|

市場調查報告書

商品編碼

2034994

中國半導體裝置:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)China Semiconductor Device - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

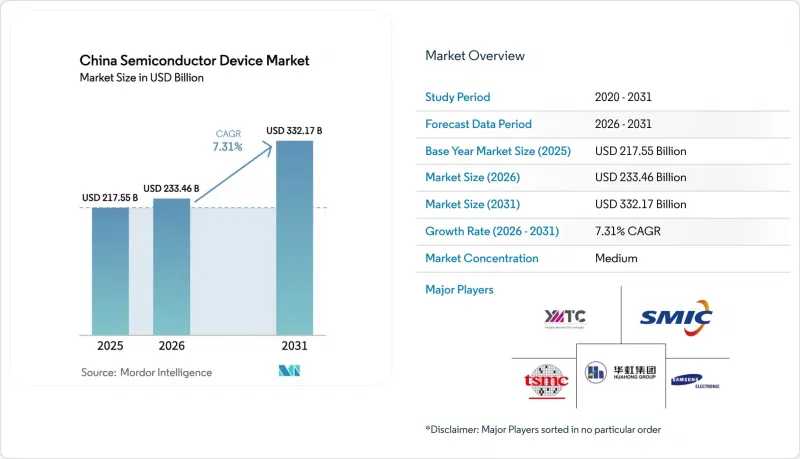

2025年中國半導體裝置市場價值為2,175.5億美元,預計到2031年將達到3,321.7億美元,而2026年為2,334.6億美元,預測期內(2026-2031年)複合年成長率為7.31%。

政府主導的資金投入、積極的私人投資以及促進技術自主的政策指導,使該行業成為戰略重點。國內晶圓代工廠產能的快速提升、3D NAND和先進封裝技術的突破,以及5G、人工智慧和新能源汽車領域日益成長的需求,都為這一擴張提供了支撐。儘管對極紫外光刻(EUV)設備的嚴格出口限制減緩了向10奈米以下節點的過渡,但各公司正致力於最佳化成熟節點、化合物半導體以及繞過EUV的新架構。競爭壓力正在推動產業整合,例如EDA領域Empyrean和Xpeedic的合併以及長江儲存的資金籌措。這些都顯示了產業發展趨勢,即規模化、垂直整合和智慧財產權累積。

中國半導體裝置市場趨勢與洞察

基於「中國製造2025」策略,加速積體電路產能擴張計劃

中國計劃在2024年將晶圓代工產能擴大15%,並計劃在2025年進一步增產14%,屆時中芯國際、華虹半導體和Nexchip等廠商將加強其在成熟節點上的生產線。國產化進程如今已從製造流程擴展到光阻劑剝離和濕式清洗設備,國內供應商的採用率也相當高。預計2027年,中國將佔全球28nm晶圓產能的31%,重塑成熟節點的價格格局。該計劃的成功取決於穩定的電力供應、程式工程人才以及能夠降低出口限制風險的備用設備生產線。總而言之,這項發展將鞏固國內消費電子、工業電子和汽車電子的供應,從而提升整個生態系統的運轉率和獲利能力。

中國一級雲端服務供應商對以人工智慧為中心的邊緣運算的需求

阿里巴巴承諾2025年至2027年間投資3,800億元人民幣(約529億美元)用於人工智慧雲端基礎建設,騰訊和百度也宣布了類似的投資計畫。市場需求推動了GPU、高頻寬記憶體和網路交換器專用積體電路(ASIC)的訂單成長,進而帶動了本土晶圓廠和記憶體製造商的訂單。 DeepSeek的基礎模式展現了中國軟硬體整合的能力,降低了對海外加速器的依賴。邊緣人工智慧工作負載更傾向於低延遲的本地運算,因此買家傾向於選擇符合國家資料主權法規的國產SoC。由此可見,超大規模資料中心業者資料中心資本投資與晶片級創新之間的良性循環將成為中期成長的主要驅動力。

美國出口管制實體清單中關於EUV和EDA工具的規定

美國於2024年10月和12月生效的法規禁止向中國半導體工廠出口極紫外光刻機、先進沉積設備和高階EDA許可證。國內製造商的量產仍停留在28nm工藝,必須在沒有ASML EUV設備的情況下進行7nm製程的概念驗證(PoC)晶圓開發。目前可行的替代方案包括測試閘極長度為1nm的2D材料電晶體和先進的深紫外線多重圖形化,但商業性良率仍需數年時間才能實現。更長的設備前置作業時間、軟體許可的不確定性以及合規性審計等因素都減緩了製程節點升級的步伐。

細分市場分析

預計到2025年,積體電路將佔半導體銷售額的86.02%,並且由於人工智慧、5G和伺服器需求的推動,對晶片尺寸和堆疊式V-cache解決方案的需求不斷成長,其佔有率預計還將略有上升。在中國半導體市場,積體電路正以8.02%的複合年成長率成長,預計到2031年新增產值將超過692億美元。長江儲存的232層3D NAND快閃記憶體和長江儲存的DDR5 80%良率凸顯了記憶體領域的強勁發展勢頭,而中芯國際的12吋晶片生產線在強勁的消費和工業需求支撐下,維持了89.6%的運轉率。

分離式功率裝置、光電子裝置和感測器合計佔據剩餘的13.98%市場佔有率,受益於新能源汽車的電氣化以及5G對光元件日益成長的需求。國內碳化矽二極體產能每18個月加倍,用於智慧型手機3D感測的垂直腔面發射雷射(VCSEL)的出貨量也正轉向國內晶圓廠。儘管這些類別在以金額為準小規模,但它們在汽車安全、智慧工廠部署和擴增實境/虛擬實境(AR/VR)硬體領域卻是關鍵的差異化因素,有助於提升多個產業的韌性。

中國半導體裝置市場按元件類型(離散半導體[二極體、電晶體等]、光電子元件[LED、雷射二極體等]、感測器和MEMS[壓力感測器、執行器等]、積體電路)、經營模式模式(IDM、設計/無晶圓廠供應商)和最終用戶進行細分、汽車、通訊、

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 「中國製造2025」積體電路生產擴張計畫正在加速推進。

- 中國主要雲端服務供應商對以人工智慧為中心的邊緣運算的需求

- 在新能源動力傳動系統中採用車用級SiC/GaN

- 日本 5G 基地台的發展正在推動射頻前端積體電路的需求成長。

- 工業4.0:從先進工業化到智慧工廠

- 疫情後AIoT賦能消費性設備(智慧穿戴設備、AR/VR)的復甦

- 市場限制因素

- 美國出口管制實體清單中關於EUV和EDA工具的規定

- 人才流向海外設計公司

- 高電力消耗量製造實驗室面臨碳排放配額上限的問題。

- 300mm優質晶圓價格持續波動

- 產業價值鏈分析

- 監理展望

- 科技趨勢

- 波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭強度

- 宏觀經濟因素影響評估

- 半導體代工市場趨勢

- 代工廠收入和市場佔有率(按公司分類)

- IDM 與無晶圓廠銷售

- 亞太地區晶圓產能(依晶圓廠位置分類)

第5章 市場規模與成長預測

- 依設備類型(按設備類型分類的出貨量為補充資料)。

- 離散半導體

- 二極體

- 電晶體

- 功率電晶體

- 整流器和閘流體

- 其他分立元件

- 光電子學

- 發光二極體(LED)

- 雷射二極體

- 影像感測器

- 歐普託卡普拉

- 其他設備類型

- 感測器和微機電系統

- 壓力

- 磁場

- 執行器

- 加速度和偏航率

- 溫度和其他

- 積體電路

- 依積體電路類型

- 模擬

- 微

- 微處理器(MPU)

- 微控制器(MCU)

- 數位訊號處理器

- 邏輯

- 記憶

- 按技術節點(不適用出貨數量)

- 小於3奈米

- 3nm

- 5nm

- 7nm

- 16nm

- 28nm

- 大於28奈米

- 依積體電路類型

- 離散半導體

- 按經營模式

- IDM

- 設計/無晶圓廠供應商

- 按最終用戶行業分類

- 車

- 通訊(有線和無線)

- 消費者使用

- 工業的

- 計算/數據存儲

- 資料中心

- AI

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Semiconductor Manufacturing International Corp(SMIC)

- Taiwan Semiconductor Manufacturing Co(TSMC)

- Hua Hong Group

- Intel Corp

- Samsung Electronics Co Ltd

- SK Hynix Inc

- Micron Technology Inc

- Yangtze Memory Technologies Co(YMTC)

- JCET Group Co Ltd

- Advanced Micro Devices Inc

- Qualcomm Inc

- Broadcom Inc

- Nvidia Corp

- NXP Semiconductors NV

- Infineon Technologies AG

- STMicroelectronics NV

- Texas Instruments Inc

- Will Semiconductor Co Ltd

- Goodix Technology

- ASE Technology Holding Co

- Renesas Electronics Corp

- Rohm Co Ltd

第7章 市場機會與未來展望

The China semiconductor device market size was valued at USD 217.55 billion in 2025 and estimated to grow from USD 233.46 billion in 2026 to reach USD 332.17 billion by 2031, at a CAGR of 7.31% during the forecast period (2026-2031).

State-directed funding, vigorous private investment, and a policy mandate for technological self-sufficiency have turned the industry into a strategic priority. Rapid capacity additions at domestic foundries, breakthroughs in 3D NAND and advanced packaging, and rising demand from 5G, AI, and new-energy vehicles underpin the expansion. Tight export controls on extreme-ultraviolet (EUV) tools have slowed the migration to sub-10 nm nodes; yet, firms have redirected their efforts toward improving mature-node efficiency, compound semiconductors, and novel architectures that bypass EUV. Competitive pressure has led to increased consolidation, as exemplified by Empyrean-Xpeedic in EDA and YMTC's funding round, illustrating a trend toward scale, vertical integration, and IP accumulation.

China Semiconductor Device Market Trends and Insights

Accelerated "Made-in-China 2025" IC Capacity Expansion Programs

China expanded foundry capacity by 15% in 2024 and is scheduled to add another 14% in 2025 as SMIC, Huahong, and Nexchip ramp mature-node lines. Localization now stretches beyond fabrication to photoresist stripping and wet-clean tools, where domestic suppliers have achieved high usage rates. By 2027, China is projected to hold 31% of global 28 nm capacity, reshaping pricing at mature nodes. The program's success hinges on stable power, process-engineering talent, and second-source equipment lines that mitigate export-control exposure. Taken together, the rollout cements domestic supply for consumer, industrial, and automotive electronics, lifting utilization rates and margins across the ecosystem.

AI-Centric Edge-Computing Demand from Tier-1 Chinese Cloud Providers

Alibaba pledged CNY 380 billion (USD 52.9 billion) over 2025-2027 for AI-ready cloud infrastructure, while Tencent and Baidu announced comparable outlays. Demand spans GPUs, high-bandwidth memory, and network switch ASICs, channeling orders to local fabs and memory houses. DeepSeek's foundation model showcases China's ability to align software and hardware, easing reliance on foreign accelerators. Edge-AI workloads favor low-latency, on-premise compute, steering buyers toward domestically designed SOCs that comply with national data-sovereignty rules. The virtuous loop between hyperscaler capex and chip-level innovation is therefore a prime mid-term growth catalyst.

US Export-Control Entity-List Restrictions on EUV and EDA Tools

Washington's October 2024 and December 2024 rules bar shipment of EUV scanners, advanced deposition gear, and high-end EDA licenses to Chinese fabs. Domestic producers remain confined to 28 nm for mass production and must innovate around 7 nm proof-of-concept wafers without ASML EUV. Work-arounds include 2D-material transistors piloted at 1 nm gate length and advanced DUV multiple-patterning, but commercial yields are years away. Longer equipment lead-times, software license uncertainty, and compliance audits dampen the pace of node migration.

Other drivers and restraints analyzed in the detailed report include:

- Automotive-Grade SiC/GaN Adoption in NEV Powertrains

- National 5G Base-Station Build-Out Driving RF Front-End IC Uptake

- Talent Drain to Overseas Design Houses

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Integrated circuits accounted for 86.02% revenue in 2025, and their share is forecast to edge higher as AI, 5G, and server demand require larger die sizes and stacked V-cache solutions. Within the Chinese semiconductor market, integrated circuits are expected to expand at an 8.02% CAGR, adding more than USD 69.2 billion in new output by 2031. YMTC's 232-layer 3D NAND and CXMT's 80% DDR5 yield underscore momentum in memory, while SMIC's 12-inch lines run at 89.6% utilization on robust consumer and industrial demand.

Discrete power devices, optoelectronics, and sensors together occupy the remaining 13.98% share but are benefiting from NEV electrification and 5G optical-component pull. Domestic SiC diode capacity is doubling every 18 months, and VCSEL shipments for 3D sensing in smartphones are moving to local fabs. Although smaller in value, these categories contribute critical differentiation in automotive safety, smart-factory deployments, and AR/VR hardware, sustaining multi-segment resilience.

China Semiconductor Device Market is Segmented by Device Type (Discrete Semiconductors [Diodes, Transistors, and More], Optoelectronics [LEDs, Laser Diodes, and More], Sensors and MEMS [Pressure, Actuators, and More], and Integrated Circuits), Business Model (IDM, and Design/ Fabless Vendor), and End-Use Industry (Automotive, Communication, Consumer, Industrial, Computing/Data Storage, Data Center, AI, and Government).

List of Companies Covered in this Report:

- Semiconductor Manufacturing International Corp (SMIC)

- Taiwan Semiconductor Manufacturing Co (TSMC)

- Hua Hong Group

- Intel Corp

- Samsung Electronics Co Ltd

- SK Hynix Inc

- Micron Technology Inc

- Yangtze Memory Technologies Co (YMTC)

- JCET Group Co Ltd

- Advanced Micro Devices Inc

- Qualcomm Inc

- Broadcom Inc

- Nvidia Corp

- NXP Semiconductors NV

- Infineon Technologies AG

- STMicroelectronics NV

- Texas Instruments Inc

- Will Semiconductor Co Ltd

- Goodix Technology

- ASE Technology Holding Co

- Renesas Electronics Corp

- Rohm Co Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated "Made-in-China 2025" IC Capacity Expansion Programs

- 4.2.2 AI-centric Edge-Computing Demand from Tier-1 Chinese Cloud Providers

- 4.2.3 Automotive-grade SiC/GaN Adoption in NEV Powertrains

- 4.2.4 National 5G Base-station Build-out Driving RF-Front-End IC Uptake

- 4.2.5 Industrial Upgrade to "Industry 4.0" Smart-Factories

- 4.2.6 Post-pandemic rebound of AIoT-enabled consumer devices (smart wearables, AR/VR)

- 4.3 Market Restraints

- 4.3.1 US Export-control Entity-List Restrictions on EUV and EDA Tools

- 4.3.2 Talent Drain to Overseas Design Houses

- 4.3.3 Electricity-Intensive Fabs Facing Provincial Carbon-Quota Caps

- 4.3.4 Persistent Price Volatility of 300 mm Prime Wafers

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Trends

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

- 4.8 Impact Assessment of Macroeconomic Factors

- 4.9 Semiconductor Foundry Landscape

- 4.9.1 Foundry Revenue and Share by Players

- 4.9.2 IDM vs Fabless Sales

- 4.9.3 Installed Wafer Capacity (by Fab Location)

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Device Type (Shipment Volume for Device Type is Complementary)

- 5.1.1 Discrete Semiconductors

- 5.1.1.1 Diodes

- 5.1.1.2 Transistors

- 5.1.1.3 Power Transistors

- 5.1.1.4 Rectifier and Thyristor

- 5.1.1.5 Other Discrete Devices

- 5.1.2 Optoelectronics

- 5.1.2.1 Light-Emitting Diodes (LEDs)

- 5.1.2.2 Laser Diodes

- 5.1.2.3 Image Sensors

- 5.1.2.4 Optocouplers

- 5.1.2.5 Other Device Types

- 5.1.3 Sensors and MEMS

- 5.1.3.1 Pressure

- 5.1.3.2 Magnetic Field

- 5.1.3.3 Actuators

- 5.1.3.4 Acceleration and Yaw Rate

- 5.1.3.5 Temperature and Others

- 5.1.4 Integrated Circuits

- 5.1.4.1 By Integrated Circuit Type

- 5.1.4.1.1 Analog

- 5.1.4.1.2 Micro

- 5.1.4.1.2.1 Microprocessors (MPU)

- 5.1.4.1.2.2 Microcontrollers (MCU)

- 5.1.4.1.2.3 Digital Signal Processors

- 5.1.4.1.3 Logic

- 5.1.4.1.4 Memory

- 5.1.4.2 By Technology Node (Shipment Volume Not Applicable)

- 5.1.4.2.1 < 3nm

- 5.1.4.2.2 3nm

- 5.1.4.2.3 5nm

- 5.1.4.2.4 7nm

- 5.1.4.2.5 16nm

- 5.1.4.2.6 28nm

- 5.1.4.2.7 > 28nm

- 5.1.4.1 By Integrated Circuit Type

- 5.1.1 Discrete Semiconductors

- 5.2 By Business Model

- 5.2.1 IDM

- 5.2.2 Design/ Fabless Vendor

- 5.3 By End-user Industry

- 5.3.1 Automotive

- 5.3.2 Communication (Wired and Wireless)

- 5.3.3 Consumer

- 5.3.4 Industrial

- 5.3.5 Computing/Data Storage

- 5.3.6 Data Center

- 5.3.7 AI

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Semiconductor Manufacturing International Corp (SMIC)

- 6.4.2 Taiwan Semiconductor Manufacturing Co (TSMC)

- 6.4.3 Hua Hong Group

- 6.4.4 Intel Corp

- 6.4.5 Samsung Electronics Co Ltd

- 6.4.6 SK Hynix Inc

- 6.4.7 Micron Technology Inc

- 6.4.8 Yangtze Memory Technologies Co (YMTC)

- 6.4.9 JCET Group Co Ltd

- 6.4.10 Advanced Micro Devices Inc

- 6.4.11 Qualcomm Inc

- 6.4.12 Broadcom Inc

- 6.4.13 Nvidia Corp

- 6.4.14 NXP Semiconductors NV

- 6.4.15 Infineon Technologies AG

- 6.4.16 STMicroelectronics NV

- 6.4.17 Texas Instruments Inc

- 6.4.18 Will Semiconductor Co Ltd

- 6.4.19 Goodix Technology

- 6.4.20 ASE Technology Holding Co

- 6.4.21 Renesas Electronics Corp

- 6.4.22 Rohm Co Ltd

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

半導體拆解服務市場:全球市場預測,2026-2032年

半導體拆解服務市場:全球市場預測,2026-2032年 用於加工應用的半導體裝置:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

用於加工應用的半導體裝置:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 光敏半導體元件市場:依元件、材料、應用、工作模式、最終用戶、國家及地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測半導體裝置:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)

光敏半導體元件市場:依元件、材料、應用、工作模式、最終用戶、國家及地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測半導體裝置:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030) 半導體環境感測器市場分析與預測(至2035年):類型、產品類型、技術、組件、應用、材料類型、最終用戶、功能、安裝方式、解決方案低功耗半導體雷達系統市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、設備、部署類型、最終用戶及功能分類光敏半導體紋身市場分析及預測(至2035年):按類型、產品、服務、技術、應用、材料類型、裝置、製程、最終用戶和功能分類半導體電化學電池市場分析及預測(至2035年):依類型、產品類型、技術、組件、應用、材料類型、製程、最終用戶、功能、安裝類型分類

半導體環境感測器市場分析與預測(至2035年):類型、產品類型、技術、組件、應用、材料類型、最終用戶、功能、安裝方式、解決方案低功耗半導體雷達系統市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、設備、部署類型、最終用戶及功能分類光敏半導體紋身市場分析及預測(至2035年):按類型、產品、服務、技術、應用、材料類型、裝置、製程、最終用戶和功能分類半導體電化學電池市場分析及預測(至2035年):依類型、產品類型、技術、組件、應用、材料類型、製程、最終用戶、功能、安裝類型分類 2026年全球工業半導體市場報告

2026年全球工業半導體市場報告 2026-2030年全球光學半導體元件市場

2026-2030年全球光學半導體元件市場