|

市場調查報告書

商品編碼

1911449

印度通訊平台即服務 (CPaaS) 市場佔有率分析、行業趨勢、統計數據和成長預測 (2026-2031)India Communication Platform As A Service (CPaaS) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

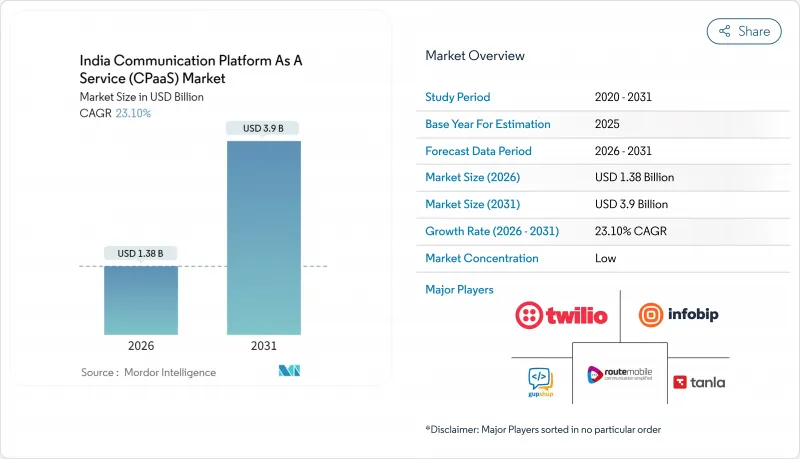

印度通訊平台即服務 (CPaaS) 市場預計將從 2025 年的 11.2 億美元成長到 2026 年的 13.8 億美元,預計到 2031 年將達到 39 億美元,2026 年至 2031 年的複合年成長率為 23.1%。

即時支付、主權雲端指令以及 5G 網路和 API 整合等因素共同推動可程式通訊成為企業經營團隊的優先事項,從而促進了企業採用率的激增。在銀行、金融服務和保險 (BFSI) 領域,身分驗證和詐欺通知、利用 WhatsApp 和 RCS 的全通路功能以及低程式碼開發工具的應用案例是成長要素。混合雲端的採用、生成式人工智慧功能以及行業特定的合規性要求正在重塑競爭策略。傳統技術堆疊的實施複雜性、A2P 簡訊定價的波動以及增強的資料安全監控仍然是主要障礙。

印度通訊平台即服務 (CPaaS) 市場趨勢與洞察

為最大限度減少資本支出,對計量收費模式的需求不斷成長

付費使用制正在重塑採購方式,印度企業更傾向於採用可變營運支出而非固定電信資本支出。利潤微薄的中小型企業在幾週內即可採用通訊平台即服務 (CPaaS),並利用「數位印度」計畫提供的雲端採用補貼和部署簡化服務。這種模式提高了成本透明度,釋放了用於核心營運的資金,並可在無需重新談判合約的情況下應對季節性流量高峰。大型企業也非常重視將支出與宣傳活動效果關聯起來的詳細分析,這加速了印度零售和物流業對通訊平台即服務 (CPaaS) 市場的接受度。供應商也積極回應,發布透明定價並捆綁免費開發者積分,進一步降低了進入門檻。

全通路互動(WhatsApp 和 RCS)採用率激增

WhatsApp Business API 在印度擁有 4.87 億用戶,使其成為 2024 年客戶服務和商務領域不可或缺的工具。然而,2025 年 7 月實施的價格調整增加了整體擁有成本,促使品牌商將 RCS 整合到其交易流程中。 RCS 在 Android 系統上提供原生已讀回執、已驗證的發送方 ID 和富媒體卡片,其功能可與 OTT 應用媲美,且無需擔心專有技術鎖定。與一家大型電商公司進行的初步試點表明,RCS 的點擊率比簡訊高出 30%,印度通訊平台即服務 (CPaaS) 市場正朝著多通路整合方向發展。 CPaaS 平台現在整合了路由邏輯,可根據成本、送達率和使用者偏好最佳化頻道選擇,從而確保在頻道中斷時服務的連續性。

異構遺留堆疊中的實作複雜度

大型企業通常混合使用大型主機時代的ERP系統、客製化CRM系統和專有中介軟體,這些系統無法原生支援現代REST或gRPC端點。因此,CPaaS部署需要適配器、佇列層和資料映射,從而推高了計劃預算。相關人員可能會發現隱藏的技術債務,例如嵌入在單體代碼庫中的硬編碼簡訊閘道器,導致專案週期超出最初的商業計劃。資料保護法的合規性審核要求對每一次資料跳轉進行可追溯,這進一步增加了工程開銷。隨著探索研討會揭示記錄系統的局限性,CPaaS即插即用的概念逐漸消退,變更管理成為成功的關鍵因素。

細分市場分析

中小企業發展勢頭強勁,預計到2031年將實現24.1%的複合年成長率,而大型企業在2025年仍維持著67.12%的收入佔有率。成本匹配的計量收費合約、捆綁式模板以及政府Start-Ups培養箱正在消除准入門檻,使中小企業無需電信資本支出即可提供企業級體驗。旅遊和零售等季節性產業在假日期間使用量激增,這反映了印度通訊平台即服務(CPaaS)市場靈活的收費模式。同時,大型企業正在數百個部門擴展全通路平台,並將人工智慧驅動的個人化引擎與客戶關係管理系統(CRM)整合,以提高提升銷售轉換率。大規模推動了批量折扣合約的簽訂,並成為供應商收入的基礎,但由於多層管治和資料居住要求,實施仍然十分複雜。

銀行、金融和保險 (BFSI) 以及醫療保健行業日益嚴格的合規措施正在推動向混合架構的轉變,這種架構在利用公共雲端進行尖峰負載平衡的同時,透過主權區域路由受監管的資料。 Copilot(一款客服中心負責人的生成式人工智慧)的先導計畫顯示,平均處理時間實現了兩位數的提升,這表明通訊平台即服務 (CPaaS) 的市場佔有率正在不斷成長。與此同時,中小企業 (SME) 正在利用低程式碼建構器來建立 WhatsApp 店鋪和自動計費機器人,將開發週期從數月縮短至數週。這種可程式通訊的普及化正在將印度通訊平台即服務 (CPaaS) 市場的管道從大都會圈擴展到二線創業叢集。

到2025年,銀行、金融和保險(BFSI)行業將佔總收入的28.22%。監管部門對動態密碼密碼(OTP)、電子授權委託書提醒、詐欺通知等的要求,對資訊的可靠送達提出了極高的要求。為了遵守印度儲備銀行關於即時客戶溝通的指令,各銀行正在實施多通路冗餘(簡訊、推播通知、應用程式內通知)。人工智慧增強型聊天機器人能夠對日常諮詢進行分類,並將人工客服僅分配給複雜案例,從而降低支援成本並提高客戶滿意度。符合資料本地化法規的自主雲端平台必不可少,這不僅縮小了供應商的選擇範圍,也提高了人們對服務品質的期望。

物流板塊以24.6%的複合年成長率領跑,主要得益於電子商務的成長和國家物流政策的數位化目標。即時貨物可視性、司機協調和異常處理依賴事件驅動型API,這些API透過簡訊、RCS和語音管道傳輸更新資訊。統一物流介面平台的標準化促進了互通性,並強化了以API為中心的框架的需求。倉庫營運商正在部署物聯網感測器和CPaaS警報系統,以產生自動補貨訊息,從而最佳化供應鏈閉迴路。隨著遠端醫療和全通路行銷的成熟,醫療保健零售板塊保持了穩定擴張,但其成長速度並未跟上物流板塊高度垂直整合的步伐。

其他福利

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 為最大限度減少資本支出,對計量收費模式的需求不斷成長

- 全通路互動(WhatsApp 和 RCS)採用率激增

- 企業級低程式碼/API主導的數位轉型

- 印度儲備銀行推動即時支付,為關鍵任務通訊API 提供動力

- 主權雲端服務的興起使得合規的CPaaS部署成為可能。

- 開放 5G 網路 API 將創造新的可程式通訊用例

- 市場限制

- 跨異構遺留技術棧的實作複雜度

- 網路攻擊事件的增加引發了人們對安全和資料隱私的擔憂。

- 各州電信監管法規分散,增加了合規成本。

- 批發A2P簡訊價格的波動對通訊業者的利潤率帶來壓力。

- 監管環境

- 技術展望

- 波特五力分析

- 買方的議價能力

- 供應商的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 定價和經營模式分析

- 主要趨勢

- 產業生態系分析

- 純粹的CPaaS提供商

- 通訊業者主導的CPaaS供應商

- 企業級 CPaaS 供應商

- 基於服務供應商的 CPaaS 整合商

- 宏觀經濟因素如何影響市場

第5章 市場規模與成長預測

- 按公司規模

- 中小企業

- 主要企業

- 按最終用戶行業分類

- 資訊科技和電信

- BFSI

- 零售與電子商務

- 衛生保健

- 政府和公共部門

- 物流/運輸

- 其他

- 透過通訊管道

- SMS

- 聲音的

- WhatsApp Business

- RCS 商業通訊

- 視訊 API

- 電子郵件

- 推播通知

- 按部署模式

- 公共雲端

- 混合雲端

- 本地部署

- 透過 CPaaS 功能

- 通訊API

- 語音 API

- 視訊 API

- 身份驗證和安全 API

- 全通路編配API

- 按地區

- 印度北部

- 西印度群島

- 南印度

- 印度東部和東北部

- 印度中部

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Twilio Inc.

- Tanla Platforms Limited

- Route Mobile Limited

- Gupshup Technology India Private Limited

- Infobip Ltd.

- Sinch AB

- MessageBird BV

- Vonage Holdings Corp.

- Telnyx LLC

- Plivo Inc.

- Netcore Cloud Private Limited

- Exotel Techcom Pvt. Ltd.

- EnableX.io Pte Ltd.

- Tata Communications Limited(Kaleyra)

- Bharti Airtel Limited(Airtel IQ)

- Bandwidth Inc.

- Link Mobility Group ASA

- ValueFirst Digital Media Private Limited(Tanla)

- Karix Mobile Private Limited

- CM.com NV

- Clickatell Inc.

- Unifonic Inc.

第7章 市場機會與未來展望

The India CPaaS market is expected to grow from USD 1.12 billion in 2025 to USD 1.38 billion in 2026 and is forecast to reach USD 3.9 billion by 2031 at 23.1% CAGR over 2026-2031.

Enterprise adoption surged as real-time payments, sovereign-cloud mandates, and 5G network-API exposure converged to make programmable communication a board-level priority. BFSI use cases for authentication and fraud alerts, omnichannel engagement on WhatsApp and RCS, and low-code development tooling are among the strongest growth catalysts. Hybrid-cloud deployments, generative-AI features, and industry-specific compliance requirements are reshaping competitive strategies. Implementation complexity across legacy stacks, volatile A2P SMS pricing, and heightened data-security scrutiny remain the chief obstacles.

India Communication Platform As A Service (CPaaS) Market Trends and Insights

Rising Demand for Pay-Per-Use Model to Minimise Capital Spending

Consumption-based pricing is redefining procurement as Indian organizations prefer variable opex over fixed telecom capex commitments. SMEs with thin margins implement CPaaS in weeks, riding Digital India incentives that subsidize cloud usage and streamline onboarding. The model improves cost visibility, releases cash for core operations, and supports seasonal traffic spikes without renegotiating contracts. Enterprises also value granular analytics that correlate spend with campaign performance, accelerating adoption of the India CPaaS market across retail and logistics sectors. Vendors are responding by publishing transparent rate cards and bundling free developer credits, lowering the entry barrier even further.

Exponential Surge in Omnichannel Engagement (WhatsApp and RCS) Adoption

WhatsApp Business API's audience of 487 million Indian users made it indispensable for customer service and commerce in 2024. Pricing revisions enacted in July 2025, however, raised the total cost of ownership, nudging brands to integrate RCS for transactional flows. RCS offers read receipts, verified sender IDs, and rich cards natively on Android, delivering parity with over-the-top apps minus proprietary lock-in. Early pilots by large e-commerce firms show 30% higher click-through than SMS, pushing the India CPaaS market toward multi-channel orchestration. CPaaS platforms now embed routing logic that optimizes channel selection by cost, deliverability, and user preference, ensuring continuity if one path fails.

Implementation Complexity Across Heterogeneous Legacy Stacks

Large enterprises often juggle mainframe-era ERPs, custom CRMs, and proprietary middleware that cannot natively consume modern REST or gRPC endpoints. CPaaS rollouts, therefore, require adapters, queuing layers, and data-mapping that inflate project budgets. Stakeholders may discover hidden technical debt, such as hard-coded SMS gateways embedded in monolithic codebases, extending timelines beyond initial business-case assumptions. Compliance audits under the Data Protection Act mandate traceability of every data hop, adding further engineering overhead. The perception that CPaaS is plug-and-play fades once discovery workshops reveal system-of-record constraints, making change management a critical success factor.

Other drivers and restraints analyzed in the detailed report include:

- Low-Code/API-Led Digital Transformation Across Enterprises

- RBI Real-Time-Payments Push Boosting Mission-Critical Messaging APIs

- Security and Data-Privacy Concerns Amid Rising Cyber-Attacks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

SMEs added momentum by posting a 24.1% CAGR through 2031 while large enterprises retained 67.12% revenue share in 2025. Cost-aligned pay-per-use contracts, bundled templates, and government start-up incubators remove entry barriers, allowing small firms to offer enterprise-grade experiences without telecom capex. Seasonal businesses in travel and retail spike usage during festival periods, showcasing the elastic billing models that define the India CPaaS market. In parallel, large enterprises scale omnichannel platforms across hundreds of departments, integrating AI-driven personalization engines with CRMs to enhance upsell conversions. Their sizeable traffic yields volume-discounted contracts that anchor vendor revenues, even as implementation remains complex due to multilayer governance and data residency requirements.

Heightened compliance defenses in BFSI and healthcare push many corporates toward hybrid architectures that route regulated data through sovereign zones while leveraging public cloud for peak offload. Pilot projects with generative-AI copilots for call-center agents exhibit double-digit improvements in average handling time, signaling further wallet-share gains for CPaaS. SMEs, meanwhile, tap low-code builders to craft WhatsApp storefronts and automated invoicing bots, shrinking development cycles from months to weeks. This democratization of programmable communications enlarges the India CPaaS market funnel beyond metro hubs into Tier-2 entrepreneurship clusters.

BFSI accounted for 28.22% of 2025 revenue as regulatory mandates for OTP, e-mandate alerts, and fraud notifications demand ultra-reliable delivery. Banks deploy multi-channel redundancy, SMS, push, and in-app to meet Reserve Bank circulars stipulating real-time customer communication. AI-enriched chatbots now triage routine queries, reserving human agents for complex cases, trimming support costs, and bolstering customer satisfaction. Sovereign-cloud platforms that satisfy data-localization statutes are prerequisites, narrowing vendor selection and heightening service-quality expectations.

Logistics recorded the fastest 24.6% CAGR, propelled by e-commerce growth and the National Logistics Policy's digitization targets. Real-time shipment visibility, driver coordination, and exception handling rely on event-driven APIs that stream updates across SMS, RCS, and voice channels. Unified Logistics Interface Platform standards spur interoperability, reinforcing demand for API-centric frameworks. Warehouse operators explore IoT sensors tied to CPaaS alerts, generating automated replenishment messages that tighten supply-chain loops. Healthcare and retail maintain steady expansion as telemedicine and omnichannel marketing mature, yet their growth trails the hyper-vertical momentum seen in logistics.

The India Communication Platform As A Service (CPaaS) Market is Segmented by Organization Size (Small and Medium Enterprises and Large Enterprises), End-User Industry (IT and Telecom, BFSI, and More), Communication Channel (SMS, Voice, and More), Deployment Model (Public Cloud, Hybrid Cloud, and On-Premise), Cpaas Function (Messaging API, Voice API, and More), and Region. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Twilio Inc.

- Tanla Platforms Limited

- Route Mobile Limited

- Gupshup Technology India Private Limited

- Infobip Ltd.

- Sinch AB

- MessageBird B.V.

- Vonage Holdings Corp.

- Telnyx LLC

- Plivo Inc.

- Netcore Cloud Private Limited

- Exotel Techcom Pvt. Ltd.

- EnableX.io Pte Ltd.

- Tata Communications Limited (Kaleyra)

- Bharti Airtel Limited (Airtel IQ)

- Bandwidth Inc.

- Link Mobility Group ASA

- ValueFirst Digital Media Private Limited (Tanla)

- Karix Mobile Private Limited

- CM.com N.V.

- Clickatell Inc.

- Unifonic Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for pay-per-use model to minimise capital spending

- 4.2.2 Exponential surge in omnichannel engagement (WhatsApp and RCS) adoption

- 4.2.3 Low-code/API-led digital transformation across enterprises

- 4.2.4 RBI real-time-payments push boosting mission-critical messaging APIs

- 4.2.5 Emergence of sovereign-cloud offerings enabling compliant CPaaS uptake

- 4.2.6 5G network-API exposure creating new programmable-communication use-cases

- 4.3 Market Restraints

- 4.3.1 Implementation complexity across heterogeneous legacy stacks

- 4.3.2 Security and data-privacy concerns amid rising cyber-attacks

- 4.3.3 Fragmented state-level telecom rules raising compliance cost

- 4.3.4 Volatile telco A2P-SMS wholesale pricing squeezing margins

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Buyers

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Pricing and Business-Model Analysis

- 4.8 Key Trends

- 4.9 Industry Ecosystem Analysis

- 4.9.1 Pure-Play CPaaS Providers

- 4.9.2 Telco-Driven CPaaS Providers

- 4.9.3 Enterprise-Grade CPaaS Providers

- 4.9.4 Service-Provider-Based CPaaS Integrators

- 4.10 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Organisation Size

- 5.1.1 Small and Medium Enterprises (SMEs)

- 5.1.2 Large Enterprises

- 5.2 By End-user Industry

- 5.2.1 IT and Telecom

- 5.2.2 BFSI

- 5.2.3 Retail and E-commerce

- 5.2.4 Healthcare

- 5.2.5 Government and Public Sector

- 5.2.6 Logistics and Transportation

- 5.2.7 Other End-user Industries

- 5.3 By Communication Channel

- 5.3.1 SMS

- 5.3.2 Voice

- 5.3.3 WhatsApp Business

- 5.3.4 RCS Business Messaging

- 5.3.5 Video API

- 5.3.6 Email

- 5.3.7 Push Notifications

- 5.4 By Deployment Model

- 5.4.1 Public Cloud

- 5.4.2 Hybrid Cloud

- 5.4.3 On-premise

- 5.5 By CPaaS Function

- 5.5.1 Messaging API

- 5.5.2 Voice API

- 5.5.3 Video API

- 5.5.4 Verification and Security API

- 5.5.5 Omnichannel Orchestration API

- 5.6 By Region

- 5.6.1 North India

- 5.6.2 West India

- 5.6.3 South India

- 5.6.4 East and North-East India

- 5.6.5 Central India

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Twilio Inc.

- 6.4.2 Tanla Platforms Limited

- 6.4.3 Route Mobile Limited

- 6.4.4 Gupshup Technology India Private Limited

- 6.4.5 Infobip Ltd.

- 6.4.6 Sinch AB

- 6.4.7 MessageBird B.V.

- 6.4.8 Vonage Holdings Corp.

- 6.4.9 Telnyx LLC

- 6.4.10 Plivo Inc.

- 6.4.11 Netcore Cloud Private Limited

- 6.4.12 Exotel Techcom Pvt. Ltd.

- 6.4.13 EnableX.io Pte Ltd.

- 6.4.14 Tata Communications Limited (Kaleyra)

- 6.4.15 Bharti Airtel Limited (Airtel IQ)

- 6.4.16 Bandwidth Inc.

- 6.4.17 Link Mobility Group ASA

- 6.4.18 ValueFirst Digital Media Private Limited (Tanla)

- 6.4.19 Karix Mobile Private Limited

- 6.4.20 CM.com N.V.

- 6.4.21 Clickatell Inc.

- 6.4.22 Unifonic Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

通訊平台即服務 (CPaaS) 市場規模、佔有率和成長分析:按服務類型、企業規模、應用領域、最終用戶產業、銷售管道和地區分類-2026-2033 年產業預測

通訊平台即服務 (CPaaS) 市場規模、佔有率和成長分析:按服務類型、企業規模、應用領域、最終用戶產業、銷售管道和地區分類-2026-2033 年產業預測 通訊平台即服務 (CPaaS) 市場:按最終用戶產業和地區分類

通訊平台即服務 (CPaaS) 市場:按最終用戶產業和地區分類 2026年全球通訊平台(MaaP)市場報告

2026年全球通訊平台(MaaP)市場報告 通訊平台即服務 (CPaaS) 市場預測至 2034 年—按組件、通訊管道、部署模式、企業規模、應用程式、最終用戶和地區分類的全球分析電信平台即服務 (TPaaS) 市場預測至 2034 年—按組件、部署模式、平台類型、企業用例、最終用戶和區域分類的全球分析

通訊平台即服務 (CPaaS) 市場預測至 2034 年—按組件、通訊管道、部署模式、企業規模、應用程式、最終用戶和地區分類的全球分析電信平台即服務 (TPaaS) 市場預測至 2034 年—按組件、部署模式、平台類型、企業用例、最終用戶和區域分類的全球分析 通訊平台即服務 (CPaaS) 市場:2026 年至 2032 年全球市場預測(按服務類型、部署模式、組織規模、應用程式和最終用戶分類)

通訊平台即服務 (CPaaS) 市場:2026 年至 2032 年全球市場預測(按服務類型、部署模式、組織規模、應用程式和最終用戶分類) 通訊平台即服務 (CPaaS) 市場規模、佔有率、趨勢和預測:按組件、企業規模、行業和地區分類,2026-2034 年2026年全球通訊平台即服務(CPaaS)市場報告

通訊平台即服務 (CPaaS) 市場規模、佔有率、趨勢和預測:按組件、企業規模、行業和地區分類,2026-2034 年2026年全球通訊平台即服務(CPaaS)市場報告 CPaaS(通訊平台即服務):市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031 年)

CPaaS(通訊平台即服務):市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031 年) CPaaS(通訊平台即服務)市場規模、佔有率和成長分析(按部署類型、公司規模、垂直產業和地區分類)-2026-2033年產業預測

CPaaS(通訊平台即服務)市場規模、佔有率和成長分析(按部署類型、公司規模、垂直產業和地區分類)-2026-2033年產業預測