|

市場調查報告書

商品編碼

1934623

新加坡可再生能源:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Singapore Renewable Energy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

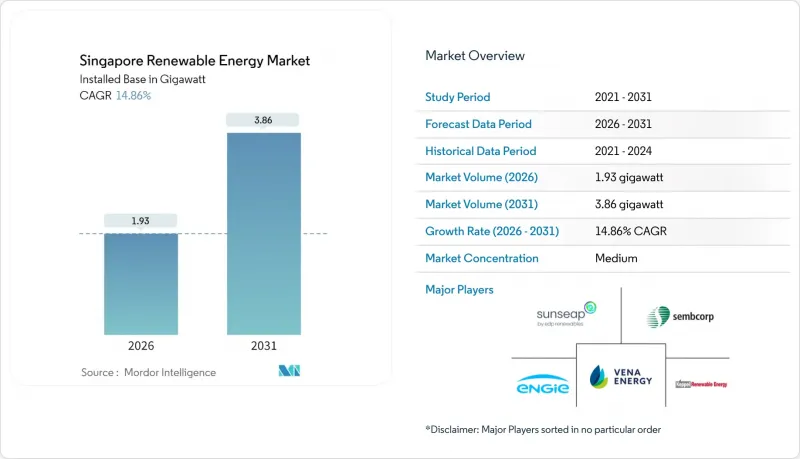

預計到 2026 年,新加坡可再生能源市場規模將達到 1.93 吉瓦。

這意味著從 2025 年的 1.68 吉瓦成長到 2031 年的 3.86 吉瓦,2026 年至 2031 年的年複合成長率(CAGR)為 14.86%。

企業對清潔能源的需求不斷成長、嚴格的淨零排放法規以及全部區域電力進口計畫正在刺激投資。在這個國土面積僅728平方公里的城邦國家,太陽能發電佔據主導地位,其中屋頂式、浮體式和沿海式太陽能系統是最節省空間的選擇。新加坡部署了東南亞最大的285兆瓦時儲能系統,並利用620萬新元的研發津貼開發了太陽能發電預測模型,這些都顯示了電網營運商如何應對間歇性問題。 2035年實現6吉瓦跨區域電力進口的目標,不僅使能源供應來源多元化,也鞏固了新加坡作為跨境清潔能源中心的位置。新加坡快速發展的資料中心叢集對永續性要求的不斷提高,也讓計劃開發商對長期電力需求更有把握。

新加坡可再生能源市場趨勢與展望

2050年淨零排放目標和2030年綠色計畫目標將加速可再生能源的普及。

2050年實現具有法律約束力的淨零排放目標,以及到2035年減少4500萬至5000萬噸二氧化碳當量排放的最新目標,都發出了明確的需求訊號。 2025年2月政策更新後,新加坡立即做出了一項投資10億美元的氫能發電廠(配備碳捕獲功能)的最終投資決定。新增發電裝置容量必須至少包含30%的氫氣,這刺激了技術創新,促進了與可再生的混合利用。能源市場管理局(EMA)將基於排放的競標標準納入電力市場,以降低高碳排放發電的成本。國家氣候變遷秘書處明確的課責機制,已將可再生能源從「自願節能措施」轉變為「監管合規要求」。因此,在新加坡的可再生能源市場中,部署前置作業時間較長的資產,例如浮體式光伏發電和大型儲能系統,可以享受更快的核准速度和更低成本的綠色融資。

由於屋頂太陽輻射過高,對太陽能發電設備的投資減少。

從2024年到2025年,一級組件的資本成本將進一步下降7%,結合新加坡每年1700千瓦時/平方公尺的太陽輻射量,這將顯著提升計劃的經濟效益。政府不會實施上網電價補貼(FIT)制度;取而代之的是,簡化的信用額度系統將允許業主出售多餘的電力,避免繁瑣的官僚程序。 2024年,私營部門將提供新增裝置容量的63.5%,顯示純粹的成本競爭力正在推動太陽能光電的普及。太陽能發電預測結合先進的氣象分析技術,可以降低併網費用並提高內部收益率。由於屋頂光伏租賃的投資回收期通常為15-20年,商業房地產所有者正日益將太陽能光伏發電視為核心基礎設施升級,而非新加坡可再生能源市場中的一項附加ESG(環境、社會和治理)措施。

大型發電設施用地嚴重短缺

新加坡僅23%的面積被劃為工業和基礎設施用地,限制了地面光伏計劃的開發。開發商尋求更長期的土地阻礙因素,以滿足25年的資產使用壽命,但政府機構通常只分配15年或更短的土地。聯合國氣候變遷綱要公約(UNFCCC)將新加坡劃為“替代能源弱勢地區”,凸顯了結構性限制。儘管建築建築幕牆垂直雙面光電陣列和停車座艙罩系統等創新技術能夠為常被忽視的表面提供電力,但其整體貢獻仍有限。因此,新加坡的政策正轉向區域進口,而浮體式光電發電則持續保持新加坡可再生能源市場的成長動能。

細分市場分析

預計到2025年,太陽能發電將佔新加坡總發電量的83.65%,並在2031年之前維持15.38%的複合年成長率,鞏固其作為新加坡可再生能源市場支柱的地位。僅登格水庫、勿洛水庫和班丹水庫的浮體式太陽能發電陣列就能產生超過200兆瓦的電力,而這些電力若要用於其他用途,則需要佔用150至200公頃的寶貴土地。屋頂太陽能系統在工業園區佔據主導地位,利用1580千瓦時/平方公尺的輻照度和雙面組件,以低於電網價格的價格為工廠和資料中心供電。由於平均風速僅2-3公尺/秒,且沿海水域擁擠,風力發電仍受到限制。此外,新加坡地勢平坦,沒有水力發電資源。垃圾焚化發電發電廠每年可處理300萬噸都市固體垃圾,增加150兆瓦的生質能源,並減少掩埋的依賴。地熱能和海洋能目前仍處於探勘階段,低溫差和潮汐範圍小是其發展的障礙。

因此,新加坡除太陽能以外的可再生能源市場佔有率更多是受制於實際需要,而非選擇性多元化。根據一項為期25年的購電協議(PPA),新加坡從寮國進口了100兆瓦的水電,未來預計還將透過從柬埔寨和越南進口低碳能源的方式連接電網。建築一體化光電發電系統在濱海灣金沙等大型開發計劃中日益普及,其建築幕牆安裝的系統符合綠建築標誌認證的要求。預計到2031年,非太陽光電技術的總裝置容量容量佔有率將維持在20%以下。

新加坡可再生能源市場報告按技術(太陽能、風能、水力、生質能源、地熱能和海洋能)和最終用戶(公共產業、商業和工業以及住宅)進行細分。市場規模和預測以裝置容量(吉瓦)為單位。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 透過實現「2050年淨零排放」和「2030年綠色計畫」目標,加速採用可再生能源。

- 儘管屋頂太陽輻射量很高,但對太陽能發電設備的投資卻在下降。

- 企業永續發展措施推動現場太陽能購電協議的實施

- 快速推廣內陸水庫浮體式太陽能發電

- 透過農光互補示範計畫實現稀缺土地的雙重利用

- 超大規模資料中心的快速成長導致對可再生能源認證(REC)的需求激增。

- 市場限制

- 大型發電設施用地嚴重短缺

- 密集網路中的間歇性和電網穩定性挑戰

- 在LTMS-P框架下與低碳電力進口展開競爭

- 廢棄物能源化優先排序後生質能原料的限制

- 供應鏈分析

- 監管環境(政府政策和法規)

- 技術展望

- 波特五力模型

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 產業間競爭

- PESTEL 分析

第5章 市場規模與成長預測

- 透過技術

- 太陽能(光伏和聚光太陽能)

- 風力發電(陸上和海上)

- 水力發電(小規模、大型、抽水蓄能)

- 生質能源

- 地熱

- 海洋能源(潮汐能和波浪能)

- 最終用戶

- 電力公司

- 商業和工業

- 住宅

第6章 競爭情勢

- 市場集中度

- 策略性措施(併購、合資、資金籌措、購電協議)

- 市場佔有率分析(主要企業的市場排名和佔有率)

- 公司簡介

- EDPR Sunseap

- Sembcorp Industries

- Keppel Renewable Energy

- Vena Energy

- ENGIE Southeast Asia

- TotalEnergies Distributed Generation SEA

- Cleantech Solar

- LYS Energy Group

- Terrenus Energy

- SP Group

- Solargy Pte Ltd

- SunPro Energies Pte Ltd

- REC Solar Holdings AS

- Keppel Seghers

- GreenYellow Singapore

- Blueleaf Energy

- Shell Energy Singapore

- JinkoSolar(Singapore)

- Trina Solar APAC

第7章 市場機會與未來展望

Singapore Renewable Energy Market size in 2026 is estimated at 1.93 gigawatt, growing from 2025 value of 1.68 gigawatt with 2031 projections showing 3.86 gigawatt, growing at 14.86% CAGR over 2026-2031.

Rising corporate demand for clean electricity, stringent net-zero rules, and region-wide power import plans are accelerating investment. Solar keeps its dominant role because rooftop, floating, and near-shore deployments are the most space-efficient options in a city-state with only 728 sq km of land. The roll-out of Southeast Asia's largest 285 MWh battery system, together with a solar forecasting model funded by SGD 6.2 million in R&D grants, shows how grid operators are tackling intermittency. Regional import targets of 6 GW by 2035 add supply diversity while anchoring Singapore's position as a cross-border clean-power hub. Intensifying sustainability mandates in the fast-growing data-center cluster further lifts long-term electricity offtake certainty for project developers.

Singapore Renewable Energy Market Trends and Insights

Net-zero 2050 & Green Plan 2030 targets intensifying renewable build-out

Singapore's legally binding net-zero target for 2050 and its updated goal of 45-50 million tCO2e by 2035 create an unambiguous demand signal. A USD 1 billion hydrogen-ready power plant with carbon-capture features reached final investment decision right after the February 2025 policy update. New generation units must now be at least 30% hydrogen-ready, forcing technology upgrades that favor renewable hybrids. The Energy Market Authority (EMA) has embedded emissions-based bidding criteria into its electricity market, tightening the cost of carbon-intensive output. Clear accountability mechanisms from the National Climate Change Secretariat have moved renewables from an optional efficiency gain to a compliance necessity. Long lead-time assets, such as floating solar or utility-scale storage, therefore secure faster permitting and cheaper green financing in the Singapore renewable energy market.

Declining solar-PV CAPEX amid high rooftop irradiance

Capital costs for Tier-1 modules fell another 7% between 2024 and 2025, intersecting with Singapore's steady 1,700 kWh/m2 annual irradiance to sharpen project economics. The government refrains from feed-in tariffs; instead, simplified credit schemes let owners sell excess power without bureaucratic delay. Private sector players delivered 63.5% of new capacity in 2024, proving that pure cost competitiveness now drives uptake. Solar forecasting linked to advanced weather analytics has trimmed balancing charges, lifting internal rates of return. With rooftop leases structured around 15- to 20-year payback horizons, commercial landlords increasingly treat photovoltaics as a core infrastructure upgrade rather than an ESG add-on in the Singapore renewable energy market.

Severe land scarcity for utility-scale assets

Only 23% of Singapore's surface is zoned for industrial or infrastructure use, constraining ground-mount projects. Developers request longer land-lease tenures to match 25-year asset lives, but state agencies often grant parcels for 15 years or less. The UNFCCC label of "alternative-energy-disadvantaged" underscores structural limits. Innovations such as vertical bifacial arrays on building facades and car-park canopy systems squeeze power into overlooked surfaces, yet aggregate contribution remains modest. Therefore, policy pivots to regional imports and floating solar maintains growth momentum in the Singapore renewable energy market.

Other drivers and restraints analyzed in the detailed report include:

- Corporate sustainability pledges pushing onsite solar PPAs

- Rapid roll-out of floating PV on inland reservoirs

- Intermittency & grid-stability challenges in a dense network

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solar supplied 83.65% of 2025 capacity and is tracking a 15.38% CAGR to 2031, cementing its role as the backbone of the Singapore renewable energy market. Floating arrays on Tengeh, Bedok, and Pandan reservoirs alone unlock more than 200 MW that would otherwise require 150-200 ha of scarce land. Roof-mounted systems dominate industrial estates, leveraging 1,580 kWh/m2 irradiance and bifacial modules to deliver sub-grid pricing to factories and data centers. Wind remains marginal given 2-3 m/s average speeds and crowded coastal waters, while domestic hydropower is nonexistent due to flat topography. Waste-to-energy plants add 150 MW of bioenergy, capturing 3 M t of municipal waste and reducing landfill reliance. Geothermal and ocean energy sit in the research phase, hindered by low thermal gradients and minimal tidal ranges.

The Singapore renewable energy market share outside solar is therefore shaped by necessity rather than optional diversification. Hydropower imports from Laos supply 100 MW under a 25-year PPA; future links could arrive from Cambodia and Vietnam via the Low-Carbon Energy Imports Scheme. Building-integrated photovoltaics are gaining traction in marquee developments such as Marina Bay Sands, where facade-mounted systems meet Green Mark mandates. Collectively, non-solar technologies will retain a sub-20% share of installed capacity through 2031.

The Singapore Renewable Energy Market Report is Segmented by Technology (Solar Energy, Wind Energy, Hydropower, Bioenergy, Geothermal, and Ocean Energy) and End-User (Utilities, Commercial and Industrial, and Residential). The Market Sizes and Forecasts are Provided in Terms of Installed Capacity (GW).

List of Companies Covered in this Report:

- EDPR Sunseap

- Sembcorp Industries

- Keppel Renewable Energy

- Vena Energy

- ENGIE Southeast Asia

- TotalEnergies Distributed Generation SEA

- Cleantech Solar

- LYS Energy Group

- Terrenus Energy

- SP Group

- Solargy Pte Ltd

- SunPro Energies Pte Ltd

- REC Solar Holdings AS

- Keppel Seghers

- GreenYellow Singapore

- Blueleaf Energy

- Shell Energy Singapore

- JinkoSolar (Singapore)

- Trina Solar APAC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Net-zero 2050 & Green Plan 2030 targets intensifying renewable build-out

- 4.2.2 Declining solar-PV CAPEX amid high rooftop irradiance

- 4.2.3 Corporate sustainability pledges pushing onsite solar PPAs

- 4.2.4 Rapid roll-out of floating PV on inland reservoirs

- 4.2.5 Agrivoltaic pilots unlocking dual-use of scarce land

- 4.2.6 Surge in REC demand from hyperscale data-centre boom

- 4.3 Market Restraints

- 4.3.1 Severe land scarcity for utility-scale assets

- 4.3.2 Intermittency & grid-stability challenges in a dense network

- 4.3.3 Competition from low-carbon power imports under LTMS-P

- 4.3.4 Limited biomass feedstock after waste-to-energy prioritisation

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape (Government Policies & Regulations)

- 4.6 Technological Outlook

- 4.7 Porters Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

- 4.8 PESTLE Analysis

5 Market Size & Growth Forecasts

- 5.1 By Technology

- 5.1.1 Solar Energy (PV and CSP)

- 5.1.2 Wind Energy (Onshore and Offshore)

- 5.1.3 Hydropower (Small, Large, PSH)

- 5.1.4 Bioenergy

- 5.1.5 Geothermal

- 5.1.6 Ocean Energy (Tidal and Wave)

- 5.2 By End-User

- 5.2.1 Utilities

- 5.2.2 Commercial and Industrial

- 5.2.3 Residential

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, JVs, Funding, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Products & Services, Recent Developments)

- 6.4.1 EDPR Sunseap

- 6.4.2 Sembcorp Industries

- 6.4.3 Keppel Renewable Energy

- 6.4.4 Vena Energy

- 6.4.5 ENGIE Southeast Asia

- 6.4.6 TotalEnergies Distributed Generation SEA

- 6.4.7 Cleantech Solar

- 6.4.8 LYS Energy Group

- 6.4.9 Terrenus Energy

- 6.4.10 SP Group

- 6.4.11 Solargy Pte Ltd

- 6.4.12 SunPro Energies Pte Ltd

- 6.4.13 REC Solar Holdings AS

- 6.4.14 Keppel Seghers

- 6.4.15 GreenYellow Singapore

- 6.4.16 Blueleaf Energy

- 6.4.17 Shell Energy Singapore

- 6.4.18 JinkoSolar (Singapore)

- 6.4.19 Trina Solar APAC

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

2026-2030年全球可再生能源市場

2026-2030年全球可再生能源市場 新一輪石油危機:推動通訊業者轉向可再生能源

新一輪石油危機:推動通訊業者轉向可再生能源 可再生能源市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測

可再生能源市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測 農業可再生能源:生質燃料、太陽能發電廠和永續農業實踐的全球市場—按應用、產品和地區分類的分析和預測(2025-2035 年)

農業可再生能源:生質燃料、太陽能發電廠和永續農業實踐的全球市場—按應用、產品和地區分類的分析和預測(2025-2035 年) 2026年全球可再生能源市場報告2026年全球多元能源系統市場報告2026年全球太陽能燃料市場報告

2026年全球可再生能源市場報告2026年全球多元能源系統市場報告2026年全球太陽能燃料市場報告 可再生能源市場:全球產業分析、市場規模、市場佔有率及預測(依投資類型、可再生能源類型、企業類型、應用、國家及地區分類)-2026-2033年

可再生能源市場:全球產業分析、市場規模、市場佔有率及預測(依投資類型、可再生能源類型、企業類型、應用、國家及地區分類)-2026-2033年 風電場變電站市場按組件類型、配置類型、連接類型、電壓等級、最終用戶和安裝類型分類,全球預測(2026-2032年)全球節能設備市場:機會與策略展望(至2034年)

風電場變電站市場按組件類型、配置類型、連接類型、電壓等級、最終用戶和安裝類型分類,全球預測(2026-2032年)全球節能設備市場:機會與策略展望(至2034年)