|

市場調查報告書

商品編碼

1911743

電動貨運自行車:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)E-Cargo Bike - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

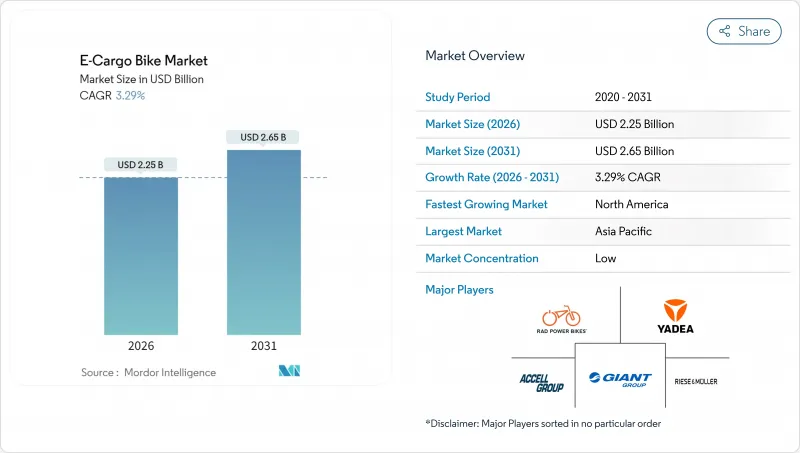

全球電動貨運自行車市場預計將從 2025 年的 21.8 億美元成長到 2026 年的 22.5 億美元,預計到 2031 年將達到 26.5 億美元,2026 年至 2031 年的複合年成長率為 3.29%。

這種穩定成長的趨勢表明,電動貨運自行車正從小眾的微出行產品清晰地轉型為商業物流基礎設施的關鍵組成部分。電池成本的下降、快速的都市化以及日益嚴格的排放法規,共同縮小了電動貨運自行車與傳統貨運自行車的總擁有成本 (TCO) 差距。隨著都市區低排放區限制柴油貨車進入市中心,車隊營運商正轉向電動貨運解決方案,以避免堵塞費並滿足範圍 3 的排放報告義務。企業永續性目標正在加速電動貨運自行車的普及,因為每輛投入使用的電動自行車都能帶來顯著的碳排放和噪音降低。同時,中置馬達和整合式遠端資訊處理系統等組件創新正在擴展商用貨運自行車的功能,提高爬坡性能和車隊運轉率。

全球電動貨運自行車市場趨勢與洞察

最後一公里配送服務的成長

隨著大城市貨物密度持續上升,車隊管理人員正在尋找能夠快速穿梭於狹窄道路和裝卸區的替代方案。物流業者表示,電動貨運車輛在尖峰時段的配送速度比輕型貨車更快,從而減少了日常停車罰款和堵塞費。亞馬遜正在歐洲逐步大規模推廣貨運自行車,顯示解決方案的徵兆遠不止於專業宅配公司。低排放區的擴張也推動了這一趨勢,因為柴油車的准入費用通常高於電動貨運車輛的日常營運成本。更快的配送速度、更低的罰款以及便利的都市區通行條件意味著電動貨運自行車市場在大都會圈配送網路中持續擴張。

政府激勵措施和補貼

財政激勵措施可以簡化車隊管理的採購決策。美國聯邦政府的稅額扣抵涵蓋符合條件的商用電動貨運自行車的購買價格,而德國則為車輛購置提供補貼,並為充電基礎設施建設提供資金。巴黎和哥本哈根等城市提供的補貼也輔以地方政府的退稅,從而縮短了高運轉率營運商的投資回收期。公車專用道優先通行權和車輛總重限制豁免等優惠政策,能夠節省營運成本,進一步增強直接補貼帶來的效益。

與傳統貨運自行車的初始成本比較

與傳統的人力驅動貨車相比,電動驅動系統顯著提高了購買成本。中小企業的租賃選擇有限,且無法透過節省燃料成本快速抵銷資本支出。在許多城市,仍需達到相當長的每週運作時間才能達到收支平衡。金融機構正在推出針對輕型電動車隊的資產支持型產品,但除歐洲和北美以外,其普及程度仍然有限。在資本市場成熟之前,前期成本可能會限制成本敏感地區的快速普及。

細分市場分析

到2025年,輔助騎乘系統將佔據電動貨運自行車市場86.62%的佔有率。這些系統符合歐洲和日本的法律標準,允許在騎乘者踩踏的情況下輸出較高的峰值功率。這種法律上的明確性降低了車隊所有者的保險和執照費用。扭力感測器系統日趨精密,能夠根據負載容量和坡度調整功率輸出,從而延長續航里程。由於北美地區放寬了功率限制,油門輔助系統正以4.12%的複合年成長率成長,但在歐洲主要城市仍面臨嚴格的牌照限制。

需求趨勢凸顯了助力車輛為何將繼續在城市物流領域佔據主導地位。這項技術允許車輛在專用車道內持續行駛,無需遵守車輛法規。由於需要踩踏板,其平均消費量低於節氣門車輛,從而延緩了途中充電的需求。在高密度配送網路中,這種效率,加上監管合規負擔的減輕,最終轉化為更低的總體擁有成本。

預計到2025年,鋰離子電池組將佔總出貨量的72.58%,並在2031年之前保持3.62%的複合年成長率。能量密度的提升已突破250Wh/kg的關口,使得相同續航里程所需的電池組體積更小。電動車供應量的增加刺激了電動貨車車架等次市場的發展,從而形成有利的價格趨勢。磷酸鋰鐵(LFP)電池因其獨特的化學特性,在鋰電池領域正佔據越來越大的佔有率。這種特性具有良好的熱穩定性,受到消防安全監管機構和末端物流保險公司的青睞。

由於價格低廉,鉛酸電池在亞洲入門級市場仍佔有一席之地,車隊營運商通常在兩次更換週期後轉向鋰電池。鋰電池更長的使用壽命減少了五年內的電池更換次數,即使在電價較高的地區,鋰電池也具有總體擁有成本 (TCO) 優勢。增強型電池管理系統整合了電池平衡和溫度切斷功能,提高了安全性並擴大了政府核准。

預計到2025年,中置馬達自行車將佔54.88%的市場佔有率,年複合成長率(CAGR)為3.84%,進一步擴大領先優勢。由於馬達直接與曲柄連接,扭矩透過自行車的傳動系統得到放大,即使在陡坡和重載情況下也能保持動力。均衡的重量分配確保了即使負重也能安全過彎。輪轂式馬達的優點在於平地行駛時能保持良好的牽引力,且維護成本略低,但反覆上坡騎乘時容易產生熱量。

對於頻繁啟停且爬坡路段較短的城市路線,車隊採購者通常選擇中置馬達車型。由於鏈條和齒輪負荷較大,保養週期會略短一些,但營運商願意接受這種權衡,以換取更佳的駕駛性能和更低的每公里電池消費量。

區域分析

到2025年,亞太地區將佔47.55%的收入佔有率,這主要得益於中國強大的供應商生態系統和日本在商用馬達核准方面較為寬鬆的監管政策。當地的原始設備製造商(OEM)正在集中整合電池、馬達和底盤,從而降低單位成本並縮短設計週期。因此,該地區既是生產中心,也是最大的單一需求中心,擁塞收費政策也促進了電動貨運自行車的普及,尤其是在中國的主要城市。

北美將成為成長最快的地區,到2031年複合年成長率將達到6.95%。聯邦稅額扣抵、政府資助的自行車道網路以及消費者對當日送達服務日益成長的期望,都推動了強勁的需求。像UPS和FedEx這樣的營運商正在公佈排放數據,這給董事會帶來了壓力,促使他們從貨車轉向自行車運輸。需求的驅動力不僅在於環保理念,還在於自行車在擁擠的城市中心帶來的實際效益——過去,街頭停車罰單將嚴重影響利潤。

歐洲市場依然成熟,但仍蘊藏著不斷成長的機會。統一的EN 15194認證簡化了跨境車輛部署流程,阿姆斯特丹和柏林等城市允許電動貨運自行車使用公車專用道以及零售店前的裝卸貨區域。清晰的監管環境和完善的基礎設施正在推動市場穩步成長。南美和非洲等新興市場雖然起步較晚,但隨著融資管道的改善和當地組裝廠降低進口關稅,其成長速度可望加快。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 主要行業趨勢

- 年度自行車銷售額

- 平均銷售價格和價格範圍構成

- 電動自行車及其零件的跨境貿易(進口/出口)

- 電動自行車在自行車總銷量中所佔的百分比

- 單程通勤距離 5-15 公里的通勤者 (%)

- 自行車和電動式自行車租賃市場規模

- 電動自行車電池組價格

- 電池化學價格比較

- 最後一公里(超本地化)配送量

- 受保護的自行車道(公里)

- 電動自行車電池容量(瓦時)

- 都市交通壅塞指數

- 法律規範

- 電動自行車型式認證與認可

- 進出口和貿易法規

- 分類、道路使用和使用者規定

- 電池、充電器和充電安全

第5章 市場情勢

- 市場概覽

- 市場促進因素

- 最後一公里配送服務的成長

- 政府激勵措施和補貼

- 鋰離子電池價格正在下降

- 擴大受保護的自行車基礎設施

- 企業永續發展報告面臨壓力

- 利用遠端資訊處理技術最佳化車隊

- 市場限制

- 與傳統貨運自行車相比,初始成本較高

- 載貨能力有限(與貨車相比)

- 充電基礎設施不足

- 零件標準碎片化

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 波特五力模型

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第6章 市場規模及成長預測(價值(美元)及銷售量(單位))

- 依推進類型

- 踏板輔助

- 油門輔助

- 依電池類型

- 鉛酸電池

- 鋰離子電池

- 其他

- 按下馬達安裝位置

- 輪轂(前/後)

- 中置馬達

- 透過驅動系統

- 鏈傳動

- 皮帶傳動

- 透過馬達輸出

- 小於250瓦

- 251-350 W

- 351-500 W

- 501-600 W

- 600瓦或以上

- 按價格範圍

- 最高可達 1,000 美元

- 1,000-1,499 美元

- 1500-2499美元

- 2,500-3,499 美元

- 3,500-5,999 美元

- 超過6000美元

- 按銷售管道

- 線上

- 離線

- 按最終用途

- 商業航運

- 零售和商品分銷

- 食品和飲料配送

- 服務供應商

- 其他

- 商業航運

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 奧地利

- 比利時

- 丹麥

- 法國

- 德國

- 義大利

- 盧森堡

- 荷蘭

- 挪威

- 波蘭

- 西班牙

- 瑞典

- 瑞士

- 英國

- 其他歐洲地區

- 亞太地區

- 澳洲

- 中國

- 印度

- 日本

- 紐西蘭

- 韓國

- 亞太其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 其他中東和非洲地區

- 北美洲

第7章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Accell Group

- Aima Technology Group Co. Ltd

- Bakfiets.nl

- CUBE Bikes

- DOUZE Factory SAS

- Giant Manufacturing Co. Ltd

- Jiangsu Xinri E-Vehicle Co. Ltd

- Jinhua Jobo Technology Co.

- Pedego Electric Bikes

- Pon Holding BV

- Rad Power Bikes Inc.

- Riese & Muller GmbH

- RYTLE GmbH

- Tern Bicycles

- Xtracycle Cargo Bikes

- XYZ CARGO

- Yadea Group Holdings Ltd.

- Yubabikes Inc.

第8章:市場機會與未來展望

第9章:CEO們需要思考的關鍵策略問題

The global e-cargo bike market is expected to grow from USD 2.18 billion in 2025 to USD 2.25 billion in 2026 and is forecast to reach USD 2.65 billion by 2031 at 3.29% CAGR over 2026-2031.

This steady trajectory reflects a clear shift from niche micromobility product to a critical component of commercial logistics infrastructure. Declining battery costs, rapid urbanization, and stricter emissions rules combine to shrink the total cost of ownership gap with conventional cargo cycles. Municipal low-emission zones now block diesel vans from dense downtown cores, so fleet operators turn to e-cargo solutions to avoid congestion fees and meet Scope 3 reporting obligations. Corporate sustainability targets accelerate adoption because every deployed bike delivers a verifiable reduction in carbon and noise. At the same time, component innovation such as mid-drive motors and integrated telematics is expanding the functional envelope of commercial cargo cycling, improving hill-climbing performance and fleet uptime.

Global E-Cargo Bike Market Trends and Insights

Growth of Last-Mile Delivery Services

Package density in large cities keeps rising and pushes fleet managers toward alternatives that navigate narrow streets and loading zones with fewer delays. Logistics operators report that e-cargo units complete peak-hour routes quicker than light vans, cutting routine parking fines and congestion fees. Amazon deployed a significant number of cargo bikes across European countries over time, signaling that the solution now scales beyond courier specialists. Emerging low-emission zones reinforce the trend because diesel entry fees often exceed the daily operating cost of an e-cargo unit. Faster drop times, fewer fines, and urban access privileges ensure that the e-cargo bike market continues to expand within metropolitan fulfillment networks .

Government Incentives and Subsidies

Fiscal instruments make purchase decisions easier for fleet accountants. The United States federal tax credit covers the acquisition price for qualifying commercial cargo e-cycles, while Germany earmarks funds for fleet grants and charging hardware. Cities, including Paris and Copenhagen, layer local rebates on top, trimming the payback horizon for high-utilization operators. Preferential access to bus lanes and exemptions from gross vehicle-weight rules add operational savings that compound the effect of direct subsidies.

High Upfront Cost vs. Conventional Cargo Bikes

Electric drivetrains significantly increase the sticker price compared to traditional human-powered cargo frames. Small businesses often lack leasing options and cannot offset capital expenditure against fuel savings quickly. The break-even point still requires significant operating hours per week in many cities. Financial institutions are gradually rolling out asset-backed products for light electric fleets, but penetration remains limited outside Europe and North America. Until capital markets mature, upfront economics will check rapid diffusion in cost-sensitive regions.

Other drivers and restraints analyzed in the detailed report include:

- Declining Lithium-Ion Battery Prices

- Expansion of Protected Cycling Infrastructure

- Limited Payload Capacity Versus Vans

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Pedal-assist configurations controlled 86.62% of the 2025 e-cargo bike market. The format lines up with European and Japanese legal thresholds that allow higher peak output so long as the rider is pedaling. That legal clarity lowers insurance and license costs for fleet owners. Torque-sensor systems have become more refined, adjusting power delivery by load and gradient to extend range. Throttle-assist bikes are growing at a 4.12% CAGR as North American jurisdictions relax wattage caps, yet the mode still faces tighter licensing in core European cities.

Demand patterns underscore why pedal-assist remains the workhorse for urban logistics. The technology allows continuous operation inside protected lanes without triggering motor-vehicle rules. Because pedal input remains mandatory, average energy consumption is lower than throttle alternatives, delaying mid-route charging stops. For high-density courier networks, that efficiency combines with lighter regulatory compliance to protect the total cost of ownership.

Lithium-ion packs delivered 72.58% of total shipments in 2025 and will retain the crown through 2031 at 3.62% CAGR. Energy density gains now break the 250 Wh/kg barrier, which shrinks pack size for a given range. Rising volumes from electric automotive lines feed secondary markets such as e-cargo frames, driving a favorable pricing glide path. LFP variants are winning share within the lithium family because the chemistry provides thermal stability valued by fire-safety regulators and last-mile insurers.

Lead-acid holds a foothold in entry-level Asian markets due to its low sticker price, yet fleet operators usually migrate to lithium within two replacement cycles. Longer cycle life translates into fewer battery swaps over a five-year horizon, tipping total cost of ownership toward lithium even where electricity prices are high. Enhanced battery management systems now bundle cell-balancing and temperature cutoffs, raising safety credentials and unlocking broader municipal approvals.

Mid-drive layouts secured 54.88% market share in 2025 and should widen the gap by posting a 3.84% CAGR. With the motor linked directly to the crank, torque multiplies through the bicycle drivetrain, preserving power on steep grades and under heavy cargo loads. Balanced weight distribution also means safer cornering with a full load. Hub motors keep traction on flat terrain and carry marginally lower maintenance costs, but face heat build-up when ascending hills repeatedly.

Fleet buyers gravitate toward mid-drive packages for downtown routes that feature frequent stop-start and short but steep climbs. Service intervals are slightly shorter because chains and gears experience higher loads, yet operators accept this trade-off for superior ride dynamics and lower battery drain per kilometer.

The E-Cargo Bike Market Report is Segmented by Propulsion Type (Pedal Assisted, Throttle Assisted), Battery Type (Lead Acid Battery, Lithium-Ion Battery, and More), Motor Placement (Hub (Front/Rear), Mid-Drive), Drive Systems (Chain Drive, Belt Drive), Motor Power (Below 250W, 251-350W, and More), Price Band, Sales Channel, End Use, and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Geography Analysis

Asia-Pacific controlled 47.55% revenue in 2025, thanks to deep supplier ecosystems in China and regulatory headroom in Japan that approves commercial motors. Local OEMs integrate battery, motor, and chassis under one roof, driving down unit cost and shortening design cycles. As a result, the region functions both as a production hub and as the largest single demand center, especially within tier-one Chinese cities where congestion charges now favor electric cargo cycles.

North America is the fastest riser with a 6.95% CAGR to 2031. Federal tax credits, city-funded bike lane networks, and growing consumer expectations for same-day delivery combine to create a strong pull. Operators such as UPS and FedEx openly publish emission dashboards, which adds board-level pressure to pivot from vans to bikes. The environmental narrative pairs with practical advantages in gridlocked downtown cores where curbside parking tickets once ate into profit margins.

Europe maintains a mature yet still expanding opportunity. Harmonized EN 15194 certification streamlines cross-border fleet deployment, and cities such as Amsterdam and Berlin grant e-cargo bikes access to bus lanes plus loading bays outside retail stores. The combination of regulation clarity and extensive infrastructure yields stable growth. Emerging markets in South America and Africa are starting from a low base but could pick up speed once credit facilities mature and local assembly plants lower import duties.

- Accell Group

- Aima Technology Group Co. Ltd

- Bakfiets.nl

- CUBE Bikes

- DOUZE Factory SAS

- Giant Manufacturing Co. Ltd

- Jiangsu Xinri E-Vehicle Co. Ltd

- Jinhua Jobo Technology Co.

- Pedego Electric Bikes

- Pon Holding B.V.

- Rad Power Bikes Inc.

- Riese & Muller GmbH

- RYTLE GmbH

- Tern Bicycles

- Xtracycle Cargo Bikes

- XYZ CARGO

- Yadea Group Holdings Ltd.

- Yubabikes Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Key Industry Trends

- 4.2.1 Annual Bicycle Sales

- 4.2.2 Average Selling Price & Price-Band Mix

- 4.2.3 Cross-Border Trade in E-Bikes & Parts (Imports/Exports)

- 4.2.4 E-Bike Share of Total Bicycle Sales

- 4.2.5 Commuters with 5-15 km One-Way Trips (%)

- 4.2.6 Bicycle/E-Bike Rental Market Size

- 4.2.7 E-Bike Battery Pack Price

- 4.2.8 Battery Chemistry Price Comparison

- 4.2.9 Last-Mile (Hyper-Local) Delivery Volume

- 4.2.10 Protected Bicycle Lanes (km)

- 4.2.11 E-Bike Battery Capacity (Wh)

- 4.2.12 Urban Traffic Congestion Index

- 4.2.13 Regulatory Framework

- 4.2.13.1 Homologation & Certification of E-Bicycles

- 4.2.13.2 Export-Import and Trade Regulation

- 4.2.13.3 Classification, Road Access & User Rules

- 4.2.13.4 Battery, Charger & Charging Safety

5 Market Landscape

- 5.1 Market Overview

- 5.2 Market Drivers

- 5.2.1 Growth of Last-Mile Delivery Services

- 5.2.2 Government Incentives and Subsidies

- 5.2.3 Declining Lithium-Ion Battery Prices

- 5.2.4 Expansion of Protected Cycling Infrastructure

- 5.2.5 Corporate Sustainability Reporting Pressure

- 5.2.6 Telematics-Enabled Fleet Optimization

- 5.3 Market Restraints

- 5.3.1 High Upfront Cost vs. Conventional Cargo Bikes

- 5.3.2 Limited Payload Capacity Versus Vans

- 5.3.3 Gaps in Charging Infrastructure

- 5.3.4 Fragmented Component Standards

- 5.4 Value / Supply-Chain Analysis

- 5.5 Regulatory Landscape

- 5.6 Technological Outlook

- 5.7 Porter's Five Forces

- 5.7.1 Threat of New Entrants

- 5.7.2 Bargaining Power of Suppliers

- 5.7.3 Bargaining Power of Buyers

- 5.7.4 Threat of Substitutes

- 5.7.5 Competitive Rivalry

6 Market Size & Growth Forecasts (Value (USD) and Volume (Units))

- 6.1 By Propulsion Type

- 6.1.1 Pedal Assisted

- 6.1.2 Throttle Assisted

- 6.2 By Battery Type

- 6.2.1 Lead Acid Battery

- 6.2.2 Lithium-ion Battery

- 6.2.3 Others

- 6.3 By Motor Placement

- 6.3.1 Hub (Front/Rear)

- 6.3.2 Mid-Drive

- 6.4 By Drive Systems

- 6.4.1 Chain Drive

- 6.4.2 Belt Drive

- 6.5 By Motor Power

- 6.5.1 Below 250 W

- 6.5.2 251-350 W

- 6.5.3 351-500 W

- 6.5.4 501-600 W

- 6.5.5 Above 600 W

- 6.6 By Price Band

- 6.6.1 Up to USD 1,000

- 6.6.2 USD 1,000-1,499

- 6.6.3 USD 1,500-2,499

- 6.6.4 USD 2,500-3,499

- 6.6.5 USD 3,500-5,999

- 6.6.6 Above USD 6,000

- 6.7 By Sales Channel

- 6.7.1 Online

- 6.7.2 Offline

- 6.8 By End Use

- 6.8.1 Commercial Delivery

- 6.8.1.1 Retail and Goods Delivery

- 6.8.1.2 Food and Beverage Delivery

- 6.8.2 Service Providers

- 6.8.3 Others

- 6.8.1 Commercial Delivery

- 6.9 By Geography

- 6.9.1 North America

- 6.9.1.1 United States

- 6.9.1.2 Canada

- 6.9.1.3 Mexico

- 6.9.2 South America

- 6.9.2.1 Brazil

- 6.9.2.2 Argentina

- 6.9.2.3 Rest of South America

- 6.9.3 Europe

- 6.9.3.1 Austria

- 6.9.3.2 Belgium

- 6.9.3.3 Denmark

- 6.9.3.4 France

- 6.9.3.5 Germany

- 6.9.3.6 Italy

- 6.9.3.7 Luxembourg

- 6.9.3.8 Netherlands

- 6.9.3.9 Norway

- 6.9.3.10 Poland

- 6.9.3.11 Spain

- 6.9.3.12 Sweden

- 6.9.3.13 Switzerland

- 6.9.3.14 United Kingdom

- 6.9.3.15 Rest of Europe

- 6.9.4 Asia-Pacific

- 6.9.4.1 Australia

- 6.9.4.2 China

- 6.9.4.3 India

- 6.9.4.4 Japan

- 6.9.4.5 New Zealand

- 6.9.4.6 South Korea

- 6.9.4.7 Rest of Asia-Pacific

- 6.9.5 Middle East and Africa

- 6.9.5.1 Saudi Arabia

- 6.9.5.2 United Arab Emirates

- 6.9.5.3 South Africa

- 6.9.5.4 Rest of the Middle East and Africa

- 6.9.1 North America

7 Competitive Landscape

- 7.1 Market Concentration

- 7.2 Strategic Moves

- 7.3 Market Share Analysis

- 7.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 7.4.1 Accell Group

- 7.4.2 Aima Technology Group Co. Ltd

- 7.4.3 Bakfiets.nl

- 7.4.4 CUBE Bikes

- 7.4.5 DOUZE Factory SAS

- 7.4.6 Giant Manufacturing Co. Ltd

- 7.4.7 Jiangsu Xinri E-Vehicle Co. Ltd

- 7.4.8 Jinhua Jobo Technology Co.

- 7.4.9 Pedego Electric Bikes

- 7.4.10 Pon Holding B.V.

- 7.4.11 Rad Power Bikes Inc.

- 7.4.12 Riese & Muller GmbH

- 7.4.13 RYTLE GmbH

- 7.4.14 Tern Bicycles

- 7.4.15 Xtracycle Cargo Bikes

- 7.4.16 XYZ CARGO

- 7.4.17 Yadea Group Holdings Ltd.

- 7.4.18 Yubabikes Inc.

8 Market Opportunities & Future Outlook

9 Key Strategic Questions for E-Bikes CEOs

電動貨運自行車市場分析及預測(至2035年):類型、產品、服務、技術、組件、應用、最終用戶、功能、安裝類型、模式

電動貨運自行車市場分析及預測(至2035年):類型、產品、服務、技術、組件、應用、最終用戶、功能、安裝類型、模式 電動貨運自行車市場預測至2034年-全球分析(按自行車類型、馬達類型、電池類型、負載能力、應用、最終用戶和地區分類)

電動貨運自行車市場預測至2034年-全球分析(按自行車類型、馬達類型、電池類型、負載能力、應用、最終用戶和地區分類) 2026年全球電動貨運自行車市場報告

2026年全球電動貨運自行車市場報告 全球電動貨運自行車市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球電動貨運自行車市場規模、佔有率、趨勢和成長分析報告(2026-2034) 電動貨運自行車市場:按類型、負載容量、驅動系統、電池類型、電壓、最終用戶、應用和分銷管道分類-2026-2032年全球市場預測

電動貨運自行車市場:按類型、負載容量、驅動系統、電池類型、電壓、最終用戶、應用和分銷管道分類-2026-2032年全球市場預測 歐洲電動貨運自行車市場-佔有率分析、產業趨勢與統計、成長預測(2026-2031)

歐洲電動貨運自行車市場-佔有率分析、產業趨勢與統計、成長預測(2026-2031) 電動貨運自行車市場規模、佔有率和成長分析(按電池類型、推進方式、產品類型和地區分類)-2026-2033年產業預測

電動貨運自行車市場規模、佔有率和成長分析(按電池類型、推進方式、產品類型和地區分類)-2026-2033年產業預測 全球電動貨運自行車市場

全球電動貨運自行車市場 電動貨物摩托車的全球市場:產品類型·電池類型·驅動方式·模式·距離·最高速度·負載容量·用途·不同地區的預測 (~2032年)

電動貨物摩托車的全球市場:產品類型·電池類型·驅動方式·模式·距離·最高速度·負載容量·用途·不同地區的預測 (~2032年)