|

市場調查報告書

商品編碼

1907301

發泡聚苯乙烯(EPS):市佔率分析、產業趨勢與統計、成長預測(2026-2031)Expanded Polystyrene (EPS) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

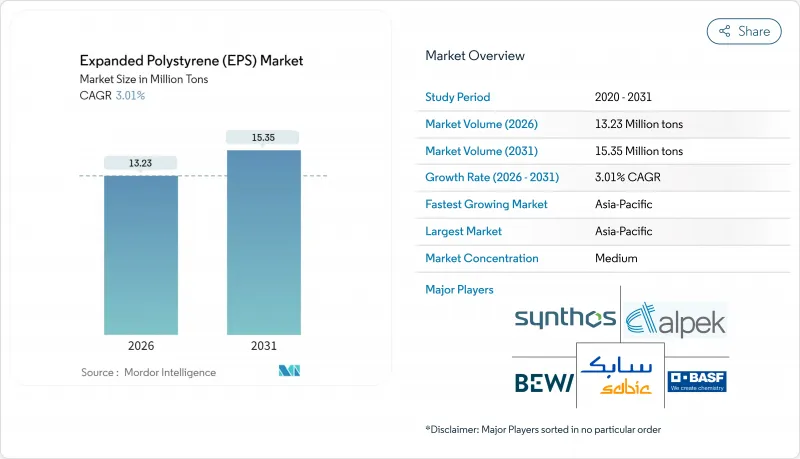

預計到 2026 年,發泡聚苯乙烯 (EPS) 市場規模將達到 1,323 萬噸,高於 2025 年的 1,284 萬噸。

預計到 2031 年產量將達到 1,535 萬噸,2026 年至 2031 年的複合年成長率為 3.01%。

這一銷售成長反映了建築和包裝行業消費量增加與苯乙烯加工過程中揮發性有機化合物 (VOC) 排放法規日益嚴格帶來的成本壓力之間的權衡。發泡聚苯乙烯市場受惠於其優異的導熱性能與價格比,儘管模塑紙漿、生物泡棉和紙襯墊越來越受歡迎,但其需求仍保持穩定。亞太地區仍然是最大的單一市場,而北美則將這種材料用作電子商務的「最後一公里」隔熱材料材料。企業策略正將重點轉向化學回收通路和原料多角化,這顯示循環經濟合規性正在成為發泡聚苯乙烯市場新的競爭優勢。

全球發泡聚苯乙烯(EPS)市場趨勢與洞察

加快淨零能耗建築的建設進程

快速脫碳目標正在重新定義全球隔熱材料規範。歐洲能源性能法規要求新建建築接近零能耗,迫使建築師尋找兼具低導熱係數(λ值)和久經考驗的耐久性的材料。灰色和銀色EPS的導熱係數比標準等級低20%,因此可以在符合U值標準的前提下建造更薄的牆體。日本2024年節能標準修訂將收緊隔熱信封標準,進一步推動對石墨增強EPS解決方案的需求。隨著建築業主優先考慮降低營運成本,EPS擴大應用於連續隔熱材料和承重斷熱板(SIP)中,從而鞏固了EPS在高性能建築市場的地位。

亞太新興市場低溫運輸投資復甦

東南亞各國政府正投入數十億美元用於低溫運輸物流,以防止食品變質並維持藥品安全標準。由於其R值穩定性好、減震性能優異且單位運輸成本最低,EPS包裝箱和內襯正逐漸成為主流。越南的半導體組裝廠使用EPS翻蓋式容器來維持嚴格的溫度範圍,而區域疫苗宣傳活動則依賴經過檢驗的EPS運輸容器來保護對溫度敏感的生物製藥。

收緊苯乙烯揮發性有機化合物排放限值。

歐盟於2024年將職業環境中苯乙烯濃度限值降至20 ppm,要求製造商維修設備並加裝減排系統,可能會使營運成本增加3-5%。同年,美國環保署(EPA)的執法力道也增加了40%,進一步加劇了合規風險。一些規模較小的加工企業可能因無力購買再生熱氧化設備而退出市場,導致區域供應減少,並對整個發泡聚苯乙烯市場造成價格上漲壓力。

細分市場分析

截至2025年,EPS將佔發泡聚苯乙烯市場的95.12%,但灰色產品的市場預計將以更快的速度成長,到2031年複合年成長率將達到3.89%。德國和法國的建築商正在指定使用石墨填充板材,以滿足隔熱性能標準(U值),而無需增加牆體厚度,這表明性能的提升即使在價格上漲的情況下也能推動需求。BASF等製造商已於2024年將Neopor的產能提高了40%,以滿足建築業的需求。同時,反光銀色EPS產品正在滲透到工業隔熱材料市場的表面溫度超過80°C,從而在小規模但不斷成長的特種市場中開闢了新的機會。通用包裝仍然嚴重依賴白色發泡聚苯乙烯,因為物流買家優先考慮的是低初始成本。然而,隨著建築規範的日益嚴格,高隔熱性能(高R值)的產品線預計將逐漸削弱白色EPS在發泡聚苯乙烯市場的主導地位。

白色EPS憑藉其成本優勢,在電器緩衝、模壓魚箱和模組化建築構件等領域鞏固了其市場地位。灰色EPS雖然價格較高,但憑藉其在節能外牆系統中的應用,正逐漸贏得市場佔有率,其中石墨級EPS更是成為近零能耗建築計劃的首選。銀色EPS由於適用於石化管道隔熱材料和LNG接收站高溫冷箱內襯,正經歷穩健但盈利的成長。這些趨勢表明,在高度同質化的發泡聚苯乙烯市場中,差異化的表現能夠創造出具有競爭優勢的價值領域。

發泡聚苯乙烯市場報告按產品類型(白色EPS、灰色EPS、銀色EPS)、終端用戶行業(建築與施工、電氣與電子、包裝、其他終端用戶行業)和地區(亞太地區、北美地區、歐洲地區、南美地區、中東和非洲)進行細分。市場預測以噸為單位。

區域分析

預計到2025年,亞太地區將佔全球總噸位的66.75%,到2031年將以3.21%的複合年成長率成長。中國的都市化計畫支撐了住宅開工量,而印度的「總理綠色力量計畫」(PM Gati Shakti)正向道路和倉儲計劃投入數十億盧比,從而帶動了隔熱材料需求的成長。在東南亞,尤其是在泰國和越南,為滿足食品安全要求資金籌措的低溫運輸擴建,正在推動托盤式海鮮容器和疫苗冷藏箱對發泡聚苯乙烯(EPS)的需求。該地區垂直整合的苯乙烯生產聯合體持續提供低成本供應,使當地生產商在整個發泡聚苯乙烯市場中擁有結構性優勢。

北美是受電子商務和模組化建築週期驅動的關鍵市場。在美國,各州的能源規範推動了連續保溫材料的普及,工廠組合式牆板通常採用EPS芯材以縮短現場施工時間。在加拿大,魁北克省和安大略省數十億美元的冷庫建設帶動了生鮮食品包裝的訂單,為該地區EPS需求提供了穩定的基礎。墨西哥與北美市場相輔相成,不斷成長的電子產品出口推動了對用於運輸印刷基板的防靜電EPS包裝的需求。

儘管歐洲的廢棄物減量法規日益嚴格,但EPS仍被用於歐盟綠色交易資助的大規模節能維修中。義大利的抗震維修激勵措施和德國的《建築能源法》促進了板材的銷售,而英國蓬勃發展的宅配服務則抵消了因一次性刀叉餐具禁用模塑紙漿而導致的銷售量下滑。沙烏地阿拉伯的石化產業擴張和巴西的基礎設施走廊表明,隨著物流網路的成熟,這些地區有望獲得更大的市場佔有率。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 加快淨零能耗建築的建設進程

- 亞太新興市場低溫運輸投資復甦

- 電子商務對最後一公里保溫包裝的需求日益成長

- 歐洲和日本的強制性隔震標準

- 模組化預製建築的興起

- 市場限制

- 收緊苯乙烯揮發性有機化合物(VOC)排放限值

- 模塑紙漿熱感襯墊的普及速度迅速提升

- 歐盟「可回收設計」指令限制一次性EPS的使用。

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 進出口趨勢

第5章 市場規模和成長預測(價值和數量)

- 依產品類型

- 白色 EPS

- 灰色和銀色 EPS

- 按最終用戶行業分類

- 建築/施工

- 電氣和電子設備

- 包裝

- 其他終端用戶產業(農業和汽車)

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- ASEAN

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 北歐國家

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- Alpek SAB de CV

- BASF

- BEWi

- Epsilyte LLC

- Ineos

- Kaneka Corporation

- Ravago

- SABIC

- Shuangliang Group Co., Ltd.(Jiangsu Leasty Chemical Co.,Ltd.)

- SIBUR International GmbH

- Sunde Group

- Sunpor

- Synthos

- TotalEnergies

- Versalis SpA

- Wuxi Xingda foam plastic new material Limited

第7章 市場機會與未來展望

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 加快淨零能耗建築的建設進程

- 亞太新興市場低溫運輸投資復甦

- 電子商務對最後一公里保溫包裝的需求日益成長

- 歐洲和日本的強制性隔震標準

- 模組化預製建築的興起

- 市場限制

- 收緊苯乙烯揮發性有機化合物(VOC)排放限值

- 模塑紙漿熱感襯墊的普及速度迅速提升

- 歐盟「可回收設計」指令限制一次性EPS的使用。

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 進出口趨勢

第5章 市場規模和成長預測(價值和數量)

- 依產品類型

- 白色 EPS

- 灰色和銀色 EPS

- 按最終用戶行業分類

- 建築/施工

- 電氣和電子設備

- 包裝

- 其他終端用戶產業(農業和汽車)

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- ASEAN

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 北歐國家

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- Alpek SAB de CV

- BASF

- BEWi

- Epsilyte LLC

- Ineos

- Kaneka Corporation

- Ravago

- SABIC

- Shuangliang Group Co., Ltd.(Jiangsu Leasty Chemical Co.,Ltd.)

- SIBUR International GmbH

- Sunde Group

- Sunpor

- Synthos

- TotalEnergies

- Versalis SpA

- Wuxi Xingda foam plastic new material Limited

第7章 市場機會與未來展望

Expanded Polystyrene market size in 2026 is estimated at 13.23 million tons, growing from 2025 value of 12.84 million tons with 2031 projections showing 15.35 million tons, growing at 3.01% CAGR over 2026-2031.

Volume growth reflects the push-pull between rising consumption in construction and packaging and the cost pressures generated by stringent volatile-organic-compound limits on styrene processing. The Expanded Polystyrene market continues to capitalize on its favorable thermal conductivity-to-price ratio, which keeps demand steady even as molded pulp, bio-foams, and paper-based liners scale up. Asia-Pacific remains the single largest outlet, while North America leverages the material for e-commerce last-mile insulation. Corporate strategies increasingly pivot on chemical recycling pathways and feedstock diversification, signaling that circular-economy compliance is an emerging competitive prerequisite across the Expanded Polystyrene market.

Global Expanded Polystyrene (EPS) Market Trends and Insights

Accelerated Push for Net-Zero-Ready Buildings

Rapid decarbonization targets are redrawing insulation specifications worldwide. Energy-performance mandates in Europe require near-zero-energy new builds, pushing architects toward materials that combine low λ-values with proven durability. Gray and silver EPS deliver up to 20% lower thermal conductivity than standard grades, enabling thinner wall assemblies without compromising U-value compliance. Japan's 2024 energy-efficiency revision tightens thermal-envelope criteria, further amplifying demand for graphite-enhanced Expanded Polystyrene market solutions. As building owners prioritize operating-cost reductions, EPS gains traction in continuous insulation and structural insulated panels, reinforcing the Expanded Polystyrene market's profile in the high-performance building segment.

Resurgent Cold-Chain Investments in Emerging APAC

Southeast Asian governments are funneling billions into cold-chain logistics to curb food spoilage and uphold drug-safety standards. EPS boxes and liners dominate because they combine R-value stability with shock absorption at the lowest delivered cost per unit. Semiconductor assembly hubs in Vietnam rely on EPS clamshells to maintain narrow thermal windows, while regional vaccine campaigns depend on validated EPS shippers to protect temperature-sensitive biologics.

Tightening VOC Emission Ceilings on Styrene

The EU lowered occupational styrene limits to 20 ppm in 2024, forcing manufacturers to retrofit abatement systems that can add 3-5% to operating costs. EPA enforcement actions in the United States climbed 40% the same year, raising compliance risk. Smaller converters lacking capital for regenerative thermal oxidizers may exit, narrowing regional supply and nudging prices upward across the Expanded Polystyrene market.

Other drivers and restraints analyzed in the detailed report include:

- E-Commerce Last-Mile Insulated Packaging Boom

- Mandatory Seismic Insulation Codes in Europe and Japan

- EU "Design for Recycling" Mandates Curbing Single-Use EPS

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

White EPS accounted for 95.12% of the Expanded Polystyrene market in 2025, yet gray variants are on track to expand faster at 3.89% CAGR through 2031. Builders in Germany and France specify graphite-infused panels to meet U-values without thicker walls, illustrating how performance upgrades redirect demand even when prices are higher. Manufacturers such as BASF added 40% Neopor capacity in 2024 to satisfy this construction pull. Concurrently, reflective silver EPS grades penetrate industrial insulation niches where surface temperatures exceed 80 °C, tapping small but growing specialized opportunities. Commodity packaging still leans heavily on white foam because logistics buyers prioritize low upfront cost. As building codes tighten, however, higher-R-value lines will gradually chip away at white EPS dominance within the Expanded Polystyrene market.

White EPS's cost edge keeps it entrenched in appliance cushioning, molded fish crates, and block-molded architectural shapes. Gray EPS, despite its premium, secures volume through energy-efficient facade systems, ensuring that every new near-zero-energy project allocates tonnage to graphite grades. The expansion of silver EPS stays modest but lucrative, given its fit for petrochemical pipe insulation and high-temperature cold-box linings in LNG terminals. These trends confirm that differentiated performance creates defensible value pockets, even inside a largely commoditized Expanded Polystyrene market.

The Expanded Polystyrene Market Report is Segmented by Product Type (White EPS and Gray and Silver EPS), End-User Industry (Building and Construction, Electrical and Electronics, Packaging, and Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

Asia-Pacific secured 66.75% of global tonnage in 2025 and is projected to rise at a 3.21% CAGR to 2031. China's urbanization pipeline sustains housing starts, while India's PM Gati Shakti program channels billions into road and warehousing projects, translating into higher insulation demand. Southeast Asia, led by Thailand and Vietnam, bankrolls cold-chain expansion to meet food-safety directives, pulling incremental EPS volumes for pallet-sized fish boxes and vaccine coolers. The region's vertically integrated styrene complexes keep delivering costs low, giving local producers a structural advantage across the Expanded Polystyrene market.

North America is a significant market, driven by e-commerce and modular construction cycles. U.S. state-level energy codes increasingly require continuous-insulation layers, and factory-assembled wall panels frequently embed EPS cores to accelerate job-site completion. Canada's multibillion-dollar cold-storage builds in Quebec and Ontario drive fresh packaging orders, ensuring a dependable baseline for regional EPS demand. Mexico rounds out the North American picture with rising electronics exports, necessitating anti-static EPS packs for printed-circuit-board transit.

Europe confronts stricter waste-reduction rules but still leans on EPS for deep-energy retrofits funded by the EU Green Deal. Italy's seismic-retrofit incentives and Germany's Building Energy Act sustain panel sales, while the United Kingdom's booming meal-delivery services offset volume lost to molded-pulp bans in single-use cutlery. Petrochemical expansions in Saudi Arabia and infrastructure corridors in Brazil suggest these territories could increase their shares as logistics networks mature.

- Alpek SAB de CV

- BASF

- BEWi

- Epsilyte LLC

- Ineos

- Kaneka Corporation

- Ravago

- SABIC

- Shuangliang Group Co., Ltd. (Jiangsu Leasty Chemical Co.,Ltd.)

- SIBUR International GmbH

- Sunde Group

- Sunpor

- Synthos

- TotalEnergies

- Versalis S.p.A.

- Wuxi Xingda foam plastic new material Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated push for net-zero ready buildings

- 4.2.2 Resurgent cold-chain investments in emerging APAC

- 4.2.3 E-commerce last-mile insulated packaging boom

- 4.2.4 Mandatory seismic insulation codes in Europe and Japan

- 4.2.5 Modular prefab construction uptake

- 4.3 Market Restraints

- 4.3.1 Tightening VOC emission ceilings on styrene

- 4.3.2 Rapid scale-up of molded pulp thermal liners

- 4.3.3 EU "Design for Recycling" mandates curbing single-use EPS

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Import-Export Trends

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Product Type

- 5.1.1 White EPS

- 5.1.2 Gray and Silver EPS

- 5.2 By End-user Industry

- 5.2.1 Building and Construction

- 5.2.2 Electrical and Electronics

- 5.2.3 Packaging

- 5.2.4 Other End-user Industries (Agriculture and Automotive)

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Nordic Countries

- 5.3.3.6 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Alpek SAB de CV

- 6.4.2 BASF

- 6.4.3 BEWi

- 6.4.4 Epsilyte LLC

- 6.4.5 Ineos

- 6.4.6 Kaneka Corporation

- 6.4.7 Ravago

- 6.4.8 SABIC

- 6.4.9 Shuangliang Group Co., Ltd. (Jiangsu Leasty Chemical Co.,Ltd.)

- 6.4.10 SIBUR International GmbH

- 6.4.11 Sunde Group

- 6.4.12 Sunpor

- 6.4.13 Synthos

- 6.4.14 TotalEnergies

- 6.4.15 Versalis S.p.A.

- 6.4.16 Wuxi Xingda foam plastic new material Limited

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Bio-based and Chemically Recycled EPS Roadmap

發泡聚苯乙烯市場報告:依產品、終端用途產業及地區分類(2026-2034 年)

發泡聚苯乙烯市場報告:依產品、終端用途產業及地區分類(2026-2034 年) 發泡聚苯乙烯市場:依形態、等級、最終用途產業、通路和應用程式分類-2026-2032年全球市場預測發泡聚苯乙烯增密設備市場:按機器類型、操作模式、類別、應用和最終用戶分類 - 全球預測 2026-2032

發泡聚苯乙烯市場:依形態、等級、最終用途產業、通路和應用程式分類-2026-2032年全球市場預測發泡聚苯乙烯增密設備市場:按機器類型、操作模式、類別、應用和最終用戶分類 - 全球預測 2026-2032 發泡聚苯乙烯市場-全球產業規模、佔有率、趨勢、機會及預測(依產品類型、最終用途、地區及競爭格局分類,2021-2031年)

發泡聚苯乙烯市場-全球產業規模、佔有率、趨勢、機會及預測(依產品類型、最終用途、地區及競爭格局分類,2021-2031年) 歐洲發泡聚苯乙烯(EPS)市場佔有率分析、產業趨勢、統計和成長預測(2026-2031)

歐洲發泡聚苯乙烯(EPS)市場佔有率分析、產業趨勢、統計和成長預測(2026-2031) 發泡聚苯乙烯包裝市場規模、佔有率和成長分析(按產品類型、最終用途產業、密度、形狀、應用和地區分類)-2026-2033年產業預測

發泡聚苯乙烯包裝市場規模、佔有率和成長分析(按產品類型、最終用途產業、密度、形狀、應用和地區分類)-2026-2033年產業預測 珠狀聚苯乙烯(EPS)泡沫包裝市場規模、佔有率、成長及全球產業分析:按類型、應用和地區劃分的洞察與預測(2024-2032 年)

珠狀聚苯乙烯(EPS)泡沫包裝市場規模、佔有率、成長及全球產業分析:按類型、應用和地區劃分的洞察與預測(2024-2032 年) 2025-2029年全球發泡聚苯乙烯市場

2025-2029年全球發泡聚苯乙烯市場 全球發泡聚苯乙烯市場:市場規模、佔有率、趨勢分析(按產品、應用和地區)、細分市場預測(2025-2033)

全球發泡聚苯乙烯市場:市場規模、佔有率、趨勢分析(按產品、應用和地區)、細分市場預測(2025-2033) 包裝用發泡聚苯乙烯市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

包裝用發泡聚苯乙烯市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測