|

市場調查報告書

商品編碼

1940727

美國智慧鎖:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)United States Smart Lock - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

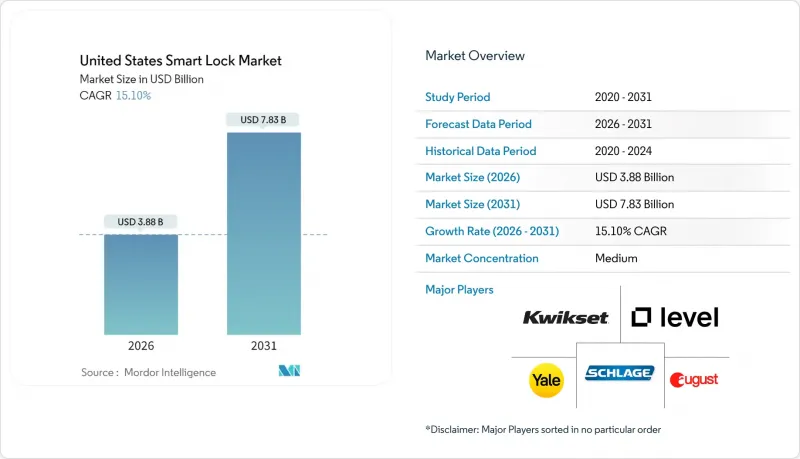

美國智慧鎖市場預計將從 2025 年的 33.7 億美元成長到 2026 年的 38.8 億美元,到 2031 年達到 78.3 億美元,2026 年至 2031 年的複合年成長率為 15.1%。

就出貨量而言,市場規模預計將從2025年的1,746萬台成長到2030年的3,903萬台,在預測期間(2025-2030年)內複合年成長率(CAGR)為17.45%。此成長主要受宅配竊盜事件頻繁、智慧家庭生態系統日趨成熟以及超寬頻(UWB)技術融入主流智慧型手機等因素驅動。與現有門鎖的兼容性推動了住宅領域的普及,而專用鎖具在商業翻新領域也越來越受歡迎。租賃住宅開發商和保險公司的獎勵刺激了市場需求,而主要品牌之間的策略整合則加劇了線上線下管道的競爭。

美國智慧鎖市場趨勢與洞察

加強與智慧家庭中心和語音助理的整合

隨著製造商實現與亞馬遜 Alexa、Google Home 和蘋果 HomeKit 的原生相容,智慧鎖的需求正在加速成長。 Matter over Thread通訊協定的出現標準化了設備通訊,使智慧鎖能夠作為節能型網狀網路節點運作。 Yale Assure Lock 2 正是這項變革的體現,它無需專用閘道器即可在生態系統中運作。語音解鎖功能透過語音模式和上下文提示增加了多重身份驗證,從而提升了安全性和便利性。每增加一台智慧型設備,整個網路的效用就會提升,隨著使用者從獨立解決方案轉向統一存取管理,系統也會隨之升級。

宅配竊盜案件的增加推動了對入戶門安防的需求。

預計到2024年,將有超過2.6億件包裹被盜,造成價值200億美元的貨物損失。智慧鎖透過向送貨人員發放臨時密碼來解決「最後一公尺安全」問題,允許他們將包裹放在室內或走廊上。亞馬遜的「Key」計畫提供監控訪問和責任險保障,已被廣泛接受。類似的功能也正在推廣到清潔工和醫療助理等服務提供者,並提供審核日誌以滿足保險公司和物業管理公司的要求。

持續存在的網路安全漏洞和公開駭客攻擊

2024年的學術測驗發現主流智慧鎖存在14個零日漏洞。這些問題包括靜態藍牙GATT值、433MHz重播攻擊向量和RFID克隆攻擊。一些舊硬體缺乏空中升級功能,使用戶面臨風險。雖然新款機型增加了加密儲存和更強大的加密技術,但一些備受矚目的概念驗證試驗正在削弱用戶信任。監管機構未能及時應對不斷演變的威脅,迫使消費者依賴第三方審核,而這些審計往往也存在缺陷。

細分市場分析

預計到2025年,插芯鎖將佔據美國智慧鎖市場61.12%的佔有率,因為美國製造的許多門都預先鑽孔以適應這種鎖具。易於改裝到現有門上鼓勵了DIY安裝,而各大品牌的平台支援也鞏固了插芯鎖的優勢。該細分市場受益於頻繁的保險折扣和豐富的配件生態系統,包括可視門鈴和感測器。隨著商業維修對建築專用五金件的需求增加,榫眼鎖和槓桿鎖等特殊類別正以17.43%的複合年成長率成長。這些產品整合了生物識別鍵盤等高級身份驗證功能,從而推高了平均售價和利潤率。

專業細分市場的成長主要得益於商業建築維修、酒店改裝以及對設計一致性要求較高的高階住宅應用。隨著系統整合商將門禁控制與建築自動化平台捆綁銷售,美國智慧鎖市場的榫眼鎖解決方案預計將穩定成長。重型掛鎖則滿足了戶外儲存和建築工地等對防風雨性能要求極高的場所的需求。儘管掛鎖市場仍屬於小眾市場,但其提供的智慧門禁功能已超越了入口大門,從而為供應商拓展了商機。

預計到2025年,住宅將貢獻88.90%的收入,主要得益於龐大的獨棟住宅用戶群和日益成長的DIY文化。語音助理互通性和保險折扣也支撐了住宅用戶的需求。儘管電池壽命的提升延長了產品更換週期,但消費者仍積極更換到具備UWB和Matter功能的下一代產品,展現出強勁的升級意願。同時,商業安裝量正以18.28%的複合年成長率成長。物業管理公司重視集中式身分驗證管理,因為它可以降低管理機械鑰匙的人事費用。

雲端控制面板使設施管理人員能夠在幾秒鐘內授予或撤銷數百扇門的存取權限。美國智慧鎖市場規模預計將在商業應用領域快速成長,尤其是在多用戶住宅和醫療保健設施領域,合規性審核將推動該技術的普及。此外,企業日益成長的ESG(環境、社會和治理)目標也在推動智慧鎖的發展,這些智慧鎖可以與能源管理系統和入住分析系統整合。

美國智慧鎖市場報告按產品類型(插銷鎖、掛鎖及其他)、最終用戶(住宅、商業)、安裝類型(維修、新建整合)和分銷管道(線上、線下)進行細分。市場預測以價值(美元)和銷售量(出貨量)為單位。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 加強與智慧家庭中心和語音助理的整合

- 包裹竊盜事件的增加推動了對入戶門安防的需求。

- 安裝智慧安防系統可享保險費折扣

- 大規模開發配備智慧門鎖的租賃住宅

- 互聯互通解決方案的ESG/LEED獎勵

- 智慧型手機上的UWB被動式門禁

- 市場限制

- 持續存在的網路安全漏洞和公開駭客攻擊

- 多用戶住宅維修設備的建築標準規範

- 安全SoC晶片組供應受限

- 消費者對資料共用的隱私擔憂

- 價值鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 競爭對手之間的競爭

- 替代品的威脅

- 定價及歷史價格趨勢

- 評估宏觀經濟對市場的影響

第5章 市場規模與成長預測

- 依產品類型

- 門栓

- 掛鎖

- 其他產品類型(例如榫眼鎖等)

- 最終用戶

- 住宅

- 商業的

- 按安裝類型

- 維修工程

- 新建時內建

- 透過分銷管道

- 線上(直銷和市場)

- 線下(零售商、安裝商)

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- August Home Inc.(ASSA ABLOY AB)

- Yale Home(ASSA ABLOY AB)

- Kwikset(ASSA ABLOY AB)

- Schlage(Allegion Company)

- Level Home Inc.

- U-Tec Group Inc.

- Wyze Labs, Inc.

- Lockly Inc.

- Eufy Security(Anker Innovations)

- SimpliSafe, Inc.

- Sentrilock, LLC

- Gate Labs Inc.

- RemoteLock

- SwitchBot Inc.

- Onity Inc.(Carrier Global)

- Digilock Inc.

- Igloohome Pte Ltd

- Nuki Home Solutions Inc.

- PDQ Locks

- Baldwin(Part of ASSA ABLOY)

第7章 市場機會與未來展望

The United States Smart Lock Market is expected to grow from USD 3.37 billion in 2025 to USD 3.88 billion in 2026 and is forecast to reach USD 7.83 billion by 2031 at 15.1% CAGR over 2026-2031.

In terms of shipment volume, the market is expected to grow from 17.46 million units in 2025 to 39.03 million units by 2030, at a CAGR of 17.45% during the forecast period (2025-2030). Momentum stems from persistent package-theft incidents, broader smart-home ecosystem maturity, and ultra-wideband (UWB) integration in mainstream smartphones. Deadbolt compatibility with existing door hardware underpins widespread residential adoption, while specialty locks gain traction in commercial retrofits. Build-to-rent developers and insurance incentives accelerate demand, and strategic consolidation among leading brands reinforces competitive intensity across both online and offline channels.

United States Smart Lock Market Trends and Insights

Increasing Integration with Smart-Home Hubs and Voice Assistants

Smart lock demand accelerates as manufacturers achieve native compatibility with Amazon Alexa, Google Home, and Apple HomeKit. The arrival of the Matter over Thread protocol standardizes device communication and allows smart locks to function as energy-efficient mesh nodes. Yale Assure Lock 2 operates across multiple ecosystems without proprietary hubs, illustrating this shift. Voice-activated unlocking now layers authentication through voice patterns and contextual cues, improving security and convenience. Each additional smart device increases overall network utility, prompting replacement cycles as users transition from point solutions to unified access management.

Rising Package-Theft Incidents Boosting Entryway Security Demand

More than 260 million deliveries faced theft in 2024, representing USD 20 billion in lost goods. Smart locks solve last-meter security by issuing temporary codes for delivery personnel, enabling in-home or vestibule drops. Amazon's Key program demonstrated mainstream acceptance when monitored access and liability coverage are present . The same capability extends to service providers such as cleaners and healthcare aides, offering audit logs that satisfy insurers and property managers.

Persistent Cyber-Security Vulnerabilities and Public Hacks

Academic testing in 2024 revealed 14 zero-day flaws in mainstream smart locks. Issues include static Bluetooth GATT values, 433 MHz replay vectors, and RFID cloning. Some older hardware lacks over-the-air update capability, leaving users exposed. High-profile demonstrations erode trust, even as new models add encrypted storage and stronger cryptography. Regulators lag behind the threat curve, so consumers rely on third-party audits that frequently uncover gaps.

Other drivers and restraints analyzed in the detailed report include:

- Insurance Premium Discounts for Smart-Security Installations

- UWB Passive-Entry in Smartphones

- Multi-Family Building Code Restrictions on Retrofit Devices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Deadbolt locks accounted for 61.12% of the US Smart Lock Market share in 2025 because most US doors are pre-bored for this format. Retrofit convenience encourages DIY adoption, and platform support from dominant brands reinforces deadbolt strength. The segment benefits from frequent insurance discounts and a rich accessory ecosystem that includes video doorbells and sensors. Specialty categories such as mortise and lever locks grow at a 17.43% CAGR as commercial renovations demand architecture-specific hardware. These products integrate advanced credentials such as biometric pads, which lift the average selling price and margin.

Specialty growth stems from commercial building upgrades, hospitality retrofits, and high-end residential applications that favor design continuity. The US Smart Lock Market size for mortise solutions is forecast to expand steadily as system integrators bundle access control with building automation platforms. Rugged padlocks address outdoor storage and construction needs where weather sealing is critical. Although niche, the padlock segment proves smart access utility beyond the front door, broadening vendor addressable revenue.

Residential buyers represented 88.90% of revenue in 2025 due to the enormous installed base of single-family homes and growing DIY culture. Voice-assistant interoperability and discounted insurance premiums sustain household demand. Battery life improvements lengthen replacement cycles, but upgrade intent remains high because UWB and Matter features motivate second-generation purchases. Commercial deployments, however, record an 18.28% CAGR. Property managers value centralized credential management that trims labor costs tied to mechanical key turnover.

Cloud dashboards let facilities revoke or grant access across hundreds of doors within seconds. The US Smart Lock Market size for commercial applications is forecast to rise sharply in multi-family and healthcare properties, where audit compliance drives technology adoption. Rising corporate ESG goals also favor smart locks that integrate with energy management systems and occupancy analytics.

The United States Smart Lock Market Report is Segmented by Product Type (Deadbolt, Padlock, Other Product Types), End-User (Residential, Commercial), Installation Type (Retrofit, New-Construction Integrated), and Distribution Channel (Online, Offline). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Shipments).

List of Companies Covered in this Report:

- August Home Inc. (ASSA ABLOY AB)

- Yale Home (ASSA ABLOY AB)

- Kwikset (ASSA ABLOY AB)

- Schlage (Allegion Company)

- Level Home Inc.

- U-Tec Group Inc.

- Wyze Labs, Inc.

- Lockly Inc.

- Eufy Security (Anker Innovations)

- SimpliSafe, Inc.

- Sentrilock, LLC

- Gate Labs Inc.

- RemoteLock

- SwitchBot Inc.

- Onity Inc. (Carrier Global)

- Digilock Inc.

- Igloohome Pte Ltd

- Nuki Home Solutions Inc.

- PDQ Locks

- Baldwin (Part of ASSA ABLOY)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing integration with smart-home hubs and voice assistants

- 4.2.2 Rising package-theft incidents boosting entryway security demand

- 4.2.3 Insurance premium discounts for smart-security installations

- 4.2.4 Build-to-rent single-family developments adopting smart locks at scale

- 4.2.5 ESG/LEED incentives for connected access solutions

- 4.2.6 UWB passive-entry in smartphones

- 4.3 Market Restraints

- 4.3.1 Persistent cyber-security vulnerabilities and public hacks

- 4.3.2 Multi-family building code restrictions on retrofit devices

- 4.3.3 Chip-set supply constraints for secure SoCs

- 4.3.4 Consumer privacy concerns over data sharing

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Intensity of Competitive Rivalry

- 4.7.5 Threat of Substitute Products

- 4.8 Pricing and Historical Price Trends

- 4.9 An Assessment of Macroeconomic Impact on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Deadbolt

- 5.1.2 Padlock

- 5.1.3 Other Product Types (Mortise, etc.)

- 5.2 By End-user

- 5.2.1 Residential

- 5.2.2 Commercial

- 5.3 By Installation Type

- 5.3.1 Retrofit

- 5.3.2 New-Construction Integrated

- 5.4 By Distribution Channel

- 5.4.1 Online (Direct and Marketplaces)

- 5.4.2 Offline (Retail, Installers)

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 August Home Inc. (ASSA ABLOY AB)

- 6.4.2 Yale Home (ASSA ABLOY AB)

- 6.4.3 Kwikset (ASSA ABLOY AB)

- 6.4.4 Schlage (Allegion Company)

- 6.4.5 Level Home Inc.

- 6.4.6 U-Tec Group Inc.

- 6.4.7 Wyze Labs, Inc.

- 6.4.8 Lockly Inc.

- 6.4.9 Eufy Security (Anker Innovations)

- 6.4.10 SimpliSafe, Inc.

- 6.4.11 Sentrilock, LLC

- 6.4.12 Gate Labs Inc.

- 6.4.13 RemoteLock

- 6.4.14 SwitchBot Inc.

- 6.4.15 Onity Inc. (Carrier Global)

- 6.4.16 Digilock Inc.

- 6.4.17 Igloohome Pte Ltd

- 6.4.18 Nuki Home Solutions Inc.

- 6.4.19 PDQ Locks

- 6.4.20 Baldwin (Part of ASSA ABLOY)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

智慧鎖市場:2026-2032年全球市場預測(依鎖類型、通訊協定、認證方式、應用及銷售管道)

智慧鎖市場:2026-2032年全球市場預測(依鎖類型、通訊協定、認證方式、應用及銷售管道) 全球智慧鎖市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球智慧鎖市場規模、佔有率、趨勢和成長分析報告(2026-2034) 智慧門鎖和門鈴市場預測至2034年-按產品類型、鎖具類型、通路、最終用戶和地區分類的全球分析

智慧門鎖和門鈴市場預測至2034年-按產品類型、鎖具類型、通路、最終用戶和地區分類的全球分析 2026年全球人工智慧(AI)智慧鎖市場報告2026年全球智慧鎖控制器市場報告

2026年全球人工智慧(AI)智慧鎖市場報告2026年全球智慧鎖控制器市場報告 智慧鎖市場規模、佔有率、趨勢和預測:按鎖類型、通訊協定、最終用戶和地區分類,2026-2034年

智慧鎖市場規模、佔有率、趨勢和預測:按鎖類型、通訊協定、最終用戶和地區分類,2026-2034年 智慧鎖市場:按產品類型、解鎖方式、應用程式和地區分類2026年全球智慧鎖市場報告

智慧鎖市場:按產品類型、解鎖方式、應用程式和地區分類2026年全球智慧鎖市場報告 智慧鎖市場分析及預測(至2035年):依類型、產品類型、技術、組件、應用、最終用戶、功能、安裝類型及解決方案分類

智慧鎖市場分析及預測(至2035年):依類型、產品類型、技術、組件、應用、最終用戶、功能、安裝類型及解決方案分類 智慧鎖:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

智慧鎖:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)