|

市場調查報告書

商品編碼

1939035

美國可再生能源:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)United States Renewable Energy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

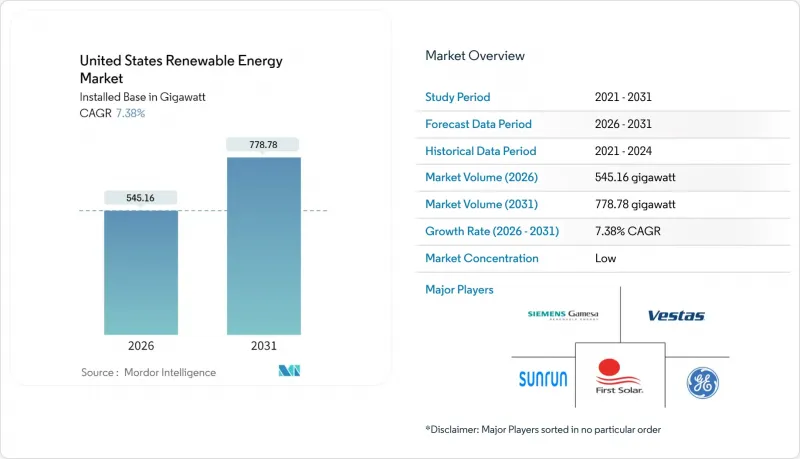

2025年美國可再生能源市場價值為507.67吉瓦,預計2031年將達到778.78吉瓦,高於2026年的545.16吉瓦。

預測期(2026-2031 年)的複合年成長率預計為 7.38%。

《通貨膨脹控制法案》下的聯邦激勵措施、太陽能和風能安裝成本的快速下降以及企業清潔能源部署目標的創紀錄高位,正在推動一個不再完全依賴補貼的投資週期。電網改革、將電池儲能與可再生能源結合的計劃結構以及國內製造業的成長,進一步增強了美國可再生能源市場的經濟效益。太陽能光電發電以41.2%的技術佔有率領先,風能保持其作為基礎能源的地位,而儲能解決方案正在加速電網的柔軟性。儘管公用事業公司仍然主導著裝機容量,但家庭和企業的分散式能源正在快速成長,重塑著收入模式,並推動美國可再生能源市場的服務創新。

美國可再生能源市場趨勢與洞察

延長聯邦投資稅額扣抵和生產稅額扣抵

太陽能光電發電30%的投資稅額扣抵和風力光電26美元/兆瓦時的生產稅額扣抵(有效期至2032年)的長期確定性,幫助美國可再生能源市場維持了穩定的建設進度,避免了以往快速成長後突然放緩的模式。國內含量要求帶來的額外收益使實際稅額扣抵率提高了10個百分點,預計到2024年,美國太陽能板的產量將增加40%。太陽能電池最高可達0.07美元/瓦的多級製造稅額扣抵,進一步改善了計劃的經濟效益,並鼓勵新工廠落腳傳統工業州,從而擴大了美國可再生能源市場的稅基。

太陽能和風能發電的平準化電成本(LCOE)迅速下降

到2024年,大型光伏發電的平準化度電成本(LCOE)將達到0.048美元/千瓦時,陸上風電的平準化度電成本將達到0.033美元/千瓦時,兩者均低於未享受補貼的聯合循環燃氣發電價格。更大的風力渦輪機、更密集的電池結構以及供應鏈的最佳化正在降低資本成本,而儲能技術的加入則將波動不定的輸出轉化為可調度的電力。商業買家將這些價格下降視為石化燃料價格波動風險的有效途徑,這不僅推動了美國可再生能源市場計劃儲備的成長,也為投資者創造了可預測的收入來源。

電網瓶頸和互聯排隊

到2024年,電網連接積壓量將達到2.6太瓦,比2020年增加四倍,並將導致計劃延長四到五年。儘管聯邦能源監管委員會(FERC)2023號令引入了叢集研究規則和商業性可行性審查,但大部分積壓項目仍需要電網升級,每兆瓦的升級成本超過100萬美元。在風能資源豐富的大平原地區,由於缺乏通往負載中心的輸電線路,阻礙了開發,並導致美國可再生能源市場近期新增裝置容量的萎縮。

細分市場分析

預計到2025年,太陽光電技術將占美國可再生能源市場佔有率的40.80%,並在2031年之前以12.05%的複合年成長率成長。 85%的新建大型太陽能發電廠都配備了儲能系統,將白天的發電轉化為高峰時段的電力供給能力,從而提高了收入的穩定性。農光互補將農業生產與太陽能發電結合,在提高農場盈利的同時,也緩解了土地資源的限制。風能仍是許多能源組合的基礎,由於塔架更高、轉子更大,風力發電的安裝面積也隨之擴大。離岸風電發展勢頭強勁,透過聯邦租賃競標和州政府公開招標,離岸風電裝置容量總合15吉瓦。水力發電和地熱雖然能夠提供可靠的電力,但資源限制和高昂的初始成本減緩了它們的發展速度。如今,技術組合決策不僅考慮千瓦時成本,還考慮電網服務價值,這正在重塑美國可再生能源市場的投資邏輯。

預計到2031年,美國純太陽能可再生能源市場規模將達到326.4吉瓦,隨著區域電網的增強,陸域風電預計將擴展至253.1吉瓦。諸如增強型地熱系統和海洋能等新興資源目前規模小規模,但先導計畫已證明,在成本最佳化後具有擴充性。總體而言,隨著關鍵州滲透率超過50%,技術多元化將有助於緩解天氣相關的波動,並提高電力可靠性。

美國可再生能源市場報告按技術(太陽能、風能、水力、生質能源能、地熱能和海洋能)和最終用戶(公共產業、商業和工業以及住宅)進行細分。市場規模和預測以吉瓦裝置容量為單位。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 延長聯邦投資稅額扣抵和生產稅額扣抵

- 太陽能和風能發電的平準化能源成本(LCOE)大幅下降

- 企業淨零排放及 RE100 採購目標

- 製造業復甦趨勢與通膨控制法有關

- 能夠促進可再生能源普及的電網強化技術

- 市場限制

- 電網瓶頸和互聯排隊

- 渦輪機和麵板原料價格波動;

- 當地民眾反對大型發電工程

- 供應鏈分析

- 監理展望

- 技術展望

- 波特五力模型

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

- PESTEL 分析

第5章 市場規模與成長預測

- 透過技術

- 太陽能(光伏和聚光太陽能)

- 風力發電(陸上和海上)

- 水力發電(小規模、大型、抽水蓄能)

- 生質能源

- 地熱

- 海洋能源(潮汐能和波浪能)

- 最終用戶

- 電力公司

- 商業和工業

- 住宅

第6章 競爭情勢

- 市場集中度

- 策略性措施(併購、合資、資金籌措、購電協議)

- 市場佔有率分析(主要企業的市場排名和佔有率)

- 公司簡介

- NextEra Energy, Inc.

- Invenergy LLC

- Orsted US Offshore Wind

- General Electric Company

- Vestas Wind Systems A/S

- First Solar, Inc.

- Canadian Solar Inc.

- Sunrun Inc.

- Enphase Energy, Inc.

- Siemens Gamesa Renewable Energy SA

- Brookfield Renewable Partners LP

- Pattern Energy Group LP

- AES Clean Energy

- Dominion Energy, Inc.

- Duke Energy Renewables

- EDF Renewables North America

- EDP Renewables North America LLC

- Clearway Energy Group LLC

- Mitsubishi Power Americas, Inc.

- Trina Solar Co., Ltd.

第7章 市場機會與未來展望

The United States Renewable Energy Market was valued at 507.67 gigawatt in 2025 and estimated to grow from 545.16 gigawatt in 2026 to reach 778.78 gigawatt by 2031, at a CAGR of 7.38% during the forecast period (2026-2031).

Federal incentives under the Inflation Reduction Act, steep cost declines in solar photovoltaic and wind equipment, and record-high corporate clean-electricity commitments are driving an investment cycle that no longer depends solely on subsidies. Transmission reforms, battery-plus-renewable project structures, and domestic manufacturing expansion further strengthen the economics of the US renewable energy market. Solar holds the leading 41.2% technology share, while wind remains a foundational resource, and storage solutions accelerate grid flexibility. Utilities still dominate installed capacity, yet distributed resources in homes and businesses grow quickly, reshaping revenue models and spurring service innovation across the US renewable energy market.

United States Renewable Energy Market Trends and Insights

Extension of Federal Investment & Production Tax Credits

Long-term certainty through 2032 for the 30% investment tax credit on solar and USD 26 per MWh production tax credit for wind keeps the US renewable energy market on a steady build schedule, avoiding the historical boom-bust pattern.Domestic-content bonuses lift effective credits by 10 percentage points and have already encouraged a 40% increase in US solar panel output during 2024. Layered manufacturing credits, worth up to USD 0.07 per watt for solar cells, further improve project economics and anchor new factories in traditional industrial states, broadening the tax base benefits of the US renewable energy market.

Rapid Decline in Solar-PV & Wind LCOE

Utility-scale solar reached USD 0.048 per kWh and onshore wind USD 0.033 per kWh in 2024, both undercutting combined-cycle gas prices without subsidies. Larger turbines, high-density cell architectures, and supply-chain optimization compress capital costs, while energy storage attachments convert variable output into dispatchable power. Corporate buyers treat these falling prices as a hedge against fossil-fuel volatility, adding momentum to the US renewable energy market's project pipeline and creating predictable revenue streams for investors.

Transmission Bottlenecks & Interconnection Queues

The interconnection backlog hit 2.6 TW by 2024, quadrupling 2020 levels and delaying projects by 4-5 years. Although FERC Order 2023 imposes cluster-study rules and commercial readiness screens, most pending applications still face network upgrades valued at more than USD 1 million per MW. The Great Plains, rich in wind, sees development stymied without conduits to load centers, resulting in trimmed near-term additions in the US renewable energy market.

Other drivers and restraints analyzed in the detailed report include:

- Corporate Net-Zero & RE100 Procurement Targets

- Inflation Reduction Act-linked Manufacturing Upswing

- Volatility in Commodity Prices for Turbines & Panels

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solar technology accounted for 40.80% of the US renewable energy market share in 2025 and is projected to grow at the fastest rate, with a 12.05% CAGR, to 2031. Pairing with batteries means that 85% of new utility solar installations include storage, turning midday generation into peaking capacity and raising revenue certainty. Agrivoltaics blends crop production and photovoltaics, easing land constraints while improving farmer economics. Wind still anchors many portfolios and benefits from taller towers and larger rotors that expand viable terrain. Offshore wind gains momentum through federal lease auctions and state solicitations totaling 15 GW. Hydropower and geothermal energy offer dependable capacity, yet resource limitations and higher upfront costs slow their relative advancement. Technology mix decisions now reflect grid-service value in addition to kilowatt-hour prices, reshaping investment logic inside the US renewable energy market.

The US renewable energy market size for solar alone is expected to reach 326.4 GW by 2031, while onshore wind is projected to expand to 253.1 GW amid regional transmission upgrades. Emerging resources, such as enhanced geothermal systems and marine energy, exhibit modest baselines, but pilot projects reveal scalability once costs are optimized. In aggregate, technology diversification cushions weather-related output swings and strengthens reliability as penetration rises beyond 50% in leading states.

The United States Renewable Energy Market Report is Segmented by Technology (Solar Energy, Wind Energy, Hydropower, Bioenergy, Geothermal, and Ocean Energy) and End-User (Utilities, Commercial and Industrial, and Residential). The Market Sizes and Forecasts are Provided in Terms of Installed Capacity (GW).

List of Companies Covered in this Report:

- NextEra Energy, Inc.

- Invenergy LLC

- Orsted US Offshore Wind

- General Electric Company

- Vestas Wind Systems A/S

- First Solar, Inc.

- Canadian Solar Inc.

- Sunrun Inc.

- Enphase Energy, Inc.

- Siemens Gamesa Renewable Energy S.A.

- Brookfield Renewable Partners L.P.

- Pattern Energy Group LP

- AES Clean Energy

- Dominion Energy, Inc.

- Duke Energy Renewables

- EDF Renewables North America

- EDP Renewables North America LLC

- Clearway Energy Group LLC

- Mitsubishi Power Americas, Inc.

- Trina Solar Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Extension of Federal Investment & Production Tax Credits

- 4.2.2 Rapid Decline in Solar-PV & Wind LCOE

- 4.2.3 Corporate Net-Zero & RE100 Procurement Targets

- 4.2.4 Inflation Reduction Act-linked Manufacturing Upswing

- 4.2.5 Grid-enhancing Technologies enabling higher renewable penetration

- 4.3 Market Restraints

- 4.3.1 Transmission Bottlenecks & Interconnection Queues

- 4.3.2 Volatility in Commodity Prices for Turbines & Panels

- 4.3.3 Community Opposition to Utility-Scale Projects

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porters Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 PESTLE Analysis

5 Market Size & Growth Forecasts

- 5.1 By Technology

- 5.1.1 Solar Energy (PV and CSP)

- 5.1.2 Wind Energy (Onshore and Offshore)

- 5.1.3 Hydropower (Small, Large, PSH)

- 5.1.4 Bioenergy

- 5.1.5 Geothermal

- 5.1.6 Ocean Energy (Tidal and Wave)

- 5.2 By End-User

- 5.2.1 Utilities

- 5.2.2 Commercial and Industrial

- 5.2.3 Residential

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, JVs, Funding, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Products & Services, Recent Developments)

- 6.4.1 NextEra Energy, Inc.

- 6.4.2 Invenergy LLC

- 6.4.3 Orsted US Offshore Wind

- 6.4.4 General Electric Company

- 6.4.5 Vestas Wind Systems A/S

- 6.4.6 First Solar, Inc.

- 6.4.7 Canadian Solar Inc.

- 6.4.8 Sunrun Inc.

- 6.4.9 Enphase Energy, Inc.

- 6.4.10 Siemens Gamesa Renewable Energy S.A.

- 6.4.11 Brookfield Renewable Partners L.P.

- 6.4.12 Pattern Energy Group LP

- 6.4.13 AES Clean Energy

- 6.4.14 Dominion Energy, Inc.

- 6.4.15 Duke Energy Renewables

- 6.4.16 EDF Renewables North America

- 6.4.17 EDP Renewables North America LLC

- 6.4.18 Clearway Energy Group LLC

- 6.4.19 Mitsubishi Power Americas, Inc.

- 6.4.20 Trina Solar Co., Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

義大利可再生能源:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)西班牙可再生能源:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)

義大利可再生能源:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)西班牙可再生能源:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年) 企業購電協議 (PPA) 平台市場預測至 2034 年—按合約類型、合約期限、能源來源、買方類型、平台模式和地區分類的全球分析海洋溫差發電(OTEC)市場預測—按組件、安裝地點、技術、應用、最終用戶和地區分類的全球分析—2034年農業用電動推進器市場預測至2034年-按系統類型、組件、技術、應用、最終用戶和地區分類的全球分析可再生能源保險:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)

企業購電協議 (PPA) 平台市場預測至 2034 年—按合約類型、合約期限、能源來源、買方類型、平台模式和地區分類的全球分析海洋溫差發電(OTEC)市場預測—按組件、安裝地點、技術、應用、最終用戶和地區分類的全球分析—2034年農業用電動推進器市場預測至2034年-按系統類型、組件、技術、應用、最終用戶和地區分類的全球分析可再生能源保險:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年) 可再生能源市場-全球產業規模、佔有率、趨勢、機會與預測:按類型、最終用途產業、地區和競爭格局分類,2021-2031年混合電池市場-全球產業規模、佔有率、趨勢、機會和預測:按產品類型、額定功率、最終用戶、連接方式、地區和競爭格局分類,2021-2031年東亞可再生能源:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)

可再生能源市場-全球產業規模、佔有率、趨勢、機會與預測:按類型、最終用途產業、地區和競爭格局分類,2021-2031年混合電池市場-全球產業規模、佔有率、趨勢、機會和預測:按產品類型、額定功率、最終用戶、連接方式、地區和競爭格局分類,2021-2031年東亞可再生能源:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年) 可再生能源領域的人工智慧市場:按組件、能源類型、部署模式、最終用戶、國家和地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測

可再生能源領域的人工智慧市場:按組件、能源類型、部署模式、最終用戶、國家和地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測