|

市場調查報告書

商品編碼

1934660

玻璃瓶和容器:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)Glass Bottles And Containers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

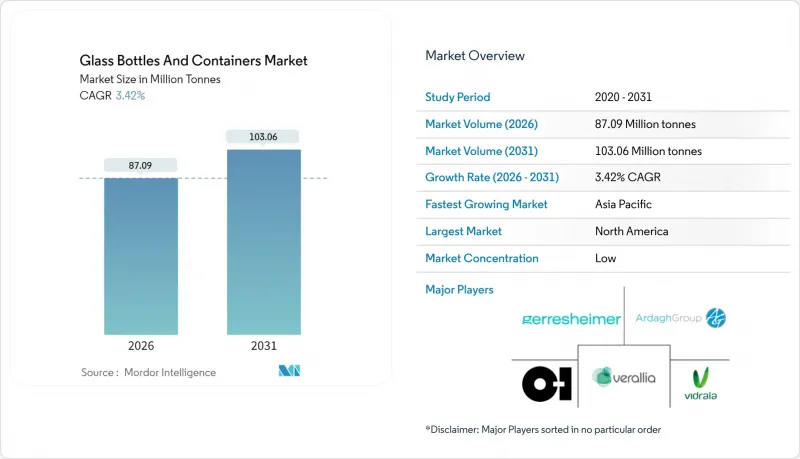

預計玻璃瓶和容器市場將從 2025 年的 8,421 萬噸成長到 2026 年的 8,709 萬噸,到 2031 年將達到 1.0306 億噸,2026 年至 2031 年的複合年成長率為 3.42%。

儘管面臨能源價格上漲、一次性塑膠製品監管趨嚴、美容和酒類飲品行業優質化以及藥品填充和表面處理工程擴張等不利因素,但市場仍保持穩定成長。加州強制減塑65%的塑膠用量以及法國禁止使用聚苯乙烯泡沫塑膠的政策,已經推動了市場對可無限循環利用玻璃的需求。混合熔爐、富氧燃燒技術和高玻璃屑配方降低了成本風險,而像Vidrala公司推出的260克750毫升玻璃瓶這樣的輕量化創新產品,在不影響貨架陳列效果的前提下,減少了材料的使用。製造商也利用顏色差異,特別是琥珀色,來保護對光敏感的藥品和精釀飲品,並強化其相對於其他輕質替代品的價值。

全球玻璃瓶及容器市場趨勢及洞察

塑膠法規推動可回收玻璃包裝轉型

加州SB54法案規定,到2032年一次性塑膠包裝的使用量必須減少65%。法國也將於2025年1月起禁止使用發泡聚苯乙烯食品容器,將促使品牌商轉向玻璃包裝。歐盟正在審議的雙酚A法規也將進一步推動食品接觸應用領域的玻璃包裝轉型。玻璃包裝形成了一個無限閉合迴路,完善的上門回收系統使加工商能夠在滿足新需求的同時,有效吸收設備升級成本。這種連鎖反應在大零售商的飲料和調味品生產線上體現得淋漓盡致,玻璃容器正逐漸回歸市場。儘管玻璃屑供應暫時緊張,但混合熔爐和輕量化技術在一定程度上抵消了利潤率的下降,從而在預測期內保持了持續成長的趨勢。

高階美妝產品中玻璃材質的流行趨勢正在推動對瓶罐的需求。

為了提升產品品質和環保理念,高階護膚和香水品牌正擴大採用玻璃包裝。 Veraria 的 Vista 瓶身採用 100% 回收玻璃 (PCR) 製成,與使用原生原料生產相比,能耗降低了 40%,充分展現了循環經濟與奢華理念的和諧共存。壓紋、漸層色和可重複填充設計增強了商店脫穎而出的視覺效果,也為高價位提供了合理的依據。由於包裝成本在美妝產業的零售價格中所佔比例較小,品牌更容易承受單價上漲,這在一般飲料市場中並不常見。這一趨勢正在全球蔓延,尤其在北美和西歐地區更為顯著,從而帶動了對客製化模具和小批量生產的長期需求。

能源價格波動威脅反應器經濟效益

2024年,英國電價飆升至歷史新高,迫使玻璃製造商在尖峰時段時段停產。能源成本約佔製造成本的18%,因此,在市場價格調整反映之前,價格波動會迅速壓低利潤率。碳定價進一步加劇了石化燃料的消耗,加速了對混合熔爐和自備發電設施的資本投資。同時,儘管OI Glass獲得了1.25億美元的聯邦資金用於脫碳,但規模較小的區域性玻璃廠卻難以融資,這可能導致短期供應減少。

區域分析

到2025年,北美將佔據全球玻璃容器包裝市場55.18%的佔有率,這主要得益於成熟的上門回收系統以及推動高玻璃屑含量的企業永續性目標。玻璃包裝協會提出的2030年達到50%回收率的藍圖,為長期原料供應提供了保障。然而,能源價格波動以及再生PET(rPET)在低價飲料領域的滲透率不斷提高,正在抑制銷售成長,因此策略重點正轉向高階酒類和美容護理領域。

歐洲雖然落後於其他國家,但歐盟80.8%的回收率確保了玻璃屑供應安全,並降低了熔爐的能源需求。 Ardagh和Verallia正在投資建造電力輔助、氫氣熔爐,以維持產量並規避排放交易風險。然而,電價上漲和環境課稅限制了短期利潤,促使企業加強在共用可再生能源微電網和跨境碎玻璃屑交易的合作。

亞太地區是成長最快的地區,預計到2031年將以4.76%的複合年成長率成長,並迅速縮小容器玻璃包裝市場的差距。印度和中國正在建造需要無菌管瓶的新型製藥廠,而韓國和日本則正在進口用於高階護膚品的優質化妝品玻璃。 OI Glass在哥倫比亞錫帕基拉投資1.2億美元的工廠升級項目,體現了生產商致力於在新興地區複製最尖端科技以滿足市場需求並遵守ESG(環境、社會和治理)要求的決心。東南亞部分地區玻璃屑加工基礎設施有限,限制了再生材料的使用,使製造商與西方競爭對手相比處於成本劣勢。然而,收入水準的提高和促進循環經濟的法規的加強預計將支撐強勁的長期需求。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 塑膠禁令推動可回收玻璃包裝轉型

- 奢侈美妝產品中「玻璃」包裝的流行趨勢推動了對瓶罐的需求。

- 藥品填充和表面處理工程的擴展推動了對管瓶的需求。

- 精釀酒精飲料的蓬勃發展帶動了對客製化玻璃容器的需求

- 外商直接投資將用於實施混合爐技術,以擴大綠色玻璃產能。

- ESG合規性推動出口市場邁向高玻璃屑玻璃轉型

- 市場限制

- 能源價格波動威脅爐窯的經濟效益

- 在通路嚴重的配送通路中,採用 rPET 瓶將減少對玻璃容器的需求。

- 薄弱的玻璃屑收集基礎設施限制了再生材料的使用。

- 長途運輸過程中路緣玻璃的破損損失

- 產業供應鏈分析

- 全球容器玻璃熔爐產能及位置

- 工廠選址及投產

- 生產能力

- 爐型

- 所產玻璃的顏色

- 貨櫃玻璃進出口資料-涵蓋主要進出口目的地

- 進口量及進口額(2021-2024 年)

- 出口量和出口額(2021-2024 年)

- 波特五力分析

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

- 原料分析

- 玻璃包裝的回收趨勢

- 玻璃包裝需求與供給分析

第5章 市場規模與成長預測

- 最終用戶

- 飲料

- 酒精飲料

- 啤酒

- 葡萄酒

- 烈酒

- 其他酒精飲料(蘋果酒和其他發酵飲料)

- 非酒精性

- 汁

- 碳酸軟性飲料(CSD)

- 乳製品飲料

- 其他非酒精飲料

- 酒精飲料

- 食品(果醬、果凍、橘子醬、蜂蜜、香腸和調味品、食用油、醃菜)

- 化妝品和個人護理

- 藥品(不含管瓶和安瓿瓶)

- 香水

- 飲料

- 按顏色

- 綠色的

- 琥珀色

- 燧石

- 其他顏色

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 亞太其他地區

- 中東和非洲

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 其他非洲地區

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢與發展

- 公司市佔率分析(基於當前產能)

- 公司簡介

- OI Glass, Inc.

- Verallia SA

- Ardagh Group SA

- Vidrala SA

- Vetropack Holding AG

- Gerresheimer AG

- SGD SA

- Stoelzle Oberglas GmbH

- Wiegand-Glas Holding GmbH

- Hindusthan National Glass & Industries Limited

- Piramal Glass Private Limited

- Nihon Yamamura Glass Co., Ltd.

- Sisecam

- Compagnie de Saint-Gobain SA(Packaging division)

- Heinz-Glas GmbH & Co. KGaA

- Vitro, SAB de CV

- BA Glass BV

- Ciner Glass Holdings Limited

第7章 市場機會與未來展望

The Glass Bottles and Containers market is expected to grow from 84.21 million tonnes in 2025 to 87.09 million tonnes in 2026 and is forecast to reach 103.06 million tonnes by 2031 at 3.42% CAGR over 2026-2031.

Heightened regulatory pressure on single-use plastics, premiumization in beauty and spirits, and pharmaceutical fill-finish expansion are steering steady gains despite energy-price headwinds. California's 65% plastic-reduction mandate and France's polystyrene ban have already swung demand toward infinitely recyclable glass.Hybrid furnaces, oxy-fuel combustion, and high-cullet recipes are mitigating cost exposure, while lightweighting breakthroughs such as Vidrala's 260-gram 75 cl bottle trim material intensity without sacrificing shelf appeal. Producers also leverage color differentiation, especially amber, to protect light-sensitive drugs and craft beverages, reinforcing value over lighter substitutes.

Global Glass Bottles And Containers Market Trends and Insights

Plastic Bans Drive Shift to Recyclable Glass Packaging

California's SB 54 mandates a 65% cut in single-use plastic packaging by 2032, while France has barred expanded polystyrene food containers from January 2025, propelling brand owners to switch to glass. The European Union's pending bisphenol-A restrictions further reinforce conversion in food contact segments. Because glass maintains an endless closed loop and established curb-side collection, converters are capturing new volumes even as they absorb retooling costs. The ripple effect is evident in beverage and condiment lines moving back to glass at big-box retailers. Though cullet supply tightens temporarily, hybrid furnaces and lightweighting partially offset margin compression, paving a sustained uplift through the forecast horizon.

Prestige Beauty "Glassification" Trend Lifts Jar and Bottle Volumes

Luxury skincare and fragrance brands increasingly adopt glass to signal premium quality and environmental stewardship. Verallia's 100% post-consumer-recycled (PCR) Vista bottles cut energy use by 40% versus virgin production, proving that circularity can coexist with high-end aesthetics.Embossing, color gradations, and refillable designs amplify shelf differentiation and justify higher price points. Since packaging cost is a small share of retail value in beauty, brands absorb higher unit costs more easily than mass-market beverages. The trend scales globally but is most pronounced in North America and Western Europe, reinforcing long-tail demand for custom molds and short production runs.

Energy Price Volatility Threatens Furnace Economics

Electricity prices in the United Kingdom spiked to record levels in 2024, compelling glassmakers to idle lines during peak tariffs. Energy constitutes roughly 18% of production costs, so volatility can erase margins faster than price adjustments reach the market. Carbon-pricing schemes further penalize fossil-fuel consumption, intensifying capital commitments toward hybrid furnaces and on-site renewables. In contrast, O-I Glass secured USD 125 million in federal funding for decarbonization, but smaller regional plants face liquidity strains, potentially curbing short-term supply.

Other drivers and restraints analyzed in the detailed report include:

- Pharma Fill-Finish Expansion Boosts Demand for Glass Vials

- Craft Alcohol Boom Spurs Custom Glass Container Demand

- rPET Bottle Adoption Undercuts Glass in Logistics-Sensitive Channels

For complete list of drivers and restraints, kindly check the Table Of Contents.

Geography Analysis

North America captured 55.18% of the container glass packaging market in 2025, leveraging mature curbside collection and corporate sustainability goals that encourage high-cullet recipes. The Glass Packaging Institute's roadmap to reach a 50% recycling rate by 2030 underpins the long-term feedstock base. Yet energy-price swings and growing rPET penetration in value beverages temper volume gains, shifting strategic emphasis toward premium spirits and beauty care.

Europe trails but benefits from the EU's 80.8% recycling rate, which secures cullet and lowers furnace energy demand. Ardagh and Verallia are investing in electric-boost and hydrogen-ready furnaces to hedge carbon-pricing exposure while maintaining output. However, power-price stress and environmental levies suppress near-term margins, sparking collaboration on shared renewable micro-grids and cross-border cullet trade.

Asia Pacific is the fastest-growing region, expanding 4.76% CAGR through 2031 and rapidly closing the gap in the container glass packaging market. India and China build greenfield pharmaceutical plants that require sterile vials, while South Korea and Japan import premium cosmetic glass for luxury skincare. O-I Glass's USD 120 million upgrade in Zipaquira, Colombia, signals how producers replicate best-in-class technology in emerging regions to capture demand while aligning with ESG mandates. Limited cullet infrastructure in parts of Southeast Asia constrains recycled content, creating cost penalties versus Western peers; nevertheless, rising incomes and regulatory push for circularity promise robust long-term demand.

- O-I Glass, Inc.

- Verallia S.A.

- Ardagh Group S.A.

- Vidrala S.A.

- Vetropack Holding AG

- Gerresheimer AG

- SGD S.A.

- Stoelzle Oberglas GmbH

- Wiegand-Glas Holding GmbH

- Hindusthan National Glass & Industries Limited

- Piramal Glass Private Limited

- Nihon Yamamura Glass Co., Ltd.

- Sisecam

- Compagnie de Saint-Gobain S.A. (Packaging division)

- Heinz-Glas GmbH & Co. KGaA

- Vitro, S.A.B. de C.V.

- BA Glass B.V.

- Ciner Glass Holdings Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Plastic Bans Drive Shift to Recyclable Glass Packaging

- 4.2.2 Prestige Beauty "Glassification" Trend Lifts Jar and Bottle Volumes

- 4.2.3 Pharma Fill-Finish Expansion Boosts Demand for Glass Vials

- 4.2.4 Craft Alcohol Boom Spurs Custom Glass Container Demand

- 4.2.5 FDI-Funded Hybrid Furnaces Expand Green Glass Capacity

- 4.2.6 ESG Compliance Spurs Shift to High-Cullet Glass for Export Markets

- 4.3 Market Restraints

- 4.3.1 Energy Price Volatility Threatens Furnace Economics

- 4.3.2 rPET Bottle Adoption Undercuts Glass in Logistics-Sensitive Channels

- 4.3.3 Weak Cullet Collection Infrastructure Limits Recycled Content

- 4.3.4 Breakage Losses in Long-Haul Shipping Discourage Glass Use

- 4.4 Industry Supply-Chain Analysis

- 4.5 Container Glass Furnace Capacity and Locations in Global

- 4.5.1 Plant Locations and Year of Commencement

- 4.5.2 Production Capacities

- 4.5.3 Types of Furnaces

- 4.5.4 Color of Glass Produced

- 4.6 Export-Import Data of Container Glass - Covering Key Import and Export Destinations

- 4.6.1 Import Volume and Value, 2021-2024

- 4.6.2 Export Volume and Value, 2021-2024

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Raw Material Analysis

- 4.9 Recycling Trends for Glass Packaging

- 4.10 Demand vs Supply Analysis for Glass Packaging

5 MARKET SIZE AND GROWTH FORECASTS (VOLUME)

- 5.1 By End-user

- 5.1.1 Beverages

- 5.1.1.1 Alcoholic

- 5.1.1.1.1 Beer

- 5.1.1.1.2 Wine

- 5.1.1.1.3 Spirits

- 5.1.1.1.4 Other Alcoholic Beverages (Cider and Other Fermented Drinks)

- 5.1.1.2 Non-Alcoholic

- 5.1.1.2.1 Juices

- 5.1.1.2.2 Carbonated Drinks (CSDs)

- 5.1.1.2.3 Dairy Product Based Drinks

- 5.1.1.2.4 Other Non-Alcoholic Beverages

- 5.1.1.1 Alcoholic

- 5.1.2 Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles)

- 5.1.3 Cosmetics and Personal Care

- 5.1.4 Pharmaceuticals (excluding Vials and Ampoules)

- 5.1.5 Perfumery

- 5.1.1 Beverages

- 5.2 By Color

- 5.2.1 Green

- 5.2.2 Amber

- 5.2.3 Flint

- 5.2.4 Other Colors

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 South America

- 5.3.2.1 Brazil

- 5.3.2.2 Argentina

- 5.3.2.3 Rest of South America

- 5.3.3 Europe

- 5.3.3.1 United Kingdom

- 5.3.3.2 Germany

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 Rest of Europe

- 5.3.4 Asia Pacific

- 5.3.4.1 China

- 5.3.4.2 Japan

- 5.3.4.3 India

- 5.3.4.4 South Korea

- 5.3.4.5 Australia

- 5.3.4.6 Rest of Asia Pacific

- 5.3.5 Middle East and Africa

- 5.3.5.1 Middle East

- 5.3.5.1.1 United Arab Emirates

- 5.3.5.1.2 Saudi Arabia

- 5.3.5.1.3 Turkey

- 5.3.5.1.4 Rest of Middle East

- 5.3.5.2 Africa

- 5.3.5.2.1 South Africa

- 5.3.5.2.2 Nigeria

- 5.3.5.2.3 Rest of Africa

- 5.3.5.1 Middle East

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves and Developments

- 6.3 Company Market Share Analysis, (Based on Latest Production Capacity)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 O-I Glass, Inc.

- 6.4.2 Verallia S.A.

- 6.4.3 Ardagh Group S.A.

- 6.4.4 Vidrala S.A.

- 6.4.5 Vetropack Holding AG

- 6.4.6 Gerresheimer AG

- 6.4.7 SGD S.A.

- 6.4.8 Stoelzle Oberglas GmbH

- 6.4.9 Wiegand-Glas Holding GmbH

- 6.4.10 Hindusthan National Glass & Industries Limited

- 6.4.11 Piramal Glass Private Limited

- 6.4.12 Nihon Yamamura Glass Co., Ltd.

- 6.4.13 Sisecam

- 6.4.14 Compagnie de Saint-Gobain S.A. (Packaging division)

- 6.4.15 Heinz-Glas GmbH & Co. KGaA

- 6.4.16 Vitro, S.A.B. de C.V.

- 6.4.17 BA Glass B.V.

- 6.4.18 Ciner Glass Holdings Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

非洲玻璃瓶和容器:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)

非洲玻璃瓶和容器:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年) 玻璃瓶和容器市場規模、佔有率和成長分析(按產品、應用、顏色、最終用途產業和地區分類)—產業預測(2026-2033 年)

玻璃瓶和容器市場規模、佔有率和成長分析(按產品、應用、顏色、最終用途產業和地區分類)—產業預測(2026-2033 年) 2025-2029年全球玻璃瓶與容器市場英國玻璃瓶和容器:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)中東和非洲玻璃瓶和容器市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030)亞太地區玻璃瓶和容器:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)拉丁美洲玻璃瓶和容器:市場佔有率分析、行業趨勢和成長預測(2025-2030)歐洲玻璃瓶和容器:市場佔有率分析、行業趨勢和成長預測(2025-2030)

2025-2029年全球玻璃瓶與容器市場英國玻璃瓶和容器:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)中東和非洲玻璃瓶和容器市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030)亞太地區玻璃瓶和容器:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)拉丁美洲玻璃瓶和容器:市場佔有率分析、行業趨勢和成長預測(2025-2030)歐洲玻璃瓶和容器:市場佔有率分析、行業趨勢和成長預測(2025-2030) 玻璃瓶及容器市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

玻璃瓶及容器市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測 全球玻璃瓶和容器市場

全球玻璃瓶和容器市場