|

市場調查報告書

商品編碼

1939126

歐洲玻璃包裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Europe Glass Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

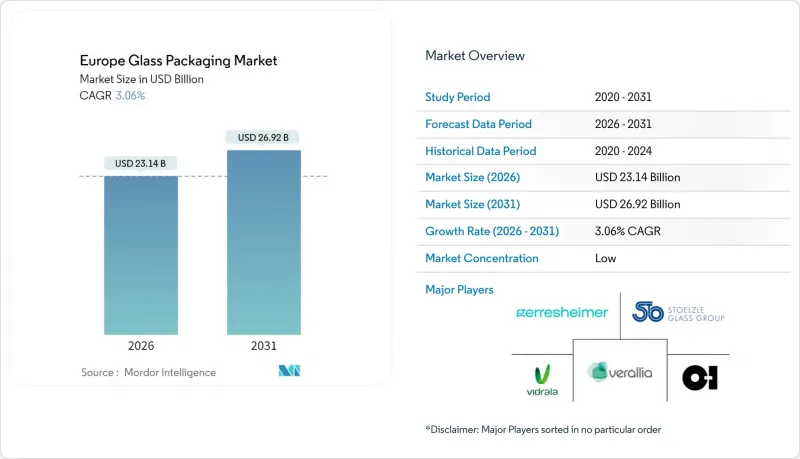

2025年歐洲玻璃包裝市場價值為224.5億美元,預計到2031年將達到269.2億美元,高於2026年的231.4億美元。

預計在預測期(2026-2031 年)內,複合年成長率將達到 3.06%。

與市場成熟同步的是變革性的監管壓力,其中包括歐盟包裝和包裝廢棄物法規 (PPWR)。該法規要求在 2030 年實現包裝完全可回收,並在結構上優先考慮玻璃,因為玻璃可以無限循環利用且不會劣化。對混合爐和電爐的技術投資降低了碳排放強度,抵消了天然氣價格波動的影響。同時,儘管面臨物流成本上升的不利因素,飲料、化妝品和製藥業的高階定位仍然保持了定價權。從 2024 年起,為了保護不斷縮減的利潤空間,競爭策略的重點是合理化產能、提高玻璃屑品質以及為製藥業提供專用產品。

歐洲玻璃包裝市場趨勢與洞察

歐盟包裝和包裝廢棄物法規加速了可無限循環利用玻璃的普及。

《包裝和包裝廢棄物條例》(PPWR) 規定,到 2030 年,歐盟境內銷售的所有包裝形式都必須被視為可回收。提案的費用調整方案將對複合結構進行懲罰,並鼓勵使用單一材料容器,例如玻璃。目前,大多數成員國的玻璃回收率已超過 80%,義大利到 2023 年的回收率將超過 90%。與聚合物替代品不同,玻璃不會因反覆回收而分解。食品接觸面上的 PFAS 含量限制對塑膠和多層複合材料構成了額外的合規障礙,進一步鞏固了玻璃作為低風險替代品的地位。該條例設定的 2030 年飲料容器重複使用率達到 10% 的目標,也為填充用玻璃容器的發展奠定了基礎,尤其是在那些正在擴大押金返還制度的國家。

飲料和化妝品的優質化推動了對設計的需求。

奢侈品牌強調玻璃瓶獨特的美學和質感,以此彰顯其真實性並為其更高的價格辯護。例如,Bienaim 售價 160 歐元的「Monsieur」香水就裝在 Walter Sparger 訂製的瓶子中。烈酒裝瓶商、精釀酒廠和精品酒莊紛紛採用精細的壓紋工藝、獨特的色彩和再生玻璃混合材質,以滿足消費者對高階且永續體驗的需求。像 SGD Pharma 這樣的化妝品製造商現在供應含有 20% 消費後碎玻璃的玻璃屑瓶,使奢侈品牌能夠在不降低透明度的前提下,宣稱其產品符合更低的範圍 3 排放標準。優質化往往能夠抵禦經濟放緩的影響,因為目標消費者更重視感知品質和永續性,而非單價。

輕質鋁材和PET材料憑藉物流優勢擴大市場佔有率。

受輕量罐裝產品需求成長的推動,Arda Metal Packaging的歐洲分公司預計2024年銷售額將成長6%,達到21.6億美元。輕型罐裝產品因其體積和重量效率高,能夠降低單位運輸成本,因此深受注重價格的飲料填充商的青睞。 31%的葡萄酒生產商表示,他們已將部分產品改用襯袋紙盒或PET容器包裝,以減少運輸排放和運費。這一趨勢在東歐尤為明顯,因為東歐地區零售點距離遙遠,燃油成本轉嫁有限。

細分市場分析

預計到2025年,歐洲玻璃包裝市場中瓶/容器細分市場規模將達到148.4億美元(佔總規模的66.12%)。成熟的飲料和食品分銷管道維持基本需求,但由於消費者對輕量化產品的需求,利潤率正在下降。管瓶、安瓿瓶和注射器雖然小規模,但在生物製藥、GLP-1療法和豐富的注射劑研發管線的推動下,預計將以4.35%的複合年成長率成長。隨著Gerresheimer和SGD Pharma產能的運作,以及嚴格的ISO 15378品質標準的保障,歐洲管瓶玻璃包裝市場佔有率預計將逐步提升。

醫藥買家願意為尺寸精度、抗剝離性和可追溯性更高的產品支付更高的單價,這促成了多年期供應協議的簽訂,並降低了生產商的收入波動。像肖特公司(SCHOTT)的Velocity管瓶(採用I型硼矽酸玻璃管製造)這樣的創新產品,能夠加快填充速度並減少外觀缺陷,從而增強專業供應商的競爭優勢。

截至2025年,鈉鈣玻璃(III型)佔據了歐洲玻璃包裝市場57.75%的佔有率,這主要得益於其成本結構適合大規模生產的飲料和食品瓶。然而,鑑於製藥業對純度標準的嚴格要求,硼矽酸玻璃(I型)預計將以4.58%的複合年成長率成長。受先進生物製藥相關法規不斷完善的推動,預計到2031年,歐洲I型硼矽酸玻璃包裝市場規模將達到66.6億美元。

硼矽酸玻璃製造需要更嚴格的爐溫控制和更高純度的原料。製造商正在投資全電爐,以確保更穩定的加熱曲線並減少二氧化碳排放。基於ISO標準的審核追蹤和藥典合規要求構成了准入壁壘,保護現有供應商免受主導競爭的影響。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 歐盟包裝和包裝廢棄物法規 (PPWR) 加速向可無限循環利用的玻璃材料轉型

- 飲料和化妝品行業的優質化正在推動對時尚玻璃瓶的需求。

- 消費者對惰性、不含微塑膠包裝的偏好增強了品牌忠誠度。

- 產業轉型為混合/電爐可減少碳排放並保障營運許可證。

- 人工智慧光學分選技術提高了玻璃廢料的品質和供應量

- 永續性計劃和塑膠禁令推動了玻璃包裝的普及

- 市場限制

- 輕質鋁材和PET材料因其物流成本優勢而擴大市場佔有率。

- 能源價格波動對熔煉利潤造成壓力

- Z世代認為盒裝和罐裝葡萄酒比玻璃瓶裝葡萄酒更環保。

- 塑膠和金屬包裝替代品正在蠶食大批量SKU中玻璃包裝的市場佔有率

- 產業價值鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭強度

- 貿易情景分析

第5章 市場規模與成長預測

- 依產品

- 瓶子/容器

- 管瓶

- 安瓿

- 注射器/藥筒

- 按玻璃類型

- I型(硼矽酸玻璃)

- II 型(處理過的鈉石灰)

- 第三類(鈉鈣玻璃)

- 琥珀色

- 最終用戶

- 食物

- 軟性飲料

- 酒精飲料

- 化妝品和個人護理

- 製藥

- 按容量範圍

- 少於30毫升

- 30~100 ml

- 100~500 ml

- 500~1,000 ml

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Verallia SA

- BA Glass BV

- OI Glass, Inc.

- Vidrala, SA

- Verescence SAS

- Gerresheimer AG

- Saverglass SAS

- ALGLASS SA

- Quadpack Industries SA

- Berlin Packaging LLC

- Wiegand-Glas Holding GmbH

- Ardagh Group SA

- Heinz-Glas GmbH & Co. KGaA

- Zignago Vetro SpA

- Beatson Clark Limited

- Stoelzle Oberglas GmbH

- Vetropack Austria GmbH

- CP Glass SA

第7章 市場機會與未來展望

- 閒置頻段與未滿足需求評估

The Europe glass packaging market was valued at USD 22.45 billion in 2025 and estimated to grow from USD 23.14 billion in 2026 to reach USD 26.92 billion by 2031, at a CAGR of 3.06% during the forecast period (2026-2031).

Maturation of the market coexists with transformative regulatory pressure, notably the EU Packaging and Packaging Waste Regulation (PPWR), which mandates full recyclability by 2030 and structurally favors glass because it can be recycled infinitely without quality loss. Technology investments in hybrid and electric furnaces are lowering carbon intensity and countering the impact of volatile natural-gas prices, while premium positioning in beverages, cosmetics, and pharmaceuticals sustains pricing power despite logistics cost headwinds. Competitive strategies revolve around capacity rationalization, cullet-quality upgrades, and specialized pharmaceutical offerings to protect margins that have come under pressure since 2024.

Europe Glass Packaging Market Trends and Insights

EU Packaging and Packaging-Waste Regulation Accelerates Infinitely Recyclable Glass Adoption

The PPWR stipulates that every packaging format sold in the bloc be deemed recyclable by 2030, and its proposed fee modulation will penalize composite structures while rewarding mono-material containers such as glass. Glass already enjoys collection rates exceeding 80% across most member states, with Italy surpassing 90% in 2023, and unlike polymeric substitutes, it does not down-cycle during repeated loops. PFAS restrictions on food-contact surfaces introduce further compliance hurdles for plastic and multilayer laminates, reinforcing glass as the low-risk alternative. The regulation's 10% reuse target for beverage containers by 2030 also underpins refillable glass growth, particularly in countries extending deposit-return schemes.

Premiumisation in Beverages and Cosmetics Boosts Design-Rich Demand

Luxury brands highlight glass aesthetics and tactile weight to signal authenticity and justify premium price points, as illustrated by Bienaime's EUR 160 Monsieur eau de parfum packaged in a custom flacon from Waltersperger. Spirits bottlers, craft breweries, and boutique wineries adopt intricate embossing, unique hues, and recycled glass blends to satisfy consumer desires for premium yet sustainable experiences. Cosmetics players such as SGD Pharma now supply flint bottles containing 20% post-consumer cullet, enabling high-end brands to market lower Scope 3 profiles without sacrificing clarity. Premiumisation resists economic slowdowns because target shoppers prioritize perceived quality and sustainability over unit price.

Lightweight Aluminium and PET Gain Share Through Logistics Edge

Ardagh Metal Packaging's European unit grew 6% to USD 2.16 billion revenue in 2024, behind demand for light cans whose superior cube and weight efficiency reduces freight cost per unit, appealing to price-sensitive beverage fillers. Wine producers report that 31% have migrated part of their portfolio to bag-in-box or PET to shave transport emissions and freight bills, trends pronounced in Eastern Europe, where the distance to retail hubs is larger and fuel cost pass-through is limited.

Other drivers and restraints analyzed in the detailed report include:

- Consumer Preference for Inert, Micro-Plastic-Free Containers Strengthens Loyalty

- Industry Shift to Hybrid and Electric Furnaces Protects Licence to Operate

- Volatile Energy Prices Squeeze Melting Margins and Production Economics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The European glass packaging market size tied to Bottles/Containers stood at USD 14.84 billion in 2025, equal to 66.12% of the total value. Mature beverage and food channels sustain their baseline demand, but margins compress as customers demand lightweight options. Vials, Ampoules, and Syringes together form a smaller pool but grow at 4.35% CAGR on the back of biologics, GLP-1 therapies, and a strong pipeline of parenteral drugs. The European glass packaging market share for Vials will gradually expand as capacity additions by Gerresheimer and SGD Pharma come online, supported by stringent ISO 15378 quality specifications.

Pharmaceutical buyers accept higher unit prices for dimensional accuracy, delamination resistance, and traceability, driving multi-year supply agreements that reduce revenue volatility for producers. Innovations such as SCHOTT's Velocity Vials, manufactured from Type I borosilicate tubing, increase filling-line speeds and reduce cosmetic defects, sharpening the competitive edge of specialty suppliers.

Type III soda-lime captured 57.75% of the Europe glass packaging market share in 2025 because its cost profile aligns with mass beverages and food jars. Nevertheless, Type I borosilicate is projected to expand at a 4.58% CAGR given the pharmaceutical sector's uncompromising purity standards. The Europe glass packaging market size tied to Type I borosilicate is forecast to crest USD 6.66 billion by 2031, aided by regulatory momentum around advanced biologics.

Borosilicate manufacture demands tighter furnace temperature control and higher raw-material purity. Producers invest in all-electric furnaces to secure a more stable heat curve while cutting CO2 output. ISO-based audit trails and pharmacopoeia conformity requirements serve as entry barriers that shield established vendors from price-led competition.

The Europe Glass Packaging Market Report is Segmented by Product (Bottles/Containers, Vials, Ampoules, and Syringes/Cartridges), Glass Type (Type I Borosilicate, Type II Treated Soda-Lime, Type III (Soda-Lime), and Amber), End-User Vertical (Food, Soft-Drink Beverages, Alcoholic Beverages, Pharmaceutical, and More), Capacity Range (<30 Ml, 30-100 Ml, 100-500 Ml and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Verallia S.A

- BA Glass B.V.

- O-I Glass, Inc.

- Vidrala, S.A.

- Verescence SAS

- Gerresheimer AG

- Saverglass SAS

- ALGLASS S.A.

- Quadpack Industries S.A.

- Berlin Packaging L.L.C.

- Wiegand-Glas Holding GmbH

- Ardagh Group S.A.

- Heinz-Glas GmbH & Co. KGaA

- Zignago Vetro S.p.A.

- Beatson Clark Limited

- Stoelzle Oberglas GmbH

- Vetropack Austria GmbH

- CP Glass S.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 EU Packaging and Packaging-Waste Regulation (PPWR) accelerates switch to infinitely-recyclable glass

- 4.2.2 Premiumisation in beverages and cosmetics boosts demand for design-rich glass bottles

- 4.2.3 Consumer preference for inert, micro-plastic-free containers strengthens brand loyalty

- 4.2.4 Industry shift to hybrid-/electric furnaces lowers carbon footprint, protecting licence to operate

- 4.2.5 AI-enabled optical sorting raises cullet quality and glass availability

- 4.2.6 Sustainability Push and Plastic Bans Accelerate Glass Packaging Adoption

- 4.3 Market Restraints

- 4.3.1 Lightweight aluminium and PET gaining share on logistics cost advantage

- 4.3.2 Volatile energy prices squeeze melting margins

- 4.3.3 Gen-Z perception that boxed and canned wine is "greener" than glass

- 4.3.4 Plastic and Metal Packaging Alternatives Erode Glass Share in Mass SKUs

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

- 4.8 Trade Scenario Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product

- 5.1.1 Bottles / Containers

- 5.1.2 Vials

- 5.1.3 Ampoules

- 5.1.4 Syringes / Cartridges

- 5.2 By Glass Type

- 5.2.1 Type I (Borosilicate)

- 5.2.2 Type II (Treated Soda-lime)

- 5.2.3 Type III (Soda-lime)

- 5.2.4 Amber

- 5.3 By End-user

- 5.3.1 Food

- 5.3.2 Soft-drink Beverages

- 5.3.3 Alcoholic Beverages

- 5.3.4 Cosmetics and Personal Care

- 5.3.5 Pharmaceutical

- 5.4 By Capacity Range

- 5.4.1 <30 ml

- 5.4.2 30 - 100 ml

- 5.4.3 100 - 500 ml

- 5.4.4 500 - 1,000 ml

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Verallia S.A

- 6.4.2 BA Glass B.V.

- 6.4.3 O-I Glass, Inc.

- 6.4.4 Vidrala, S.A.

- 6.4.5 Verescence SAS

- 6.4.6 Gerresheimer AG

- 6.4.7 Saverglass SAS

- 6.4.8 ALGLASS S.A.

- 6.4.9 Quadpack Industries S.A.

- 6.4.10 Berlin Packaging L.L.C.

- 6.4.11 Wiegand-Glas Holding GmbH

- 6.4.12 Ardagh Group S.A.

- 6.4.13 Heinz-Glas GmbH & Co. KGaA

- 6.4.14 Zignago Vetro S.p.A.

- 6.4.15 Beatson Clark Limited

- 6.4.16 Stoelzle Oberglas GmbH

- 6.4.17 Vetropack Austria GmbH

- 6.4.18 CP Glass S.A.

7 MARKET OPPORTUNITIES ANDFUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

復古相機市場:全球產業規模、市場佔有率、趨勢、機會和預測(按類型、狀況、分銷管道和地區分類)、競爭格局(2021-2031 年)

復古相機市場:全球產業規模、市場佔有率、趨勢、機會和預測(按類型、狀況、分銷管道和地區分類)、競爭格局(2021-2031 年) 玻璃包裝市場報告:按產品、最終用戶和地區分類(2026-2034 年)

玻璃包裝市場報告:按產品、最終用戶和地區分類(2026-2034 年) 玻璃包裝市場:2026-2032年全球市場預測(依包裝類型、應用、玻璃類型及通路分類)

玻璃包裝市場:2026-2032年全球市場預測(依包裝類型、應用、玻璃類型及通路分類) 玻璃包裝市場:按類型、終端用戶行業和地區分類

玻璃包裝市場:按類型、終端用戶行業和地區分類 全球玻璃包裝市場規模、佔有率、趨勢和成長分析報告(2026-2034年)琥珀色玻璃容器市場:按應用、類型和分銷管道分類-2026-2032年全球市場預測玻璃復古包裝市場:按銷售量、最終用途和分銷管道分類,全球預測(2026-2032年)

全球玻璃包裝市場規模、佔有率、趨勢和成長分析報告(2026-2034年)琥珀色玻璃容器市場:按應用、類型和分銷管道分類-2026-2032年全球市場預測玻璃復古包裝市場:按銷售量、最終用途和分銷管道分類,全球預測(2026-2032年) 全球玻璃包裝市場:趨勢與展望(至2034年)烈酒玻璃市場:按產品類型、材質、設計美學、銷售管道和最終用戶分類,全球預測(2026-2032)

全球玻璃包裝市場:趨勢與展望(至2034年)烈酒玻璃市場:按產品類型、材質、設計美學、銷售管道和最終用戶分類,全球預測(2026-2032) 復古相機市場規模、佔有率和成長分析(按相機類型、目標用戶、價格範圍、配件和地區分類)—2026-2033年產業預測

復古相機市場規模、佔有率和成長分析(按相機類型、目標用戶、價格範圍、配件和地區分類)—2026-2033年產業預測