|

市場調查報告書

商品編碼

1910568

地板材料:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Floor Covering - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

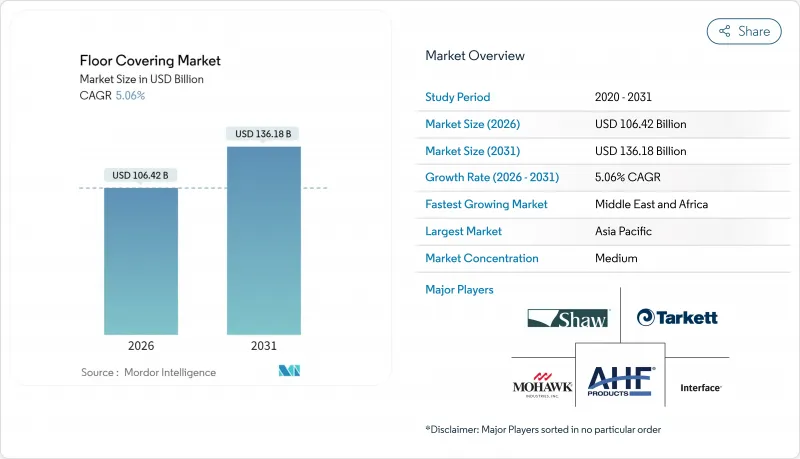

2025 年地板材料市場價值為 1,012.8 億美元,預計從 2026 年的 1,064.2 億美元成長到 2031 年的 1,361.8 億美元,在預測期(2026-2031 年)內複合年成長率為 5.06%。

北美強勁的住宅維修需求、亞太地區的大規模計劃活動以及中東酒店業的復甦,都推動了對高品質、耐用地板材料的需求。諸如硬芯防水地板和無PVC彈性地板材料等創新產品拓寬了地板的應用範圍,使供應商能夠在不大幅犧牲設計的情況下,滿足從潮濕地下室到人流量大的商業走廊等各種場所的需求。製造商正在擴大其在美國的生產規模,以規避關稅風險、縮短前置作業時間並遵守更嚴格的VOC排放法規。這項策略也有助於增強供應鏈抵禦國際運輸中斷的能力。電子商務正在透過整合擴增實境(商店)視覺化工具和直接面對消費者的物流模式,改變購買流程,推動家居裝潢連鎖店採用虛擬設計諮詢和線上訂購線下取貨服務。競爭差異化正在轉向環境認證,再生材料含量、回收項目正成為企業採購規範的關鍵要素,而LEED、BREEAM和WELL標準也成為常規參考標準。

全球地板材料市場趨勢與洞察

快速的都市化和蓬勃發展的維修活動

預計到2025年,光是印度的城市人口就將超過5億。這種結構性變化,加上北美地區住宅存量,使得房屋維修房屋抵押貸款利率限制了新建房屋的供應。現有住宅的轉售週期與地板材料升級密切相關,因為業主通常會在出售房產時更換磨損的地毯和破損的地磚。商業地產業主也在翻新職場,以適應混合辦公模式,這就要求地板材料能夠承受頻繁的隔間和家具調整,同時保持表面的完整性。與節能維修相關的市政獎勵通常將地板材料維修維修相結合,鼓勵使用低揮發性有機化合物(VOC)黏合劑和可回收的底層材料。在亞太新興城市,隨著地方政府推廣最低生活標準,要求高層住宅鋪設防滑、易清潔的地板材料,公共住宅現代化進程正在加速。這些趨勢的同步發展將確保穩定的需求基礎,並保護地板材料市場免受新建房屋需求週期性下降的影響。能夠將各種設計與快速應用系統結合的供應商,最有希望滿足自居住和出租房屋的需求,因為在這些房屋中,最短的運作至關重要。

從軟表面到硬表面的過渡

消費者的偏好顯然正在轉向兼具防水、耐刮擦和易於清潔的表面材料。對於有寵物和孩子的繁忙家庭來說,豪華硬乙烯基瓷磚已成為首選。這一趨勢反映了生活方式的改變,例如養狗人數的增加和開放式室內設計的普及,使得液體潑灑更容易擴散到整個房間。石塑複合板能夠模仿橡木、山核桃木和拋光混凝土的質感,同時在溫度波動下保持尺寸穩定性,從而拓展了其在日光室和半封閉式地下室的應用範圍。地毯製造商正在重新定位地毯,以滿足特定用途的需求,例如為豪華酒店套房提供優質寬幅地毯,在這些場所,奢華的舒適度和隔音效果比維護保養更為重要。零售買家現在透過獨立的壓痕和抗污測試來評估產品的耐用性,而FloorScore和GREENGUARD等認證在最終選擇中也變得越來越重要。隨著硬質地板市場佔有率的持續成長,隔音墊層和軟性過渡條等相關配件市場也蓬勃發展。承包商反映,採用黏合劑浮動卡扣系統可加快計劃週轉速度,這一優勢在一定程度上彌補了技術純熟勞工短缺的問題。未來三年,隨著數位噴墨印刷技術在美觀性方面的不斷提升,裝飾工藝有望得到進一步完善,從而進一步鞏固低維護成本的硬質板材的吸引力。

原物料價格波動

自2023年以來,PVC樹脂、高嶺土和硬木材料的價格季度波動幅度超過20%,這使得合約競標中的利潤率預測變得更加複雜。高度依賴進口的市場將最快感受到這種影響,因為外匯波動加劇了商品價格上漲,迫使經銷商維持高額安全庫存,從而佔用大量營運資金。雖然遠期購買樹脂期貨可以對沖成本,但如果設計週期發生變化,也會使企業面臨庫存過時的風險。價格波動也會促使企業使用替代材料。例如,當預算緊張時,客戶可能會降低規格,例如從橡木改為樺木,或從釉藥瓷磚改為拋光混凝土。由於合約中很少包含價格調整條款,小規模安裝商被迫承擔不成比例的高風險。雖然這種影響會限制地板材料市場的短期成長,但隨著亞洲和北美產能擴張後供需平衡的恢復正常,長期前景依然樂觀。供應商與多家供應商簽訂多年原物料採購協議,可降低風險,並為指定方維持物價穩定。

細分市場分析

到2025年,彈性地板材料將佔據31.78%的最高市場佔有率,鞏固其在維修和新建項目中的主導地位,這些項目優先考慮快速施工和防水性能。在這一類別中,石塑複合材料地板材料正以11.10%的複合年成長率推動市場規模的成長。傳統地面材料無法企及此成長速度,這主要得益於可縮短安裝時間的卡扣式拼接系統。瓷磚保持了18.23%的市場佔有率,這主要得益於能夠承受更高機械負荷的改良瓷磚,使其在機場和購物中心等場所的應用範圍不斷擴大。儘管仿木紋乙烯基複合地板材料取得了長足進步,但實木地板材料仍維持了8.42%的市場佔有率。工程複合地板材料尤其受到青睞,因為它兼具實木裝飾層板的美觀性和地暖系統所需的尺寸穩定性。超耐磨地板的年成長率為6.18%,這得益於製造商開始對邊緣倒角進行密封處理,並實現了此前只有乙烯基複合地板才具備的24小時防水保證。地毯和塊毯佔地面面積的31.45%,但在客廳中,其佔有率已被硬質地板超越。然而,在開放式辦公室的模組化設計中,方塊地毯的需求依然強勁。永續性是貫穿整個產業的優先事項,供應商正積極推動採用符合循環經濟採購準則的再生PET背襯和不含PVC的耐磨層。性能提升與環境法規的整合,確保了產品創新將持續成為塑造整個地板材料市場品類組合的關鍵驅動力。

硬質芯材和數位印刷技術的快速發展從根本上改變了定價格局,使得中等價位的產品能夠以更低的成本複製木材和石材的紋理細節,從而與高階產品展開競爭。各大品牌也開始採用複合材料,例如混合板材——在礦物芯材之間夾有木紋裝飾層板和軟木墊片——這種板材既能隔熱又能防止潮氣滲入。隨著全球原料價格趨於穩定,複合材料相對於採石場大理石和實木的成本優勢可能會進一步擴大,從而重新調整建築師和住宅對價值的認知。儘管區域偏好依然顯著(例如歐洲的寬幅橡木地板和東南亞的亮面瓷質磚),但線上視覺化工具正在逐步統一風格選擇,並推動全球對統一圖案的需求成長。陶瓷和地毯行業面臨激烈的競爭,但防滑、隔音和防污技術的創新正在幫助這些材料保持其競爭優勢。展望未來,能否將可再生材料和循環物流融入產品故事將決定誰能在不斷擴大的地板材料市場中贏得佔有率。

地板材料市場報告按產品類型(地毯、木塊毯、瓷磚地板材料、超耐磨地板地板材料、 PVC地板、石材地板材料及其他產品)、最終用戶(商業、住宅)、配銷通路(家居裝飾商店、旗艦店、專賣店及其他)和地區(北美及其他)進行細分。市場預測以美元為單位,並基於現有資訊提供。

區域分析

亞太地區在2025年將以37.10%的市場佔有率領跑,這主要得益於都市區住宅需求的持續成長和不斷擴張的大都會圈交通網路,這些因素每年消耗數百萬平方公尺的陶瓷和彈性地板材料。印度的房地產藍圖預計到2030年將打造一個1兆美元的市場,將推動高層公寓大樓、區域零售中心和IT園區大廳對複合地板材料的需求。儘管中國的宏觀審慎政策抑制了投機性建設的開工,但該國仍在繼續維修老舊多用戶住宅,採用節能建築幕牆,從而更換室內地板材料。越南958億美元的建設產業正以7%的年成長率成長,這主要得益於政府基礎設施支出以及地鐵站和工業訓練中心對瓷磚需求的穩定成長。東南亞4.5%的累積GDP成長率正在推動旅遊業復甦,並促進採用設計感十足的複合木地板的精品酒店的發展。

北美市場持續維持30.95%的市佔率和4.15%的複合年成長率,主要受翻新需求的推動。節能維修的稅收優惠鼓勵住宅用隔熱、防水且可與地暖維修相容的地板材料替換老舊的地毯。國內LVT地板的生產降低了運費波動風險,而美墨加協定(USMCA)則促進了加拿大鋸木廠和墨西哥層壓板廠之間的原料流通。歐洲市場維持27.85%的市佔率和3.06%的複合年成長率,主要得益於德國和義大利的維修計畫。兩國的補貼政策鼓勵使用低VOC(揮發性有機化合物)塗料。同時,REACH法規制定了嚴格的化學品標準,加速了不合規進口產品的退出市場。中東和非洲地區雖然目前市佔率小規模,但其複合年成長率高達8.05%,表現最為突出。沙烏地阿拉伯的「2030願景」計畫正在推動酒店業的快速發展,從而帶動了NEOM等計劃對地板材料的需求;與此同時,阿拉伯聯合大公國的住宅項目正在使用大理石紋理的乙烯基材料來抵禦沙漠沙礫的磨損。

不同地區的建築標準差異導致產品組合的差異。在歐洲,符合地暖效率要求的卡扣式陶瓷複合地板佔據主導地位;而在北美,寬幅SPC地板則因其適用於地下室維修備受青睞。物流基礎設施也影響市場需求;非洲港口吞吐能力的提升為重型瓷磚的進口開闢了新的途徑,而本地石材對於豪華別墅而言依然具有成本效益。貨幣穩定性影響拉丁美洲地區進口複合地板與本地實木地板的市場選擇。然而,更廣泛的南美洲數據超出了本文的研究範圍,因此在此不做贅述。總體而言,地域多元化能夠保護地板材料市場免受區域景氣衰退,並確保其在全球範圍內穩步擴張。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 快速的都市化和蓬勃發展的維修活動

- 從軟地板材料過渡到硬地面(LVT、SPC、木紋地板材料)

- 亞太地區和中東及非洲市場的建築業蓬勃發展

- 剛性芯材與防水技術的產品創新

- 美國LVT生產線回流(關稅減免措施)

- 醫療和教育設施對抗菌地板材料的需求

- 市場限制

- 原料價格波動(PVC樹脂、硬木、陶瓷)

- 對塑膠地板材料的環境法規更加嚴格

- 持證地板施工技術人員短缺

- 關稅和貿易政策的突然變化導致進口供應鏈中斷

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 波特五力模型

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 依產品

- 地毯和塊毯

- 木地板

- 磁磚地板材料

- 複合地板

- 乙烯基地板材料

- 石材地板材料

- 其他產品

- 最終用戶

- 商業的

- 住宅

- 透過分銷管道

- 家居建材商店

- 旗艦店

- 專賣店

- 網路商店

- 其他分銷管道

- 按地區

- 北美洲

- 加拿大

- 美國

- 墨西哥

- 南美洲

- 巴西

- 秘魯

- 智利

- 阿根廷

- 其他南美洲

- 歐洲

- 英國

- 德國

- 法國

- 西班牙

- 義大利

- 比荷盧經濟聯盟(比利時、荷蘭、盧森堡)

- 北歐國家(丹麥、芬蘭、冰島、挪威、瑞典)

- 其他歐洲地區

- 亞太地區

- 印度

- 中國

- 日本

- 澳洲

- 韓國

- 東南亞(新加坡、馬來西亞、泰國、印尼、越南、菲律賓)

- 亞太其他地區

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 奈及利亞

- 其他中東和非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Mohawk Industries

- Shaw Industries

- Tarkett SA

- Interface Inc.

- Armstrong Flooring/AHF Products

- Beaulieu International Group

- Gerflor Group

- Mannington Mills

- Milliken & Company

- Forbo Holding

- Congoleum Corporation

- Swiss Krono Group

- Boral Limited

- Orientbell Tiles

- Kajaria Ceramics

- Grupo Lamosa

- Ragno Ceramics

- Victoria PLC

- Roppe Corporation

- Ege Carpets

第7章 市場機會與未來展望

The floor covering market was valued at USD 101.28 billion in 2025 and estimated to grow from USD 106.42 billion in 2026 to reach USD 136.18 billion by 2031, at a CAGR of 5.06% during the forecast period (2026-2031).

Robust residential renovation in North America, megaproject activity in Asia-Pacific, and recovery in hospitality construction across the Middle East collectively anchor demand for premium, long-life surfaces. Technological breakthroughs such as rigid-core waterproof planks and PVC-free resilient options broaden application versatility, allowing suppliers to address both moisture-prone basements and high-traffic commercial corridors without major design compromises. Manufacturers are increasingly localizing production in the United States to sidestep tariff exposure, compress lead times, and meet stringent VOC emission rules, a strategy that also bolsters supply-chain resilience against global shipping disruptions. E-commerce is reshaping purchasing journeys by merging augmented-reality visualization tools with direct-to-consumer logistics, which is motivating home-center chains to integrate virtual design consultations and click-and-collect fulfillment. Competitive differentiation is shifting toward environmental credentials, with recycled-content formulations and take-back recycling programs becoming decisive in corporate procurement specifications that now routinely reference LEED, BREEAM, and WELL benchmarks.

Global Floor Covering Market Trends and Insights

Rapid Urbanization & Booming Renovation Activities

Urban populations in India alone are expected to top 500 million by 2025, and that structural shift, combined with aging housing stock across North America, keeps retrofit spending elevated even while mortgage rates temper new-build volumes. Existing-home resale cycles correlate strongly with flooring upgrades because owners typically replace outdated carpet or chipped tiles when preparing a property for listing. Commercial landlords are similarly retrofitting workplaces to support hybrid office strategies, which requires surfaces that tolerate frequent reconfiguration of partitions and furniture glides without losing finish integrity. Municipal incentives tied to energy-efficient retrofits often bundle floor replacement grants with broader envelope-upgrade programs, stimulating adoption of low-VOC adhesives and recycled underlayment. In emerging Asia-Pacific cities, public housing modernization is accelerating as provincial authorities push minimum living-standard codes that mandate non-slip, easy-clean floor materials in high-rise dwellings. These simultaneous dynamics ensure a consistent baseline demand that cushions the floor covering market against cyclical dips in new construction. Suppliers that package pattern-rich visuals and rapid-install systems are best positioned to capture volume across both owner-occupied and rental properties, where minimal downtime is critical.

Shift from Soft to Hard-Surface Flooring

Consumer attitudes have swung decisively toward surfaces that combine waterproof integrity, scratch resistance, and quick sanitation, propelling rigid luxury vinyl tile to the top of specification lists for busy households with pets and children. The move reflects lifestyle shifts such as rising dog ownership and open-concept interiors where spills travel unimpeded across rooms. Stone plastic composite boards emulate oak, hickory, or polished concrete yet remain dimensionally stable under temperature swings, which widens their suitability for sunrooms and semi-conditioned basements. Carpet manufacturers are repositioning toward niche use-cases like premium broadloom for high-end hospitality suites where plush comfort and acoustic dampening outweigh maintenance concerns. Retail buyers now benchmark product durability through independent indentation and stain-resistance tests, elevating the status of certifications such as FloorScore and GREENGUARD in final selection. As the hard-surface share widens, accessory markets for sound-absorbing underlayment and flexible transition strips experience adjacent growth spurts. Installers report quicker project turnover because floating-click systems eliminate the need for adhesives, a benefit that partially offsets skilled-labor shortages. Over the coming three years, incremental aesthetic gains from digital-ink printing are expected to satisfy decor cycles, further cementing the appeal of low-maintenance rigid formats.

Volatile Raw-Material Prices

PVC resin, ceramic clay, and hardwood lumber have experienced price swings exceeding 20% within single fiscal quarters since 2023, complicating margin forecasting for contract bids. Import-heavy markets feel the pinch fastest because currency fluctuations compound commodity spikes, compelling distributors to hold higher safety stocks that tie up working capital. Forward-buying resin futures can hedge costs but expose companies to inventory obsolescence if design cycles shift. Volatility encourages substitution; for example, customers may down-spec from oak to birch or from glazed porcelain to polished concrete overlays when budgets tighten. Smaller installers absorb disproportionately high risk because their contracts seldom include escalation clauses. The net effect trims near-term floor covering market growth, although the long-run outlook remains positive as supply-demand imbalances normalize post-capacity additions in Asia and North America. Suppliers that negotiate multi-year feedstock agreements with diversified sources limit exposure and maintain price stability for specification writers.

Other drivers and restraints analyzed in the detailed report include:

- Construction Boom in Asia-Pacific & MEA Markets

- On-shoring of LVT Production in the United States

- Environmental Scrutiny of Plastic-Based Flooring

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Resilient flooring commanded the highest share at 31.78% in 2025, confirming its dominance in renovation and new-build schedules that emphasize fast installation and water resistance. Within the category, stone plastic composite is propelling the floor covering market size by expanding at an 11.10% CAGR, a pace unmatched by traditional surfaces and aided by click systems that cut labor hours. Ceramic tiles held an 18.23% share thanks to porcelain improvements that now withstand high mechanical loads, widening their fit for airports and shopping centers. Wood flooring retained an 8.42% foothold despite encroachment from wood-look vinyl, with engineered formats gaining traction because they pair genuine veneer aesthetics with dimensional stability across radiant-heat subfloors. Laminate grew 6.18% yearly after manufacturers sealed edge bevels to deliver 24-hour water warranties, a feature once exclusive to vinyl. Carpet and area rugs still covered 31.45% of installed square footage, but ceded living-room ground to hard surfaces, even though carpet tiles thrive in open-office modular plans. Sustainability is a cross-cutting priority, pushing suppliers to introduce recycled PET backings and PVC-free wear layers that qualify under circular-economy procurement guidelines. The convergence of performance upgrades and environmental mandates ensures that product innovation remains the principal lever shaping category mix across the floor covering market.

The surge of rigid-core and digital-print capabilities fundamentally shifts pricing ladders, enabling mid-tier products to encroach on premium wood or stone positions by replicating texture nuances at a fraction of the cost. Brands are also embracing mixed materials such as hybrid planks that sandwich mineral cores between wood veneers or cork pads, delivering thermal comfort while guarding against moisture ingress. As global raw-material prices stabilize, cost advantages may widen for engineered composites over quarried marble or solid hardwood, realigning value perceptions among architects and homeowners. Geographic preferences persist-Europe still favors wide-plank oak while Southeast Asia leans toward glossy porcelain-but online visualization tools are gradually homogenizing style choices, funneling incremental volume toward globally consistent patterns. Although ceramic and carpet segments face stiff competition, innovations in slip-rating, acoustic insulation, and stain technology preserve niches where these materials outperform. In the future, the ability to weave renewable content and recycling logistics into product stories will increasingly determine which brands claim a share of the growing floor covering market size.

The Floor Covering Market Report is Segmented by Product (Carpet & Area Rugs, Wood Flooring, Ceramic Tiles Flooring, Laminate Flooring, Vinyl Flooring, Stone Flooring, Other Products), End User (Commercial, Residential), Distribution Channel (Home Centers, Flagship Stores, Specialty Stores, and Other), and Geography (North America, and Other). The Market Forecasts are Provided in Terms of Value (USD), Based On Availability.

Geography Analysis

Asia-Pacific led with 37.10% share in 2025, buoyed by unrelenting urban housing growth and megacity transportation expansions that consume millions of square meters of ceramic and resilient surfaces annually. India's real-estate roadmap envisions a USD 1 trillion sector by 2030, translating into compounded floor demand spanning high-rise condos, tier-III city retail hubs, and IT campus lobbies. China continues to retrofit older apartment blocks with energy-efficient facades that bundle interior floor replacement, although macroprudential controls temper speculative building starts. Vietnam's USD 95.8 billion construction sector grows at 7% annually on the back of government infrastructure outlays, reflecting steady tile uptake for metro stations and industrial training centers. Southeast Asia's cumulative 4.5% GDP growth propels tourism rebound, spurring boutique hotel developments that specify design-forward composite wood planks .

North America followed at 30.95% share and 4.15% CAGR, driven mainly by remodeling; stimulus tax incentives for energy-efficient retrofits encourage homeowners to swap outdated carpet for insulated, waterproof planks that integrate with radiant-heat upgrades. Domestic LVT production dampens exposure to freight volatility, and USMCA provisions facilitate raw-material flows between Canadian lumber mills and Mexican laminate plants. Europe maintained a 27.85% share and a 3.06% CAGR, anchored by renovation programs in Germany and Italy, where subsidies promote low-VOC finishes; meanwhile, the REACH regulation sets stringent chemical thresholds that accelerate market exit for non-compliant imports. The Middle East & Africa, albeit the smallest region today, stands out with the fastest 8.05% CAGR as Saudi Arabia's Vision 2030 hospitality boom expands flooring footprints in giga-projects like NEOM, and UAE residential schemes utilize marble-look vinyl that survives desert sand abrasion.

Regional variance in building codes produces product-mix differences: Europe leans toward click-ceramic hybrids to satisfy underfloor-heating efficiency, while North America favors wide-plank SPC for basement remodeling. Logistics infrastructure also shapes demand; Africa's improving port capacity opens routes for heavyweight porcelain imports while local quarry stone remains cost-effective for luxury villas. Currency stability influences the adoption of imported laminate versus locally milled hardwood across Latin America, though broader South American data were outside our input scope and are not elaborated here. Overall, geographic diversification balances the floor covering market against localized recessions, ensuring a globally steady expansion trajectory.

- Mohawk Industries

- Shaw Industries

- Tarkett SA

- Interface Inc.

- Armstrong Flooring / AHF Products

- Beaulieu International Group

- Gerflor Group

- Mannington Mills

- Milliken & Company

- Forbo Holding

- Congoleum Corporation

- Swiss Krono Group

- Boral Limited

- Orientbell Tiles

- Kajaria Ceramics

- Grupo Lamosa

- Ragno Ceramics

- Victoria PLC

- Roppe Corporation

- Ege Carpets

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid urbanisation & booming renovation activities

- 4.2.2 Shift from soft to hard-surface flooring (LVT, SPC, wood-look)

- 4.2.3 Construction boom in APAC & MEA markets

- 4.2.4 Product innovations in rigid-core & waterproof technologies

- 4.2.5 On-shoring of LVT production in the U.S. (tariff mitigation)

- 4.2.6 Demand for antimicrobial-treated floors in healthcare & education

- 4.3 Market Restraints

- 4.3.1 Volatile raw-material prices (PVC, hardwood, ceramics)

- 4.3.2 Environmental scrutiny of plastic-based flooring

- 4.3.3 Shortage of certified floor-installation labour

- 4.3.4 Tariff/trade-policy shocks disrupting import supply chains

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Product

- 5.1.1 Carpet & Area Rugs

- 5.1.2 Wood Flooring

- 5.1.3 Ceramic Tiles Flooring

- 5.1.4 Laminate Flooring

- 5.1.5 Vinyl Flooring

- 5.1.6 Stone Flooring

- 5.1.7 Other Products

- 5.2 By End User

- 5.2.1 Commercial

- 5.2.2 Residential

- 5.3 By Distribution Channel

- 5.3.1 Home Centers

- 5.3.2 Flagship Stores

- 5.3.3 Specialty Stores

- 5.3.4 Online Stores

- 5.3.5 Other Distribution Channels

- 5.4 By Region

- 5.4.1 North America

- 5.4.1.1 Canada

- 5.4.1.2 United States

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Peru

- 5.4.2.3 Chile

- 5.4.2.4 Argentina

- 5.4.2.5 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 United Kingdom

- 5.4.3.2 Germany

- 5.4.3.3 France

- 5.4.3.4 Spain

- 5.4.3.5 Italy

- 5.4.3.6 BENELUX (Belgium, Netherlands, Luxembourg)

- 5.4.3.7 NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- 5.4.3.8 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 India

- 5.4.4.2 China

- 5.4.4.3 Japan

- 5.4.4.4 Australia

- 5.4.4.5 South Korea

- 5.4.4.6 South East Asia (SG, MY, TH, ID, VN, PH)

- 5.4.4.7 Rest of Asia-Pacific

- 5.4.5 Middle East & Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 South Africa

- 5.4.5.4 Nigeria

- 5.4.5.5 Rest of Middle East & Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Mohawk Industries

- 6.4.2 Shaw Industries

- 6.4.3 Tarkett SA

- 6.4.4 Interface Inc.

- 6.4.5 Armstrong Flooring / AHF Products

- 6.4.6 Beaulieu International Group

- 6.4.7 Gerflor Group

- 6.4.8 Mannington Mills

- 6.4.9 Milliken & Company

- 6.4.10 Forbo Holding

- 6.4.11 Congoleum Corporation

- 6.4.12 Swiss Krono Group

- 6.4.13 Boral Limited

- 6.4.14 Orientbell Tiles

- 6.4.15 Kajaria Ceramics

- 6.4.16 Grupo Lamosa

- 6.4.17 Ragno Ceramics

- 6.4.18 Victoria PLC

- 6.4.19 Roppe Corporation

- 6.4.20 Ege Carpets

7 Market Opportunities & Future Outlook

- 7.1 Circular-economy take-back & recycling platforms for post-consumer LVT

- 7.2 AI-guided virtual design tools that shorten specification-to-install cycle for commercial projects

全球地板材料市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球地板材料市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 地板材料市場規模、佔有率和成長分析:按產品類型、應用、分銷管道和地區分類-2026-2033年產業預測

地板材料市場規模、佔有率和成長分析:按產品類型、應用、分銷管道和地區分類-2026-2033年產業預測 地板材料市場:2026-2032年全球市場預測(依產品類型、安裝方式、銷售管道及最終用戶分類)

地板材料市場:2026-2032年全球市場預測(依產品類型、安裝方式、銷售管道及最終用戶分類) 美國地板材料:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)英國地板覆蓋材料:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

美國地板材料:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)英國地板覆蓋材料:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 2026年全球家居佈置和地板覆蓋材料市場報告

2026年全球家居佈置和地板覆蓋材料市場報告 日本地面鋪裝材料市場報告(按材料、配銷通路、最終用戶和地區分類,2026-2034年)

日本地面鋪裝材料市場報告(按材料、配銷通路、最終用戶和地區分類,2026-2034年) 地板覆蓋市場-全球產業規模、佔有率、趨勢、機會和預測,按材料(彈性、非彈性、軟地板覆蓋)、按應用(住宅、商業、工業)、按地區、按競爭細分,2020-2030 年預測彈性地板材料:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)印尼地板樹脂:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

地板覆蓋市場-全球產業規模、佔有率、趨勢、機會和預測,按材料(彈性、非彈性、軟地板覆蓋)、按應用(住宅、商業、工業)、按地區、按競爭細分,2020-2030 年預測彈性地板材料:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)印尼地板樹脂:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)