|

市場調查報告書

商品編碼

1940619

摩擦材料:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Friction Material - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

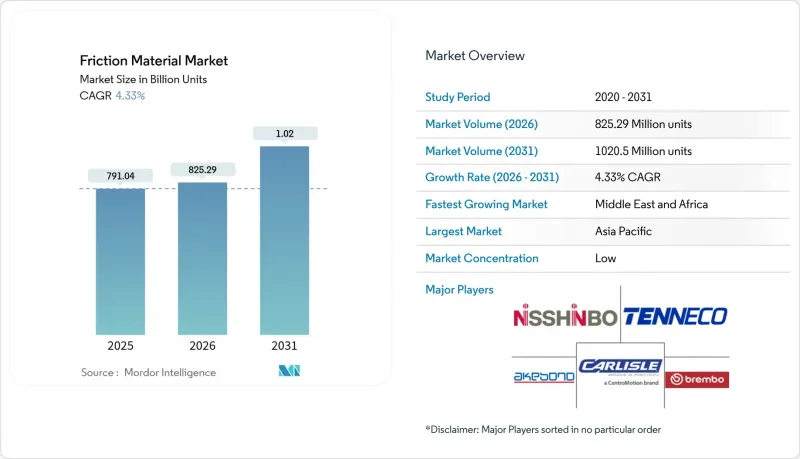

摩擦材料市場規模預計到 2026 年將達到 8.2529 億單位,高於 2025 年的 7.9104 億單位。

預計到 2031 年,銷量將達到 10.205 億輛,從 2026 年到 2031 年的複合年成長率為 4.33%。

歐7顆粒物排放法規等監管里程碑、對低粉塵煞車片的強勁需求以及不斷成長的車輛保有量,正推動摩擦材料市場穩步成長。製造商正在重新設計煞車片的化學成分,以保持無銅特性,同時,配備感測器的「智慧煞車片」的普及也有助於拓展維護即服務(MaaS)的收入模式。亞太地區的汽車製造能力和完善的售後市場生態系統支撐著該地區最大的市場佔有率,而東歐成本最佳化工廠則幫助全球供應商平衡銅、芳香聚醯胺和陶瓷纖維價格波動帶來的利潤壓力。中型區域專業企業和大規模跨國公司競相將軟體、預測分析和再生材料融入下一代產品,共同塑造了當前的競爭格局。

全球摩擦材料市場趨勢與洞察

工業和非道路機械的需求不斷成長

由於採礦、建築和農業用重型設備的摩擦部件需要承受極端高溫和污染,其單位體積的耗材量高於乘用車。自動駕駛礦用卡車使用配備感測器的碟片和煞車片組件,可將磨損數據即時傳輸至車隊管理系統,從而減少非計劃性停機時間。在新興市場,由於本地支援有限,原始設備製造商 (OEM) 正在使用更高密度的襯片來延長使用壽命。整合式傳動系統供應商正在將煞車、離合器和緩速器系統捆綁銷售,以增加交叉銷售機會。工業採購團隊,尤其是在東南亞地區,擴大選擇擁有本地庫存的供應商,以縮短大型盤片的前置作業時間。由於政府持續為基礎設施擴建和大噸位貨物運輸提供資金,預計中期內對駕駛員需求的衝擊將保持強勁。

全球汽車保有量快速成長以及煞車皮更換週期

在印度、印尼和越南,車輛保有量的成長速度超過了新車銷量,由於車齡超過九年,售後市場煞車片的需求持續強勁。在交通擁擠的都市區環境中,頻繁的走走停停會加速煞車片的磨損,縮短更換週期,抵消了電氣化帶來的銷售下滑。訂閱制和叫車車隊正在實施預防性維護計劃,儘管陶瓷煞車片價格較高,但由於其磨損更可預測,因此更傾向於選擇陶瓷煞車片。與汽車製造商合作的售後服務網路儲備了適用於多種平台的煞車片,從而簡化了跨車型代際的庫存管理。高階煞車片品牌正在利用線上管道,結合相容性數據,精準觸達DIY消費者。從長遠來看,這一因素預計將成為全球複合年成長率的最大積極貢獻者。

高昂的生命週期成本與再生煞車減少磨損之間的權衡

都市區環境中電動乘用車的煞車片壽命已超過10萬英里,與內燃機車型相比,更換頻率顯著降低。車隊成本會計會權衡低粉塵煞車片的價格與降低的維修成本,這給售後市場通路帶來了利潤壓力。配備主動式能源回收的混合動力SUV在緊急煞車時仍需要高摩擦係數的煞車來令片,這就需要高成本的雙組分煞車片解決方案。市政公車業者報告稱,隨著能量回收煞車進入能量回收階段,整個煞車系統的總擁有成本降低,從而延緩了煞車片的更換。儘管供應商正將營收重心從銷售轉向高附加價值塗層和分析技術,但此限制因素仍對摩擦材料市場的複合年成長率(CAGR)產生顯著的抑製作用。

細分市場分析

到2025年,煞車皮將繼續主導全球替換零件市場,佔據摩擦材料市場40.85%的佔有率。煞車片相關摩擦材料市場規模龐大,反映了其高損耗率以及標準化設計模板帶來的跨平台供應便利性。同時,煞車碟盤將以5.59%的複合年成長率成為成長最快的產品,因為整合式電子煞車系統需要更大尺寸、精密金屬加工的煞車碟盤,從而推高了平均售價。

煞車片的改進主要集中在無銅有機混合物上,這種混合物能夠在不犧牲摩擦係數穩定性的前提下抑製粉塵產生。豪華SUV為了降低簧下質量,紛紛採用通風式和碳陶瓷煞車盤,這推動了煞車盤需求的成長。鐵路和重工業領域對煞車塊和襯片的需求保持穩定,但自動化正在延長煞車塊的更換週期。離合器摩擦片等小眾零件正在推動機器人和工業自動化領域的成長。雖然煞車片仍然佔據主導地位,但煞車碟盤的營收成長速度更快,這拓寬了全球供應商的策略關注範圍。

到2025年,半金屬複合材料將佔據摩擦材料市場37.95%的佔有率,這主要得益於其優異的成本績效。這類複合材料將鋼纖維或銅纖維與有機黏合劑結合,兼具抗熱衰減性和降噪性。陶瓷複合材料雖然落後於半金屬複合材料,但其年複合成長率也達到了5.98%,這主要得益於歐7排放標準和高性能電動車的需求。

Brembo 的 GreenTor 雷射沉積轉子塗層可降低 PM10 的排放,展現了陶瓷材料在改變法規遵循成本方面的潛力。燒結金屬在鐵路和航空領域至關重要,但市佔率小規模。富含醯胺纖維的煞車片因其輕量化和高強度特性,在航太和高性能摩托車市場中佔據了一席之地。分階段的研發重點是生物基黏合劑,旨在減少碳排放,同時又不影響耐用性。

區域分析

亞太地區在2025年佔據摩擦材料市場45.90%的主導地位,這主要得益於成熟的供應鏈、具有成本競爭力的勞動力以及中國、印度和東南亞國協汽車保有量的快速成長。中國轉子製造商正將鑄造廠和加工廠整合到同一產業園區,進而降低物流成本,並提升全球出口競爭力。印度在2024會計年度上半年實現了收入成長,這主要得益於摩托車銷售的復甦和售後市場網路的擴張。日本在電動摩托車煞車套件領域保持主導地位,為高性能車輛專案相關的高階碟煞技術出口做出了貢獻。

北美和歐洲擁有成熟的市場基礎,這主要得益於其在環保領域的領先地位。歐盟7排放標準和加州銅排放法規使這些市場成為低粉塵光碟和感測器墊的試驗場,隨後擴展到了亞太地區。為了平衡成本,生產正向東轉移至羅馬尼亞、波蘭和墨西哥,而設計和檢驗中心則仍設在德國、義大利和美國。

中東和非洲地區複合年成長率最高,達到4.66%,這主要得益於建築業的蓬勃發展、礦產開採以及對需要耐候型煞車片的進口乘用車的需求。波灣合作理事會正在投資建設都會區域網路和輕軌,刺激了對煞車片和襯片的需求。撒哈拉以南非洲的礦用車輛正在採用專為重型卡車設計的大型濕式碟式煞車。在南美洲,儘管巴西汽車製造業正在逐步復甦,但由於貨幣波動抑制了售後市場支出,市場前景仍然低迷。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 工業和非公路機械的需求不斷成長

- 全球汽車保有量快速成長以及煞車皮更換週期

- 由於對無銅和低噪音材料的法規日益嚴格,材料重新設計正在加速推進。

- 亞洲摩托車和微型交通工具的快速電氣化

- 採用內建感測器的「智慧墊」進行預測性維護

- 市場限制

- 高昂的生命週期成本與再生煞車帶來的磨損減少形成對比

- 銅、芳香聚醯胺和陶瓷纖維的價格波動

- 由於汽車製造商轉向使用密封式、免維護變速箱,對離合器摩擦材料的需求正在下降。

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代產品和服務的威脅

- 競爭程度

第5章 市場規模與成長預測

- 依產品類型

- 磁碟

- 軟墊

- 堵塞

- 襯墊

- 其他類型

- 材料

- 陶瓷(包括碳陶瓷和碳碳陶瓷)

- 石棉

- 半金屬

- 燒結金屬

- 醯胺纖維

- 其他成分

- 透過使用

- 離合器和煞車系統

- 齒輪系統

- 其他用途

- 按最終用戶行業分類

- 車

- 鐵路

- 航太(民用和國防)

- 礦業

- 其他終端用戶產業

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- ABS Friction

- Akebono Brake Industry Co., Ltd.

- ASK FRAS-LE FRICTION PVT LTD.

- Brembo SpA

- Carlisle Brake & Friction(CentroMotion)

- ContiTech Deutschland GmbH

- EBC Brakes

- Haldex

- Hindustan Composites Ltd.

- ITT Inc.

- Japan Brake Industrial Co., Ltd.

- Miba AG

- Nisshinbo Holdings Inc.

- SGL Carbon

- Tenneco Inc.

- Yantai Haina Brake Technology Co., Ltd.

第7章 市場機會與未來展望

Friction Material Market size in 2026 is estimated at 825.29 million units, growing from 2025 value of 791.04 million units with 2031 projections showing 1020.5 million units, growing at 4.33% CAGR over 2026-2031.

Regulatory milestones such as the Euro 7 particulate limits, brisk demand for low-dust discs and pads, and rising vehicle parc volumes keep the friction material market on a steady growth path. Manufacturers are re-engineering pad chemistry to remain copper-free, while adoption of sensor-enabled "smart pads" is broadening maintenance-as-a-service revenue models. The Asia-Pacific's vehicle production strength and deep aftermarket ecosystem anchor the largest regional volume share, whereas cost-optimized Eastern European plants help global suppliers balance margin pressure from volatile prices of copper, aramid, and ceramic fiber. Competitive intensity is shaped by mid-sized regional specialists and large multinational players racing to embed software, predictive analytics, and recycled inputs into next-generation products.

Global Friction Material Market Trends and Insights

Growing need for industrial and off-highway machinery

Heavy mining, construction, and agricultural equipment consume friction components that tolerate extreme heat and contamination, lifting unit volumes well above those of passenger vehicles. Autonomous mining trucks now feature sensor-fed disc and pad sets that transmit wear data in real-time to fleet dashboards, reducing unscheduled downtime. Original-equipment manufacturers adopt higher-density linings to extend service life in emerging markets where on-site support is scarce. Integrated drivetrain suppliers bundle brake, clutch, and retarder systems, boosting cross-selling potential. Industrial procurement teams increasingly select suppliers with localized stock points to reduce lead times on oversized discs, particularly in Southeast Asia. The driver's mid-term impact remains firm as governments fund infrastructure expansion and commodities continue to move at high tonnage.

Surging global vehicle parc and brake-pad replacement cycles

Vehicle fleets in India, Indonesia, and Vietnam are growing faster than new-car sales, as the average car age climbs past nine years, sustaining aftermarket pad demand. Replacement intervals shorten in dense urban traffic because stop-and-go conditions accelerate pad wear, offsetting electrification-driven volume losses. Subscription and ride-hailing fleets impose proactive maintenance schedules that favor predictable-wear ceramic pads despite higher ticket prices. OEM-aligned service networks stock multi-platform pad lines to streamline inventory across model generations. Premium pad brands utilize online channels, leveraging fitment data, to target do-it-yourself consumers. Over the long term, this driver adds the largest positive swing to the global CAGR.

High lifecycle cost versus regenerative-braking wear reduction

Electric passenger cars in urban duty show pad life stretching past 100,000 miles, slashing replacement events relative to internal-combustion models. Fleet calculations weigh the pricing of low-dust pads against fewer interventions, placing margin pressure on aftermarket channels. Hybrid SUVs with aggressive regen reclaim still demand robust pad friction for emergency stops, forcing costly dual-compound solutions. Municipal bus operators report a drop in total brake system cost of ownership once regenerative braking reaches recovery, delaying pad changeouts. Suppliers shift their revenue focus from volume to value-added coatings and analytics, but the restraint remains a noticeable drag on the CAGR of the friction material market.

Other drivers and restraints analyzed in the detailed report include:

- Stricter copper-free and low-noise regulations accelerating material reformulation

- Rapid electrification of two-wheelers and micro-mobility fleets in Asia

- Volatile prices of copper, aramid and ceramic fibers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Brake pads captured 40.85% of the friction material market share in 2025 and continue to form the backbone of the global replacement business. The friction material market size tied to pads reflects high wear rates and standardized design templates that simplify cross-platform supply. Discs, however, post the quickest 5.59% CAGR as integrated electronic braking systems demand larger rotors with precise metallurgy, nudging average selling prices upward.

Pad upgrades center on copper-free organic blends that limit dust without compromising coefficient stability. Rotor demand gains a tailwind from premium SUVs specifying ventilated or carbon-ceramic discs, which reduce unsprung mass. Block and lining volumes remain steady in rail and heavy industry, although automation is extending block change intervals. Other niche components, such as clutch facings, leverage growth in robotics and industrial automation. Aggregate dynamics keep pads dominant, although discs accrue incremental revenue faster, thereby widening the strategic focus for global suppliers.

Semi-metallic recipes accounted for 37.95% of the friction material market size in 2025, thanks to proven cost-performance trade-offs. These blends combine steel or copper fibers with organic binders, providing a balance between fade resistance and noise control. Ceramic formulations trail but expand at 5.98% CAGR, propelled by Euro 7 dust caps and high-performance electric vehicle demand.

Brembo's Greentell laser-deposited rotor coating reduces PM10 and demonstrates the ceramic's potential to shift the economics of regulatory compliance. Sintered metals remain essential for rail and aircraft, but they account for a smaller slice. Aramid-rich pads capture a niche share in the aerospace and performance motorcycle markets due to their lightweight strength. Incremental research and development efforts focus on bio-based binders, aiming to reduce the carbon footprint without compromising durability.

The Global Friction Material Market Report is Segmented by Product Type (Discs, Pads, Blocks, Linings, and Other Types), Material (Ceramic, Asbestos, Semi-Metallic, and More), Application (Clutch and Brake Systems, Gear Tooth Systems, and Other Applications), End-User Industry (Automotive, Railway, and More), and Geography (Asia-Pacific, North America, and More). The Market Forecasts are Provided in Terms of Volume (Units).

Geography Analysis

The Asia-Pacific region held a commanding 45.90% market share of the friction material market in 2025, thanks to its entrenched supply chains, cost-competitive labor, and soaring vehicle ownership across China, India, and ASEAN. Chinese rotor producers integrate foundries and machining shops within a single industrial park, slashing logistics costs and supporting global export competitiveness. India reported a revenue growth in H1 2024, as two-wheeler sales rebounded and aftermarket networks expanded. Japan contributed premium disc technology exports tied to performance vehicle programs and maintained leadership in electric-motorcycle braking kits.

North America and Europe together form a mature volume base governed by environmental leadership. Euro 7 and California's copper restrictions position these markets as test beds for low-dust discs and sensorized pads, knowledge that subsequently scales to the Asia-Pacific region. Production shifts eastward to Romania, Poland, and Mexico, keeping cost parity, while design and validation centers stay in Germany, Italy, and the United States.

The Middle East and Africa represent the fastest-growing regional CAGR at 4.66%, driven by construction booms, mineral extraction, and the demand for imported passenger vehicles, which require climate-resilient pads. Gulf Cooperation Council projects funnel capital into metro networks and light-rail, spurring block and lining demand. Sub-Saharan mining fleets utilize oversized wet-disc brakes, specifically designed for heavy-haul trucks. South America exhibits a tempered outlook as currency volatility restrains aftermarket spending, despite a gradual recovery in Brazilian auto output.

- ABS Friction

- Akebono Brake Industry Co., Ltd.

- ASK FRAS-LE FRICTION PVT LTD.

- Brembo S.p.A.

- Carlisle Brake & Friction (CentroMotion)

- ContiTech Deutschland GmbH

- EBC Brakes

- Haldex

- Hindustan Composites Ltd.

- ITT Inc.

- Japan Brake Industrial Co., Ltd.

- Miba AG

- Nisshinbo Holdings Inc.

- SGL Carbon

- Tenneco Inc.

- Yantai Haina Brake Technology Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing need for industrial and off-highway machinery

- 4.2.2 Surging global vehicle parc and brake-pad replacement cycles

- 4.2.3 Stricter copper-free and low-noise regulations accelerating material reformulation

- 4.2.4 Rapid electrification of two-wheelers and micro-mobility fleets in Asia

- 4.2.5 Adoption of sensor-embedded "smart pads" for predictive maintenance

- 4.3 Market Restraints

- 4.3.1 High lifecycle cost versus regenerative-braking wear reduction

- 4.3.2 Volatile prices of copper, aramid and ceramic fibers

- 4.3.3 OEM shift to sealed, maintenance-free transmissions cutting clutch friction demand

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products and Services

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts

- 5.1 By Product Type

- 5.1.1 Discs

- 5.1.2 Pads

- 5.1.3 Blocks

- 5.1.4 Linings

- 5.1.5 Other Types

- 5.2 By Material

- 5.2.1 Ceramic (incl. carbon-ceramic and carbon-carbon)

- 5.2.2 Asbestos

- 5.2.3 Semi-metallic

- 5.2.4 Sintered Metals

- 5.2.5 Aramid Fibers

- 5.2.6 Other Materials

- 5.3 By Application

- 5.3.1 Clutch and Brake Systems

- 5.3.2 Gear Tooth Systems

- 5.3.3 Other Applications

- 5.4 By End-user Industry

- 5.4.1 Automotive

- 5.4.2 Railway

- 5.4.3 Aerospace (Commercial and Defense)

- 5.4.4 Mining

- 5.4.5 Other End-User Industries

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 NORDIC Countries

- 5.5.3.8 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 South Africa

- 5.5.5.4 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 ABS Friction

- 6.4.2 Akebono Brake Industry Co., Ltd.

- 6.4.3 ASK FRAS-LE FRICTION PVT LTD.

- 6.4.4 Brembo S.p.A.

- 6.4.5 Carlisle Brake & Friction (CentroMotion)

- 6.4.6 ContiTech Deutschland GmbH

- 6.4.7 EBC Brakes

- 6.4.8 Haldex

- 6.4.9 Hindustan Composites Ltd.

- 6.4.10 ITT Inc.

- 6.4.11 Japan Brake Industrial Co., Ltd.

- 6.4.12 Miba AG

- 6.4.13 Nisshinbo Holdings Inc.

- 6.4.14 SGL Carbon

- 6.4.15 Tenneco Inc.

- 6.4.16 Yantai Haina Brake Technology Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and unmet-need assessment

摩擦產品市場:2026-2032年全球市場預測(依產品類型、材料、銷售管道及最終用途產業分類)

摩擦產品市場:2026-2032年全球市場預測(依產品類型、材料、銷售管道及最終用途產業分類) 全球摩擦改進劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年)摩擦改進劑市場:按類型、基礎油相容性、應用、終端用戶產業和銷售管道分類-2026-2032年全球市場預測摩擦材料市場:2026-2032年全球市場預測(依產品類型、材料類型、應用、終端用戶產業及銷售管道)全球摩擦材料市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球摩擦改進劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年)摩擦改進劑市場:按類型、基礎油相容性、應用、終端用戶產業和銷售管道分類-2026-2032年全球市場預測摩擦材料市場:2026-2032年全球市場預測(依產品類型、材料類型、應用、終端用戶產業及銷售管道)全球摩擦材料市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 摩擦改質劑市場 - 全球產業規模、佔有率、趨勢、機會及預測(按類型、應用、地區和競爭格局分類,2021-2031年)

摩擦改質劑市場 - 全球產業規模、佔有率、趨勢、機會及預測(按類型、應用、地區和競爭格局分類,2021-2031年) 2026-2030年全球摩擦產品市場摩擦改進劑市場-2026-2031年預測

2026-2030年全球摩擦產品市場摩擦改進劑市場-2026-2031年預測 摩擦改進劑市場規模、佔有率和成長分析(按類型、應用和地區分類)—2026-2033年產業預測

摩擦改進劑市場規模、佔有率和成長分析(按類型、應用和地區分類)—2026-2033年產業預測 摩擦改進劑添加劑市場報告:2030 年趨勢、預測與競爭分析

摩擦改進劑添加劑市場報告:2030 年趨勢、預測與競爭分析