|

市場調查報告書

商品編碼

1940699

英國快遞、速遞和小包裹(CEP) 市場佔有率分析、行業趨勢和統計數據、成長預測 (2026-2031)United Kingdom Courier, Express, And Parcel (CEP) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

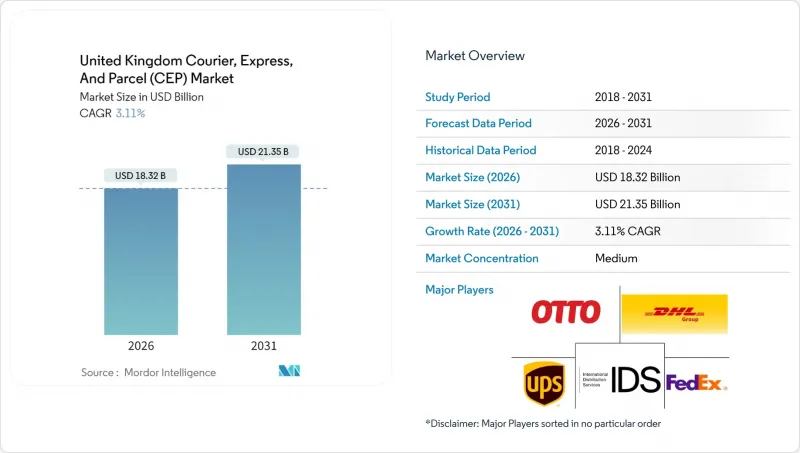

2025年英國快遞小包裹(CEP)市值為177.7億美元,預計2031年將達到213.5億美元,高於2026年的183.2億美元。

預計在預測期(2026-2031 年)內,複合年成長率將達到 3.11%。

這種溫和的擴張顯示市場環境競爭日益成熟,技術主導的效率提升、自動化和網路最佳化已發展到足以影響盈利的階段,而不僅僅是表面上的銷售成長。國內配送仍佔據主導地位,但隨著英國脫歐後貿易協定的穩定,跨境配送量正在復甦。同時,以消費者為中心的電子商務正在重新定義服務組合和配送速度預期。競爭策略強調數據驅動的路線規劃、輕資產夥伴關係以及旨在提高最後一公里配送密度的定向收購。 2024 年《數位市場、競爭和消費者法案》加強了法律規範,增加了合規成本,但也創建了一個清晰的營運框架,強調透明度和消費者保護。

英國快遞小包裹(CEP) 市場趨勢與洞察

電子商務滲透率快速成長

線上零售小包裹量持續成長,消費者對更快、可追蹤、更靈活的配送服務提出了更高的期望。能夠保證準時時限的業者獲得了豐厚的利潤,而依賴標準服務的業者則面臨利潤壓力。專門處理易碎品或高價值物品的物流網路正利用差異化服務贏得顧客忠誠度。同時,點對點轉售平台正在擴大繞過傳統實體店供應鏈的貨運量,從而擴大了大型承運商提供的儲物櫃網路和無標籤配送服務的基本客群。這些因素共同推動了對路線規劃軟體和自動化分類系統的投資,以支持盈利、高速的最後一公里配送業務。

跨境電子商務的擴張

可預測的海關規則的重建重振了國際小包裹流通,尤其是歐盟境內的包裹流通。擁有海關專業知識和多語言支援的貨運代理公司正在縮短清關週期,並透過人工智慧驅動的分類引擎等數據豐富的預申報工具來擴大市場佔有率。根據溫莎框架,北愛爾蘭享有獨特的雙市場結構,允許其在英國和歐盟範圍內提案服務,而無需重複提交文件。消費者對從歐洲大陸企業訂購商品信心的恢復,提高了貨運價值密度,並增加了對限時送達的需求。

司機短缺和工資上漲

該行業持續面臨人才短缺的挑戰,這推高了人事費用並威脅到準點率。薪資調整空間有限的獨立營運商正面臨盈利壓力,而大型運輸網路則透過實施留任獎金、車載安全技術和職業發展路徑來穩定離職率。一些運輸公司已開始試驗群眾外包車輛和自動駕駛配送,以減少對傳統大型貨車牌照的依賴。人事費用的上漲也推高了保險和培訓費用,加劇了季節性需求高峰期的成本壓力。

細分市場分析

製造業在可預測的生產計畫和零件採購流程的驅動下,將在2025年維持33.27%的市場佔有率。然而,隨著全通路零售商將履約和最後一公里配送外包,電子商務將成為最突出的成長領域,2026年至2031年的複合年成長率將達到3.41%。醫療保健物流也呈現強勁成長勢頭,這主要得益於居家臨床試驗和直接送藥給患者的模式,這些都需要嚴格的溫度控制和監管鏈通訊協定。

金融服務業對安全文件運輸的需求依然旺盛,但由於數位化,實體運輸量正在逐步下降。工業用品和原料的配送仰賴能夠處理危險物品和受管制貨物的承運商,這提升了英國國內快遞、速遞和小包裹(CEP) 市場中專業認證的價值。

從2026年到2031年,國際物流將以3.24%的複合年成長率成長,顯示穩定的海關框架正在重振英國與歐洲大陸之間的貿易往來。將數位化海關預清關功能整合到預訂平台的快遞業者,正在打造無縫的跨境購物體驗,並滿足消費者對限時送達服務的需求。在電子商務和優先考慮區域供應鏈韌性的回流措施的推動下,到2025年,國內運輸仍將佔英國快遞、速遞和小包裹(CEP)市場佔有率的64.62%。

英國快遞、速遞和小包裹(CEP) 市場的規模正受惠於業務量的多元化成長,平台業者不斷拓展國際消費群,英國消費者也擴大了採購選擇。擁有多語種客服支援、透明的關稅計算工具和便捷的退貨流程的營運商正將這種多元化轉化為盈利的重複業務。北愛爾蘭憑藉其更便捷的歐盟通道,正崛起為物流橋頭堡,使承運商能夠將其樞紐遷至此處,從而高效覆蓋英國當地和歐洲市場。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 人口統計數據

- 按經濟活動分類的GDP分配

- 按經濟活動分類的GDP成長

- 通貨膨脹

- 經濟表現及概況

- 電子商務產業的趨勢

- 製造業趨勢

- 運輸和倉儲業GDP

- 出口趨勢

- 進口趨勢

- 燃油價格

- 物流績效

- 基礎設施

- 法律規範

- 價值鍊和通路分析

- 市場促進因素

- 電子商務滲透率快速成長

- 跨境電子商務的擴張

- 引入自動化和即時追蹤系統

- 車隊電氣化獎勵

- 微型倉配快速電商的興起

- 室內/室外儲物櫃生態系統

- 市場限制

- 促進要素短缺和工資上漲

- 燃料和能源價格波動

- 都市區擁擠/超低排放區(ULEZ)收費區

- 由於土地短缺導致樞紐容量受限

- 市場創新

- 波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 目的地

- 國內的

- 國際的

- 配送速度

- 快遞

- 非快遞

- 模型

- B2B

- B2C

- C2C

- 運輸重量

- 重型貨物

- 輕型貨物

- 中等重量貨物

- 交通工具

- 航空

- 陸上

- 其他

- 終端用戶產業

- 電子商務

- 金融服務(BFSI)

- 衛生保健

- 製造業

- 一級產業

- 批發零售(線下)

- 其他

第6章 競爭情勢

- 市場集中度

- 重大策略舉措

- 市佔率分析

- 公司簡介

- APC Overnight

- DHL Group

- FedEx

- GEODIS

- International Distributions Services(including Royal Mail)

- La Poste Group

- Otto Group(including The Hermes Group)

- Rapid Parcel

- United Parcel Service(UPS)

- Yodel

第7章 市場機會與未來展望

The United Kingdom courier, express, and parcel market was valued at USD 17.77 billion in 2025 and estimated to grow from USD 18.32 billion in 2026 to reach USD 21.35 billion by 2031, at a CAGR of 3.11% during the forecast period (2026-2031).

This measured expansion indicates a mature competitive arena in which technology-led efficiency, automation, and network optimization now influence profitability more than headline volume growth. Domestic deliveries still dominate activity, but cross-border volumes are rebounding as post-Brexit trade protocols stabilize, while consumer-centric e-commerce is redefining service mix and delivery speed expectations. Competitive strategies emphasize data-driven routing, asset-light partnerships, and targeted acquisitions that deepen last-mile density. Regulatory oversight has intensified under the Digital Markets, Competition and Consumers Act 2024, sharpening compliance costs but also creating a clearer operating framework that rewards transparency and consumer protection.

United Kingdom Courier, Express, And Parcel (CEP) Market Trends and Insights

E-commerce Penetration Surge

Online retail continues to lift parcel volumes, reshaping service expectations toward faster, traceable, and flexible deliveries. Operators able to guarantee narrow time windows capture premium yields, while those relying on standard services face margin pressure. Specialist networks that handle fragile or high-value items leverage their service differentiation to win customer loyalty. At the same time, peer-to-peer resale platforms are scaling shipments that bypass traditional store-based supply chains, broadening the customer base for locker networks and label-free shipping options offered by major carriers. These forces collectively push investment into routing software and automated sortation systems that underpin profitable high-velocity last-mile operations.

Cross-Border E-commerce Expansion

The re-establishment of predictable customs rules has reignited international parcel flows, especially toward EU destinations. Carriers with customs brokerage depth and multilingual support are now widening market share by shortening clearance cycles through data-rich pre-declaration tools exemplified by AI-enabled classification engines. Northern Ireland enjoys a unique dual-market profile under the Windsor Framework, encouraging service propositions that span Great Britain and the EU without duplicative paperwork. As shoppers regain confidence in ordering from continental merchants, shipment value density rises, favoring time-definite express products.

Driver Shortages and Wage Inflation

The industry confronts persistent recruitment gaps that elevate labor costs and threaten on-time performance. Independent operators with limited wage flexibility see profitability squeezed, whereas larger networks deploy retention bonuses, in-cab safety tech, and career pathways to stabilize turnover. Some carriers are piloting crowd-sourced fleets and autonomous delivery pilots to reduce reliance on traditional HGV licenses. Rising payroll also inflates insurance premiums and training overheads, compounding cost pressure during seasonal surges.

Other drivers and restraints analyzed in the detailed report include:

- Automation and Real-Time Tracking Roll-Out

- Rise of Micro-Fulfillment Q-commerce

- Urban Congestion and ULEZ Charging Zones

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Manufacturing maintains a 33.27% share in 2025, leveraging predictable production schedules and inbound component flows. However, e-commerce is the brightest growth spot at 3.41% CAGR between 2026-2031 as omnichannel retailers outsource fulfillment and last-mile delivery. Healthcare logistics registers brisk momentum, supported by home-based clinical trials and direct-to-patient pharmaceutical deliveries that demand strict temperature and chain-of-custody protocols.

Financial services continue to require secure documentation transport, but digitalization is gradually trimming physical shipment volumes. Industrial and raw-material flows depend on carriers equipped to handle hazardous or regulated goods, reinforcing the value of specialized certifications inside the United Kingdom courier, express, and parcel market.

International values, expanding at a 3.24% CAGR between 2026-2031, illustrate how stabilized customs frameworks are reinvigorating trade flows between the United Kingdom and continental Europe. Express carriers that integrate digital customs pre-clearance into booking platforms facilitate seamless cross-border shopping experiences, thereby capturing demand for time-definite delivery. Domestic traffic still anchors 64.62% of the United Kingdom courier, express, and parcel market share in 2025, buoyed by e-commerce and reshoring initiatives that prioritize local supply chain resilience.

The United Kingdom courier, express, and parcel market size benefits from volume diversification as platform-based merchants tap foreign consumer bases and U.K. shoppers broaden sourcing choices. Operators with multilingual support desks, transparent duty calculators, and consumer-friendly returns processes convert these flows into profitable repeat business. Northern Ireland, enjoying streamlined EU access, is emerging as a logistics bridgehead, enabling carriers to reposition hubs that serve both Great Britain and Europe efficiently.

The United Kingdom Courier, Express, and Parcel (CEP) Market Report is Segmented by End User Industry (E-Commerce, Manufacturing, and More), Destination (Domestic and International), Speed of Delivery (Express and Non-Express), Shipment Weight (Heavy Weight Shipments, and More), Mode of Transport (Air, Road, and Others), and Model (Business-To-Business, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- APC Overnight

- DHL Group

- FedEx

- GEODIS

- International Distributions Services (including Royal Mail)

- La Poste Group

- Otto Group (including The Hermes Group)

- Rapid Parcel

- United Parcel Service (UPS)

- Yodel

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Demographics

- 4.3 GDP Distribution by Economic Activity

- 4.4 GDP Growth by Economic Activity

- 4.5 Inflation

- 4.6 Economic Performance and Profile

- 4.6.1 Trends in E-Commerce Industry

- 4.6.2 Trends in Manufacturing Industry

- 4.7 Transport and Storage Sector GDP

- 4.8 Export Trends

- 4.9 Import Trends

- 4.10 Fuel Price

- 4.11 Logistics Performance

- 4.12 Infrastructure

- 4.13 Regulatory Framework

- 4.14 Value Chain and Distribution Channel Analysis

- 4.15 Market Drivers

- 4.15.1 E-Commerce Penetration Surge

- 4.15.2 Cross-Border E-Commerce Expansion

- 4.15.3 Automation and Real-Time Tracking Roll-Out

- 4.15.4 Fleet Electrification Incentives

- 4.15.5 Rise of Micro-Fulfilment Q-Commerce

- 4.15.6 Indoor/Out-of-Home Locker Ecosystems

- 4.16 Market Restraints

- 4.16.1 Driver Shortages and Wage Inflation

- 4.16.2 Volatile Fuel and Energy Prices

- 4.16.3 Urban Congestion/ULEZ Charging Zones

- 4.16.4 Land-Scarce Hub Capacity Constraints

- 4.17 Technology Innovations in the Market

- 4.18 Porter's Five Forces Analysis

- 4.18.1 Threat of New Entrants

- 4.18.2 Bargaining Power of Buyers

- 4.18.3 Bargaining Power of Suppliers

- 4.18.4 Threat of Substitutes

- 4.18.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 Destination

- 5.1.1 Domestic

- 5.1.2 International

- 5.2 Speed of Delivery

- 5.2.1 Express

- 5.2.2 Non-Express

- 5.3 Model

- 5.3.1 Business-to-Business (B2B)

- 5.3.2 Business-to-Consumer (B2C)

- 5.3.3 Consumer-to-Consumer (C2C)

- 5.4 Shipment Weight

- 5.4.1 Heavy Weight Shipments

- 5.4.2 Light Weight Shipments

- 5.4.3 Medium Weight Shipments

- 5.5 Mode of Transport

- 5.5.1 Air

- 5.5.2 Road

- 5.5.3 Others

- 5.6 End User Industry

- 5.6.1 E-Commerce

- 5.6.2 Financial Services (BFSI)

- 5.6.3 Healthcare

- 5.6.4 Manufacturing

- 5.6.5 Primary Industry

- 5.6.6 Wholesale and Retail Trade (Offline)

- 5.6.7 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 APC Overnight

- 6.4.2 DHL Group

- 6.4.3 FedEx

- 6.4.4 GEODIS

- 6.4.5 International Distributions Services (including Royal Mail)

- 6.4.6 La Poste Group

- 6.4.7 Otto Group (including The Hermes Group)

- 6.4.8 Rapid Parcel

- 6.4.9 United Parcel Service (UPS)

- 6.4.10 Yodel

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

2026年全球宅配服務市場報告2026年全球宅配市場報告2026年全球當日配送服務市場報告2026年全球超當地語系化配送應用市場報告

2026年全球宅配服務市場報告2026年全球宅配市場報告2026年全球當日配送服務市場報告2026年全球超當地語系化配送應用市場報告 2026-2030年全球宅配包裹(CEP)市場

2026-2030年全球宅配包裹(CEP)市場 宅配、包裹及小包裹市場報告:按服務類型、目的地、物品、最終用途行業和地區分類(2026-2034 年)2026年全球宅配車輛市場報告

宅配、包裹及小包裹市場報告:按服務類型、目的地、物品、最終用途行業和地區分類(2026-2034 年)2026年全球宅配車輛市場報告 超當地語系化配送應用市場分析及預測(至2035年):按類型、產品、服務、技術、組件、應用、設備、流程、部署類型及最終用戶分類

超當地語系化配送應用市場分析及預測(至2035年):按類型、產品、服務、技術、組件、應用、設備、流程、部署類型及最終用戶分類 亞太地區快遞、速遞和小包裹(CEP):市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)泰國快遞、速遞和小包裹(CEP) 市場佔有率分析、行業趨勢和統計數據、成長預測 (2026-2031)

亞太地區快遞、速遞和小包裹(CEP):市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)泰國快遞、速遞和小包裹(CEP) 市場佔有率分析、行業趨勢和統計數據、成長預測 (2026-2031)