|

市場調查報告書

商品編碼

2043861

英國黏合劑:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)United Kingdom Hot-Melt Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

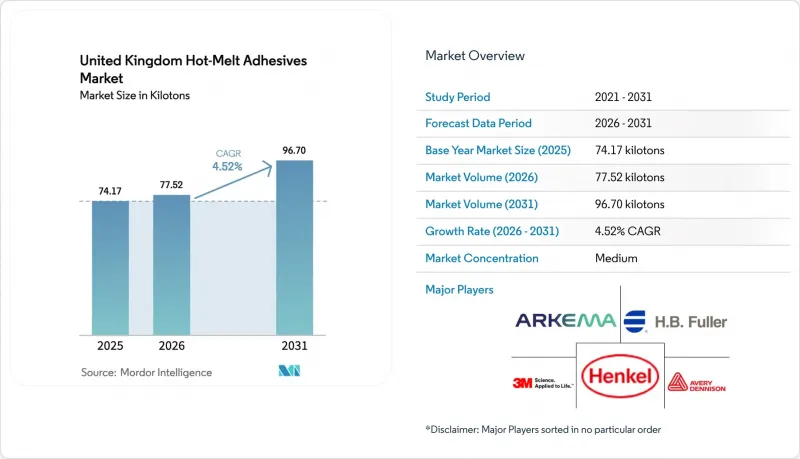

英國黏合劑市場預計將從 2025 年的 74.17 千噸成長到 2026 年的 77.52 千噸,到 2031 年達到 96.70 千噸,2026 年至 2031 年的複合年成長率為 4.52%。

隨著電子商務小包裹運輸量的激增和塑膠包裝稅的實施,加工商正轉向使用生物基和水溶性化學品。這些選擇不僅允許使用回收材料,還能維持生產線的速度。這種轉變在瓦楞紙板和軟包裝生產線上尤其明顯,這些生產線正在採用低溫快速固化樹脂以避免生產瓶頸。茂金屬聚烯技術的進步使這一轉變成為可能。與此同時,汽車產量下降和對二異氰酸酯暴露的更嚴格監管正在給傳統聚氨酯的需求帶來壓力。然而,模組化建築和醫療設備等領域正成為新的成長點,穩定了市場需求。目前,供應商正透過提供包含黏合劑、混煉技術、應用設備和法規專業知識的完整解決方案來建立競爭優勢。

英國熱熔膠黏合劑趨勢與洞察

英國塑膠包裝稅促進可回收黏合劑的銷售

2024年,相當一部分註冊產品申請了包裝中再生材料含量低於30%的課稅優惠。然而,隨著2027年4月認證義務的實施,合規要求已顯著收緊。化合物生產商現在必須確保黏合劑殘留物在低於60°C的溫度下於浮選槽中分離,這項要求淘汰了許多高交聯度的EVA等級產品。漢高強調轉向既能保持可回收性又能與現有生產線相容的解決方案,並推出了一款獲得ISCC PLUS認證的生物基替代產品。隨著課稅調整以應對通貨膨脹,原生材料和再生材料之間的成本差距預計將擴大,可回收性將成為英國熱熔膠市場黏合劑選擇的關鍵標準。

黏合劑低溫茂金屬基熱熔膠

採用茂金屬催化劑的聚烯熱熔膠的黏合溫度低於傳統的EVA熱熔膠,不僅節能,還能使熱敏標籤在不變形的情況下使用。較低的黏合溫度還能縮短冷卻時間,無需額外的點膠設備即可提高生產線速度。這對於致力於永續性的飲料工廠尤其有利。此外,此熱熔膠對非極性薄膜具有極強的剝離和粘貼粘合力,使加工商能夠減少用量,從而降低排放氣體和材料成本。隨著電費上漲,這些技術的應用日益廣泛,帶來了實質的投資回報,並提升了該技術在英國黏合劑市場的吸引力。

自動化導致熟練塗裝工人短缺

在英國,學徒制訓練體系的不足導致合格技術人員短缺,無法滿足黏合劑產業的需求。因此,加工商不得不依賴手動膠槍,造成黏合劑浪費增加和缺陷率上升。雖然配備預測性維護功能的物聯網熔化設備提供了一定的幫助,但它無法取代現場實踐操作和解決問題的能力。除非職業學校的課程設置得到改進,否則這種人才短缺問題將繼續阻礙英國熱熔膠黏合劑的生產力提升。

細分市場分析

2025年,熱塑性聚氨酯憑藉其獨特的柔軟性、耐磨性和黏合強度組合,佔據了英國黏合劑市場61.69%的佔有率。這些特性使其成為汽車內裝、鞋類和高阻隔薄膜層壓等多種應用領域的首選材料。亨斯邁的IROGRAN系列產品專為各種噴塗貼合加工應用而設計,在180 度C下的熔體黏度低於10,000 cP。乙烯-醋酸乙烯酯共聚物(EVA)因其成本效益而一直是瓦楞紙板密封的首選材料,但隨著加工商轉向固化速度更快、固化溫度更低的材料,其市場佔有率正在下降。苯乙烯-丁二烯共聚物預計在2026年至2031年的預測期內將以5.78%的複合年成長率成長,正在逼近聚丙烯標籤,尤其是在剝離強度和可回收性至關重要的應用領域。隨著品牌所有者轉向單一材料的軟質包裝,英國黏合劑市場對苯乙烯-丁二烯共聚物的需求正在增加,特別是對於能夠保持聚乙烯流完整性的黏合劑。

面對利潤率壓力,加工商正日益探索將熱塑性聚氨酯和聚烯彈性體結合的混合材料,以期在成本和性能之間取得平衡。科思創的「Desmomelt」系列產品包含生物基成分,符合永續性目標並具有良好的熱穩定性,但其應用僅限於願意支付溢價的目的地設備製造商 (OEM)。儘管聚醯胺類產品在高溫紡織領域仍佔據主導地位,但茂金屬聚烯正在迅速發展,尤其是在生產線能源效率優先於傳統 120 度C工作溫度的情況下。目前樹脂的選擇受到課稅和可回收性因素的影響,這表明英國黏合劑市場的未來將更多地取決於混煉技術,而不僅僅是價格。

《英國熱熔膠黏合劑報告》按樹脂類型(熱塑性聚氨酯、乙烯-醋酸乙烯酯共聚物、苯乙烯-丁二烯共聚物及其他樹脂類型)和終端用戶行業(建築施工、紙板包裝、木工、運輸、鞋類和皮革、醫療保健等)進行細分。市場預測以噸為單位。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場促進因素

- 英國脫歐後電子商務包裝熱潮

- 英國塑膠包裝稅促進可回收黏合劑的開發

- 採用低溫茂金屬基HMA

- 異地模組化建築的激增

- 英國國家醫療服務體系 (NHS) 向無溶劑醫療設備過渡

- 市場限制因素

- 自動化導致熟練工人短缺

- 英國REACH 式異氰酸酯法規

- 國內汽車產量下滑

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 依樹脂類型

- 熱塑性聚氨酯

- 乙烯-醋酸乙烯酯

- 苯乙烯-丁二烯共聚物

- 其他樹脂類型

- 按最終用戶行業分類

- 建築/施工

- 紙板和包裝

- 木工和細木工

- 運輸

- 鞋類和皮革

- 衛生保健

- 電氣和電子設備

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- 3M

- Adco(UK)Ltd

- Alphabond Adhesives

- Arkema

- Avery Dennison Corporation

- Delo Industrial Adhesives

- Dow Chemical Company

- Drytac Corporation

- EOC Group

- HB Fuller Company

- Henkel AG & Company KGaA

- Hexcel Corporation

- Huntsman Corporation

- Jowat UK Limited

- KLEBCHEMIE MG Becker GmbH & Co. KG

- Sika AG

第7章 市場機會與未來展望

The United Kingdom Hot-Melt Adhesives Market size is expected to increase from 74.17 kilotons in 2025 to 77.52 kilotons in 2026 and reach 96.70 kilotons by 2031, growing at a CAGR of 4.52% over 2026-2031.

As e-commerce parcel traffic surges and the Plastic Packaging Tax takes effect, converters are pivoting towards bio-derived and water-compatible chemistries. These choices not only support substrates with recycled content but also maintain production line speeds. This shift is particularly evident in corrugated and flexible-film lines, which are now opting for lower-temperature, faster-curing resins to avoid bottlenecks. This transition has been made possible by advancements in metallocene polyolefin technology. At the same time, a decline in automotive output and tightening limits on diisocyanate exposure are pressuring legacy polyurethane demand. However, sectors such as modular construction and medical devices are emerging as stabilizing volume pockets. Currently, suppliers find a competitive edge not only in selling adhesives but also in bundling formulation expertise, dispensing equipment, and regulatory insights.

United Kingdom Hot-Melt Adhesives Market Trends and Insights

UK Plastic Packaging Tax Pushes Recyclable Adhesives

In 2024, a significant portion of the registered tonnage claimed an exemption from the levy on packaging with less than 30% recycled content. However, compliance is tightening with the certification mandate set for April 2027. Formulators are now ensuring that adhesive residues separate in float-sink tanks at temperatures below 60 degrees Celsius, a requirement that eliminates many high-crosslink EVA grades. Henkel, highlighting a shift toward solutions compatible with existing lines and maintaining recyclability, has introduced bio-attributed drop-in alternatives certified under ISCC PLUS. As the levy adjusts with inflation, the cost disparity between virgin and recycled substrates is expected to grow, solidifying recyclability as a key criterion in adhesive selection within the United Kingdom hot-melt adhesives market.

Low-Temperature Metallocene HMA Adoption

Metallocene-catalyzed polyolefin hot melts bond at lower temperatures than conventional EVA, saving energy and allowing the use of heat-sensitive labels without distortion. These lower bonding temperatures also reduce cool-down dwell time, enabling increased line speed without extra applicators. This is particularly beneficial for beverage plants aiming for sustainability. Additionally, strong peel adhesion on non-polar films allows converters to reduce coat weight, cutting emissions and material costs. With rising electricity tariffs, these practices have seen increased adoption, leading to tangible paybacks and enhancing the technology's appeal in the United Kingdom hot-melt adhesives market

Skilled Applicator Shortage for Automation

In the United Kingdom, apprenticeships are falling short, producing fewer certified technicians than the hot-melt adhesive sector demands. As a result, converters are turning to manual guns, which leads to increased adhesive waste and a rise in defect rates. Although the IoT-enabled melters with predictive maintenance provide some assistance, they cannot replace the need for hands-on problem-solving on the shop floor. Without an enhancement in technical college curricula, this talent gap continues to hinder productivity in the United Kingdom's hot-melt adhesives market.

Other drivers and restraints analyzed in the detailed report include:

- Surge in Off-Site Modular Construction

- NHS Shift to Solvent-Free Medical Devices

- UK REACH-Style Limits on Isocyanates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, thermoplastic polyurethane captured 61.69% of the United Kingdom hot-melt adhesives market, due to its unique combination of flexibility, abrasion resistance, and bond strength. These qualities make it a preferred choice for diverse applications, including automotive interiors, footwear, and high-barrier film lamination. Huntsman's IROGRAN grades, designed for broad spray applications in laminations, feature melt viscosities dropping below 10,000 cP at 180°C. Ethylene-vinyl acetate, traditionally favored for carton sealing due to its cost-effectiveness, is losing ground as converters turn to faster-curing and lower-temperature options. Styrenic-butadiene copolymers, set to grow at a 5.78% CAGR through the forecast period of 2026-2031, are closing in on polypropylene labels, especially in applications prioritizing peel strength and recyclability. With brand owners shifting towards mono-material flexible packs, the demand for styrenic-butadiene copolymers in the United Kingdom hot-melt adhesives market is increasing, particularly for adhesives that preserve the integrity of polyethylene streams.

Converters, facing margin pressures, are increasingly exploring hybrid blends that merge thermoplastic polyurethane with polyolefin elastomers, achieving a balance between cost and performance. Covestro's bio-attributed Desmomelt line aligns with sustainability objectives and offers thermal stability, but its uptake is limited to original equipment manufacturers (OEMs) ready to pay a premium. While polyamide grades still lead in high-temperature textiles, metallocene polyolefins are gaining traction, especially where energy efficiency on the production line is prioritized over the conventional 120°C service temperature. Today's resin choices are influenced by taxation and recyclability factors, highlighting that the future of the United Kingdom hot-melt adhesives market will hinge more on formulation science than on pricing alone.

The United Kingdom Hot-Melt Adhesives Market Report is Segmented by Resin Type (Thermoplastic Polyurethane, Ethylene Vinyl Acetate, Styrene-Butadiene Copolymers, and Other Resin Types) and End-User Industry (Building and Construction, Paper Board and Packaging, Woodworking and Joinery, Transportation, Footwear and Leather, Healthcare, and More). The Market Forecasts are Provided in Terms of Volume (Tons).

List of Companies Covered in this Report:

- 3M

- Adco (UK) Ltd

- Alphabond Adhesives

- Arkema

- Avery Dennison Corporation

- Delo Industrial Adhesives

- Dow Chemical Company

- Drytac Corporation

- EOC Group

- HB Fuller Company

- Henkel AG & Company KGaA

- Hexcel Corporation

- Huntsman Corporation

- Jowat UK Limited

- KLEBCHEMIE M. G. Becker GmbH & Co. KG

- Sika AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Drivers

- 4.1.1 E-commerce packaging boom post-Brexit

- 4.1.2 UK Plastic Packaging Tax pushes recyclable adhesives

- 4.1.3 Low-temperature metallocene HMA adoption

- 4.1.4 Surge in off-site modular construction

- 4.1.5 NHS shift to solvent-free medical devices

- 4.2 Market Restraints

- 4.2.1 Skilled applicator shortage for automation

- 4.2.2 UK REACH-style limits on isocyanates

- 4.2.3 Sluggish domestic auto production

- 4.3 Value Chain Analysis

- 4.4 Porter's Five Forces

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitutes

- 4.4.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Resin Type

- 5.1.1 Thermoplastic Polyurethane

- 5.1.2 Ethylene Vinyl Acetate

- 5.1.3 Styrene-butadiene Copolymers

- 5.1.4 Other Resin Types

- 5.2 By End-user Industry

- 5.2.1 Building and Construction

- 5.2.2 Paper Board and Packaging

- 5.2.3 Woodworking and Joinery

- 5.2.4 Transportation

- 5.2.5 Footwear and Leather

- 5.2.6 Healthcare

- 5.2.7 Electrical and Electronic Appliances

- 5.2.8 Other End-user Industries

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 3M

- 6.4.2 Adco (UK) Ltd

- 6.4.3 Alphabond Adhesives

- 6.4.4 Arkema

- 6.4.5 Avery Dennison Corporation

- 6.4.6 Delo Industrial Adhesives

- 6.4.7 Dow Chemical Company

- 6.4.8 Drytac Corporation

- 6.4.9 EOC Group

- 6.4.10 HB Fuller Company

- 6.4.11 Henkel AG & Company KGaA

- 6.4.12 Hexcel Corporation

- 6.4.13 Huntsman Corporation

- 6.4.14 Jowat UK Limited

- 6.4.15 KLEBCHEMIE M. G. Becker GmbH & Co. KG

- 6.4.16 Sika AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

熱熔膠市場:依技術、形態、黏合機制、溫度類型、終端應用產業和分銷管道分類-2026 - 2032年全球市場預測熱熔膠帶市場:按產品類型、黏合劑樹脂類型、厚度、應用和分銷管道分類-全球預測,2026-2032年

熱熔膠市場:依技術、形態、黏合機制、溫度類型、終端應用產業和分銷管道分類-2026 - 2032年全球市場預測熱熔膠帶市場:按產品類型、黏合劑樹脂類型、厚度、應用和分銷管道分類-全球預測,2026-2032年 熱熔膠市場:依產品、原料、應用、最終用途、國家及地區黏合劑-全球產業分析、市場規模、市場佔有率及2026年至2033年預測

熱熔膠市場:依產品、原料、應用、最終用途、國家及地區黏合劑-全球產業分析、市場規模、市場佔有率及2026年至2033年預測 熱熔膠市場規模、佔有率和成長分析:按材料(基體樹脂)、產品形式、最終用途產業、分銷管道和地區分類-2026 - 2033年產業預測

熱熔膠市場規模、佔有率和成長分析:按材料(基體樹脂)、產品形式、最終用途產業、分銷管道和地區分類-2026 - 2033年產業預測 熱熔膠市場規模、佔有率和趨勢分析報告:按產品、原料、應用、地區和細分市場黏合劑(2026-2033 年)聚酯熱熔膠市場規模、佔有率和趨勢分析報告:按黏合劑、地區和細分市場預測(2026-2033 年)結構膠帶市場:2026-2032年全球市場預測(按建築應用、材料、黏合劑類型、用途和最終用途分類)

熱熔膠市場規模、佔有率和趨勢分析報告:按產品、原料、應用、地區和細分市場黏合劑(2026-2033 年)聚酯熱熔膠市場規模、佔有率和趨勢分析報告:按黏合劑、地區和細分市場預測(2026-2033 年)結構膠帶市場:2026-2032年全球市場預測(按建築應用、材料、黏合劑類型、用途和最終用途分類) 高黏性膠帶市場:按產品類型、應用、銷售管道、最終用戶和地區分類。

高黏性膠帶市場:按產品類型、應用、銷售管道、最終用戶和地區分類。 全球熱熔包裝黏合劑市場規模、佔有率、趨勢及成長分析報告(2026-2034年)熱熔膠市場:依聚合物基材、應用及地區黏合劑

全球熱熔包裝黏合劑市場規模、佔有率、趨勢及成長分析報告(2026-2034年)熱熔膠市場:依聚合物基材、應用及地區黏合劑