtain-wall frames could neutralize the competitive gap, but for now, rainscreens enjoy a structural growth advantage in the US facade market.

The US Facade Market Report is Segmented by Type (Ventilated, Non-Ventilated, and Others), by Facade System Type (Rainscreen Cladding, Curtain-Wall Systems, and Others), by Material (Glass, Metal, Plastics and Fibers, and More), by Installation (New Construction, Renovation & Retrofit), by End-User (Commercial, and More), and by Region (Northeast, Midwest, South, and West). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Apogee Enterprises Inc.

- Oldcastle BuildingEnvelope

- YKK AP America

- Kawneer North America

- Permasteelisa North America

- Enclos Corp

- Walters & Wolf

- Benson Industries

- EFCO Corporation

- CENTRIA

- Kingspan Insulated Panels US

- Sto Corp.

- Clark Pacific

- C.R. Laurence (U.S. Aluminum)

- National Enclosure Company

- GlassFab Tempering Services

- Technical Glass Products

- PPG Architectural Coatings

- Guardian Glass North America

- Schuco USA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rebound in non-residential construction increases demand for advanced facade systems

- 4.2.2 Stricter IECC and ASHRAE 90.1 building envelope codes drive high-performance facade adoption

- 4.2.3 Aging commercial building stock triggers large-scale facade retrofit and modernization projects

- 4.2.4 Rising demand for high-performance glazing improves building energy efficiency outcomes

- 4.2.5 Expansion of hyperscale data centers increases investment in specialized facade structures

- 4.2.6 FEMA resilience grants encourage installation of hurricane-rated and disaster-resistant facades

- 4.3 Market Restraints

- 4.3.1 Volatility in aluminum and glass prices raises facade system project costs

- 4.3.2 Shortage of certified facade installers delays project execution and increases labor costs

- 4.3.3 Insurance exclusions for combustible cladding under NFPA 285 limit material choices

- 4.3.4 City-level embodied carbon regulations such as Buy Clean policies increase compliance costs

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Pricing Analysis

- 4.8 Consumer Behavior Analysis

- 4.9 Sustainability Trends

- 4.10 Porter's Five Forces

- 4.10.1 Bargaining Power of Suppliers

- 4.10.2 Bargaining Power of Consumers

- 4.10.3 Threat of New Entrants

- 4.10.4 Threat of Substitutes

- 4.10.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value in USD)

- 5.1 By Type

- 5.1.1 Ventilated

- 5.1.2 Non-Ventilated

- 5.1.3 Others

- 5.2 By Facade System Type

- 5.2.1 Rainscreen Cladding

- 5.2.2 Curtain-Wall Systems

- 5.2.3 Others

- 5.3 By Material

- 5.3.1 Glass

- 5.3.2 Metal

- 5.3.3 Plastic & Fibres

- 5.3.4 Stone

- 5.3.5 Others

- 5.4 By Installation

- 5.4.1 New Construction

- 5.4.2 Renovation & Retrofit

- 5.5 By End-User

- 5.5.1 Commercial

- 5.5.2 Residential

- 5.5.3 Others

- 5.6 By Region

- 5.6.1 Northeast

- 5.6.2 Midwest

- 5.6.3 South

- 5.6.4 West

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, Recent Developments)

- 6.3.1 Apogee Enterprises Inc.

- 6.3.2 Oldcastle BuildingEnvelope

- 6.3.3 YKK AP America

- 6.3.4 Kawneer North America

- 6.3.5 Permasteelisa North America

- 6.3.6 Enclos Corp

- 6.3.7 Walters & Wolf

- 6.3.8 Benson Industries

- 6.3.9 EFCO Corporation

- 6.3.10 CENTRIA

- 6.3.11 Kingspan Insulated Panels US

- 6.3.12 Sto Corp.

- 6.3.13 Clark Pacific

- 6.3.14 C.R. Laurence (U.S. Aluminum)

- 6.3.15 National Enclosure Company

- 6.3.16 GlassFab Tempering Services

- 6.3.17 Technical Glass Products

- 6.3.18 PPG Architectural Coatings

- 6.3.19 Guardian Glass North America

- 6.3.20 Schuco USA

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment

帷幕牆系統市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、材料、應用、地區和競爭格局分類,2021-2031年

帷幕牆系統市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、材料、應用、地區和競爭格局分類,2021-2031年 帷幕牆市場:按產品類型、材料、最終用途和地區分類,2026-2034 年

帷幕牆市場:按產品類型、材料、最終用途和地區分類,2026-2034 年 2026年全球帷幕牆錨固系統市場報告

2026年全球帷幕牆錨固系統市場報告 建築幕牆:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)2026年全球建築幕牆系統市場報告歐洲建築幕牆:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)帷幕牆市場-全球產業規模、佔有率、趨勢、機會和預測,依產品、帷幕牆類型、建築類型、地區和競爭格局分類,2021-2031年預測日本建築幕牆市場規模、佔有率、趨勢及預測(按產品類型、材料、最終用途和地區分類,2026-2034年)

建築幕牆:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)2026年全球建築幕牆系統市場報告歐洲建築幕牆:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)帷幕牆市場-全球產業規模、佔有率、趨勢、機會和預測,依產品、帷幕牆類型、建築類型、地區和競爭格局分類,2021-2031年預測日本建築幕牆市場規模、佔有率、趨勢及預測(按產品類型、材料、最終用途和地區分類,2026-2034年) 自癒式帷幕牆材料市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)

自癒式帷幕牆材料市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年) 帷幕建築幕牆系統市場按材料類型、系統類型、應用、最終用途和功能分類-2025-2032年全球預測

帷幕建築幕牆系統市場按材料類型、系統類型、應用、最終用途和功能分類-2025-2032年全球預測