|

市場調查報告書

商品編碼

1939720

越南快遞、速遞和小包裹(CEP):市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)Vietnam Courier, Express, And Parcel (CEP) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

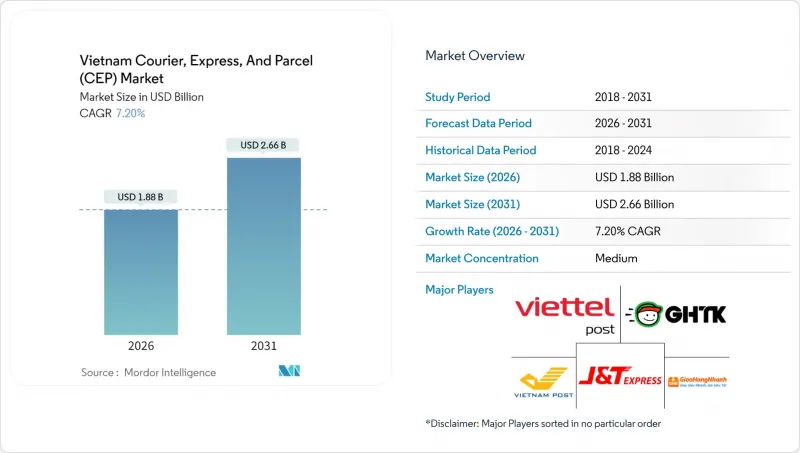

越南快遞、速遞和小包裹(CEP) 市場預計將從 2025 年的 17.5 億美元成長到 2026 年的 18.8 億美元,預計到 2031 年將達到 26.6 億美元,2026 年至 2031 年的複合年成長率為 7.2%。

精通數位技術的消費者、不斷壯大的製造業基礎以及配套的基礎設施規劃正在推動配送量的成長。從TikTok Shop到Shopee等社交電商平台正在改變消費者的訂購習慣,使其轉向更小、更頻繁的小包裹配送,這就需要靈活的末端物流網路。同時,外商直接投資(FDI)在出口導向電子和服裝產業的湧入,正在支撐強大的B2B物流,並提高長途和跨境路線的運力運轉率。可更換電池的電動車(EV)車隊正逐漸成為一種節省成本的措施,預計將縮短配送週期並大幅降低燃料成本。然而,越南的物流成本仍然高昂,佔GDP的16%至20%,迫使企業持續控制成本並投資最佳化路線。

越南快遞、速遞與小包裹(CEP) 市場趨勢與洞察

電子商務的快速成長和數位錢包的日益普及

智慧型手機普及率高達78%,推動了線上零售的爆炸性成長,也使得小小包裹以兩位數的月成長率持續攀升。如今,數位錢包已佔B2C支付的55%以上,縮短了貨到付款週期,並支持了胡志明市和河內等地當日達試點計畫的發展。為了應對激增的包裹量,快遞業者正在升級基於OCR的地址識別技術和自動化分類設備,同時與電商平台合作,確保足夠的貨量,從而支持固定路線摩托車配送。數位錢包的日益普及也刺激了郊區和區域城市的需求,使越南的宅配市場遠遠超出了主要零售區。然而,日益激烈的競爭也給單價帶來了壓力,迫使快遞公司共用配送密度並整合高速公路運輸資源。

持續的交通基礎設施擴建

越南正投資131億美元用於機場、港口和公路計劃,預計省際平均運輸時間將縮短18%。新建的隆城國際機場貨運設施年吞吐能力將達120萬噸,進而緩解新山一機場和內排機場的壓力。在越南的宅配市場,幹線周轉率的提高將提升河內至胡志明市幹線的網路速度和飛機運轉率。同時,為蓋梅港供應貨物的內陸駁船碼頭正將高附加價值電子產品出口納入一體化的多模態鏈,從而降低每小包裹公里的柴油消耗量。展望2027年及以後,當這些改善措施全面實現時,貨運代理商已開始在新樞紐附近預訂倉庫空間,以應對運力短缺的問題。

物流成本佔GDP比重高

越南整體物流系統成本約佔國內生產總值的18%,是經合組織平均水準的兩倍以上。這給承運商的利潤率帶來壓力,並限制了它們的投資能力。多項道路通行費、港口附加費和非正式收費推高了每件小包裹的營運成本,尤其是在主要通道以外的地區。因此,越南的宅配市場嚴重依賴聚合策略(聚合遞送和共用轉運樞紐)來分散固定成本。雖然大型平台可以協商獲得網路存取折扣,但小規模托運人卻被迫承擔更高的費用,這抑制了當地電子商務的訂單頻率,並減緩了整體市場擴張。

細分市場分析

至2025年,製造業將佔總收入的32.60%,其出貨量穩定,且多為多年期合約。電子產品和紡織品行業的出貨週期可預測,與季節性時尚週期和產品發布活動密切相關。受人均收入成長和積極的免運費促銷宣傳活動的推動,越南宅配市場規模預計將在2026年至2031年間以8.02%的複合年成長率快速成長。

醫療保健、銀行和保險業是規模雖小但成長迅速的利基市場,而藥品低溫運輸配送和重要文件的安全遞送則蘊含著高利潤率,這促使具備符合GDP標準的包裝和監管鏈通訊協定的專家進入該領域。

至2025年,國際小包裹將佔越南國際包裹總量的37.90%,並在2026年至2031年間以7.60%的複合年成長率超過國內包裹量。歐盟-越南自由貿易協定(EVFTA)下的關稅減免數位化清關流程已將平均清關時間縮短至24小時,促進了服裝和運動鞋的出口。隨著海外市場佔有率的成長,預計到2020年代末,越南國際宅配市場規模將達到10.6億美元。雖然國內服務在人口稠密的都市區地區保持著規模優勢,但Voso和Postmart等公司的區域擴張措施迫使快遞公司服務於需求較低的地區,從而降低了單位經濟效益。因此,快遞公司正透過將出口貨運與國內逆向物流結合併減少空駛回程來規避風險。

日益增強的國際化趨勢也推動了服務品質標準的提升。以往只有大型宅配業者才能提供的服務,例如ISO認證流程、雙重掃描追蹤和保稅倉庫,如今在中型本土公司中也變得越來越普遍。科技的普及加劇了競爭,並將越南宅配市場佔有率向那些能夠在不犧牲盈利的前提下達到國際水平KPI的營運商轉移。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 人口統計數據

- 按經濟活動分類的GDP分配

- 按經濟活動分類的GDP成長

- 通貨膨脹

- 經濟表現及概覽

- 電子商務產業的趨勢

- 製造業趨勢

- 運輸和倉儲業的GDP

- 出口趨勢

- 進口趨勢

- 燃油價格

- 物流績效

- 基礎設施

- 法律規範

- 價值鍊和通路分析

- 市場促進因素

- 電子商務的快速成長和數位錢包的日益普及

- 持續的交通基礎設施擴建

- 製造業外商直接投資轉移至越南(中國+1)

- 社群電商(例如TikTok Shops)的快速成長

- 政府透過 Voso/Postmart 促進本地電子商務發展

- 可換電池電動車網路實現超低成本的最後一公里

- 市場限制

- 物流成本佔GDP比重較高(約16-20%)

- 都市區交通擁擠和最後一公里延誤

- 物流人員缺乏具備數位技能的人員

- 分散式道路運輸基礎設施限制了規模經濟效益。

- 市場創新

- 波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 收件地址

- 國內的

- 國際的

- 配送速度

- 快遞

- 非快遞

- 模型

- B2B

- B2C

- C2C

- 運輸重量

- 重型貨物運輸

- 輕型貨物

- 中等重量貨物

- 交通工具

- 航空郵件

- 陸上

- 其他

- 終端用戶產業

- 電子商務

- 金融服務(BFSI)

- 衛生保健

- 製造業

- 一級產業

- 批發零售(線下)

- 其他

第6章 競爭情勢

- 市場集中度

- 關鍵策略舉措

- 市佔率分析

- 公司簡介

- 247 Express

- DHL Group

- FedEx

- Giao Hang Nhanh

- Giaohangtietkiem

- J&T Express

- United Parcel Service(UPS)

- Vietnam Posts and Telecommunications Group(including Vietnam Post Corporation)

- Vietstar Express

- ViettelPost

第7章 市場機會與未來展望

The Vietnam courier express parcel market is expected to grow from USD 1.75 billion in 2025 to USD 1.88 billion in 2026 and is forecast to reach USD 2.66 billion by 2031 at 7.2% CAGR over 2026-2031.

Digitally savvy consumers, an expanding manufacturing base, and supportive infrastructure programs are accelerating shipment volumes. Social-commerce platforms-from TikTok Shop to Shopee-are reshaping order profiles toward small, high-frequency parcels that demand agile last-mile networks. At the same time, foreign direct investment (FDI) in export-oriented electronics and apparel supports steady B2B flows, underpinning capacity utilization for long-haul and cross-border lanes. Battery-swap electric-vehicle (EV) fleets are emerging as a cost lever, promising faster rounds and sharply lower fuel expenses. Yet operators continue to battle Vietnam's 16-20% logistics-cost-to-GDP burden, forcing relentless cost discipline and route-optimization investments.

Vietnam Courier, Express, And Parcel (CEP) Market Trends and Insights

E-commerce Boom and Rising Digital-Wallet Adoption

Explosive online retail growth, reinforced by 78% smartphone penetration, is pouring small parcels into city hubs at double-digit monthly rates. Digital wallets now settle more than 55% of B2C checkouts, shortening cash-on-delivery cycles and supporting same-day service pilots in Ho Chi Minh City and Hanoi. CEP operators upgraded OCR-based address recognition and automated sorters to manage the surge, while marketplace alliances guarantee volume pools that justify constant-route motorcycles. Wider wallet acceptance is also unlocking suburban and tier-2 demand, expanding the Vietnam courier express parcel market well beyond primary retail districts. Intensifying competition, however, is compressing unit yields, pushing carriers toward higher drop densities and shared line-haul assets.

Ongoing Transport-Infrastructure Expansion

USD 13.1 billion in airport, seaport, and expressway projects is shrinking average interprovincial transit times by up to 18%. The new Long Thanh International Airport cargo facilities promise 1.2 million tons of annual throughput, a capacity boost that eases pressure on Tan Son Nhat and Noi Bai. For the Vietnam courier express parcel market, faster line-haul turns translate into higher network velocity and better aircraft utilization on Hanoi-Ho Chi Minh trunk routes. Inland barge terminals feeding Cai Mep port, meanwhile, are steering high-value electronics exports into integrated multimodal chains, burning less diesel per parcel kilometre. These improvements will reach full scale only after 2027, but forwarders already lock in warehouse plots near new interchanges to pre-empt capacity shortages.

High Logistics-Cost-to-GDP Ratio

Total system costs absorb close to 18% of national output, more than double the OECD average, squeezing carrier margins and hindering investment headroom. Multiple road-use tolls, port surcharges, and informal fees inflate per-parcel operating expenditure, especially outside major corridors. The Vietnam courier express parcel market, therefore, relies heavily on densification plays-clustered deliveries and shared trans-shipment nodes-to dilute fixed costs. Large platforms negotiate discounted network access, but small shippers bear higher tariffs, stunting rural e-commerce order frequency and slowing overall market expansion.

Other drivers and restraints analyzed in the detailed report include:

- Manufacturing-FDI Shift to Vietnam (China+1)

- Rapid Growth of Social-Commerce

- Urban Traffic Congestion and Last-Mile Delays

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Manufacturing generated 32.60% of 2025 revenue, providing volume stability and multi-year contracts. Electronics and textiles anchor predictable shipment calendars tied to seasonal fashion cycles and product-launch events. Vietnam courier express parcel market size from e-commerce is set to surge, given its 8.02% CAGR between 2026-2031, powered by rising per-capita income and aggressive free-shipping promotions.

Healthcare, banking, and insurance verticals represent smaller but fast-growing niches. Cold-chain pharmaceutical deliveries and secure document dispatches carry high margins, attracting specialist entrants with GDP-compliant packaging and chain-of-custody protocols.

International parcels accounted for 37.90% of volume in 2025, but their 7.60% CAGR between 2026-2031 outpaces the domestic track. Tariff relief under EVFTA and digitized customs pipelines have cut average EU-bound clearance to 24 hours, catalyzing apparel and sneaker exports. As overseas share widens, the Vietnam courier express parcel market size for cross-border flows is projected to close the decade at USD 1.06 billion. Domestic services retain scale advantages in dense urban sprawl, though rural push initiatives such as Voso/Postmart chip away at unit economics by forcing carriers to serve low-drop zones. Carriers therefore hedge by bundling outbound export freight with domestic reverse logistics to reduce empty backhauls.

A stronger international orientation also raises service-quality benchmarks. ISO-certified processes, double-scan tracking, and bonded warehousing-once exclusive to express giants-are diffusing to mid-tier local firms. This technology diffusion tightens competition and nudges overall Vietnam courier express parcel market share toward operators that can match global-standard KPIs without eroding profitability.

The Vietnam Courier, Express, and Parcel (CEP) Market Report is Segmented by Destination (Domestic and International), Speed of Delivery (Express and Non-Express), Model (Business-To-Business (B2B), and More), Shipment Weight (Heavy Weight, Light Weight, and Medium Weight), Mode of Transport (Air, Road, and Others), and End User Industry (E-Commerce, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- 247 Express

- DHL Group

- FedEx

- Giao Hang Nhanh

- Giaohangtietkiem

- J&T Express

- United Parcel Service (UPS)

- Vietnam Posts and Telecommunications Group (including Vietnam Post Corporation)

- Vietstar Express

- ViettelPost

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Demographics

- 4.3 GDP Distribution by Economic Activity

- 4.4 GDP Growth by Economic Activity

- 4.5 Inflation

- 4.6 Economic Performance and Profile

- 4.6.1 Trends in E-Commerce Industry

- 4.6.2 Trends in Manufacturing Industry

- 4.7 Transport and Storage Sector GDP

- 4.8 Export Trends

- 4.9 Import Trends

- 4.10 Fuel Price

- 4.11 Logistics Performance

- 4.12 Infrastructure

- 4.13 Regulatory Framework

- 4.14 Value Chain and Distribution Channel Analysis

- 4.15 Market Drivers

- 4.15.1 E-commerce Boom and Rising Digital-Wallet Adoption

- 4.15.2 Ongoing Transport-Infrastructure Expansion

- 4.15.3 Manufacturing-FDI Shift to Vietnam (China + 1)

- 4.15.4 Rapid Growth of Social-Commerce (Tiktok Shop, etc.)

- 4.15.5 Government Push for Rural E-Commerce via Voso/Postmart

- 4.15.6 Battery-Swap EV Networks Enabling Ultra-Low-Cost Last-Mile

- 4.16 Market Restraints

- 4.16.1 High Logistics-Cost-to-GDP Ratio (≈ 16-20 %)

- 4.16.2 Urban Traffic Congestion and Last-Mile Delays

- 4.16.3 Shortage of Digitally-Skilled Logistics Labour

- 4.16.4 Fragmented Road-Transport Base Limiting Scale Economies

- 4.17 Technology Innovations in the Market

- 4.18 Porter's Five Forces Analysis

- 4.18.1 Threat of New Entrants

- 4.18.2 Bargaining Power of Buyers

- 4.18.3 Bargaining Power of Suppliers

- 4.18.4 Threat of Substitutes

- 4.18.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 Destination

- 5.1.1 Domestic

- 5.1.2 International

- 5.2 Speed of Delivery

- 5.2.1 Express

- 5.2.2 Non-Express

- 5.3 Model

- 5.3.1 Business-to-Business (B2B)

- 5.3.2 Business-to-Consumer (B2C)

- 5.3.3 Consumer-to-Consumer (C2C)

- 5.4 Shipment Weight

- 5.4.1 Heavy Weight Shipments

- 5.4.2 Light Weight Shipments

- 5.4.3 Medium Weight Shipments

- 5.5 Mode of Transport

- 5.5.1 Air

- 5.5.2 Road

- 5.5.3 Others

- 5.6 End User Industry

- 5.6.1 E-Commerce

- 5.6.2 Financial Services (BFSI)

- 5.6.3 Healthcare

- 5.6.4 Manufacturing

- 5.6.5 Primary Industry

- 5.6.6 Wholesale and Retail Trade (Offline)

- 5.6.7 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 247 Express

- 6.4.2 DHL Group

- 6.4.3 FedEx

- 6.4.4 Giao Hang Nhanh

- 6.4.5 Giaohangtietkiem

- 6.4.6 J&T Express

- 6.4.7 United Parcel Service (UPS)

- 6.4.8 Vietnam Posts and Telecommunications Group (including Vietnam Post Corporation)

- 6.4.9 Vietstar Express

- 6.4.10 ViettelPost

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

2026年全球宅配服務市場報告2026年全球宅配市場報告2026年全球當日配送服務市場報告2026年全球超當地語系化配送應用市場報告

2026年全球宅配服務市場報告2026年全球宅配市場報告2026年全球當日配送服務市場報告2026年全球超當地語系化配送應用市場報告 2026-2030年全球宅配包裹(CEP)市場

2026-2030年全球宅配包裹(CEP)市場 宅配、包裹及小包裹市場報告:按服務類型、目的地、物品、最終用途行業和地區分類(2026-2034 年)2026年全球宅配車輛市場報告

宅配、包裹及小包裹市場報告:按服務類型、目的地、物品、最終用途行業和地區分類(2026-2034 年)2026年全球宅配車輛市場報告 超當地語系化配送應用市場分析及預測(至2035年):按類型、產品、服務、技術、組件、應用、設備、流程、部署類型及最終用戶分類

超當地語系化配送應用市場分析及預測(至2035年):按類型、產品、服務、技術、組件、應用、設備、流程、部署類型及最終用戶分類 亞太地區快遞、速遞和小包裹(CEP):市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)泰國快遞、速遞和小包裹(CEP) 市場佔有率分析、行業趨勢和統計數據、成長預測 (2026-2031)

亞太地區快遞、速遞和小包裹(CEP):市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)泰國快遞、速遞和小包裹(CEP) 市場佔有率分析、行業趨勢和統計數據、成長預測 (2026-2031)