|

市場調查報告書

商品編碼

1940854

越南建設化學品:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Vietnam Construction Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

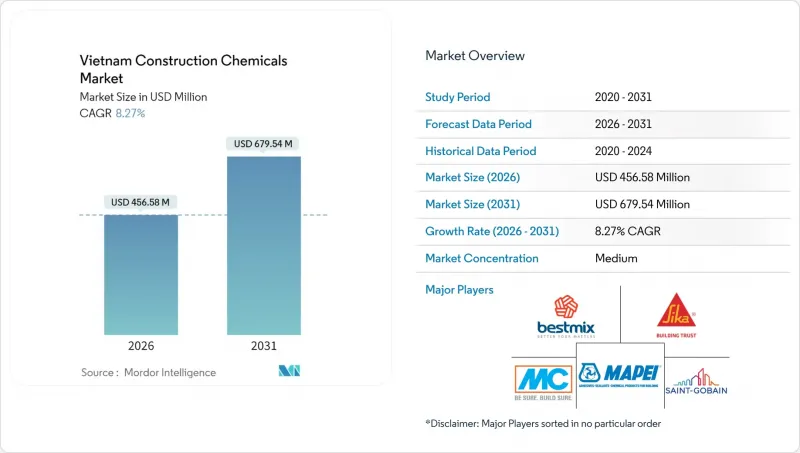

預計到 2026 年,越南建築化學品市場規模將達到 4.5658 億美元。

這代表著從 2025 年的 4.2171 億美元成長到 2031 年的 6.7954 億美元,2026 年至 2031 年的複合年成長率為 8.27%。

政府791兆越南盾公共投資計畫下的強勁基礎建設支出,加上2024年預計231.5億美元的外國直接投資流入,共同支撐了對高性能化學配方的持續需求。開發人員正在尋求防水耐用的解決方案以應對越南的季風氣候,同時,隨著越南力爭在2050年實現淨零排放,低碳混凝土外加劑的應用也日益廣泛。承包商正在採用數位化稱重設備,將材料浪費減少高達20%,從而拉大了優質產品與一般產品之間的性能差距。同時,第10/2024/TT-BXD號通知強化了品質標準,提高了不合格供應商的進入門檻。

越南建設化學品市場趨勢及洞察

基礎建設主導公共部門支出激增

2025年正式核准的670億美元公共投資正重新分配資金用於機場、港口、地鐵和高速公路建設。混凝土用量巨大、計劃工期緊張,以及基於TCVN和QCVN標準的嚴格品管,促使建築公司採用高性能減水劑、快乾修補砂漿和防腐蝕塗料。擁有準時物流和現場技術支援良好記錄的供應商已報告2026年訂單兩位數。因此,越南建設化學品市場與優先採用國際標準材料的國家資本支出計畫直接相關。

外資產業園區的快速擴張

預計2024年,越南實際外商直接投資(FDI)將達216.8億美元,2030年計畫新建221個工業園區。新加坡、中國和韓國的電子產品、電池和半導體製造商需要防靜電地板材料、耐化學腐蝕的襯裡和防潮水泥漿來維持GMP認證。每個新的VSIP專案階段都會消耗1.5萬至2萬噸的添加劑、密封劑和地板塗料。提案符合ISO 14644無塵室標準的配方的產品經理正在將詢價轉化為多年供應協議,這鞏固了越南建設化學品市場到2030年的成長趨勢。

水泥和石化原料價格波動

2024年原油價格上漲時,PVC樹脂價格在三個月內飆升了15%至20%。水泥運轉率從2022年的58%下降到2023年的55%。水泥熟料出口稅擠壓了生產商的利潤空間,迫使外加劑配方生產商每季重新談判價格。由於庫存緩衝不足,越南建設化學品市場的小規模品牌受到的衝擊最大,它們通常會推遲創新投資,直到成本曲線穩定下來。

細分市場分析

至2025年,防水解決方案將佔越南建設化學品市場45.02%的佔有率。在胡志明市,海拔3公尺以下的地下室指定使用高回彈防水卷材。由於自動噴塗設備和品質保證感測器的廣泛應用,表面處理化學品預計將以8.41%的複合年成長率成長,超過越南建設化學品市場的整體成長速度。

承包商擴大將矽烷/矽氧烷防水劑與奈米二氧化矽密封劑結合使用,以實現兩位數的吸水率降低。混凝土外加劑對於公路梁至關重要,其中高效減水劑的使用可確保即使在中部沿海地區常見的35°C以上的施工溫度下也能保持坍落度。 1號國道沿線的老舊橋樑需要使用耐氯砂漿,推動了對修補組合藥物的需求。地板樹脂,特別是防靜電環氧樹脂,正在河內北部電子產業叢集中佔據一席之地,其產品範圍已不再局限於傳統的以水泥為中心的產品。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 基礎建設主導公共部門支出激增

- 外資產業園區的快速擴張

- 引入低碳混凝土外加劑

- 數位化現場稱重和品質保證系統

- 循環經濟對米糠灰奈米二氧化矽的需求

- 市場限制

- 水泥和石化原料價格波動

- 分散的承包商採購做法

- 國家產品標準協調統一進程緩慢

- 價值鏈分析

- 監管環境

- 波特五力模型

- 競爭對手之間的競爭

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

第5章 市場規模與成長預測

- 依產品

- 黏合劑

- 熱熔膠

- 反應性

- 溶劑型

- 水溶液

- 錨栓和水泥漿

- 水泥基固定劑

- 樹脂固定

- 混凝土外加劑

- 加速器

- 空氣引射器

- 高效減水劑

- 緩速器

- 收縮抑制劑

- 黏度調節劑

- 塑化劑

- 其他

- 混凝土保護塗層

- 丙烯酸纖維

- 醇酸樹脂

- 環氧樹脂

- 聚氨酯

- 其他樹脂

- 地板樹脂

- 丙烯酸纖維

- 環氧樹脂

- 聚天門冬胺酸樹脂

- 聚氨酯

- 其他樹脂

- 修復和修復化學品

- 纖維纏繞系統

- 壓漿

- 微型混凝土砂漿

- 改質砂漿

- 鋼筋保護材料

- 密封劑

- 丙烯酸纖維

- 環氧樹脂

- 聚氨酯

- 矽酮

- 其他樹脂

- 表面處理化學品

- 固化劑

- 釋放劑

- 其他

- 防水解決方案

- 化學品

- 防水膜

- 黏合劑

- 按最終用戶類別

- 商業的

- 工業和公共設施

- 基礎設施

- 住宅

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率**(%)/排名分析

- 公司簡介

- Adchem Construction Chemical(Berry Global Inc.)

- BESTMIX

- GPS Vietnam

- MAPEI SpA

- MC-Bauchemie

- Saint-Gobain

- Schomburg

- Sika AG

- Thermax Limited

- Arkema(Bostik)

- Henkel AG & Co. KGaA

第7章 市場機會與未來展望

- 閒置頻段與未滿足需求評估

第8章:執行長面臨的關鍵策略挑戰

Vietnam Construction Chemicals Market size in 2026 is estimated at USD 456.58 million, growing from 2025 value of USD 421.71 million with 2031 projections showing USD 679.54 million, growing at 8.27% CAGR over 2026-2031.

Robust infrastructure spending under the government's VND 791 trillion public investment plan, coupled with USD 23.15 billion of foreign direct investment (FDI) inflows in 2024, underpins sustained demand for high-performance chemical formulations. Developers are pursuing waterproofing and durability solutions to address Vietnam's monsoon climate, while low-carbon concrete admixtures are gaining traction as the country advances toward achieving net-zero status by 2050. Contractors are adopting digitalized dosing equipment that cuts material waste by up to 20%, widening the performance gap between premium and commodity offerings. Meanwhile, Circular 10/2024/TT-BXD tightens quality standards, elevating entry barriers for non-compliant suppliers.

Vietnam Construction Chemicals Market Trends and Insights

Infrastructure-led Public-Sector Spending Surge

Public investment officially approved at USD 67 billion for 2025 is redirecting cash toward airports, seaports, metros, and expressways. Large concrete volumes, rigid project-delivery schedules, and tighter quality control standards under TCVN and QCVN codes are incentivizing contractors to specify high-range water reducers, rapid-set repair mortars, and corrosion-inhibiting coatings. Suppliers with a track record of on-time logistics and job-site technical support already report double-digit order backlogs for 2026. The Vietnam construction chemicals market, therefore, links directly to state capital expenditure plans that favor global-standard materials.

Rapid Expansion of Foreign-Invested Industrial

Realized FDI hit USD 21.68 billion in 2024, and 221 additional industrial parks are scheduled before 2030. Singaporean, Chinese, and Korean manufacturers building electronics, batteries, and semiconductors require antistatic floors, chemical-resistant linings, and moisture-tolerant grouts that preserve GMP certifications. Each new VSIP phase consumes 15,000-20,000 tons of admixtures, sealers, and floor toppings. Product managers that align formulations with ISO 14644 clean-room norms are converting inquiries into multi-year supply contracts, reinforcing upside for the Vietnam construction chemicals market through 2030.

Volatile Cement and Petro-Chemical Feedstock Prices

PVC resin spiked 15-20% within three months when crude oil rose in 2024. Cement utilization dipped from 58% in 2022 to 55% in 2023. Clinker export taxes trimmed producer margins, forcing admixture formulators to renegotiate quarterly prices. Smaller brands in the Vietnam construction chemicals market with low inventory buffers absorb the greatest shocks, often delaying innovation spending until cost curves stabilize.

Other drivers and restraints analyzed in the detailed report include:

- Adoption of Low-Carbon Concrete Admixtures

- Digitalized Job-Site Dosing and QA Systems

- Fragmented Contractor Purchasing Practices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Waterproofing solutions held 45.02% of the Vietnam construction chemicals market share in 2025, with high-elasticity membranes specified for basements built three meters below sea level in Ho Chi Minh City. Surface-treatment chemicals, helped by automated sprayers and QA sensors, are set to outpace the broader Vietnam construction chemicals market at an 8.41% CAGR.

Contractors increasingly pair silane-siloxane repellents with nano-silica sealers to achieve double-digit reductions in water absorption. Concrete admixtures remain indispensable for expressway girders; super-plasticizers ensure slump retention under 35°C site temperatures common along the central coast. Repair formulations grow as aging bridges along National Route 1 require chloride-resistant mortars. Flooring resins, especially ESD-safe epoxies, move into electronics clusters north of Hanoi, signaling diversification beyond legacy cement-centric products.

The Vietnam Construction Chemicals Market Report is Segmented by Product (Adhesives, Anchors and Grouts, Concrete Admixtures, Concrete Protective Coatings, Flooring Resins, Repair and Rehabilitation Chemicals, Sealants, Surface-Treatment Chemicals, Waterproofing Solutions) and End-User Sector (Commercial, Industrial and Institutional, Infrastructure, Residential). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Adchem Construction Chemical (Berry Global Inc.)

- BESTMIX

- GPS Vietnam

- MAPEI S.p.A

- MC-Bauchemie

- Saint-Gobain

- Schomburg

- Sika AG

- Thermax Limited

- Arkema (Bostik)

- Henkel AG & Co. KGaA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Infrastructure-led public-sector spending surge

- 4.2.2 Rapid expansion of foreign-invested industrial parks

- 4.2.3 Adoption of low-carbon concrete admixtures

- 4.2.4 Digitalised job-site dosing and QA systems

- 4.2.5 Circular-economy demand for rice-husk-ash nano-silica

- 4.3 Market Restraints

- 4.3.1 Volatile cement and petro-chemical feedstock prices

- 4.3.2 Fragmented contractor purchasing practices

- 4.3.3 Slow harmonisation of national product standards

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Competitive Rivalry

- 4.6.2 Threat of New Entrants

- 4.6.3 Bargaining Power - Suppliers

- 4.6.4 Bargaining Power - Buyers

- 4.6.5 Threat of Substitutes

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product

- 5.1.1 Adhesives

- 5.1.1.1 Hot-Melt

- 5.1.1.2 Reactive

- 5.1.1.3 Solvent-borne

- 5.1.1.4 Water-borne

- 5.1.2 Anchors and Grouts

- 5.1.2.1 Cementitious Fixing

- 5.1.2.2 Resin Fixing

- 5.1.3 Concrete Admixtures

- 5.1.3.1 Accelerator

- 5.1.3.2 Air-Entraining

- 5.1.3.3 Super-plasticizer

- 5.1.3.4 Retarder

- 5.1.3.5 Shrinkage-Reducer

- 5.1.3.6 Viscosity-Modifier

- 5.1.3.7 Plasticizer

- 5.1.3.8 Other Types

- 5.1.4 Concrete Protective Coatings

- 5.1.4.1 Acrylic

- 5.1.4.2 Alkyd

- 5.1.4.3 Epoxy

- 5.1.4.4 Polyurethane

- 5.1.4.5 Other Resins

- 5.1.5 Flooring Resins

- 5.1.5.1 Acrylic

- 5.1.5.2 Epoxy

- 5.1.5.3 Polyaspartic

- 5.1.5.4 Polyurethane

- 5.1.5.5 Other Resins

- 5.1.6 Repair and Rehabilitation Chemicals

- 5.1.6.1 Fiber-Wrapping Systems

- 5.1.6.2 Injection Grouting

- 5.1.6.3 Micro-concrete Mortars

- 5.1.6.4 Modified Mortars

- 5.1.6.5 Rebar Protectors

- 5.1.7 Sealants

- 5.1.7.1 Acrylic

- 5.1.7.2 Epoxy

- 5.1.7.3 Polyurethane

- 5.1.7.4 Silicone

- 5.1.7.5 Other Resins

- 5.1.8 Surface-Treatment Chemicals

- 5.1.8.1 Curing Compounds

- 5.1.8.2 Mold-Release Agents

- 5.1.8.3 Other Types

- 5.1.9 Waterproofing Solutions

- 5.1.9.1 Chemicals

- 5.1.9.2 Membranes

- 5.1.1 Adhesives

- 5.2 By End-User Sector

- 5.2.1 Commercial

- 5.2.2 Industrial and Institutional

- 5.2.3 Infrastructure

- 5.2.4 Residential

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share**(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Adchem Construction Chemical (Berry Global Inc.)

- 6.4.2 BESTMIX

- 6.4.3 GPS Vietnam

- 6.4.4 MAPEI S.p.A

- 6.4.5 MC-Bauchemie

- 6.4.6 Saint-Gobain

- 6.4.7 Schomburg

- 6.4.8 Sika AG

- 6.4.9 Thermax Limited

- 6.4.10 Arkema (Bostik)

- 6.4.11 Henkel AG & Co. KGaA

7 Market Opportunities Future Outlook

- 7.1 White-space and Unmet-need Assessment

8 Key Strategic Questions for CEOs

固定式機械錨栓市場:依產品類型、材料、應用、終端用戶產業及通路分類,全球預測,2026-2032年

固定式機械錨栓市場:依產品類型、材料、應用、終端用戶產業及通路分類,全球預測,2026-2032年 建築化學品市場分析及預測(至2035年):類型、產品、應用、形態、材質類型、技術、最終用戶、功能、安裝類型、解決方案

建築化學品市場分析及預測(至2035年):類型、產品、應用、形態、材質類型、技術、最終用戶、功能、安裝類型、解決方案 建築化學品:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)歐洲建設化學品:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)美國建設化學品:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

建築化學品:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)歐洲建設化學品:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)美國建設化學品:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 全球建築化學品市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球建築化學品市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 建築化學品市場規模、佔有率、趨勢及預測(按類型、應用和地區分類)(2026-2034 年)

建築化學品市場規模、佔有率、趨勢及預測(按類型、應用和地區分類)(2026-2034 年) 2026年全球建築化學品市場報告

2026年全球建築化學品市場報告 建築化學品市場-全球產業規模、佔有率、趨勢、機會及預測(2021-2031 年)(依產品類型、應用、地區及競爭格局分類)中東建築化學品市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)

建築化學品市場-全球產業規模、佔有率、趨勢、機會及預測(2021-2031 年)(依產品類型、應用、地區及競爭格局分類)中東建築化學品市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)