|

市場調查報告書

商品編碼

1934581

美國石油和天然氣:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)United States Oil And Gas - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

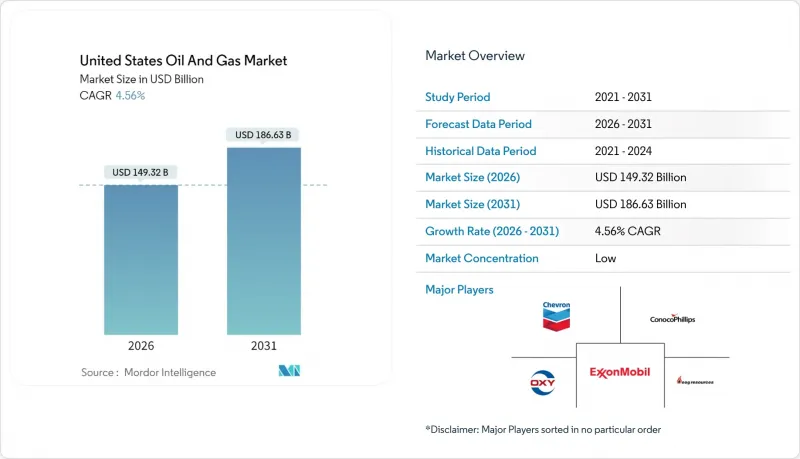

據估計,美國石油和天然氣市場在 2026 年的價值為 1,493.2 億美元,高於 2025 年的 1,428.1 億美元,預計到 2031 年將達到 1,866.3 億美元。

預計2026年至2031年年複合成長率(CAGR)為4.56%。

這一擴張得益於緻密油藏強勁的鑽井產能、墨西哥灣沿岸液化天然氣(LNG)工廠的快速擴張以及成熟盆地技術的穩步推廣。結構性轉變顯而易見,出口導向成長超過了國內需求,預計到2028年將新增150億立方英尺/日的LNG液化產能。儘管上游再投資較為溫和,但效率的提昇在鑽井平台鑽機下降的情況下仍提高了產量。同時,大型併購案將油田集中在二疊紀盆地,透過共用基礎設施降低了成本,並增強了損益平衡能力。

美國油氣市場趨勢與洞察

提高二疊紀盆地緻密油產量

先進的完井設計和人工智慧引導鑽井技術將推動二疊紀盆地的石油產量在2024年達到每日630萬桶,占美國石油總增產的60%,儘管鑽機數量有所下降。更長的水平井段、更高的支撐劑用量以及即時壓裂最佳化技術正在提高單井採收率並降低成本。埃克森美孚收購先鋒公司旨在透過標準化作業和共用基礎設施,進一步提高15%的產能。獨立鑽井公司也正在採用類似的策略以保持競爭力。因此,追求效率是提高產量的基礎,也是保護美國油氣市場免受價格波動影響的有效方法。

液化天然氣出口能力快速成長

墨西哥灣沿岸新建的液化工廠正透過將國內供應與全球價格溢價連結起來,改變市場需求。 Venture Global公司的普拉克明斯終端將於2024年新增2,000萬噸/年的產能,隨後金山口終端也將新增1,560萬噸/年的產能。出口激增推動了阿巴拉契亞盆地和海恩斯維爾盆地的鑽探活動,一條耗資150億美元的新管道將石油輸送到南方。與全球市場更緊密的聯繫將降低亨利港的季節性價格波動,提高生產商和中游運營商的可預測性,並進一步促進美國油氣市場的擴張。

遵守美國環保署 OOOOb/c 甲烷排放法規的成本

自2024年起,甲烷排放超過設定閾值將受到附加稅從每噸900美元起,到2026年將增加至每噸1,500美元。新增的監測和修復項目將使一口典型頁岩油井的營運成本增加每桶2至4美元,對中小型生產商的影響尤其嚴重。合規要求將推動連續洩漏檢測等技術的快速普及,並加速產業整合,從而改變美國油氣市場的成本結構。

細分市場分析

預計到2025年,上游產業將占美國油氣市場的71.85%,並在2031年之前維持4.84%的複合年成長率。中游產業將佔18.40%,這主要得益於管線擴建和LNG接收站的建設;而下游煉油業在產能有限和排放法規日益嚴格的雙重壓力下,將維持9.75%的複合年成長率。目前,營運商的目標是在原油價格為每桶60美元的情況下,實現15%以上的內部收益率,並將資金集中投入高收益頁岩氣水平井和部分長期計劃。康菲石油公司的Willow計劃計劃正是這一轉變的體現,其30年的蘊藏量能夠提供短期頁岩氣專案中罕見的現金流永續性。鑽井效率的提高和審慎的再投資策略,使得上游產業成為美國油氣市場持續成長的核心。

上游產業的主導地位得益於生產效率的快速提升,這使得損益平衡點一直低於每桶40美元。中游產業仍蘊藏著發展機遇,液化天然氣(LNG)的成長帶動了儲存和運輸需求,但資本紀律抑制了投機性計劃。下游產業的利潤率因可再生柴油的競爭和監管成本的上升而不斷下降。這些趨勢共同鞏固了上游產業對美國油氣市場收入趨勢的獨特影響力。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 提高二疊紀盆地緻密油產量

- 液化天然氣出口能力快速成長-(墨西哥灣沿岸地區新建工廠)

- 利用基於人工智慧的地震分析提高獲利油井的產量

- 利用 IRA 45Q 和 45V稅額扣抵抵免降低 CCS 成本

- 企業綠債券資金籌措中游擴張

- 先進塑膠對小眾石油原料的需求

- 市場限制

- 根據美國環保署(EPA)的 OOOOb/c 計算的甲烷排放法規合規成本

- 加強州級的監管(如科羅拉多、新墨西哥州)

- 二疊紀盆地裂縫發育受水應力限制。

- WTI原油與布蘭特原油價格持續存在價差,這對出口產生了負面影響。

- 供應鏈分析

- 監管環境

- 技術展望

- 原油產量和消費量預測

- 天然氣生產與消費預測

- 已安裝管道容量分析

- 非傳統資源資本支出展望(緻密油、油砂、深水)

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- PESTEL 分析

第5章 市場規模與成長預測

- 按行業

- 上游部門

- 中游產業

- 下游產業

- 按地區

- 陸上

- 離岸

- 透過服務

- 建造

- 維護和檢修

- 退休

第6章 競爭情勢

- 市場集中度

- 策略趨勢(併購、聯盟、購電協議)

- 市場佔有率分析(主要企業的市場排名和佔有率)

- 公司簡介

- Exxon Mobil Corp.

- Chevron Corp.

- ConocoPhillips Co.

- EOG Resources Inc.

- Occidental Petroleum Corp.

- Pioneer Natural Resources Co.

- Phillips 66 Co.

- Valero Energy Corp.

- Marathon Petroleum Corp.

- Hess Corp.

- Devon Energy Corp.

- BP PLC

- Shell PLC

第7章 市場機會與未來展望

The United States Oil And Gas Market size in 2026 is estimated at USD 149.32 billion, growing from 2025 value of USD 142.81 billion with 2031 projections showing USD 186.63 billion, growing at 4.56% CAGR over 2026-2031.

Robust drilling productivity in tight-oil plays, the rapid build-out of Gulf Coast LNG trains, and steady technology diffusion into mature basins underpin this expansion. Structural change is evident as export-oriented growth outpaces domestic demand, with 15 billion cubic feet per day of new LNG liquefaction slated by 2028. Upstream reinvestment remains disciplined, yet efficiency gains allow production to rise even as rig counts fall. Meanwhile, mega-mergers concentrate Permian Basin acreage, unlocking shared infrastructure savings that strengthen breakeven resilience.

United States Oil And Gas Market Trends and Insights

Tight-oil Productivity Gains in the Permian

Advanced completion designs and AI-guided drilling lifted Permian Basin output to 6.3 million barrels per day in 2024, representing 60% of total US growth despite a leaner rig fleet. Longer laterals, higher proppant loading, and real-time frac optimization push recovery per well higher while trimming costs. ExxonMobil's integration of Pioneer aims for a further 15% uplift through standardized execution and shared infrastructure. Independent drillers mirror these tactics to remain competitive. Efficiency, therefore, anchors continued output gains that fortify the US oil and gas market against price swings

Surging LNG Export Capacity

New Gulf Coast liquefaction trains reshape demand by linking domestic supply to global price premia. Venture Global's Plaquemines terminal added 20 million tpa capacity in 2024, with Golden Pass to follow at 15.6 million tpa. The export surge boosts Appalachian and Haynesville drilling, while USD 15 billion of new pipelines funnel volumes south. Closer alignment with world markets tempers seasonal Henry Hub volatility, strengthening forward visibility for producers and midstream players, and reinforcing expansion in the US oil and gas market.

Methane-fee Compliance Costs Under EPA OOOOb/c

Beginning in 2024, methane emissions exceeding set thresholds incur fees starting at USD 900 per metric ton and rising to USD 1,500 by 2026. Added monitoring and repair programs raise operating costs by USD 2-4 per barrel for typical shale wells, hitting smaller producers hardest. Compliance demands speed consolidation and quick adoption of technology, such as continuous leak detection, to alter cost structures within the US oil and gas market.

Other drivers and restraints analyzed in the detailed report include:

- AI-driven Seismic Analytics for Marginal Well Recovery

- IRA 45Q & 45V Tax Credits Lowering CCS Costs

- Water-stress Limits on Permian Fracturing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Upstream claimed 71.85% of the US oil and gas market size in 2025 and is on track for a 4.84% CAGR to 2031. Midstream captured 18.40%, buoyed by pipeline additions and LNG terminal build-outs, while downstream refining held 9.75% amid capacity limits and tighter emissions rules. Operators now target internal rates above 15% at USD 60 oil, steering capital toward high-return shale laterals and select long-cycle projects. ConocoPhillips' Willow development illustrates the shift, with 30-year reserves offering cash-flow depth rare in short-cycle shale projects. Drilling efficiency and disciplined reinvestment keep the upstream segment at the center of continued gains in the US oil and gas market.

Upstream's dominance rests on rapid productivity gains that hold costs near sub-USD 40 per barrel breakevens. Midstream remains an opportunity-rich sector as LNG growth drives storage and takeaway needs, yet capital discipline tempers speculative projects. Downstream margins are tightening amid competition from renewable diesel and the cost of regulatory upgrades. Together, these dynamics reinforce the upstream sector's outsized influence on revenue trends within the US oil and gas market.

The United States Oil and Gas Market Report is Segmented by Sector (Upstream, Midstream, and Downstream), Location (Onshore and Offshore), and Service (Construction, Maintenance and Turn-Around, and Decommissioning). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Exxon Mobil Corp.

- Chevron Corp.

- ConocoPhillips Co.

- EOG Resources Inc.

- Occidental Petroleum Corp.

- Pioneer Natural Resources Co.

- Phillips 66 Co.

- Valero Energy Corp.

- Marathon Petroleum Corp.

- Hess Corp.

- Devon Energy Corp.

- BP PLC

- Shell PLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Tight-oil productivity gains in the Permian

- 4.2.2 Surging LNG export capacity -(new Gulf Coast trains)

- 4.2.3 AI-driven seismic analytics for marginal well recovery

- 4.2.4 IRA 45Q & 45V tax credits lowering CCS costs

- 4.2.5 Corporate green-bond funding for midstream build-out

- 4.2.6 Niche petro-feedstock demand from advanced plastics

- 4.3 Market Restraints

- 4.3.1 Methane-fee compliance costs under EPA OOOOb/c

- 4.3.2 Growing state-level setback rules (e.g., CO, NM)

- 4.3.3 Water-stress limits on Permian fracturing

- 4.3.4 Persistent WTI-Brent discount hurting exports

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Crude-Oil Production & Consumption Outlook

- 4.8 Natural-Gas Production & Consumption Outlook

- 4.9 Installed Pipeline Capacity Analysis

- 4.10 Unconventional Resources CAPEX Outlook (tight oil, oil sands, deep-water)

- 4.11 Porter's Five Forces

- 4.11.1 Bargaining Power - Suppliers

- 4.11.2 Bargaining Power - Buyers

- 4.11.3 Threat of New Entrants

- 4.11.4 Threat of Substitutes

- 4.11.5 Competitive Rivalry

- 4.12 PESTLE Analysis

5 Market Size & Growth Forecasts

- 5.1 By Sector

- 5.1.1 Upstream

- 5.1.2 Midstream

- 5.1.3 Downstream

- 5.2 By Location

- 5.2.1 Onshore

- 5.2.2 Offshore

- 5.3 By Service

- 5.3.1 Construction

- 5.3.2 Maintenance and Turn-around

- 5.3.3 Decommissioning

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Exxon Mobil Corp.

- 6.4.2 Chevron Corp.

- 6.4.3 ConocoPhillips Co.

- 6.4.4 EOG Resources Inc.

- 6.4.5 Occidental Petroleum Corp.

- 6.4.6 Pioneer Natural Resources Co.

- 6.4.7 Phillips 66 Co.

- 6.4.8 Valero Energy Corp.

- 6.4.9 Marathon Petroleum Corp.

- 6.4.10 Hess Corp.

- 6.4.11 Devon Energy Corp.

- 6.4.12 BP PLC

- 6.4.13 Shell PLC

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

印度石油和天然氣:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

印度石油和天然氣:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 2026年全球油氣管道及相關結構建設市場報告

2026年全球油氣管道及相關結構建設市場報告 石油和天然氣市場規模、佔有率和成長分析(按產品類型、產業類型、部署類型、應用和地區分類)-2026-2033年產業預測英國石油天然氣:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)越南石油天然氣:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)

石油和天然氣市場規模、佔有率和成長分析(按產品類型、產業類型、部署類型、應用和地區分類)-2026-2033年產業預測英國石油天然氣:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)越南石油天然氣:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年) 日本油氣市場報告:按類型、應用和地區分類(2026-2034年)2026年全球油氣市場報告

日本油氣市場報告:按類型、應用和地區分類(2026-2034年)2026年全球油氣市場報告 石油和天然氣營運維護服務市場(按維護類型、合約類型、資產類型、交付方式、能力、服務供應商和最終用戶行業分類),全球預測,2026-2032年印尼油氣:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)馬來西亞油氣:市場佔有率分析、產業趨勢、統計數據和成長預測(2026-2031)

石油和天然氣營運維護服務市場(按維護類型、合約類型、資產類型、交付方式、能力、服務供應商和最終用戶行業分類),全球預測,2026-2032年印尼油氣:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)馬來西亞油氣:市場佔有率分析、產業趨勢、統計數據和成長預測(2026-2031)