|

市場調查報告書

商品編碼

1910613

延展實境(XR):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Extended Reality (XR) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

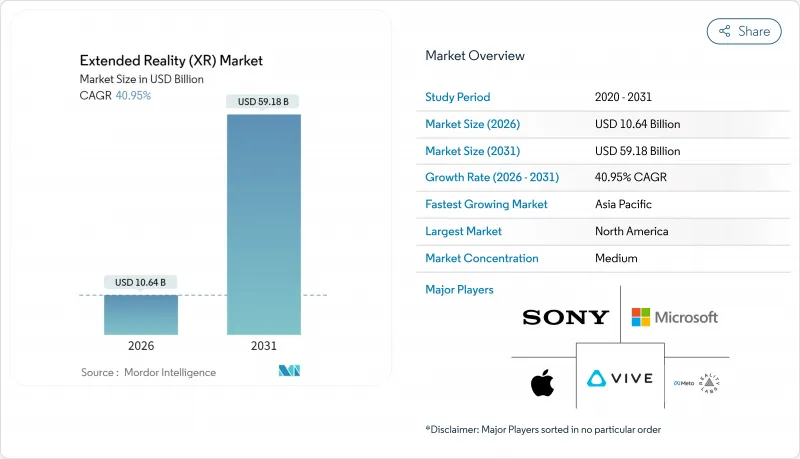

預計到 2026 年,延展實境(XR) 市場規模將達到 106.4 億美元。

這意味著從 2025 年的 75.5 億美元成長到 2031 年的 591.8 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 40.95%。

XR技術在製造業、醫療保健和國防領域的快速企業應用,其發展速度已超越消費娛樂領域,使其從遊戲新奇玩意轉變為必不可少的生產力工具。 5G行動網路與邊緣運算的結合,正在消除延遲障礙,使毫秒精度的可視化在工廠車間和手術室等場所實用化。嵌入空間運算的人工智慧正在實現培訓內容的個人化,而即時分析則正在完善反饋循環,從而進一步提升可衡量的盈利。美國和中國的政府資助,以及OpenXR等開放標準的推行,正在加速生態系統的成熟,並緩解人們對廠商鎖定的擔憂。供應鏈限制和不斷上漲的零件價格仍然是阻礙因素,但隨著新的半導體產能和替代材料來源投入生產,這些挑戰正在逐步緩解。

全球延展實境(XR)市場趨勢與洞察

擴展 5G 覆蓋範圍和邊緣運算的協同效應

低於 20 毫秒的低延遲使得多人 VR 協作無需背負式設備即可實現,愛立信、AT&T、Dreamscape 和高通的試驗均證實了這一點。中國鋼鐵集團公司 (CSCC) 的 5G 虛擬工廠參觀整合了來自 85 個生產節點的即時數據,展現了其在重工業領域的價值。 DHL 的智慧眼鏡試驗表明,即時揀貨指導能夠提高物流效率。將運算能力轉移到網路邊緣可以減輕設備重量,從而提升使用者舒適度。為此,通訊業者正在用戶 50 公里範圍內部署微型資料中心,以維持身臨其境型體驗的流暢性。

加強XR技術與數位雙胞胎和工業4.0框架的融合

和碩的 PEGAVERSE 基於 NVIDIA Omniverse 建造了五個虛擬工廠,實現了遠距離診斷和場景測試,從而減少了停機時間和現場訪問次數。BASF的 AR 賦能工廠規劃將感測器數據與身臨其境型視覺化相結合,能夠更有效率地識別危險。西門子和SONY推出的 SRH-S1 工程頭戴式顯示器,用於實現像素級精確的設計協作,售價 4,750 美元。 OpenUSD 整合可以將不同的 CAD、PLM 和物聯網資料來源整合到單一的空間層。平台供應商透過訂閱式視覺化服務而非一次性授權費來獲利。

高清光學元件和處理器的初始成本很高

鎵和鍺的供不應求導致光學設備價格上漲高達25%。 Meta公司的Reality Labs自2020年以來已累計虧損600億美元,而其2024年第四季的XR硬體銷售額僅為11億美元,凸顯了盈利方面的挑戰。缺乏資金或投資收益率(ROI)的小型公司對進入市場持謹慎態度。雲端渲染的XR技術雖然降低了設備負載,但會增加延遲,因此其應用範圍僅限於5G網路覆蓋良好的地區。

細分市場分析

儘管硬體在2024年將構成比營收的53.2%,但服務業務的成長速度最快,複合年成長率將達到42.5%。將設備、軟體和管理支援結合的訂閱方案模式,能夠將資本支出(CapEx)轉化為營運支出(OpEx),因此備受財務部門青睞。這種轉變不僅為供應商創造了可預測的經常性收入,也降低了客戶的進入門檻。 Meta的平台轉型正是這一趨勢的體現,該公司正在探索企業訂閱模式,並將其與硬體更新換代相結合。

由於對專業內容的需求,託管式培訓和模擬服務的單價很高。光是Vertex Solutions就已在全球範圍內交付了500多台軍用級模擬器,充分展現了其垂直領域的專業實力。這些合約通常為期多年,使供應商能夠獲得較高的終身價值。硬體製造商擴大選擇與整合商合作,而非直接競爭,這反映了以服務主導的延展實境(XR)市場日趨成熟。

頭戴式顯示器在2024年佔總營收的42.7%,但成長重心正轉向空間和全像顯示器,預計複合年成長率將達到43.1%。共用顯示牆克服了個人頭戴式顯示器在衛生和舒適度方面的局限性,並支援協作式工程評審和客戶演示。三星的「Project Moohan」就是一個很好的例子,它是一款針對工業部署最佳化的下一代獨立式設備。

無需配戴眼鏡的解決方案也正在湧現;Distance Technologies公司已籌集1,000萬歐元(約1,173萬美元),旨在將車輛車窗改造為動態混合實境畫布。智慧型手機連接的手持設備在現場維護中仍然十分常見,抬頭顯示器)也在飛機和汽車駕駛座中找到了應用領域。從長遠來看,像XPANCEO的原型產品這樣的智慧隱形眼鏡可能會將延展實境(XR)市場推向隱形穿戴裝置領域。

延展實境(XR) 市場按產品/服務(硬體、軟體、服務)、裝置類型(頭戴式顯示器(有線、獨立式)、抬頭顯示器等)、技術(虛擬實境 (VR)、擴增實境(AR)、混合實境(MR))和終端用戶產業(遊戲與娛樂、醫療保健與生命科學等)進行細分。市場預測以美元計價。

區域分析

在北美,受醫療、航太和國防領域持續採購的推動,XR設備的安裝基礎正在不斷擴大。 Infinite Reality公司籌集了3.5億美元的新資金,並以4.5億美元收購了Landvault公司,這印證了投資者對空間運算平台的樂觀態度。美國創新部門在空軍基地部署了225套身臨其境型訓練設備,進一步鞏固了XR技術在企業中的應用。隨著模擬器精度逐漸接近實體駕駛座標準,航空領域對替代認證的監管支援正在推動設備訂單的成長。

亞太地區發展最為快速。光是中國一國,到2024年就將推出超過100個VR計劃。韓國正利用近乎全國覆蓋的5G網路,為三星的「Project Moohan」計畫做準備。在印度,Meta和HCLTech合作建立的公私合營培養箱正在扶持基層應用開發。龐大的製造業基礎為持續的價值驗證試點計畫提供了支持,使亞太地區成為大眾硬體經濟的核心參與者。歐洲正努力成為負責任創新的中心。 Distance Technologies獲得的1000萬歐元(約1173萬美元)種子輪資金籌措表明,市場對汽車級混合實境表面有著巨大的需求。BASF、西門子和SONY正在合作研發符合嚴格CE安全標準的頭戴式設備。歐盟的隱私法規正在影響資料處理架構,並鼓勵全球供應商建立符合GDPR的分析模組。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 擴展 5G 覆蓋範圍和邊緣運算的協同效應

- 將XR技術日益融入數位雙胞胎與工業4.0框架

- 企業對身臨其境型遠距培訓的需求日益成長

- 將空間感測器整合到大眾市場智慧型手機中

- 政府對元宇宙相關研究與發展(R&D)的資助

- 採用開放的XR標準可以減少廠商鎖定。

- 市場限制

- 高清光學元件和處理器的初始成本很高

- 使用者穩定性不足和人體工學限制

- 眼動追蹤追蹤與手部偵測分析中的資料隱私挑戰

- 內容創作工具的生態系支離破碎

- 供應鏈分析

- 監管環境

- 技術展望

- 波特五力模型

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 對影響市場的宏觀經濟因素進行評估

第5章 市場規模與成長預測

- 報價

- 硬體

- 軟體

- 服務

- 依設備類型

- 頭戴式顯示器(有線和獨立式)

- 抬頭顯示器

- 手持行動裝置

- 其他

- 透過技術

- 虛擬實境(VR)

- 擴增實境(AR)

- 混合實境(MR)

- 按最終用戶行業分類

- 遊戲與娛樂

- 醫療保健和生命科學

- 工業和製造業

- 零售與電子商務

- 教育和培訓

- 航太/國防

- 建築、工程及施工

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 其他歐洲

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 澳洲

- 亞太其他地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 埃及

- 其他非洲地區

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Meta Platforms Inc.(Reality Labs)

- Sony Group Corp.

- Microsoft Corp.

- Apple Inc.

- HTC Corp.(Vive)

- Qualcomm Technologies Inc.

- Samsung Electronics Co. Ltd.

- Alphabet Inc.(Google XR)

- Pico Interactive Inc.(ByteDance)

- Varjo Technologies Oy

- Magic Leap Inc.

- Nvidia Corp.

- Unity Technologies Inc.

- Vuzix Corp.

- Lenovo Group Ltd.

- Snap Inc.

- Niantic Inc.

- Ultraleap Ltd.

- HP Inc.

- Immersion Corp.

第7章 市場機會與未來展望

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 擴展 5G 覆蓋範圍和邊緣運算的協同效應

- 將XR技術日益融入數位雙胞胎與工業4.0框架

- 企業對身臨其境型遠距培訓的需求日益成長

- 將空間感測器整合到大眾市場智慧型手機中

- 政府對元宇宙相關研究與發展(R&D)的資助

- 採用開放的XR標準可以減少廠商鎖定。

- 市場限制

- 高清光學元件和處理器的初始成本很高

- 使用者穩定性不足和人體工學限制

- 眼動追蹤追蹤與手部偵測分析中的資料隱私挑戰

- 內容創作工具的生態系支離破碎

- 供應鏈分析

- 監管環境

- 技術展望

- 波特五力模型

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 對影響市場的宏觀經濟因素進行評估

第5章 市場規模與成長預測

- 報價

- 硬體

- 軟體

- 服務

- 依設備類型

- 頭戴式顯示器(有線和獨立式)

- 抬頭顯示器

- 手持行動裝置

- 其他

- 透過技術

- 虛擬實境(VR)

- 擴增實境(AR)

- 混合實境(MR)

- 按最終用戶行業分類

- 遊戲與娛樂

- 醫療保健和生命科學

- 工業和製造業

- 零售與電子商務

- 教育和培訓

- 航太/國防

- 建築、工程及施工

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 其他歐洲

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 澳洲

- 亞太其他地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 埃及

- 其他非洲地區

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Meta Platforms Inc.(Reality Labs)

- Sony Group Corp.

- Microsoft Corp.

- Apple Inc.

- HTC Corp.(Vive)

- Qualcomm Technologies Inc.

- Samsung Electronics Co. Ltd.

- Alphabet Inc.(Google XR)

- Pico Interactive Inc.(ByteDance)

- Varjo Technologies Oy

- Magic Leap Inc.

- Nvidia Corp.

- Unity Technologies Inc.

- Vuzix Corp.

- Lenovo Group Ltd.

- Snap Inc.

- Niantic Inc.

- Ultraleap Ltd.

- HP Inc.

- Immersion Corp.

第7章 市場機會與未來展望

Extended Reality market size in 2026 is estimated at USD 10.64 billion, growing from 2025 value of USD 7.55 billion with 2031 projections showing USD 59.18 billion, growing at 40.95% CAGR over 2026-2031.

Rapid enterprise adoption across manufacturing, healthcare, and defense now outpaces consumer entertainment, turning XR from a gaming novelty into a mission-critical productivity tool. Five-generation mobile networks paired with edge computing have erased latency barriers, making millisecond-accurate visualization practical on factory floors and in surgical suites. Artificial intelligence embedded in spatial computing personalizes training content while real-time analytics close feedback loops, further raising measurable returns. Government funding in the United States and China, coupled with open standards such as OpenXR, is accelerating ecosystem maturity and reducing vendor lock-in worries. Supply chain constraints and component price inflation remain headwinds but continue to ease as new semiconductor capacity and alternative material sourcing enter production.

Global Extended Reality (XR) Market Trends and Insights

Expanding 5G Coverage and Edge Computing Synergy

Sub-20 ms latency now enables multi-user VR collaboration without tethered backpack PCs, as trials by Ericsson, AT&T, Dreamscape, and Qualcomm have shown. China Steel Corporation's 5G-enabled virtual factory tours integrate live data from 85 production nodes, proving value for heavy industry. DHL smart-glasses pilots illustrate logistics gains from real-time pick guidance. Device weight drops as compute moves to the network edge, boosting shift-length comfort. Telcos therefore place micro-data-centers within 50 km of users to sustain immersive throughput.

Increased Integration of XR into Digital Twin and Industry 4.0 Frameworks

Pegatron's PEGAVERSE builds five virtual factories on NVIDIA Omniverse for remote diagnostics and scenario testing, lowering downtime and travel. BASF's AR-enabled plant planning links sensor data with immersive visualization to streamline hazard identification. Siemens and Sony priced the SRH-S1 engineering headset at USD 4,750 to deliver pixel-accurate design collaboration. OpenUSD alignment lets disparate CAD, PLM, and IoT feeds merge into a single spatial layer. Platform vendors thus monetize subscription-based visualization rather than one-off license fees.

High Upfront Costs of High-Fidelity Optics and Processors

Gallium and germanium shortages have inflated optics prices by up to 25%. Meta's Reality Labs has accumulated USD 60 billion losses since 2020 while selling USD 1.1 billion in Q4 2024 XR hardware, underscoring profitability challenges. Smaller firms hesitate without capital or clear ROI. Cloud-rendered XR lightens devices yet introduces latency trade-offs that limit usage to well-served 5G zones.

Other drivers and restraints analyzed in the detailed report include:

- Rising Enterprise Demand for Immersive Remote Training

- Mass-Market Smartphone Integration of Spatial Sensors

- User Motion-Sickness and Ergonomic Limitations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware controlled 53.2% of revenue in 2024, yet Services is set to grow fastest at 42.5% CAGR. Subscription bundles that combine devices, software, and managed support convert capex into opex, a structure favored by finance departments. The shift drives predictable recurring income for suppliers and lowers barrier-to-entry for customers. Meta's platform pivot illustrates this movement, exploring enterprise-grade subscriptions alongside hardware refreshes.

Managed training and simulation services command premium rates thanks to specialized content needs. Vertex Solutions alone shipped more than 500 military-grade simulators worldwide, highlighting vertical expertise. As these contracts often span multi-year periods, vendors capture higher lifetime value. Hardware makers therefore partner with integrators rather than compete head-on, reflecting a maturing services-led Extended Reality market.

Head-Mounted Displays captured 42.7% revenue in 2024 but growth now shifts to Spatial and Holographic Displays, which head toward a 43.1% CAGR. Shared viewing walls overcome hygiene and comfort limits found in personal headsets, supporting collaborative engineering reviews and customer demonstrations. Samsung's Project Moohan exemplifies next-generation standalone units optimized for industrial deployment.

Glasses-free solutions also emerge, with Distance Technologies raising EUR 10 million (USD 11.73 million) to transform vehicle windows into dynamic mixed-reality canvases. Smartphone-tethered handheld devices remain common in field maintenance, while head-up displays secure niche positions in aviation and automotive cockpits. Longer term, smart contact lenses such as XPANCEO's prototype could push the Extended Reality market into invisible wearables.

Extended Reality (XR) Market is Segmented by Offering (Hardware, Software, Services), Device Type (Head-Mounted Displays (Tethered, Stand-Alone), Head-Up Displays and More), Technology (Virtual Reality (VR), Augmented Reality (AR), Mixed Reality (MR)), End User Industry (Gaming and Entertainment Healthcare and Life Sciences, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America's installed base expands through steady healthcare, aerospace, and defense procurement. Infinite Reality closed USD 350 million in new capital and bought Landvault for USD 450 million, underscoring investor optimism in spatial computing platforms. The US Defense Innovation Unit fielded 225 immersive trainers across Air Force sites, further entrenching enterprise XR usage. Regulatory support for alternative certification in aviation spurs equipment orders as simulator fidelity approaches physical cockpit standards.

Asia-Pacific scales fastest. China alone launched more than 100 VR projects in 2024. South Korea readies Samsung's Project Moohan release, leveraging the country's near-universal 5G coverage. India's public-private incubator with Meta and HCLTech cultivates grassroots application developers. Wide manufacturing bases feed continuous proof-of-value pilots, making APAC pivotal to hardware volume economics. Europe positions itself as the responsible innovation hub. Distance Technologies' EUR 10 million (USD 11.73 million) seed illustrates appetite for automotive-grade mixed-reality surfaces. BASF, Siemens, and Sony collaborate on engineering headsets that comply with strict CE safety norms. The EU's privacy regime shapes data-handling architectures, influencing global vendors to build GDPR-ready analytics modules.

- Meta Platforms Inc. (Reality Labs)

- Sony Group Corp.

- Microsoft Corp.

- Apple Inc.

- HTC Corp. (Vive)

- Qualcomm Technologies Inc.

- Samsung Electronics Co. Ltd.

- Alphabet Inc. (Google XR)

- Pico Interactive Inc. (ByteDance)

- Varjo Technologies Oy

- Magic Leap Inc.

- Nvidia Corp.

- Unity Technologies Inc.

- Vuzix Corp.

- Lenovo Group Ltd.

- Snap Inc.

- Niantic Inc.

- Ultraleap Ltd.

- HP Inc.

- Immersion Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expanding 5G coverage and edge computing synergy

- 4.2.2 Increased integration of XR into digital twin and Industry 4.0 frameworks

- 4.2.3 Rising enterprise demand for immersive remote-training

- 4.2.4 Mass-market smartphone integration of spatial sensors

- 4.2.5 Government funding for metaverse-related Rand

- 4.2.6 Adoption of open XR standards lowering vendor lock-in

- 4.3 Market Restraints

- 4.3.1 High upfront costs of high-fidelity optics and processors

- 4.3.2 User motion-sickness and ergonomic limitations

- 4.3.3 Data-privacy gaps in eye- and hand-tracking analytics

- 4.3.4 Fragmented content-authoring tool ecosystem

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assesment of Macroeconomic Factors on the market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Offering

- 5.1.1 Hardware

- 5.1.2 Software

- 5.1.3 Services

- 5.2 By Device Type

- 5.2.1 Head-Mounted Displays (Tethered, Stand-alone)

- 5.2.2 Head-Up Displays

- 5.2.3 Handheld and Mobile Devices

- 5.2.4 Others

- 5.3 By Technology

- 5.3.1 Virtual Reality (VR)

- 5.3.2 Augmented Reality (AR)

- 5.3.3 Mixed Reality (MR)

- 5.4 By End-user Industry

- 5.4.1 Gaming and Entertainment

- 5.4.2 Healthcare and Life Sciences

- 5.4.3 Industrial and Manufacturing

- 5.4.4 Retail and E-commerce

- 5.4.5 Education and Training

- 5.4.6 Aerospace and Defense

- 5.4.7 Architecture, Engineering and Construction

- 5.4.8 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Egypt

- 5.5.5.2.4 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Meta Platforms Inc. (Reality Labs)

- 6.4.2 Sony Group Corp.

- 6.4.3 Microsoft Corp.

- 6.4.4 Apple Inc.

- 6.4.5 HTC Corp. (Vive)

- 6.4.6 Qualcomm Technologies Inc.

- 6.4.7 Samsung Electronics Co. Ltd.

- 6.4.8 Alphabet Inc. (Google XR)

- 6.4.9 Pico Interactive Inc. (ByteDance)

- 6.4.10 Varjo Technologies Oy

- 6.4.11 Magic Leap Inc.

- 6.4.12 Nvidia Corp.

- 6.4.13 Unity Technologies Inc.

- 6.4.14 Vuzix Corp.

- 6.4.15 Lenovo Group Ltd.

- 6.4.16 Snap Inc.

- 6.4.17 Niantic Inc.

- 6.4.18 Ultraleap Ltd.

- 6.4.19 HP Inc.

- 6.4.20 Immersion Corp.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

2026年全球擴增實境(XR)內容低程式碼建構器市場報告

2026年全球擴增實境(XR)內容低程式碼建構器市場報告 XR(延展實境)硬體的演進2026年全球擴增實境培訓市場報告2026年全球擴增實境晶片系統(XR SoC)市場報告

XR(延展實境)硬體的演進2026年全球擴增實境培訓市場報告2026年全球擴增實境晶片系統(XR SoC)市場報告 擴增實境(XR)市場規模、佔有率、趨勢和預測:按類型、最終用途和地區分類,2026-2034年

擴增實境(XR)市場規模、佔有率、趨勢和預測:按類型、最終用途和地區分類,2026-2034年 擴增實境(XR)顯示市場:按連接方式、設備類型、顯示技術、技術和最終用戶分類-2026-2032年全球市場預測

擴增實境(XR)顯示市場:按連接方式、設備類型、顯示技術、技術和最終用戶分類-2026-2032年全球市場預測 全球XR市場(2026-2036年)2026年建築業延展實境(XR)全球市場報告擴增實境(XR)市場:按組件、技術、設備類型、產業和企業規模分類-2026-2032年全球市場預測2026年全球個人擴增實境硬體市場報告

全球XR市場(2026-2036年)2026年建築業延展實境(XR)全球市場報告擴增實境(XR)市場:按組件、技術、設備類型、產業和企業規模分類-2026-2032年全球市場預測2026年全球個人擴增實境硬體市場報告