|

市場調查報告書

商品編碼

1940797

美國IT服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)United States (US) IT Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

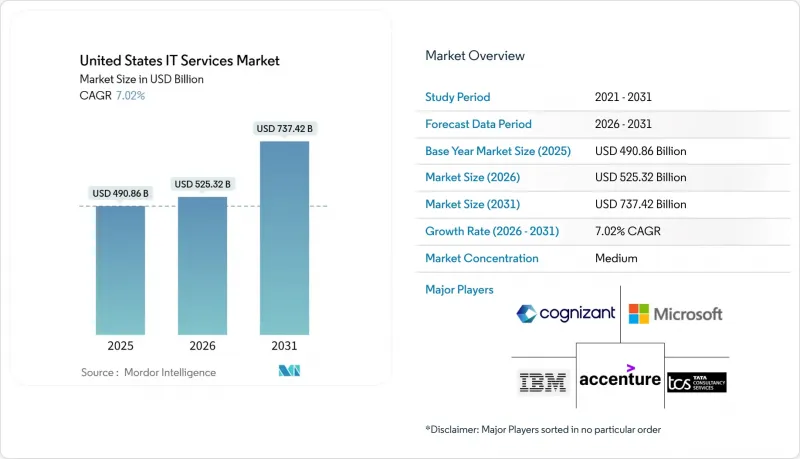

據估計,美國 IT 服務市場在 2026 年的價值將達到 5,253.2 億美元,高於 2025 年的 4,908.6 億美元,預計到 2031 年將達到 7,374.2 億美元。

預計 2026 年至 2031 年的複合年成長率為 7.02%。

生成式人工智慧已成為企業技術預算的首要驅動力,聯邦政府為安全雲端遷移、5G邊緣部署和零信任架構提供的獎勵進一步推動了這一趨勢。美國IT服務市場也受益於強勁的企業現金流以及公共和私營機構向基於消費的營運模式的快速轉型。競爭依然激烈,隨著全球系統整合商不斷收購專業利基公司以獲取人才和專有人工智慧平台,供應商整合正在加劇。區域趨勢也使情況更加複雜:雖然西部地區主導,但南部地區的擴張速度最快,新的資料中心走廊正在湧現,以滿足不斷成長的人工智慧工作負載需求。

美國IT服務市場趨勢與洞察

聯邦獎勵加速了美國公共部門的雲端遷移。

聯邦機構宣佈在2024會計年度上半年簽訂價值130億美元的新IT服務契約,而2025會計年度民事機構預算為技術領域撥款751.3億美元,其中16.4%用於網路安全。一項兩黨共同提出的提案呼籲為人工智慧舉措追加320億美元,這將為獲得FedRAMP授權的雲端和安全供應商拓展更多機會。 14028號行政命令作為合規基礎,強制所有機構採用安全雲端技術。總部位於華盛頓特區、維吉尼亞和馬裡蘭州的服務合作夥伴已開始擴大其交付中心,以抓住快速成長的公共部門業務。

財富 1000 強企業大規模部署生成式人工智慧

到2025年中期,預計近半數財富1000強企業將把生成式人工智慧融入其核心業務流程,隨著執行長將企業級部署列為優先事項,這一比例預計將呈指數級成長。預計到2025年,年度人工智慧預算平均將成長14%,支出將主要集中在資料工程基礎、管治模型和負責任的人工智慧管理方面。因此,美國IT服務市場對雲端平台重構、LLM調優和模型維運管理服務的需求創下歷史新高,尤其是在東北走廊的金融中心和西海岸的創新叢集。

高級雲端安全人才短缺

美國雇主普遍反映雲端架構師和高階安全工程師長期短缺,人才缺口限制了計劃能力,並推高了薪資水平。在西雅圖、奧斯汀和北維吉尼亞等科技叢集,這種壓力尤其突出,因為超大規模資料中心業者和顧問公司都在爭奪同一批高階人才。實施零信任框架的政府機構發現,其薪資水準難以與私部門匹敵,因此開始使用人員外包公司,這些公司將國內領導力與近岸交付能力結合。目前,一些服務供應商正在部署基於人工智慧的招募工具,以加快候選人篩檢並縮小職缺。

細分市場分析

到2025年,託管服務將占美國IT服務市場27.85%的佔有率,主要得益於企業將營運職能外包,並將稀缺人才集中於差異化創新。混合基礎設施日益複雜以及持續存在的網路威脅,推動了對完全託管的可觀測性、修補程式和合規性服務的需求。服務提供者將捆綁式託管服務定位為增值轉型計劃的墊腳石,從而確保持續的收入來源和客戶留存。

雲端和平台服務是美國IT服務市場的成長引擎,預計2026年至2031年將以9.02%的複合年成長率成長。客戶正在加速在公共雲端基礎架構上直接進行大規模生成式人工智慧試點項目,而計量收費的經濟模式正在推動工作負載從私人資料中心遷移。服務合作夥伴正在擴展其認證雲端團隊和財務營運(FinOps)能力,以更好地管理支出。隨著傳統環境向微服務和無伺服器架構轉型,應用開發和維護服務持續保持顯著的交易量。同時,在監管審查力度加大以及董事會對現代化藍圖的重視下,網路安全和數位轉型諮詢服務也保持著強勁的交易動能。

截至2025年,美國IT服務市場中,本土交付將佔62.65%,反映出客戶對合規性、時區一致性和領域知識的偏好。美國本土的計費標準為每小時115美元至175美元,高技能顧問的薪酬較高,尤其是受監管產業。服務提供者透過將高價值的架構和管治工作集中在大都會圈,並將執行工作分散到成本較低的美國城市,來維持利潤率。

預計到2031年,近岸交付將以10.05%的複合年成長率成長,以滿足日益成長的對西班牙語和葡萄牙語敏捷團隊的需求,這些團隊能夠連接美國業務團隊和拉丁美洲的工程人才。採用「近岸+」模式的公司將解決方案架構師設在美國,並將開發業務擴展到墨西哥、哥倫比亞和哥斯大黎加,時薪穩定在85美元左右。雖然離岸交付仍然保持著成本優勢,但班加羅爾和馬尼拉等傳統離岸外包地點的工資上漲正在推動一些敏感工作選擇性地回流到美國。

美國IT服務市場按類型(IT諮詢/實施、應用開發與維護等)、部署模式(境內交付、近岸交付等)、合約類型(企劃為基礎/固定價格等)、組織規模(大型企業、中小企業)、最終用戶(銀行、金融服務和保險、製造業、政府等)以及地區進行細分。市場預測以美元計價。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 聯邦獎勵加速了美國公共部門的雲端遷移。

- 財富 1000 強企業大規模部署生成式人工智慧

- 5G和邊緣部署推動了對網路融合的需求

- 零信任網路安全要求驅動保全服務

- 醫療保健互通性規則促進電子健康記錄 (EHR) 整合服務

- 私募股權投資助力中型企業ERP現代化浪潮

- 市場限制

- 高級雲端安全人才短缺

- 基於績效的定價模式所帶來的利潤率壓力

- CCPA/CPRA訴訟中合規的複雜性

- 離岸工資上漲會削弱成本優勢。

- 價值/供應鏈分析

- 監理展望

- 技術展望

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 競爭程度

- 替代品的威脅

- 比較分析:一級供應商與二級供應商

- 內部開發與外包分析

- 投資分析

第5章 市場規模與成長預測

- 按服務類型

- IT諮詢與實施支持

- 應用開發與維護(ADM)

- 基礎設施服務

- 託管服務

- IT外包(ITO)

- 業務流程外包(BPO)

- 雲端和平台服務

- 保全服務

- 數位轉型與新興技術(人工智慧、物聯網、區塊鏈)

- 按部署模式

- 陸上交付

- 近岸交付

- 離岸交付

- 按合約模式

- 企劃為基礎/固定價格

- 人員增補/工時及材料法

- 管理式服務/結果導向型

- 按組織規模

- 主要企業

- 中小企業

- 按最終用戶行業分類

- 銀行、金融服務和保險(BFSI)

- 製造業

- 政府/公共部門

- 醫學與生命科學

- 零售和消費品

- 通訊與媒體

- 運輸/物流

- 能源與公共產業

- 其他

- 按地區

- 東北

- 中西部

- 南部

- 西

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Accenture plc

- IBM Corporation

- Cognizant Technology Solutions Corp.

- Tata Consultancy Services Ltd.

- Microsoft Corporation

- Infosys Ltd.

- Wipro Ltd.

- Deloitte Consulting LLP

- Capgemini SE

- HCL Technologies Ltd.

- CGI Inc.

- DXC Technology Co.

- Booz Allen Hamilton Inc.

- Leidos Holdings Inc.

- Atos SE

- EPAM Systems Inc.

- NTT DATA Services

- Kyndryl Holdings Inc.

- LTI Mindtree Ltd.

- Tech Mahindra Ltd.

- Slalom LLC

- Perficient Inc.

- ThoughtWorks Inc.

- Persistent Systems Ltd.

第7章 市場機會與未來展望

United States IT Services Market size in 2026 is estimated at USD 525.32 billion, growing from 2025 value of USD 490.86 billion with 2031 projections showing USD 737.42 billion, growing at 7.02% CAGR over 2026-2031.

Generative AI ranks as the single largest driver of enterprise technology budgets, while federal incentives for secure cloud migration, 5G-edge roll-outs, and zero-trust mandates supply additional tailwinds. The United States IT services market also benefits from resilient corporate cash flows and the rapid shift of both public and private organizations toward consumption-based operating models. Competition remains intense, yet vendor consolidation continues as global systems integrators acquire niche specialists to secure talent and proprietary AI platforms. Regional dynamics add another layer of complexity: the West retains leadership, but the South is scaling fastest as new data-center corridors emerge to meet surging AI workload demand.

United States (US) IT Services Market Trends and Insights

Federal Incentives Accelerating Cloud Migration in US Public Sector

Federal agencies announced USD 13 billion in new IT services contracts during H1 2024, and the civilian-agency budget for 2025 allocates USD 75.13 billion toward technology, 16.4% of which is earmarked for cybersecurity. A bipartisan proposal seeks an additional USD 32 billion for AI initiatives, widening opportunities for providers with FedRAMP-authorized cloud and security practices.Executive Order 14028 acts as the compliance backbone, mandating secure cloud adoption across agencies. Service partners positioned around Washington, DC, Virginia, and Maryland have begun expanding delivery centers to capture the rapidly growing public-sector pipeline.

Large-Scale Adoption of Generative AI among Fortune 1000

By mid-2025, nearly half of Fortune 1000 enterprises had embedded generative AI into core workflows, and the share is projected to climb sharply as CEOs prioritize enterprise-wide rollouts. Average annual AI budgets are set to rise 14% in 2025, concentrating spend on data-engineering foundations, governance models, and responsible AI controls.The United States IT services market is therefore witnessing record demand for cloud re-platforming, LLM tuning, and model-ops managed services, especially in financial centers along the Northeast corridor and innovation clusters on the West Coast.

Scarcity of Senior Cloud & Security Talent

Employers across the United States report persistent shortages of cloud architects and senior security engineers, a gap that limits project throughput and increases wage inflation. The pressure is fiercest in technology clusters such as Seattle, Austin, and Northern Virginia, where hyperscalers and consultancies compete for the same high-end talent pools. Agencies implementing zero-trust frameworks struggle to match private-sector compensation, encouraging heavier use of staff-augmentation firms that combine domestic leadership with nearshore delivery capacity. Several service providers now deploy AI-based sourcing tools to accelerate candidate screening and reduce vacancy gaps.

Other drivers and restraints analyzed in the detailed report include:

- 5G & Edge Roll-out Driving Network Integration Demand

- Zero-Trust Cybersecurity Mandates Boosting Security Services

- Margin Pressure from Outcome-Based Pricing Models

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Managed Services held 27.85% of the United States IT services market in 2025, driven by enterprises outsourcing run-and-operate functions to focus scarce talent on differentiating innovation. Hybrid-infrastructure complexity and relentless cyberthreats reinforce demand for fully managed observability, patching, and compliance services. Providers position bundled managed offerings as stepping stones to higher-value transformation engagements, ensuring annuity revenue streams and sticky client relationships.

Cloud & Platform Services, expanding at a 9.02% CAGR from 2026-2031, represents the growth engine of the United States IT services market. Clients accelerate large-scale generative-AI pilots directly onto public-cloud foundations, and consumption-based economics move more workloads off private data centers. Service partners, therefore, scale certified cloud squads and FinOps capabilities to control spend. Application Development & Maintenance services still secure sizable deal flow as legacy estates shift toward microservices and serverless paradigms. Meanwhile, cybersecurity and digital-transformation advisory maintain strong pipelines, given regulatory scrutiny and board-level prioritization of modernization road maps.

Onshore Delivery accounted for 62.65% of the United States IT services market size in 2025, reflecting client preference for regulatory compliance, timezone alignment, and domain knowledge. Domestic bill rates in the USD 115-175 per hour band reward deeply specialized consultants, especially in regulated industries. Providers sustain margin by concentrating high-touch architecture and governance roles in metropolitan hubs while dispersing execution to lower-cost U.S. cities.

Nearshore Delivery, forecast to grow 10.05% CAGR to 2031, meets rising demand for Spanish- and Portuguese-speaking agile pods that bridge U.S. business teams and Latin American engineering talent. Firms adopting a "Nearshore Plus" model base solution architects in the U.S. and scale development in Mexico, Colombia, and Costa Rica at blended rates near USD 85 per hour. Offshore delivery continues to supply cost leverage, but wage inflation in traditional hubs such as Bengaluru and Manila triggers selective reshoring of sensitive workloads.

The United States (US) IT Services is Segmented by Type (IT Consulting and Implementation, ADM, and More), Deployment Model (Onshore Delivery, Nearshore Delivery, and More), Engagement Model (Project-Based / Fixed Price, and More), Organization Size (Large Enterprises, Smes), End-User (BFSI, Manufacturing, Government, and More), and by Geography. The Market Forecasts are Provided in Terms of Value in USD.

List of Companies Covered in this Report:

- Accenture plc

- IBM Corporation

- Cognizant Technology Solutions Corp.

- Tata Consultancy Services Ltd.

- Microsoft Corporation

- Infosys Ltd.

- Wipro Ltd.

- Deloitte Consulting LLP

- Capgemini SE

- HCL Technologies Ltd.

- CGI Inc.

- DXC Technology Co.

- Booz Allen Hamilton Inc.

- Leidos Holdings Inc.

- Atos SE

- EPAM Systems Inc.

- NTT DATA Services

- Kyndryl Holdings Inc.

- LTI Mindtree Ltd.

- Tech Mahindra Ltd.

- Slalom LLC

- Perficient Inc.

- ThoughtWorks Inc.

- Persistent Systems Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Federal Incentives Accelerating Cloud Migration in US Public Sector

- 4.2.2 Large-scale Adoption of Generative AI among Fortune 1000

- 4.2.3 5G and Edge Roll-out Driving Network Integration Demand

- 4.2.4 Zero-Trust Cybersecurity Mandates Boosting Security Services

- 4.2.5 Healthcare Interoperability Rules Fueling EHR Integration Services

- 4.2.6 PE-Backed ERP Modernization Wave in Mid-Market Firms

- 4.3 Market Restraints

- 4.3.1 Scarcity of Senior Cloud and Security Talent

- 4.3.2 Margin Pressure from Outcome-Based Pricing Models

- 4.3.3 Compliance Complexity under CCPA/CPRA Litigation

- 4.3.4 Offshore Wage Inflation Eroding Cost Advantages

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Degree of Competition

- 4.7.5 Threat of Substitutes

- 4.8 Comparative Insights: Tier 1 vs Tier 2 Vendors

- 4.9 In-housing vs Outsourcing Analysis

- 4.10 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 IT Consulting and Implementation

- 5.1.2 Application Development and Maintenance (ADM)

- 5.1.3 Infrastructure Services

- 5.1.4 Managed Services

- 5.1.5 IT Outsourcing (ITO)

- 5.1.6 Business Process Outsourcing (BPO)

- 5.1.7 Cloud and Platform Services

- 5.1.8 Cybersecurity Services

- 5.1.9 Digital Transformation and Emerging Tech (AI, IoT, Blockchain)

- 5.2 By Deployment Model

- 5.2.1 Onshore Delivery

- 5.2.2 Nearshore Delivery

- 5.2.3 Offshore Delivery

- 5.3 By Engagement Model

- 5.3.1 Project-based / Fixed Price

- 5.3.2 Staff Augmentation / Time-and-Material

- 5.3.3 Managed Services / Outcome-based

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises (SMEs)

- 5.5 By End-User Industry

- 5.5.1 Banking, Financial Services and Insurance (BFSI)

- 5.5.2 Manufacturing

- 5.5.3 Government and Public Sector

- 5.5.4 Healthcare and Life Sciences

- 5.5.5 Retail and Consumer Goods

- 5.5.6 Telecom and Media

- 5.5.7 Transportation and Logistics

- 5.5.8 Energy and Utilities

- 5.5.9 Others

- 5.6 By Geography

- 5.6.1 Northeast

- 5.6.2 Midwest

- 5.6.3 South

- 5.6.4 West

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Accenture plc

- 6.4.2 IBM Corporation

- 6.4.3 Cognizant Technology Solutions Corp.

- 6.4.4 Tata Consultancy Services Ltd.

- 6.4.5 Microsoft Corporation

- 6.4.6 Infosys Ltd.

- 6.4.7 Wipro Ltd.

- 6.4.8 Deloitte Consulting LLP

- 6.4.9 Capgemini SE

- 6.4.10 HCL Technologies Ltd.

- 6.4.11 CGI Inc.

- 6.4.12 DXC Technology Co.

- 6.4.13 Booz Allen Hamilton Inc.

- 6.4.14 Leidos Holdings Inc.

- 6.4.15 Atos SE

- 6.4.16 EPAM Systems Inc.

- 6.4.17 NTT DATA Services

- 6.4.18 Kyndryl Holdings Inc.

- 6.4.19 LTI Mindtree Ltd.

- 6.4.20 Tech Mahindra Ltd.

- 6.4.21 Slalom LLC

- 6.4.22 Perficient Inc.

- 6.4.23 ThoughtWorks Inc.

- 6.4.24 Persistent Systems Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

IT 服務市場:2026-2032 年全球市場預測(按服務類型、合約模式、最終用戶、組織規模和部署方式分類)

IT 服務市場:2026-2032 年全球市場預測(按服務類型、合約模式、最終用戶、組織規模和部署方式分類) 2026年全球5G網路部署服務市場報告2026年全球IT服務市場報告2026年全球硬體支援服務市場報告

2026年全球5G網路部署服務市場報告2026年全球IT服務市場報告2026年全球硬體支援服務市場報告 IT 服務市場分析及預測(至 2035 年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶和解決方案分類Oracle服務市場分析及預測(至 2035 年):依類型、產品類型、服務、技術、元件、應用、部署類型、終端使用者、功能及解決方案分類

IT 服務市場分析及預測(至 2035 年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶和解決方案分類Oracle服務市場分析及預測(至 2035 年):依類型、產品類型、服務、技術、元件、應用、部署類型、終端使用者、功能及解決方案分類 英國IT服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)

英國IT服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年) 中小企業的IT服務策略:10家業者案例研究

中小企業的IT服務策略:10家業者案例研究 IT服務市場-全球產業規模、佔有率、趨勢、機會及預測(按服務、組織規模、部署類型、業務功能、最終用戶、地區和競爭格局分類),2021-2031年IT服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)

IT服務市場-全球產業規模、佔有率、趨勢、機會及預測(按服務、組織規模、部署類型、業務功能、最終用戶、地區和競爭格局分類),2021-2031年IT服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)