|

市場調查報告書

商品編碼

2043840

歐洲聚氨酯(PU)黏合劑:市場佔有率分析、產業趨勢和統計數據以及成長預測(2026-2031)Europe Polyurethane (PU) Hot-Melt Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

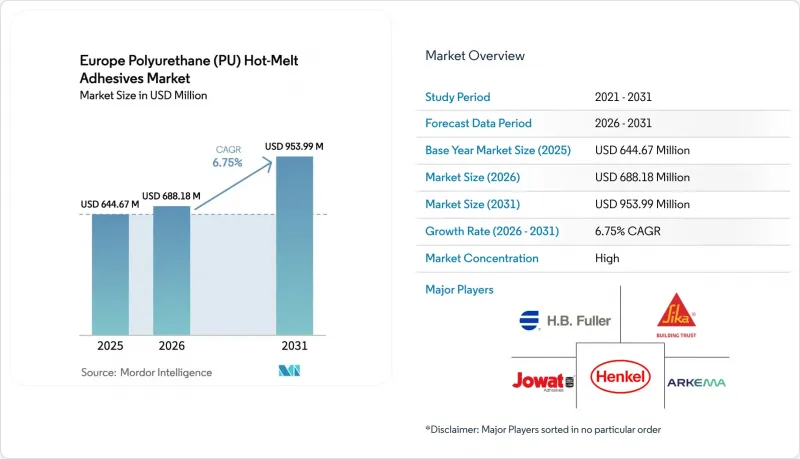

歐洲聚氨酯黏合劑市場預計將從 2025 年的 6.4467 億美元和 2026 年的 6.8818 億美元成長到 2031 年的 9.5399 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 6.75%。

溶劑型化學品的淘汰速度加快、封邊和汽車組裝自動化技術的進步,以及對輕量、易修復包裝日益成長的需求,都在推動高性能反應型配方的需求。預計到2025年,西歐小包裹遞送網路將在歐盟內部處理21億件貨物,這將擴大與再生瓦楞紙板和高速封箱機相容的快速固化型黏合劑的基本客群。汽車原始設備製造商(OEM)正在用聚氨酯黏合劑取代機械緊固件,以減輕車身本體重量,每塊車頂面板最多可減輕2公斤,從而直接提高電動車的續航里程。同時,德國、波蘭和義大利的家具製造商正在安裝無縫封邊設備,這些設備需要黏合劑在25公尺/分鐘的生產線速度下,於10秒內固化。儘管由於異氰酸酯原料的供應風險,原料成本波動性增大,但主要的配方生產商正在透過後向整合多元醇生產能力來規避風險,並透過進行生物衍生中間體的實驗來降低風險敞口。

歐洲聚氨酯(PU)熱熔膠黏合劑趨勢與洞察

電子商務包裝量激增。

2025年,歐盟境內的跨境小包裹運輸量將達21億件,較上年增加12%。這一成長推動了履約中心從固化速度較慢的水性黏合劑轉向可在5秒內固化於再生瓦楞紙板基材上的反應型膠粘劑。漢高公司於2025年初推出的Technomelt Supra 100系列產品,能夠黏合低紙張重量的襯紙,並能承受自動化分類機的衝擊負荷。即將訂定的歐盟包裝和包裝廢棄物法規的目標是到2030年實現65%的再生材料使用率,這進一步強調了即使在粗糙纖維表面上也能表現良好的化學成分的重要性。波斯基公司報告稱,2025年其在歐洲的包裝黏合劑銷量將成長15%,其中聚氨酯基熱熔膠的增幅超過一半。

歐盟VOC法規正在加速無溶劑黏合劑的採用。

工業排放指令將工廠層級的VOC排放限制在每公斤黏合劑50克以內,使得歐洲大多數新裝置不再使用溶劑型接觸黏合劑。 2024年德國《TA Luft》法規的修訂將家具和汽車生產線的VOC排放量限制收緊至每公斤20克,進一步鞏固了向100%固態聚氨酯熱熔膠的轉變。科思創的「Desmomelt」產品線不排放VOC,且可在環境濕度下固化,由於目的地設備製造商(OEM)優先考慮受監管的替代品,該產品線在2025年的銷量成長了22%。根據法國的ICPE(環境保護分類設施)框架,使用超過一噸黏合劑的工廠現在必須進行年度VOC審核,這增加了固定管理成本,並促使無溶劑系統得到推廣。產業整合正在加速。 2025年,受監管障礙的推動,西卡收購了波蘭和西班牙的兩家區域製造商。

異氰酸酯原料價格波動

2025年,歐洲MDI現貨均價預估為每噸2,450歐元,較2024年1月大幅上漲18%,主因是中國減產及歐洲天然氣成本上漲。BASF、科思創和亨斯邁將區域產量削減了12%,以優先滿足利潤率更高的硬質發泡體客戶的需求,並保障黏合劑供應。 2025年,TDI價格在每噸2100歐元至2900歐元之間波動,這反映了BASF維希港工廠和科思創多爾馬根工廠的關閉。現貨採購加工商的利潤率壓縮超過300個基點,導致義大利和西班牙的幾家工廠停止新產品研發。 2025年下半年,布魯塞爾對異氰酸酯生產商展開反壟斷調查,進一步加劇了擴張計畫的不確定性。

細分市場分析

截至2025年,反應型聚氨酯(PU)熱熔膠將佔歐洲PU黏合劑市場規模的86.20%,預計在預測期(2026-2031年)內將以6.92%的年均成長率成長。這主要得益於胺甲酸乙酯-脲交聯技術的應用,該技術可生產出耐熱耐濕、強度超過10 MPa的接合。汽車車身本體黏合、電池組封裝和醫療穿戴式裝置均依賴這種化學反應,以承受134 度C的高溫消毒和1000次充放電振動循環。加工企業也高度重視其在等離子體活化後對低表面能基材(例如聚烯彈性體)的黏合性能。德國嚴格的VOC(揮發性有機化合物)法規對反應型配方有利,因為它們是100%固態且不含溶劑的。

非反應型聚氨酯熱熔膠因其冷卻固化速度快且可透過加熱重新運作,在書籍裝訂、紡織品層壓和臨時鞋帶固定等領域仍十分實用。書籍裝訂商欣賞柔軟性的開放時間,這有助於對齊多個環襯;而軟包裝加工商則讚賞其可在低於 120 度C 的溫度下使用,從而減少天然氣消耗。葡萄牙的製鞋廠正擴大將非反應型熱熔膠用於鞋頭(鞋面)的焊接,因為熱成型後需要徹底清除黏合劑。儘管具有這些優勢,該行業仍面臨結構性挑戰。歐盟循環經濟指南強調耐用組裝和可回收性,這降低了易於返工的黏合劑的吸引力。因此,歐洲聚氨酯 (PU)黏合劑市場將繼續向反應型化學體系傾斜,而非反應型系統則將繼續保持其在短開放時間和低熱基材方面的利基市場地位。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 電子商務包裝材料處理量激增。

- 電子設備組裝向低VOC黏合劑的過渡

- 歐盟的 VOC 法規正在加速無溶劑黏合劑的採用。

- 需要高速循環黏合的輕量化汽車結構

- 模組化家俱生產線封邊自動化

- 市場限制因素

- 異氰酸酯原料價格波動

- 二異氰酸酯處理人員強制訓練條例(歐盟 2023/C)

- 由於歐洲能源價格飆升,熔煉生產線營運成本(OPEX)不斷上升。

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模與成長預測

- 按類型

- 無回應

- 反應性

- 透過使用

- 包裝

- 衛生保健

- 車

- 家具

- 鞋類

- 纖維

- 電子學

- 書籍裝訂

- 其他

- 按地區

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- 3M

- AdCo(UK)Ltd.

- Arkema

- Artimelt AG

- BASF SE

- Buhnen Gmbh & Co. KG

- Delo Industrial Adhesives

- DIC CORPORATION

- Dow

- Franklin International

- HB Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC

- Jowat SE

- Klebchemie MG Becker GmbH & Co. KG

- Mapei SpA

- Master Bond Inc.

- Sika AG

第7章 市場機會與未來展望

The Europe Polyurethane Hot-Melt Adhesives Market size is projected to expand from USD 644.67 million in 2025 and USD 688.18 million in 2026 to USD 953.99 million by 2031, registering a CAGR of 6.75% between 2026 to 2031. Accelerated migration away from solvent-based chemistries, rising automation in edge-banding and vehicle assembly, and the quest for lighter, repair-friendly packaging are steering volume toward high-performance reactive formulations. Western European parcel networks handled 2.1 billion intra-EU shipments in 2025, broadening the customer base for fast-setting grades that tolerate recycled board and high-speed case sealers. Automotive OEMs are substituting mechanical fasteners with polyurethane bonding to cut body-in-white weight by up to 2 kg per roof panel, directly improving electric-vehicle range. At the same time, furniture lines in Germany, Poland, and Italy have adopted zero-joint edge-banding equipment that demands adhesives curing in less than 10 seconds at 25 m min line speeds. Supply risk for isocyanate feedstocks has elevated input-cost volatility, but leading formulators are hedging by backward-integrating polyol capacity and experimenting with bio-based intermediates to soften exposure.

Europe Polyurethane (PU) Hot-Melt Adhesives Market Trends and Insights

Surge in E-Commerce Packaging Volumes

Cross-border parcel traffic within the European Union rose 12% year-on-year to 2.1 billion units in 2025. Higher throughput has pushed fulfillment centers to replace slower water-based adhesives with reactive grades that set within five seconds on recycled corrugated substrates. Henkel's Technomelt Supra 100 series, launched in early 2025, withstands the impact loads of automated sorters while bonding to lower-grammage liners. Upcoming European Union (EU) Packaging and Packaging Waste Regulation targets 65% recycled content by 2030, further tilting specifications toward chemistries that perform on rougher fiber surfaces. Bostik recorded a 15% jump in European packaging-adhesive revenue in 2025, noting that polyurethane hot melts supplied more than half of the incremental growth.

European Union VOC Rules Accelerating Solvent-Free Adhesive Adoption

The Industrial Emissions Directive caps plant-level VOC emissions at 50 g kg adhesive applied, eliminating most solvent-based contact adhesives from new European installations. Germany's TA Luft revision in 2024 tightened the limit to 20 g/kg for furniture and automotive lines, cementing the transition to 100%-solids polyurethane hot melts. Covestro's Desmomelt portfolio, which emits zero VOCs (Volatile Organic Compounds) and cures via ambient moisture, registered a 22% sales rise in 2025 as OEMs (Original Equipment Manufacturers) prioritized compliance-ready alternatives. France's ICPE (Installations classified for environmental protection) framework now requires annual VOC audits for plants using more than one ton of adhesive, raising fixed administrative costs and favoring solvent-free systems. Consolidation is accelerating: Sika purchased two regional producers in Poland and Spain during 2025, citing the regulatory hurdle as a catalyst.

Isocyanate Feedstock Price Volatility

European MDI spot prices averaged EUR 2,450 t in 2025, an 18% leap over January 2024, driven by Chinese production cuts and Europe's elevated gas costs. BASF, Covestro, and Huntsman trimmed regional output by 12%, prioritizing higher-margin rigid foam customers and tightening adhesive supply. TDI prices fluctuated between EUR 2,100 and EUR 2,900 t during 2025, reflecting outages at BASF Ludwigshafen and Covestro Dormagen. Margin compression exceeded 300 basis points for spot-buying converters, pushing several Italian and Spanish shops to halt new-product development. Brussels opened an antitrust investigation into isocyanate producers in late 2025, injecting added uncertainty into expansion plans.

Other drivers and restraints analyzed in the detailed report include:

- Automotive Lightweight Structures Needing Fast-Cycle Bonding

- Edge-Banding Automation in Modular Furniture Lines

- Mandatory Di-Isocyanate Worker-Training Regulation (EU 2023/C)

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Reactive grades accounted for 86.20% of the Europe Polyurethane (PU) Hot-Melt Adhesives market size in 2025 and are projected to grow at 6.92% during the forecast period (2026-2031), propelled by urethane-urea crosslinking that yields heat- and moisture-resistant joints above 10 MPa. Automobile body-in-white bonding, battery-pack encapsulation, and medical wearables rely on this chemistry to resist sterilization at 134°C or endure 1,000 charge-discharge vibration cycles. Converters also prize the adhesives for their ability to bond to low-surface-energy substrates such as polyolefin elastomers after plasma activation. Germany's stringent VOC limits provide a regulatory tailwind because reactive formulations are 100% solids and solvent-free.

Non-reactive polyurethane hot melts' utility persists in bookbinding, textile lamination, and temporary footwear lasting since they cool-set rapidly and can be heat-reactivated. Book manufacturers value the open time flexibility for multi-signature alignment, while flexible-packaging converters laud the sub-120°C application that cuts natural-gas usage. Footwear factories in Portugal have shifted to non-reactive grades for toe-lasting, where the bond must release cleanly post-thermoforming. Despite these strengths, the segment faces structural headwinds: EU circular-economy guidelines reward durable assemblies and recyclability, diminishing the appeal of easy-rework adhesives. Consequently, the Europe polyurethane (PU) hot-melt adhesives market will continue tilting toward reactive chemistries, but non-reactive systems will defend niches tied to short dwell times and low-heat substrates.

The Europe Polyurethane (PU) Hot-Melt Adhesives Market is Segmented by Type (Non-Reactive and Reactive), Application (Packaging, Healthcare, Automotive, Furniture, Footwear, Textile, Electronics, Bookbinding, and Others), and Geography (Germany, United Kingdom, France, Italy, Spain, Russia, and the Rest of Europe). The Market Sizing and Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- 3M

- AdCo (UK) Ltd.

- Arkema

- Artimelt AG

- BASF SE

- Buhnen Gmbh & Co. KG

- Delo Industrial Adhesives

- DIC CORPORATION

- Dow

- Franklin International

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC

- Jowat SE

- Klebchemie M. G. Becker GmbH & Co. KG

- Mapei SpA

- Master Bond Inc.

- Sika AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in e-commerce packaging volumes

- 4.2.2 Electronics assembly shift toward low-VOC bonding

- 4.2.3 European Union VOC rules accelerating solvent-free adhesive adoption

- 4.2.4 Automotive lightweight structures needing fast-cycle bonding

- 4.2.5 Edge-banding automation in modular furniture lines

- 4.3 Market Restraints

- 4.3.1 Isocyanate feedstock price volatility

- 4.3.2 Mandatory di-isocyanate worker-training regulation (EU 2023/ C)

- 4.3.3 High European energy prices raising melt-line OPEX

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Non-reactive

- 5.1.2 Reactive

- 5.2 By Application

- 5.2.1 Packaging

- 5.2.2 Healthcare

- 5.2.3 Automotive

- 5.2.4 Furniture

- 5.2.5 Footwear

- 5.2.6 Textile

- 5.2.7 Electronics

- 5.2.8 Bookbinding

- 5.2.9 Others

- 5.3 By Geography

- 5.3.1 Germany

- 5.3.2 United Kingdom

- 5.3.3 France

- 5.3.4 Italy

- 5.3.5 Spain

- 5.3.6 Russia

- 5.3.7 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 3M

- 6.4.2 AdCo (UK) Ltd.

- 6.4.3 Arkema

- 6.4.4 Artimelt AG

- 6.4.5 BASF SE

- 6.4.6 Buhnen Gmbh & Co. KG

- 6.4.7 Delo Industrial Adhesives

- 6.4.8 DIC CORPORATION

- 6.4.9 Dow

- 6.4.10 Franklin International

- 6.4.11 H.B. Fuller Company

- 6.4.12 Henkel AG & Co. KGaA

- 6.4.13 Huntsman International LLC

- 6.4.14 Jowat SE

- 6.4.15 Klebchemie M. G. Becker GmbH & Co. KG

- 6.4.16 Mapei SpA

- 6.4.17 Master Bond Inc.

- 6.4.18 Sika AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

熱熔膠市場:依技術、形態、黏合機制、溫度類型、終端應用產業和分銷管道分類-2026 - 2032年全球市場預測熱熔膠帶市場:按產品類型、黏合劑樹脂類型、厚度、應用和分銷管道分類-全球預測,2026-2032年

熱熔膠市場:依技術、形態、黏合機制、溫度類型、終端應用產業和分銷管道分類-2026 - 2032年全球市場預測熱熔膠帶市場:按產品類型、黏合劑樹脂類型、厚度、應用和分銷管道分類-全球預測,2026-2032年 熱熔膠市場:依產品、原料、應用、最終用途、國家及地區黏合劑-全球產業分析、市場規模、市場佔有率及2026年至2033年預測

熱熔膠市場:依產品、原料、應用、最終用途、國家及地區黏合劑-全球產業分析、市場規模、市場佔有率及2026年至2033年預測 熱熔膠市場規模、佔有率和成長分析:按材料(基體樹脂)、產品形式、最終用途產業、分銷管道和地區分類-2026 - 2033年產業預測

熱熔膠市場規模、佔有率和成長分析:按材料(基體樹脂)、產品形式、最終用途產業、分銷管道和地區分類-2026 - 2033年產業預測 熱熔膠市場規模、佔有率和趨勢分析報告:按產品、原料、應用、地區和細分市場黏合劑(2026-2033 年)聚酯熱熔膠市場規模、佔有率和趨勢分析報告:按黏合劑、地區和細分市場預測(2026-2033 年)結構膠帶市場:2026-2032年全球市場預測(按建築應用、材料、黏合劑類型、用途和最終用途分類)

熱熔膠市場規模、佔有率和趨勢分析報告:按產品、原料、應用、地區和細分市場黏合劑(2026-2033 年)聚酯熱熔膠市場規模、佔有率和趨勢分析報告:按黏合劑、地區和細分市場預測(2026-2033 年)結構膠帶市場:2026-2032年全球市場預測(按建築應用、材料、黏合劑類型、用途和最終用途分類) 高黏性膠帶市場:按產品類型、應用、銷售管道、最終用戶和地區分類。

高黏性膠帶市場:按產品類型、應用、銷售管道、最終用戶和地區分類。 全球熱熔包裝黏合劑市場規模、佔有率、趨勢及成長分析報告(2026-2034年)

全球熱熔包裝黏合劑市場規模、佔有率、趨勢及成長分析報告(2026-2034年) 英國黏合劑:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

英國黏合劑:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)