|

市場調查報告書

商品編碼

2043891

亞太地區保險科技:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)Asia-Pacific Insurtech - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

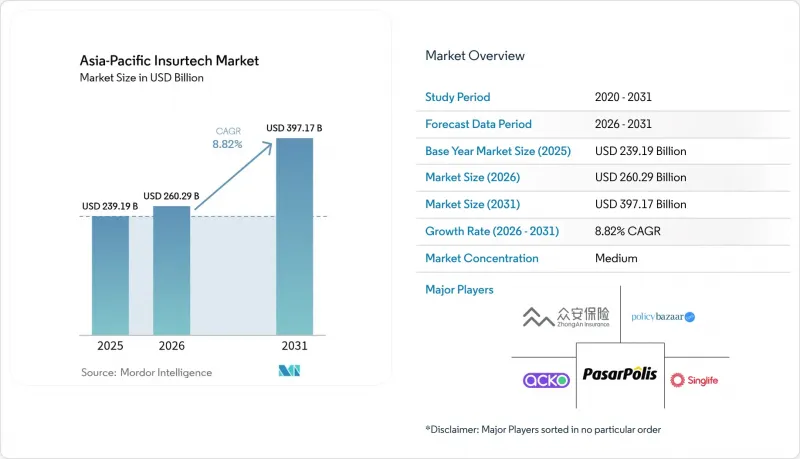

預計亞太地區的保險科技市場規模將從 2025 年的 2,391.9 億美元成長到 2026 年的 2,602.9 億美元,然後在 2031 年達到 3,971.7 億美元,2026 年至 2031 年的複合年成長率為 8.82%。

這一強勁成長得益於以智慧型手機為中心的銷售管道的經濟效益、監管沙盒的加速發展以及先進分析技術的應用,這些技術能夠提高承保準確性並實現理賠流程自動化。嵌入式保險生態系統正穩步拓展先前難以觸及的個人客戶和中小企業客戶群,而東協內部跨境監管的協調統一也降低了多市場平台的進入門檻。行動端客戶獲取成本的降低、特定風險意識的增強以及流入參數型保險解決方案的新資本,進一步增強了亞太地區保險科技市場的成長潛力。由於人工智慧驅動的承保正在削弱傳統的賠付率優勢,競爭格局依然瞬息萬變,促使老牌公司與金融科技公司建立策略夥伴關係。

亞太地區保險科技市場的趨勢與洞察。

嵌入式保險生態系的興起

嵌入式平台將保險融入日常購物流程,使用者無需離開應用程式即可購買保險。這種無縫流程消除了中間環節的摩擦,並將獲客成本降低高達 40%。成本的降低提高了大規模部署的單位盈利。螞蟻集團與阿里巴巴的合作展示了該模式的擴展,透過電子商務、旅遊和錢包交易產生保費收入。新加坡清晰的 API 指南允許非保險公司在現有金融科技牌照下銷售產品,從而降低合規負擔。透過多個觸點提升用戶互動,可以將行為數據回饋給核保部門,從而提高定價準確性並降低賠付率。這些網路效應正在推動嵌入式保險的普及,使其成為亞太地區保險科技市場結構性成長的引擎。

亞太地區面臨的網路風險激增。

數位轉型正在擴大醫療保健、金融和製造業的攻擊面,導致網路保險需求激增。新加坡2024年人工智慧模型風險管理條例要求金融機構展示健全的控制結構,因此買家要求保險公司提供合規證明。保險科技公司正積極應對,部署參數化網路保險產品,根據停機時間等指標自動支付賠款,避免冗長的調查。即時定價引擎整合了威脅情報和漏洞掃描數據,使負責人能夠根據每位客戶的安全狀況設定保費。隨著超大規模服務提供者擴大其區域佈局,以雲端為中心的風險日益增加,導致客製化保險的需求激增。儘管這些因素推動了網路保險滲透率的成長,但對於敏捷的新興參與企業而言,保障仍然存在缺口。

各司法管轄區的資料隱私法規碎片化

亞太地區的監管機構各自製定了不同的同意、儲存和傳輸規則,迫使保險科技公司為每個市場建立獨立的資料堆疊。合規團隊必須掌握新加坡的《個人資料保護法》(PDPA)、印度的《數位個人資料保護法》以及中國的《網路安全法》,導致其成本比專注於單一市場的同業高出25%至35%。這種碎片化阻礙了嵌入式保險的部署,因為與合作夥伴即時共用資料可能違反居住規則。當特定司法管轄區最嚴格的要求適用於所有共用資料時,再保險公司在跨境風險分擔方面面臨挑戰。政府在短時間內收緊或放寬條款等持續變化進一步加劇了不確定性。由此產生的複雜性分散了產品開發資金,並限制了亞太地區保險科技市場的區域擴張。

細分市場分析

到2025年,產物保險將佔保費總額的40.62%,成為亞太保險科技市場中佔有率最大的領域。穩定的理賠模式、長期累積的監管經驗以及高度數位化的汽車和房屋保險支撐了其主導地位。然而,日益激烈的價格競爭和災難性事件造成的損失正對承保利潤率構成壓力,減緩其成長速度。相較之下,專業保險領域正以9.86%的複合年成長率快速擴張,網路保險、寵物保險和旅遊保險在企業和消費者群體中的認知度不斷提高,逐年擴大亞太保險科技市場的規模。菲律賓和斐濟的參數型颶風保險試點計畫表明,具備快速支付功能的產品可以填補長期存在的保障缺口,並吸引跨國捐助者的資金,從而為專業保險公司帶來社會意義和盈利規模。

儘管網路保險因勒索軟體贖金不斷攀升而依然是熱門細分市場,但精算利潤率低導致再保險門檻居高不下,限制了其短期普及。保險科技公司正透過整合威脅情報、終端遙測和雲端服務運轉率指標來解決資料不足的問題,建構動態承保模型,為擁有強大安全措施的公司提供更低的保費。寵物保險也正沿著類似的數據驅動型發展軌跡前進,利用遠端獸醫服務提供持續的行為訊息,從而提高定價的準確性。海運和內河航運保險則利用衛星貨物追蹤技術,在航程中斷的情況下自動進行參數化理賠,減輕出口商的理賠負擔。這些創新措施共同推動了平均保費成長顯著高於市場基準,使專業險種成為亞太保險科技市場領先的長期價值創造引擎。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 嵌入式保險生態系的興起

- 亞太地區正面臨網路風險激增的局面。

- 由於重點放在智慧型手機上,客戶獲取成本正在下降。

- 亞太地區的沙盒式放鬆管制措施

- 透過通用人工智慧進行進階分析/提高核保準確性

- 對與氣候變遷相關的參數化產品的需求正在成長。

- 市場限制因素

- 不同司法管轄區的資料隱私法規仍存在碎片化現象。

- 新風險產品缺乏精算損失數據

- 利潤集中在現有企業手中,限制了它們退出市場的能力。

- 再保險費率上漲和承保能力受限

- 價值/供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

- 競爭公司之間的競爭

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

第5章 市場規模及成長預測(價值,百萬美元)

- 按產品線(保險類型)

- 人壽保險

- 健康保險

- 產物保險(汽車、住宅、商業、責任險)

- 專業領域(網路安全、寵物、海事、旅遊)

- 透過分銷管道

- 直接面對消費者(數位)

- 聚合器/市場

- 數位仲介/MGA

- 嵌入式保險平台

- 傳統代理商/仲介(相容數位化)

- 銀行保險(數位化相容)

- 其他頻道

- 最終用戶

- 個人/個人客戶

- 中小企業/公司

- 大型公司/企業

- 政府/公共部門

- 國家

- 印度

- 中國

- 日本

- 澳洲

- 韓國

- 東南亞

- 亞太其他地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- ZhongAn

- Policybazaar

- Acko

- PasarPolis

- Singlife

- OneDegree

- CXA Group

- Waterdrop

- Koala

- CoverGo

- Bolttech

- Shift Technology

- CarDekho(Insurance arm)

- Turtlemint

- Tokio Marine & Nichido(Digital Lab)

- Ping An OneConnect

- Munich Re Digital Partners

- FWD Group

- Sompo Himaraya

- NTUC Income(Income Insurance)

第7章 市場機會與未來展望

The Asia-Pacific Insurtech Market size is expected to grow from USD 239.19 billion in 2025 to USD 260.29 billion in 2026 and is forecast to reach USD 397.17 billion by 2031 at 8.82% CAGR over 2026-2031.

This resilient growth is rooted in smartphone-first distribution economics, regulatory sandbox acceleration, and the use of advanced analytics that enhance underwriting precision and claims automation. Embedded-insurance ecosystems now secure previously unreachable retail and SME customers, while cross-border regulatory harmonization inside ASEAN lowers entry barriers for multi-market platforms. Falling mobile-acquisition costs, a surge in specialty-risk awareness, and fresh capital flowing into parametric solutions further reinforce the upside for the Asia-Pacific insurtech market. Competitive dynamics remain fluid as AI-enabled underwriting erodes traditional loss-ratio advantages and encourages incumbents to form strategic alliances with fintechs.

Asia-Pacific Insurtech Market Trends and Insights

Rise of Embedded-Insurance Ecosystems

Embedded platforms place cover inside everyday purchase journeys, letting users buy protection without leaving the host app. This seamless flow removes agent friction and cuts acquisition costs by up to 40%, a saving that improves unit economics at scale. Ant Group's partnership with Alibaba shows the model's reach as premiums emerge from e-commerce, travel, and wallet transactions. Singapore's clear API guidelines allow non-insurers to distribute products under existing fintech licenses, keeping compliance overhead low. Higher engagement across multiple touchpoints feeds behavioral data back to underwriters, raising pricing accuracy and lowering loss ratios. These network effects reinforce adoption, positioning embedded insurance as a structural growth engine for the Asia-Pacific insurtech market.

Sharp Increase in Asia-Pacific Cyber-Risk Exposure

Digital transformation widens attack surfaces across health care, finance, and manufacturing, driving urgent demand for cyber cover. Singapore's 2024 AI Model Risk Management rules compel financial firms to prove robust controls, pushing buyers toward policies that document compliance. Insurtechs respond with parametric cyber products that pay automatically on metrics like downtime minutes, avoiding long investigations. Real-time pricing engines ingest threat-intel feeds and vulnerability scans, letting underwriters match premiums to each client's security posture. Cloud concentration risk grows as hyperscale providers expand regional centers, adding urgency for bespoke policies. Together, these forces raise cyber insurance penetration yet leave ample protection gaps for agile entrants.

Persistent Data-Privacy Fragmentation by Jurisdiction

APAC regulators each impose unique consent, storage, and transfer rules, forcing insurtechs to build separate data stacks for every market. Compliance teams must master Singapore's PDPA, India's Digital Personal Data Protection Act, and China's Cybersecurity Law, driving costs 25-35% higher than single-market peers. Fragmentation slows embedded-insurance rollouts because real-time data sharing with partners may breach residency rules. Reinsurers struggle to pool risks across borders when one jurisdiction's strictest requirement governs all shared data. Ongoing changes add further uncertainty as governments tighten or relax clauses with short notice. The resulting complexity diverts capital from product development and constrains the Asia-Pacific insurtech market's regional scaling.

Other drivers and restraints analyzed in the detailed report include:

- Smartphone-First Customer Acquisition Costs Falling

- Sandbox-Style Regulatory Fast-Tracks Across Asia-Pacific

- Thin Actuarial Loss Histories for New-Risk Products

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Property & Casualty retained 40.62% of 2025 premiums, giving it the largest slice of the Asia-Pacific insurtech market share. Stable claim patterns, long-standing regulatory familiarity, and highly digitized motor and household lines underpin this dominance, yet growth momentum is slowing as pricing competition intensifies and catastrophe losses pressure underwriting margins. Specialty Lines, in contrast, are expanding at a 9.86% CAGR, lifting their contribution to the Asia-Pacific insurtech market size year after year as cyber, pet, and travel covers gain recognition across corporate and consumer segments. Parametric cyclone pilots in the Philippines and Fiji illustrate how rapid-payout products can fill long-standing protection gaps and attract multilateral donor funding, giving specialty carriers both social relevance and profitable scale.

Cyber insurance remains the specialty headline as ransomware costs rise, yet actuarial thinness keeps reinsurance attachment points high, tempering near-term penetration. Insurtechs mitigate data scarcity by fusing threat-intelligence feeds, endpoint telemetry, and cloud-service uptime metrics into dynamic underwriting models that reward strong security hygiene with lower premiums. Pet insurance follows a similar data-rich trajectory as tele-vet usage supplies continuous behavioral information that sharpens pricing. Marine and inland transit lines leverage satellite cargo tracking to trigger parametric payouts for voyage disruptions, cutting claims friction for exporters. Together, these innovations lift average premium growth well above the market baseline, positioning Specialty Lines as the primary long-run value engine of the Asia-Pacific insurtech market.

The Asia-Pacific Insurtech Market Report is Segmented by Product Line (Life Insurance, Health Insurance, Property & Casualty, Specialty Lines), Distribution Channel (Direct-To-Consumer Digital, Aggregators/Marketplaces, and More), End User (Retail/Individual, SME/Commercial, and More), and Geography (India, China, Japan, Australia, South Korea, South-East Asia, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- ZhongAn

- Policybazaar

- Acko

- PasarPolis

- Singlife

- OneDegree

- CXA Group

- Waterdrop

- Koala

- CoverGo

- Bolttech

- Shift Technology

- CarDekho (Insurance arm)

- Turtlemint

- Tokio Marine & Nichido (Digital Lab)

- Ping An OneConnect

- Munich Re Digital Partners

- FWD Group

- Sompo Himaraya

- NTUC Income (Income Insurance)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rise of embedded-insurance ecosystems

- 4.2.2 Sharp increase in Asia-Pacific cyber-risk exposure

- 4.2.3 Smartphone-first customer acquisition costs falling

- 4.2.4 Sandbox-style regulatory fast-tracks across Asia-Pacific

- 4.2.5 Advanced analytics/Gen-AI driving underwriting accuracy

- 4.2.6 Climate-linked parametric products gaining traction

- 4.3 Market Restraints

- 4.3.1 Persistent data-privacy fragmentation by jurisdiction

- 4.3.2 Thin actuarial loss histories for new-risk products

- 4.3.3 Profit-pool concentration in incumbents limits exits

- 4.3.4 Rising reinsurance pricing & capacity constraints

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Competitive Rivalry

- 4.7.2 Threat of New Entrants

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Bargaining Power of Suppliers

- 4.7.5 Threat of Substitutes

5 Market Size & Growth Forecasts (Value, USD Million)

- 5.1 By Product Line (Insurance Type)

- 5.1.1 Life Insurance

- 5.1.2 Health Insurance

- 5.1.3 Property & Casualty (Motor, Home, Commercial, Liability)

- 5.1.4 Specialty Lines (Cyber, Pet, Marine, Travel)

- 5.2 By Distribution Channel

- 5.2.1 Direct-to-Consumer (Digital)

- 5.2.2 Aggregators / Marketplaces

- 5.2.3 Digital Brokers / MGAs

- 5.2.4 Embedded Insurance Platforms

- 5.2.5 Traditional Agents / Brokers (digitally enabled)

- 5.2.6 Bancassurance (digitally enabled)

- 5.2.7 Other Channels

- 5.3 By End User

- 5.3.1 Retail / Individual

- 5.3.2 SME / Commercial

- 5.3.3 Large Enterprise / Corporate

- 5.3.4 Government / Public Sector

- 5.4 By Country

- 5.4.1 India

- 5.4.2 China

- 5.4.3 Japan

- 5.4.4 Australia

- 5.4.5 South Korea

- 5.4.6 South-East Asia

- 5.4.7 Rest of Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 ZhongAn

- 6.4.2 Policybazaar

- 6.4.3 Acko

- 6.4.4 PasarPolis

- 6.4.5 Singlife

- 6.4.6 OneDegree

- 6.4.7 CXA Group

- 6.4.8 Waterdrop

- 6.4.9 Koala

- 6.4.10 CoverGo

- 6.4.11 Bolttech

- 6.4.12 Shift Technology

- 6.4.13 CarDekho (Insurance arm)

- 6.4.14 Turtlemint

- 6.4.15 Tokio Marine & Nichido (Digital Lab)

- 6.4.16 Ping An OneConnect

- 6.4.17 Munich Re Digital Partners

- 6.4.18 FWD Group

- 6.4.19 Sompo Himaraya

- 6.4.20 NTUC Income (Income Insurance)

7 Market Opportunities & Future Outlook

- 7.1 Cross-border expansion patterns and market consolidation trends

- 7.2 Emerging technology applications and regulatory changes

保險科技市場-2026-2032年全球市場預測

保險科技市場-2026-2032年全球市場預測 保險科技市場規模、佔有率、趨勢和預測:按類型、服務、技術和地區分類,2026-2034年

保險科技市場規模、佔有率、趨勢和預測:按類型、服務、技術和地區分類,2026-2034年 2026-2030年全球保險科技市場

2026-2030年全球保險科技市場 2026年全球保險科技市場報告

2026年全球保險科技市場報告 保險科技市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶和解決方案分類

保險科技市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶和解決方案分類 2026-2034年全球保險科技市場規模、佔有率、趨勢和成長分析報告

2026-2034年全球保險科技市場規模、佔有率、趨勢和成長分析報告 全球保險科技市場(至 2035 年):依保險科技類型、服務類型、技術類型、最終用戶、公司類型、地區、產業趨勢和預測

全球保險科技市場(至 2035 年):依保險科技類型、服務類型、技術類型、最終用戶、公司類型、地區、產業趨勢和預測 保險科技市場-全球產業規模、佔有率、趨勢、機會及預測(按類型、保費範圍、地區及競爭格局分類,2021-2031年)

保險科技市場-全球產業規模、佔有率、趨勢、機會及預測(按類型、保費範圍、地區及競爭格局分類,2021-2031年) 保險科技:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)保險科技市場規模、佔有率、成長及全球產業分析:按類型、應用和地區劃分的洞察與預測(2026-2034)

保險科技:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)保險科技市場規模、佔有率、成長及全球產業分析:按類型、應用和地區劃分的洞察與預測(2026-2034)