|

市場調查報告書

商品編碼

1907217

電氣外殼:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)Electrical Enclosures - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

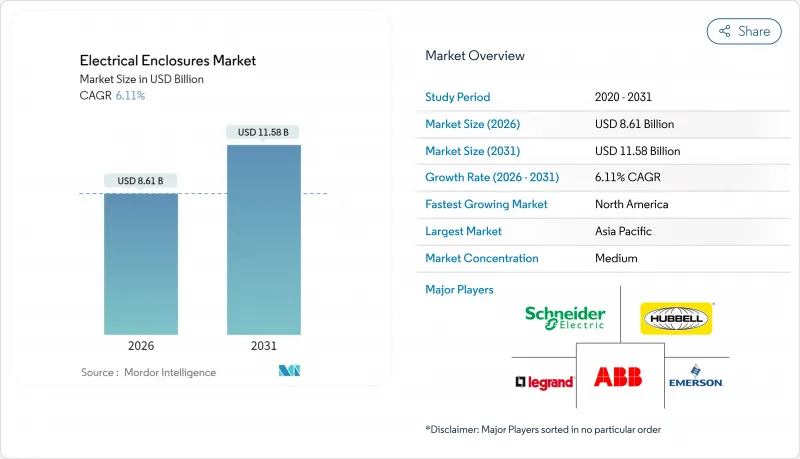

預計到 2025 年,電氣外殼市場價值將達到 81.1 億美元,從 2026 年的 86.1 億美元成長到 2031 年的 115.8 億美元,在預測期(2026-2031 年)內,複合年成長率將達到 6.11%。

隨著公用事業公司、工廠和通訊業者配備感測器、邊緣處理器和無線模組的智慧機櫃取代傳統機殼,市場需求正在加速成長。電力產業的快速擴張、5G 的興起以及交通運輸的電氣化,都保持了強勁的訂單週期;同時,紫外線穩定聚碳酸酯和玻璃纖維等材料的創新,有效解決了腐蝕、散熱和重量等難題。供應商正透過模組化、溫度控管和工業物聯網 (IIoT) 連接來打造差異化優勢,並積極尋求策略併購,專注於資料中心、可再生能源和電網現代化等細分領域。

全球電氣外殼市場趨勢與洞察

加速可再生能源設施的擴張

公用事業規模的太陽能和離岸風力發電指定使用防護等級為 IP67/IP68 的機櫃,這些機櫃能夠承受鹽霧、超過 1000 W/m² 的紫外線輻射以及超過 70°C 的內部溫度。主動冷卻、突波保護和整合通訊模組是太陽能匯流箱、逆變器外殼和電池儲能配電盤的基本要求。符合 IEC 61215 和 UL 1741 標準指導機櫃設計,並增強電弧故障偵測和絕緣追蹤功能,以確保安全並網。

工業自動化和工業4.0的擴展

數位化化工廠將振動、濕度和溫度感測器直接整合到開關設備中,從而將非計劃性停機時間減少高達 82%。隨著邊緣伺服器從控制室轉移到現場,機櫃必須能夠散發更高的熱負荷。面板內部溫度每升高 10°C,故障風險就會增加一倍。模組化框架和快速安裝導軌系統可以實現快速調整,幫助汽車、電子和食品製造商適應訂單策略。

原物料價格波動

能源成本飆升和出口限制導致鋁材溢價在2024年上漲10%,擠壓機殼毛利率,並促使廠商簽訂雙重採購協議。不銹鋼附加費與鎳價波動掛鉤,迫使原始設備製造商(OEM)在300毫米以上的機櫃中轉向使用玻璃纖維增強塑膠和聚碳酸酯。外匯波動進一步加劇了成本計算的複雜性,導致廠商採用準時制庫存管理和在多年合約中加入價格調整條款。

細分市場分析

到2025年,金屬外殼在機殼。碳鋼是工廠自動化領域的主流材料,而316L不銹鋼則是食品、製藥和海洋環境領域的主流材料。非金屬外殼市場規模預計將以7.98%的複合年成長率成長,超過整體市場成長速度,因為聚碳酸酯具有IK10抗衝擊等級和25年抗紫外線性能,而成本約為不銹鋼的三分之一。玻璃纖維增強聚酯材料因其良好的可塑性和耐化學性,將在300mm x 300mm以上的機櫃市場佔據主導地位,而鋁材將滿足鐵路和航太產業對輕量化的需求。

聚碳酸酯箱體整合透明蓋,方便目視檢查,並採用正在申請專利的鉸鏈鏈卡扣,可將組裝時間縮短 40%。玻璃纖維的介電強度使其可在帶電作業,且無需接地裝置。不銹鋼在衛生應用領域仍佔據主導地位,其無焊接接縫和光滑的 4 號表面可抑制細菌滋生。供應商正競相研發新一代阻燃樹脂和生物基複合複合材料,以便在不影響性能的前提下減少生命週期排放。

預計到2025年,壁掛式機櫃將在分散式控制迴路和建築自動化終端市場佔據46.20%的收入佔有率。然而,隨著設施擴建和資料中心需求的成長,電氣外殼市場正轉向落地式機架,其複合年成長率(CAGR)高達7.51%,這主要得益於超大規模業者採用承重能力達3500磅的通道封閉式機架。模組化底座允許電纜從各個方向接入,抗震套件符合加州和日本4區抗震標準。

電線杆和地面安裝設備支援電錶、電動車充電器和 5G 節點,並採用粉末塗層鋁製機殼和防破壞鎖。地下安裝式設備專為郊區電網設計,透過將開關設備隱藏在地面蓋板下,保持街道景觀的美觀。製造商正在推廣快速搖擺門和 180 度鉸鏈,即使在狹窄的通道中,也能讓技術人員暢通無阻地維護設備。

區域分析

北美地區將佔2025年總收入的38.10%,這主要得益於美國老舊開關設備的更換以及為加強電網網路安全防護所做的努力。聯邦政府資助的智慧電網部署計畫強制要求採用符合IEEE 1613標準的機殼級入侵偵測和突波保護裝置。在加拿大,面臨-40°C嚴寒冬季的採礦、液化天然氣和風電發電工程,由於玻璃纖維和雙層鋼具有優異的隔熱性能,因此更傾向於使用這兩種材料。

亞太地區將以7.22%的複合年成長率實現最快增速,各國政府在輸電走廊、半導體製造廠和高速鐵路領域的投資超過3兆美元。中國正逐步淘汰焊接鋼箱,轉而採用智慧化的、配備豐富感測器的配電櫃,並將其接入變電站的數位雙胞胎。印度的智慧城市規劃將33千伏環路開關與可抵禦季風洪水的墊片安裝式組合控制亭結合。東南亞正積極推動電子製造業的轉移,因此對能夠承受90%相對濕度的不銹鋼控制設備的訂單大幅成長。

在歐洲,離岸風電、氫能和工廠自動化計畫正穩步推進。德國在工業4.0應用方面主導,已將狀態監測功能整合到Rittal VX系列機架中。北歐公用事業公司要求使用配備矽膠加熱器和透氣親水通風口的耐寒外殼。歐盟網路安全法規要求原始設備製造商(OEM)在控制面板門中整合安全啟動和防篡改記錄功能,這增加了認證的複雜性。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 可再生能源的快速發展

- 工業自動化和工業4.0的擴展

- 電網現代化與變電站維修

- 更嚴格的全球安全和防塵/防水標準

- 戶外5G小型基地台部署需要IP防護等級的外殼。

- 用於預測性維護的智慧物聯網機殼

- 市場限制

- 原物料價格(鋼鐵、鋁)波動

- 密封完整性和溫度控管故障

- 網路機殼中的網路攻擊風險

- 客製化製造業技術純熟勞工短缺

- 產業價值鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 材料

- 金屬(碳鋼、不鏽鋼、鋁)

- 非金屬材質(聚碳酸酯、玻璃纖維增強塑膠、聚酯、ABS樹脂)

- 按安裝類型

- 壁掛式

- 落地式/獨立式

- 地下安裝類型/地上安裝類型

- 桿式安裝型

- 按外形規格

- 小型(小於10公升)

- 緊湊型(10-50公升)

- 均碼/大尺寸(50公升或以上)

- 模組化/可配置系統

- 按最終用戶行業分類

- 能源與電力

- 石油和天然氣

- 工業製造與機器人

- 金屬和採礦

- 交通運輸(鐵路、公路、航空、電動車充電)

- 資料中心和電信

- 食品、飲料和藥品

- 按地區

- 北美洲

- 美國

- 加拿大

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 亞太其他地區

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 其他中東地區

- 非洲

- 南非

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Schneider Electric SE

- ABB Ltd.

- Eaton Corporation plc

- nVent Electric plc(Hoffman and Schroff)

- Rittal GmbH and Co. KG

- Emerson Electric Company

- Hubbell Incorporated

- Pentair plc

- Legrand SA

- Hammond Manufacturing Ltd.

- AZZ Inc.

- Adalet(Scott Fetzer Company)

- Allied Moulded Products, Inc.

- Fibox Oy Ab

- Eldon Holding AB

- Siemens AG

- General Electric Company

- Saginaw Control and Engineering

- BOXCO Co., Ltd.

- Nitto Kogyo Corp.

- Socomec Group SA

- Bison ProFab Inc.

- Integra Enclosures Inc.

- Austin Electrical Enclosures

- ITS Enclosures(Builder's Service Company)

第7章 市場機會與未來展望

The electrical enclosures market was valued at USD 8.11 billion in 2025 and estimated to grow from USD 8.61 billion in 2026 to reach USD 11.58 billion by 2031, at a CAGR of 6.11% during the forecast period (2026-2031).

Demand accelerates as utilities, factories and telecom providers replace legacy cabinets with intelligent housings that host sensors, edge processors and wireless modules. Rapid power-sector build-outs, 5G densification and the electrification of transportation keep ordering cycles robust, while material innovations such as UV-stabilized polycarbonate and fiberglass address corrosion, thermal and weight challenges. Vendors differentiate through modularity, thermal management and IIoT connectivity, driving strategic mergers focused on data-center, renewable-energy and grid-modernization niches.

Global Electrical Enclosures Market Trends and Insights

Accelerating Renewable-Energy Build-Out

Utility-scale solar and offshore-wind farms specify IP67/IP68 cabinets that tolerate salt spray, UV irradiance above 1,000 W/m2 and internal temperatures surpassing 70 °C. Active cooling, surge protection and integrated communication modules are now baseline requirements for photovoltaic combiner boxes, inverter housings and battery-energy-storage switchboards. Compliance with IEC 61215 and UL 1741 standards guides enclosure designs toward enhanced arc-fault detection and insulation tracking, supporting safe grid interconnection.

Industrial Automation and Industry 4.0 Expansion

Digitized plants embed vibration, humidity and temperature sensors directly in switchgear to cut unplanned downtime by up to 82%. As edge servers migrate from control rooms to the shop floor, cabinets must dissipate higher heat loads; every 10 °C rise inside a panel doubles outage risk. Modular frames and quick-mount rail systems enable rapid re-tooling, helping automotive, electronics and food producers align with make-to-order strategies.

Raw-Material Price Volatility

Aluminum premiums rose 10% in 2024 amid energy-cost spikes and export curbs, squeezing enclosure gross margins and prompting dual-sourcing pacts. Stainless-steel surcharges track nickel swings, pushing OEMs toward fiberglass and polycarbonate for cabinets exceeding 300 mm dimensions. Currency gyrations further complicate costing, prompting just-in-time inventories and price-adjustment clauses in multiyear framework deals.

Other drivers and restraints analyzed in the detailed report include:

- Grid-Modernization and Substation Retrofits

- Stricter Global Safety and Ingress-Protection Codes

- Seal-Integrity and Thermal-Management Failures

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Metallic housings retained 74.15% of electrical enclosures market share in 2025, anchored by carbon steel in factory automation and 316L stainless in food, pharma and marine environments. The electrical enclosures market size for non-metallic alternatives is projected to grow at an 7.98% CAGR, outpacing the overall curve as polycarbonate delivers IK10 impact ratings and 25-year UV endurance at roughly one-third the cost of stainless. Fiberglass-reinforced polyester dominates cabinets larger than 300 mm X 300 mm thanks to moldability and chemical resistance, while aluminum addresses rail and aerospace weight targets.

Polycarbonate boxes integrate transparent lids for visual inspection and patent-pending hingeless snaps that cut assembly time by 40%. Fiberglass' dielectric strength supports live-line work, eliminating grounding hardware. Stainless continues to command hygienic applications where weld-less seams and smooth #4 finishes deter bacterial growth. Vendors compete on next-generation flame-retardant resins and bio-based composites that reduce lifecycle emissions without sacrificing performance.

Wall-mounted cabinets captured 46.20% revenue in 2025 for distributed control loops and building automation endpoints. Facility expansions and data centers, however, are driving the electrical enclosures market toward floor-standing racks, forecast to post a 7.51% CAGR as hyperscale operators adopt aisle-containment frames with 3,500-lb load ratings. Modular base plinths enable cable entry from any side, while seismic kits satisfy Zone 4 requirements in California and Japan.

Pole- and pad-mounted variants support utility metering, EV chargers and 5G nodes, combining powder-coated aluminum shells with vandal-proof locks. Underground housings serve suburban distribution networks, hiding switchgear beneath grade-level lids to preserve streetscape aesthetics. Manufacturers push quick-swing doors and 180-degree hinges that let technicians service gear without obstruction in cramped corridors.

The Electrical Enclosures Market Report is Segmented by Material (Metallic, and Non-Metallic), Mounting Type (Wall-Mounted, Floor-mounted/Free-standing, and More), Form Factor (Small [Less Than or Equal To 10L], Compact [10-50L], and More), End-User Industry (Energy and Power, Oil and Gas, Industrial Manufacturing and Robotics, Metals and Mining, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America accounted for 38.10% of 2025 revenue, led by United States initiatives to replace aging switchgear and harden grids against cyber threats. Federal funding drives smart-grid rollouts that specify enclosure-level intrusion detection and IEEE 1613-rated surge protection. Canada adds demand from mining, LNG and wind projects that face -40 °C winters, favoring fiberglass and double-wall steel for thermal buffering.

Asia-Pacific will register the quickest 7.22% CAGR as governments channel more than USD 3 trillion into transmission corridors, semiconductor fabs and high-speed rail. China transitions from welded sheet-metal boxes to intelligent, sensor-rich cabinets that feed substation digital twins. India's smart-city plans couple 33-kV ring-main units with pad-mounted composite kiosks capable of resisting monsoon floods. Southeast Asia absorbs relocated electronics manufacturing, lifting orders for stainless controls that endure 90% relative humidity.

Europe advances steadily on offshore-wind, hydrogen and factory-automation programs. Germany leads Industry 4.0 adoption, embedding condition monitoring in Rittal VX series racks. Nordic utilities request cold-climate enclosures that deploy silicon heaters and breathable hydrophilic vents. The EU Cyber-Resilience Act pushes OEMs to embed secure boot and tamper logging at the panel door, elevating certification complexity.

- Schneider Electric SE

- ABB Ltd.

- Eaton Corporation plc

- nVent Electric plc (Hoffman and Schroff)

- Rittal GmbH and Co. KG

- Emerson Electric Company

- Hubbell Incorporated

- Pentair plc

- Legrand SA

- Hammond Manufacturing Ltd.

- AZZ Inc.

- Adalet (Scott Fetzer Company)

- Allied Moulded Products, Inc.

- Fibox Oy Ab

- Eldon Holding AB

- Siemens AG

- General Electric Company

- Saginaw Control and Engineering

- BOXCO Co., Ltd.

- Nitto Kogyo Corp.

- Socomec Group SA

- Bison ProFab Inc.

- Integra Enclosures Inc.

- Austin Electrical Enclosures

- ITS Enclosures (Builder's Service Company)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating renewable-energy build-out

- 4.2.2 Industrial automation and Industry 4.0 expansion

- 4.2.3 Grid-modernization and substation retrofits

- 4.2.4 Stricter global safety and ingress-protection codes

- 4.2.5 Outdoor 5G small-cell rollout needing IP-rated housings

- 4.2.6 Smart, IoT-enabled enclosures for predictive maintenance

- 4.3 Market Restraints

- 4.3.1 Raw-material price volatility (steel, aluminium)

- 4.3.2 Seal-integrity and thermal-management failures

- 4.3.3 Cyber-attack risk in connected enclosures

- 4.3.4 Skilled-labour shortage for custom fabrication

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Metallic (Carbon Steel, Stainless Steel, Aluminum)

- 5.1.2 Non-metallic (Polycarbonate, Fiberglass, Polyester, ABS)

- 5.2 By Mounting Type

- 5.2.1 Wall-mounted

- 5.2.2 Floor-mounted / Free-standing

- 5.2.3 Underground / Pad-mounted

- 5.2.4 Pole-mounted

- 5.3 By Form Factor

- 5.3.1 Small (Less than or Equal to 10 L)

- 5.3.2 Compact (10-50 L)

- 5.3.3 Free-size / Full-size (Above 50 L)

- 5.3.4 Modular / Configurable systems

- 5.4 By End-user Industry

- 5.4.1 Energy and Power

- 5.4.2 Oil and Gas

- 5.4.3 Industrial Manufacturing and Robotics

- 5.4.4 Metals and Mining

- 5.4.5 Transportation (Rail, Road, Air, EV-charging)

- 5.4.6 Data Centres and Telecom

- 5.4.7 Food and Beverage and Pharmaceuticals

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Schneider Electric SE

- 6.4.2 ABB Ltd.

- 6.4.3 Eaton Corporation plc

- 6.4.4 nVent Electric plc (Hoffman and Schroff)

- 6.4.5 Rittal GmbH and Co. KG

- 6.4.6 Emerson Electric Company

- 6.4.7 Hubbell Incorporated

- 6.4.8 Pentair plc

- 6.4.9 Legrand SA

- 6.4.10 Hammond Manufacturing Ltd.

- 6.4.11 AZZ Inc.

- 6.4.12 Adalet (Scott Fetzer Company)

- 6.4.13 Allied Moulded Products, Inc.

- 6.4.14 Fibox Oy Ab

- 6.4.15 Eldon Holding AB

- 6.4.16 Siemens AG

- 6.4.17 General Electric Company

- 6.4.18 Saginaw Control and Engineering

- 6.4.19 BOXCO Co., Ltd.

- 6.4.20 Nitto Kogyo Corp.

- 6.4.21 Socomec Group SA

- 6.4.22 Bison ProFab Inc.

- 6.4.23 Integra Enclosures Inc.

- 6.4.24 Austin Electrical Enclosures

- 6.4.25 ITS Enclosures (Builder's Service Company)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

電氣外殼市場:按類型、安裝配置、材質、最終用途產業和應用分類-2026-2032年全球市場預測電氣櫃及外殼市場:依材質、防護等級、額定電壓、產品類型及最終用戶產業分類-2026-2032年全球市場預測全球機櫃冷卻器市場按類型、冷卻能力、機櫃類型、安裝方式、最終用途產業和分銷管道分類,2026-2032年預測

電氣外殼市場:按類型、安裝配置、材質、最終用途產業和應用分類-2026-2032年全球市場預測電氣櫃及外殼市場:依材質、防護等級、額定電壓、產品類型及最終用戶產業分類-2026-2032年全球市場預測全球機櫃冷卻器市場按類型、冷卻能力、機櫃類型、安裝方式、最終用途產業和分銷管道分類,2026-2032年預測 印度電氣外殼市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)美國電氣機殼:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

印度電氣外殼市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)美國電氣機殼:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 電氣外殼市場規模、佔有率、成長及全球產業分析:按類型、應用和地區的洞察,2026-2034年預測

電氣外殼市場規模、佔有率、成長及全球產業分析:按類型、應用和地區的洞察,2026-2034年預測 2026年全球電氣外殼市場報告不銹鋼烘乾櫃市場按產品類型、材質等級、容量、價格範圍、應用、終端用戶產業和分銷管道分類-2026-2032年全球預測電池外殼及機櫃市場(依產品類型、安裝類型、材料、電池類型、最終用戶和應用分類)-全球預測,2026-2032年

2026年全球電氣外殼市場報告不銹鋼烘乾櫃市場按產品類型、材質等級、容量、價格範圍、應用、終端用戶產業和分銷管道分類-2026-2032年全球預測電池外殼及機櫃市場(依產品類型、安裝類型、材料、電池類型、最終用戶和應用分類)-全球預測,2026-2032年 塑膠外殼市場規模、佔有率和成長分析(按應用、最終用途產業、材質、配置類型、產業標準和地區分類)-2026-2033年產業預測

塑膠外殼市場規模、佔有率和成長分析(按應用、最終用途產業、材質、配置類型、產業標準和地區分類)-2026-2033年產業預測