|

市場調查報告書

商品編碼

1937409

建築幕牆:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Facade - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

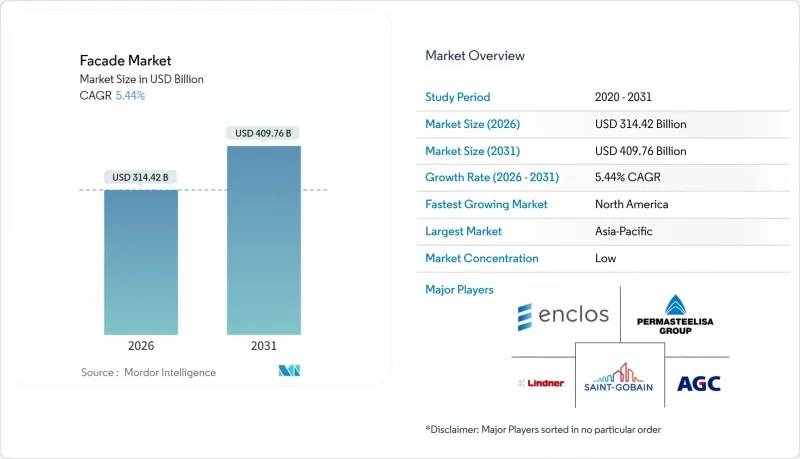

2025年,建築幕牆市場價值為2,982億美元,預計到2031年將達到4,097.6億美元,而2026年為3,144.2億美元。

預計在預測期(2026-2031 年)內,複合年成長率將達到 5.44%。

這一成長軌跡反映了強勁的需求,而這種需求的驅動力來自於建築一體化太陽能光電系統、智慧外圍結構控制系統和單元式帷幕牆的廣泛應用。亞太地區將在2024年引領營收成長,其中中東和非洲地區的成長速度最快。隨著高層建築開發商將熱性能放在首位,通風系統將繼續保持其設計優勢;即使在更嚴格的能源標準下住宅維修加速進行,商業建築仍將是重要的收入來源。

聖戈班在2024年的一系列收購後,產業整合的壓力增加,但整體供應結構仍分散,區域性專業公司和全球集團並存。鋁價波動和日益嚴格的消防法規持續擠壓計劃利潤率,但符合規範的建築幕牆可享受保險折扣,以及建築整合太陽能(BIPV)成本下降,維持了投資勢頭。

全球建築幕牆市場趨勢與洞察

亞太和中東地區的高層建築熱潮

中國、印度和海灣地區高層建築的激增,對建築性能提出了更高的要求,使得建築幕牆不再只是裝飾性的外立面,而是核心基礎設施組成部分。預計到2023年,全球將有超過176棟200公尺以上的摩天大樓竣工,而未來的建設計畫也十分強勁,這主要得益於沙烏地阿拉伯的穆卡布大廈和中國的黃金金融117大廈等大型企劃的推動。模組化異地組裝技術正在縮短關鍵路徑時間,例如,一座26層高的塔樓僅用五天就建成。因此,開發商正在尋求供應商提供工廠預製的多功能建築幕牆,將結構支撐、能源產出和數位監控等功能整合到單一的圍護結構解決方案中。

更嚴格的節能建築標準

世界各國政府正將脫碳目標轉化為嚴格的建築外圍護結構法規,並要求建築商實現淨零排放。日本2025年的法規強制要求中型新建建築安裝太陽能光電發電系統,而美國暖氣、冷氣與空調工程師協會(ASHRAE)90.1-2022標準則將美國的能源效率標準提高了9.8%。加州第24號法規和紐約市的地方法規鼓勵在資本週期內對建築幕牆維修,並對性能缺陷處以罰款。通風層、動態遮陽和低U值玻璃的補貼計畫正在推動對先進建築外圍護結構的需求,尤其是在消防安全和能源效率法規重疊的地區。

鋁和玻璃價格波動

預計到2025年初,鋁價將達到每噸2,763美元,這將導致成本上漲10%,並擠壓採用固定競標合約計劃的利潤空間。地緣政治緊張局勢和高能源價格限制了冶煉廠的產量,而汽車和可再生能源產業的需求則加劇了供應緊張。流動資金有限的小規模建築幕牆承包商難以對沖風險,這加速了產業向擁有商品風險管理計畫的垂直整合供應商的整合。

細分市場分析

到2025年,通風建築幕牆將佔市場收入的51.65%,透過自然對流將空調負載降低高達25%,從而為滿足建築規範要求提供了清晰的途徑。隨著連續空氣層和防雨功能在炎熱潮濕地區的高層計劃中變得日益重要,預計到2031年,通風建築幕牆設計的市場規模將以5.48%的複合年成長率成長。新興的物聯網風門可即時調整空腔內的氣流,進而提高能源效率並延長帷幕牆的使用壽命。雖然在氣候溫暖的市場中,為了降低建造成本,仍會採用非通風帷幕牆,但更嚴格的碳排放法規正推動兼顧成本和性能的混合空腔建築幕牆進入經濟型市場。

對於低層住宅和倉庫項目而言,非通風結構仍然很受歡迎,因為在這些項目中,建築表現力比隔熱性能更為重要。製造商提供紋理豐富的覆層、再生複合複合材料和簡化的緊固系統,顯著縮短了此類專案的安裝週期。混合建築幕牆正被應用於多功能塔樓,將陽光照射面上的通風結構與陰涼面上的經濟型覆層結合。這種選擇性方法既能最佳化計劃整體預算,又能滿足建築設計意圖。

到2025年,帷幕牆將佔總需求的43.58%,其中單元式帷幕牆產品將以5.52%的複合年成長率成長,這主要得益於開發商對施工進度確定性的追求。由於組合式框架面臨熟練勞動力短缺的問題,工廠預塗漆建築幕牆目前在高層建築計劃佔據主導地位。帷幕牆的防火性能以及在製造過程中易於整合建築整合太陽能(BIPV)組件,進一步鞏固了其市場佔有率。物流中心和資料中心越來越重視可靠的防風雨性能而非極致的透明度,促使雨幕式帷幕牆系統日益普及。

先進的幕牆組件包括電致變色玻璃、整合遮陽鰭片以及可連接建築管理系統的感測器套件。在發生多起備受矚目的外牆火災後,保險公司也更傾向於選擇經過驗證的帷幕牆結構,因此其保費低於實驗性替代方案。儘管雨幕供應商已採用礦物纖維芯材和不燃百葉片等技術進行改良以保持競爭力,但幕牆仍然是豪華高層建築性能的標竿。

區域分析

亞太地區將在建築幕牆市場中主導,無論從價值或銷售來看,預計到2025年將佔全球銷售額的39.58%。中國和印度的大型企劃,以及日本針對中型建築的光伏一體化(BIPV)法規,使得工廠使用率接近滿載運轉。國內玻璃和鋁材生產商已穩定了供應鏈,但區域性城市仍面臨熟練安裝人員短缺的問題。開發商正從歐洲進口專用錨固件和智慧嵌裝玻璃,以滿足高階規格要求。

預計到2031年,中東和非洲地區的建築業將以6.18%的複合年成長率成長,這主要得益於沙烏地阿拉伯的NEOM、The Line和Mukab項目,以及杜拜和杜哈的高層建築開發項目。嚴酷的沙漠氣候促使人們採用透氣建築幕牆和電致變色玻璃來降低冷氣負荷。當地製造商正透過從歐洲幕牆專家那裡獲得技術許可來擴大規模,而各國政府也在鼓勵在地採購以支持經濟多元化。

在歐洲,維修、日益嚴格的消防安全標準以及製造業的碳排放管理正在推動建築幕牆需求。德國在建築一體化光伏(BIPV)幕牆創新方面處於領先地位,而法國則引入了能源性能證書(EPC)以強調建築幕牆的能源效率。在英國,格倫費爾大樓火災後收緊的法規增加了對符合A2-s1-d0標準的材料的需求,並逐步淘汰不符合標準的覆層材料。為了應對嚴寒的冬季,北歐國家優先考慮隔熱框架和三層玻璃窗,這反映了不同氣候條件下的多樣化需求。

在北美,重點在於老舊辦公大樓和大學校園的維修。加州、紐約州和馬薩諸塞州日益嚴格的能源法規推動了智慧玻璃和蒸氣控制系統的改進。勞動力短缺促使承包商轉向單元式系統,從而推動了國內投資,例如YKK AP在喬治亞投資1.25億美元擴建工廠。拉丁美洲市場雖然規模較小,但在沿海城市正穩定成長,因為抗颶風外牆可以保護房地產資產。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 亞太和中東地區的高層建築熱潮

- 更嚴格的節能建築標準

- 快速過渡到模組化帷幕牆系統

- 建築幕牆整合光伏(BIPV)的激增

- 防火建築幕牆可享保險折扣

- 人工智慧建築幕牆維護和檢測的採用現狀

- 市場限制

- 鋁和玻璃價格波動

- 複雜的跨轄區消防安全法規

- 保險公司檢驗的外部系統列入黑名單。

- 合格的建築幕牆施工人員短缺

- 建築幕牆產業中使用的不同結構概述

- 定價分析

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 消費行為分析(建築商、建築師、開發商、私人買家、設施和物業經理/業主)

- 永續發展趨勢

第5章 市場區隔

- 按類型

- 通風

- 不通風的

- 其他

- 依建築幕牆系統類型

- 防雨外牆材料

- 帷幕牆系統

- 其他

- 材料

- 玻璃

- 金屬

- 塑膠和纖維

- 石材

- 其他

- 透過安裝

- 新房產

- 維修和維修工程

- 最終用戶

- 商業的

- 住宅

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 智利

- 其他南美洲

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 亞太其他地區

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 奈及利亞

- 其他中東和非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Saint-Gobain SA

- AGC Glass Europe

- Enclos Corp.

- Permasteelisa SpA

- Kawneer Company

- Kingspan Group

- Lindner Group

- Norsk Hydro ASA

- Schuco International

- YKK AP

- Reynaers Aluminium

- AluK Group

- Jangho Group

- Rockpanel Group

- Sto SE & Co. KGaA

- Trimo doo

- Gutmann AG

- AFS International

- Aluplex

- SRG Global Ltd.*

第7章 市場機會與未來展望

The Facade Market was valued at USD 298.20 billion in 2025 and estimated to grow from USD 314.42 billion in 2026 to reach USD 409.76 billion by 2031, at a CAGR of 5.44% during the forecast period (2026-2031).

This trajectory reflects resilient demand anchored in building-integrated photovoltaics, smart envelope controls, and unitised curtain wall adoption. Asia-Pacific led revenue in 2024, while the Middle East & Africa provided the quickest incremental growth. Ventilated systems preserved design primacy because high-rise developers value thermal performance, and commercial buildings remained the chief revenue stream even as residential retrofits accelerated under tighter energy codes.

Consolidation pressures rose after Saint-Gobain's 2024 acquisition series, yet overall supply stays fragmented as regional specialists coexist with global conglomerates. Volatile aluminum prices and stricter fire-safety rules continue to squeeze project margins, but insurance discounts for compliant facades and falling BIPV costs sustain investment momentum.

Global Facade Market Trends and Insights

High-rise construction boom in Asia-Pacific and Middle East

Soaring skylines in China, India, and Gulf states seed complex performance demands that make facades core infrastructure components rather than decorative skins. More than 176 buildings surpassing 200 m were completed worldwide in 2023, and the pipeline remains robust through mega-projects such as Saudi Arabia's Mukaab and resumed work on China's Goldin Finance 117. Modular off-site assembly shortens critical-path schedules, evidenced by a 26-story tower completed in just five days. Developers consequently press suppliers for factory-finished, multi-functional facades that blend structural support, energy generation, and digital monitoring into a single envelope solution.

Stricter energy-efficiency building codes

Governments translate decarbonization goals into tougher envelope rules, forcing builders to target net-zero operations. Japan's 2025 regulations require photovoltaics on new mid-size structures, and ASHRAE 90.1-2022 raises U.S. energy-savings baselines by 9.8%. California's Title 24 and New York City Local Laws levy penalties for poor performance, spurring facade retrofits during capital cycles. Credits for ventilated cavities, dynamic shading, and low-U-value glass elevate advanced envelope demand, particularly where fire-safety and energy-efficiency mandates overlap.

Volatile aluminum and glass prices

Aluminum is projected to hit USD 2,763 / t in early 2025, producing 10% cost inflation that squeezes margins on projects locked into fixed-bid contracts. Geopolitical tensions and energy-price spikes limit smelter output, while demand from automotive and renewables tightens supply. Smaller facade contractors-often operating on thin working-capital lines-struggle to hedge exposure, hastening consolidation toward vertically integrated suppliers with commodity-risk programs.

Other drivers and restraints analyzed in the detailed report include:

- Rapid shift to unitised curtain-wall systems

- Surge in facade-integrated photovoltaics

- Complex multi-jurisdictional fire-safety rules

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Ventilated assemblies contributed 51.65% of 2025 revenue, reflecting clearer paths to code compliance where natural convection reduces HVAC loads by up to 25%. The facades market size for ventilated designs is projected to rise at a 5.48% CAGR through 2031 as high-rise projects in hot-humid belts value continuous air gaps and rain-screen performance. Emerging IoT-enabled dampers now regulate cavity airflow in real time, enhancing energy efficiency and extending envelope life. Markets with milder climates still specify non-ventilated facades to save capital, though tightening carbon rules push even budget segments toward hybrid cavities that balance cost and performance.

Non-ventilated configurations remain popular for low-rise housing and warehouse schemes where architectural expression supersedes thermal stringency. Manufacturers court this segment with textured cladding, recycled composites, and simplified anchorage that slashes installation cycles. Hybrid facades appear on mixed-use towers, marrying ventilated orientations on sun-exposed elevations with cost-savvy layers on shaded sides. This selective approach satisfies architectural intent while optimizing total project budgets.

Curtain walls held 43.58% of 2025 demand, and unitised offerings are adding 5.52% CAGR as developers chase schedule certainty. Because stick-built framing struggles with shrinking trade labor pools, factory-glazed panels now dominate skyline projects. The facades market share for curtain walls is reinforced by demonstrated fire performance and the ease of embedding BIPV modules during fabrication. Rainscreen cladding gains ground in logistics hubs and data centers that prize robust weather shielding over maximum transparency.

Advanced curtain-wall packages include electrochromic glass, integrated shading fins, and sensor suites that feed building-management systems. Insurance underwriters also favor proven curtain-wall rigs after high-profile cladding fires, translating into lower premiums versus experimental alternatives. Rainscreen suppliers respond with mineral-fiber cores and non-combustible lamellas to stay competitive, but curtain walls still set the performance benchmark for premium towers.

The Facades Market Report is Segmented by Type (Ventilated, Non-Ventilated, Others), Facade System Type (Rainscreen Cladding, Curtain Wall Systems, Others), Material (Glass, Metal, Plastic and Fibres, Stones, Others), Installation (New Construction, Renovation & Retrofit), End-User (Commercial, Residential, Others), and Geography (North America, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

In 2025, Asia-Pacific accounted for 39.58% of global revenue, leading the facades market by value and volume. Mega-projects in China and India, along with Japan's BIPV regulations for medium-sized buildings, keep factories near full capacity. Domestic glass and aluminum producers stabilize supply chains, though skilled installer shortages persist in tier-two cities. Developers import proprietary anchors and smart glazing from Europe to meet premium specifications.

The Middle East and Africa are projected to grow at a 6.18% CAGR through 2031, driven by Saudi Arabia's NEOM, The Line, and Mukaab projects, alongside high-rise developments in Dubai and Doha. Extreme desert climates drive the adoption of ventilated facades and electrochromic glass to reduce cooling loads. Local fabricators expand through technology licenses from European curtain-wall specialists, while governments incentivize local content to support economic diversification.

In Europe, facade demand is driven by renovation, fire-safety upgrades, and embodied-carbon controls. Germany leads in BIPV curtain wall innovation, while France implements energy-performance certificates emphasizing facade efficiency. The U.K. enforces stricter post-Grenfell regulations, increasing demand for compliant A2-s1-d0 materials and phasing out non-compliant cladding. Nordic countries prioritize triple-glazed, thermally broken frames to address harsh winters, reflecting diverse climatic needs.

North America focuses on upgrading aging office buildings and university campuses. Stricter energy codes in California, New York, and Massachusetts encourage smart glazing and improved vapor control. Labor shortages push contractors toward unitized systems, driving domestic investments such as YKK AP's USD 125 million factory expansion in Georgia. Latin American markets remain smaller but show steady growth in coastal cities, where hurricane-rated facades protect real estate assets.

- Saint-Gobain S.A.

- AGC Glass Europe

- Enclos Corp.

- Permasteelisa S.p.A

- Kawneer Company

- Kingspan Group

- Lindner Group

- Norsk Hydro ASA

- Schuco International

- YKK AP

- Reynaers Aluminium

- AluK Group

- Jangho Group

- Rockpanel Group

- Sto SE & Co. KGaA

- Trimo d.o.o.

- Gutmann AG

- AFS International

- Aluplex

- SRG Global Ltd.*

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 High-rise construction boom in APAC & Middle East

- 4.2.2 Stricter energy-efficiency building codes

- 4.2.3 Rapid shift to unitised curtain-wall systems

- 4.2.4 Surge in facade-integrated photovoltaics (BIPV)

- 4.2.5 Insurance premium discounts for fire-safe facades

- 4.2.6 AI-driven facade maintenance & inspection adoption

- 4.3 Market Restraints

- 4.3.1 Volatile aluminium & glass prices

- 4.3.2 Complex multi-jurisdictional fire-safety rules

- 4.3.3 Insurers black-listing untested cladding systems

- 4.3.4 Shortage of certified facade installers

- 4.4 Brief on Different Structures Used in the Facades Industry

- 4.5 Pricing Analysis

- 4.6 Value / Supply-Chain Analysis

- 4.7 Regulatory Landscape

- 4.8 Technological Outlook

- 4.9 Industry Attractiveness - Porter's Five Force Analysis

- 4.9.1 Bargaining Power of Suppliers

- 4.9.2 Bargaining Power of Consumers

- 4.9.3 Threat of New Entrants

- 4.9.4 Threat of Substitutes

- 4.9.5 Intensity of Competitive Rivalry

- 4.10 Consumer Behavior Analysis (Contractors, Architects, Developers, Individual Buyers, Facility & Property Managers/Building Owners)

- 4.11 Sustainability Trends

5 MARKET SEGMENTATION

- 5.1 By Type

- 5.1.1 Ventilated

- 5.1.2 Non-Ventilated

- 5.1.3 Others

- 5.2 By Facade System Type

- 5.2.1 Rainscreen Cladding

- 5.2.2 Curtain Wall Systems

- 5.2.3 Others

- 5.3 By Material

- 5.3.1 Glass

- 5.3.2 Metal

- 5.3.3 Plastic and Fibres

- 5.3.4 Stones

- 5.3.5 Others

- 5.4 By Installation

- 5.4.1 New Construction

- 5.4.2 Renovation & Retrofit

- 5.5 By End-User

- 5.5.1 Commercial

- 5.5.2 Residential

- 5.5.3 Others

- 5.6 By Region

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Chile

- 5.6.2.4 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East & Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 South Africa

- 5.6.5.4 Nigeria

- 5.6.5.5 Rest of Middle East & Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 Saint-Gobain S.A.

- 6.4.2 AGC Glass Europe

- 6.4.3 Enclos Corp.

- 6.4.4 Permasteelisa S.p.A

- 6.4.5 Kawneer Company

- 6.4.6 Kingspan Group

- 6.4.7 Lindner Group

- 6.4.8 Norsk Hydro ASA

- 6.4.9 Schuco International

- 6.4.10 YKK AP

- 6.4.11 Reynaers Aluminium

- 6.4.12 AluK Group

- 6.4.13 Jangho Group

- 6.4.14 Rockpanel Group

- 6.4.15 Sto SE & Co. KGaA

- 6.4.16 Trimo d.o.o.

- 6.4.17 Gutmann AG

- 6.4.18 AFS International

- 6.4.19 Aluplex

- 6.4.20 SRG Global Ltd.*

7 MARKET OPPORTUNITIES & FUTURE OUTLOOK

- 7.1 White-Space & Unmet-Need Assessment

帷幕牆系統市場:2026-2032年全球市場預測(按系統類型、材料類型、功能、項目類型、應用和分銷管道分類)

帷幕牆系統市場:2026-2032年全球市場預測(按系統類型、材料類型、功能、項目類型、應用和分銷管道分類) 帷幕牆系統市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、材料、應用、地區和競爭格局分類,2021-2031年

帷幕牆系統市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、材料、應用、地區和競爭格局分類,2021-2031年 帷幕牆市場規模、佔有率和趨勢分析報告:按產品、最終用途、地區和細分市場分類(2026-2033 年)

帷幕牆市場規模、佔有率和趨勢分析報告:按產品、最終用途、地區和細分市場分類(2026-2033 年) 帷幕牆市場:按產品類型、材料、最終用途和地區分類,2026-2034 年

帷幕牆市場:按產品類型、材料、最終用途和地區分類,2026-2034 年 2026年全球帷幕牆錨固系統市場報告

2026年全球帷幕牆錨固系統市場報告 帷幕牆系統市場:依產品類型、材料、應用、技術和地區分類

帷幕牆系統市場:依產品類型、材料、應用、技術和地區分類 美國建築外觀:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)2026年全球建築幕牆系統市場報告歐洲建築幕牆:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)帷幕牆市場-全球產業規模、佔有率、趨勢、機會和預測,依產品、帷幕牆類型、建築類型、地區和競爭格局分類,2021-2031年預測

美國建築外觀:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)2026年全球建築幕牆系統市場報告歐洲建築幕牆:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)帷幕牆市場-全球產業規模、佔有率、趨勢、機會和預測,依產品、帷幕牆類型、建築類型、地區和競爭格局分類,2021-2031年預測