|

市場調查報告書

商品編碼

1905982

歐洲膠原蛋白:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Europe Collagen - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

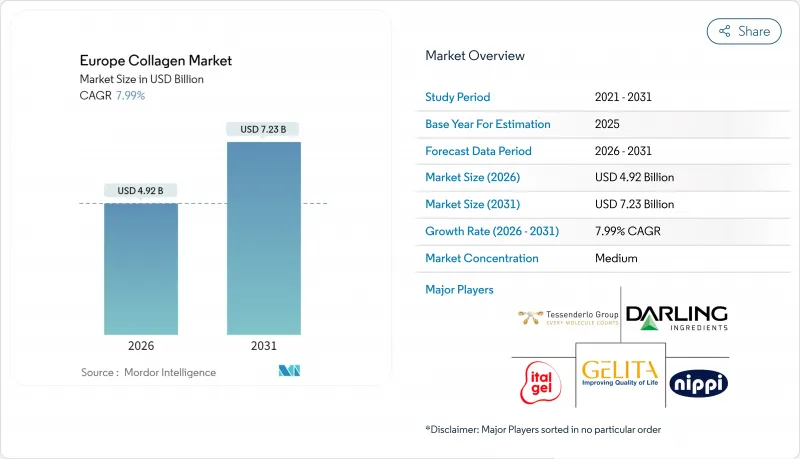

歐洲膠原蛋白市場預計將從 2025 年的 45.6 億美元成長到 2026 年的 49.2 億美元,預計到 2031 年將達到 72.3 億美元,2026 年至 2031 年的複合年成長率為 7.99%。

隨著消費者對健康維護、顯著的皮膚改善效果和關節護理功效的日益關注,該品類正在穩步升級。同時,有關健康聲明的監管政策日益明朗,加速了高級產品的創新。市場需求正從傳統的牛和豬來源轉向可追溯的海洋來源,後者俱有更高的生物利用度和更低的環境影響。將臨床驗證與負責任的採購相結合的品牌所有者正在獲得顯著的商店佔有率。德國、法國和荷蘭的零售商報告稱,儘管海洋膠原蛋白產品的價格高於同類產品的平均水平,但其銷售仍保持兩位數的持續成長。精準發酵和重組平台的創新正在拓展醫療設備和機能性食品領域的應用範圍,而一體化生產商則正利用其規模優勢來應對歐盟嚴格的合規環境。

歐洲膠原蛋白市場趨勢與洞察

消費者對健康和保健產品的需求不斷成長

歐洲消費者正積極擁抱預防性醫療保健策略,將焦點從被動的醫療照護轉向主動的健康管理。這種轉變使得膠原蛋白的應用範圍從傳統的美容領域擴展到功能性營養領域。尤其值得一提的是,35至55歲的消費者普遍認為補充膠原蛋白對於維持關節活動度和皮膚彈性至關重要。人口老化以及日益增強的健康意識,共同推動了對高品質膠原蛋白產品的穩定需求。歐洲消費者尤其願意為經科學驗證的配方支付25%至40%的溢價。此外,在歐洲食品安全局(EFSA)的指導下,法規結構正逐步核准膠原蛋白肽的健康聲明,為生產商提供了更清晰的產品定位和行銷策略。

人口老化社會尋求關節護理解決方案

隨著歐洲人口老化,對關節護理解決方案的需求激增。根據歐盟統計局的預測,歐洲老年人口扶養比預計將從2023年的33.4%上升至2100年的59.7%。發表在《整合與補充醫學日誌》上的一項臨床研究表明,補充未變性II型膠原蛋白可顯著改善膝關節的柔軟性。具體而言,在補充24週後,受試者的膝關節屈曲角度提高了3.23度,伸展角度提高了2.21度。這種人口結構的變化導致對膠原蛋白類關節保健產品的需求持續成長,尤其是在50歲以上、活動時容易出現關節不適的歐洲人群中。由於水解膠原蛋白類產品具有高生物利用度和已證實的臨床益處,因此在歐洲市場更受歡迎。值得注意的是,每日攝取10克膠原蛋白正逐漸成為關節保健應用的標準劑量。此外,歐洲各地的醫療保健系統越來越重視膠原蛋白補充劑,認為這是一種經濟有效的策略,不僅可以維持關節功能,還可以降低長期整形外科治療費用。

植物蛋白替代品的興起

在歐洲市場,植物來源蛋白替代品的成長和合成生物學的進步正加速傳統膠原蛋白來源模式的挑戰。 PlantForm公司用於生產重組人類膠原膠原蛋白的植物性系統證明了純素替代品的商業性可行性,預計到2030年,該市場規模將達到114億美元。消費者的偏好正轉向符合倫理和永續的選擇,尤其是在越來越關注環境影響和動物福利的年輕一代。隨著純素膠原蛋白替代品在功能上達到與動物源產品相當的水平,同時又具有更高的均一性和監管優勢,市場競爭日益激烈。為了應對這項挑戰,歐洲製造商正在投資基於發酵的生產技術,並開發融合傳統和替代蛋白質來源的混合配方,以在保持市場地位的同時,解決倫理方面的擔憂。

細分市場分析

動物源膠原膠原蛋白將繼續引領市場,預計到2025年將佔據65.05%的市場佔有率,這主要得益於成熟的供應鏈以及消費者對牛和豬源膠原蛋白成分的認知度不斷提高。然而,海洋源膠原膠原蛋白預計將展現出更強勁的成長潛力,到2031年複合年成長率將達到10.11%,這主要得益於其永續性優勢以及優先考慮可追溯海洋來源而非傳統動物來源的監管優勢。海洋膠原蛋白市場正受益於萃取技術的進步以及消費者對其卓越生物利用度的日益認可,其中魚源膠原膠原蛋白的吸收率是哺乳動物源膠原蛋白的1.5倍。

由於海洋來源的原料能降低瘋牛症風險並滿足明確的可追溯性要求,歐洲法規結構越來越傾向於使用海洋來源的原料。歐洲食品安全局(EFSA)的評估也證實了海洋來源的膠原蛋白比反芻動物來源的膠原膠原蛋白更具安全優勢。從魚類加工產品中提取海洋膠原蛋白的創新技術,在解決永續性問題的同時,也為廢棄物創造了經濟價值。研究表明,僅歐洲漁業每年就具有超過6500噸的產量潛力。競爭格局正在發生變化,傳統的動物膠原蛋白生產商正在投資海洋加工能力,而專業的海洋生物技術公司則透過高階定位和永續性認證來擴大市場佔有率。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 消費者對健康和保健產品的需求不斷成長;

- 老齡化人口尋求關節護理解決方案

- 美容和個人護理領域的擴張

- 在營養補充品領域的應用不斷拓展

- 向永續海洋膠原蛋白來源過渡

- 研究、開發和生產的創新進展

- 市場限制

- 植物蛋白替代品的興起

- 嚴格的監管合規和認證要求

- 與動物源性膠原蛋白相關的倫理和致敏性問題

- 採購及加工優質膠原蛋白原料成本高昂

- 供應鏈分析

- 監理展望

- 波特五力模型

- 新進入者的威脅

- 買方/消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 起源

- 動物源性

- 海洋來源

- 最終用戶/使用

- 食品/飲料

- 營養補充品

- 個人護理及化妝品

- 製藥

- 動物飼料

- 按地區

- 德國

- 英國

- 義大利

- 法國

- 西班牙

- 荷蘭

- 其他歐洲地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市場排名分析

- 公司簡介

- Gelita AG

- Darling Ingredients Inc.(Rousselot)

- PB Leiner(Tessenderlo Group)

- Italgel Srl

- Nippi, Incorporated

- Lapi Gelatine SpA

- Collagen Solutions Plc

- DSM-Firmenich

- Symrise AG

- Weishardt Group

- Gelnex

- Lonza Group Ltd.

- BioCell Technology LLC

- Jellagen Ltd

- CollaSwiss(Swiss Nutrivalor)

- Medichema GmbH

- Evonik Industries AG

- Essentia Protein Solutions

- PB Gelatins

- NovaColl(Geltor)

第7章 市場機會與未來展望

The European collagen market is expected to grow from USD 4.56 billion in 2025 to USD 4.92 billion in 2026 and is forecast to reach USD 7.23 billion by 2031 at 7.99% CAGR over 2026-2031.

Heightened consumer focus on proactive health, visible skin benefits, and joint-care efficacy underpins steady category trading up, while regulatory clarity on permissible health claims accelerates premium innovation. Demand is shifting from conventional bovine and porcine ingredients to traceable marine sources that offer superior bioavailability and a smaller environmental footprint. Brand owners that combine clinical substantiation with responsible sourcing capture disproportionate shelf visibility, and German, French, and Dutch retailers report sustained double-digit sell-out for marine collagen lines despite above-category price points. Innovation in precision fermentation and recombinant platforms is widening the addressable use-case set in medical devices and functional foods, while integrated producers leverage their scale to navigate the European Union's demanding compliance landscape.

Europe Collagen Market Trends and Insights

Increasing Consumer Demand for Health and Wellness Products

European consumers are increasingly adopting preventive health strategies, shifting their focus from reactive healthcare to proactive wellness management. This shift has expanded the use of collagen from traditional beauty applications to functional nutrition. Educated consumers aged 35-55, in particular, consider collagen supplementation essential for maintaining joint mobility and skin elasticity. The combination of aging demographics and rising health awareness is driving consistent demand for premium collagen products. European consumers are notably willing to pay 25-40% more for scientifically validated formulations. Additionally, regulatory frameworks under EFSA guidance are increasingly endorsing health claims for collagen peptides, providing manufacturers with clearer opportunities for product positioning and marketing communications.

Ageing Population Seeking Joint-Care Solutions

Europe's aging population is fueling a surge in demand for joint-care solutions. Projections from Eurostat indicate that the old-age dependency ratio in Europe will rise from 33.4% in 2023 to a staggering 59.7% by 2100. Clinical studies, as highlighted in the Journal of Integrative and Complementary Medicine, have shown that supplementation with undenatured type II collagen can notably enhance knee joint flexibility. Specifically, after 24 weeks of supplementation, subjects exhibited a 3.23° improvement in flexion and a 2.21° boost in extension. This demographic evolution is propelling a consistent demand for collagen-infused joint health products, especially among Europeans over 50 who often grapple with activity-induced joint discomfort. The European market is leaning towards collagen hydrolysate formulations, prized for their bioavailability and proven clinical benefits. Notably, a daily dosage of 10g has emerged as the benchmark for joint health applications. Furthermore, healthcare systems across Europe are increasingly viewing collagen supplementation as a budget-friendly strategy, not only to uphold joint function but also to potentially curtail long-term orthopedic care expenses.

Rise of Vegan Protein Alternatives

The European market is under increasing pressure from the growth of plant-based protein alternatives and advancements in synthetic biology, which challenge traditional collagen sourcing models. PlantForm Corporation's production of recombinant human collagen using plant-based systems highlights the commercial feasibility of vegan alternatives, with the market projected to reach USD 11.4 billion by 2030. Consumer preferences are shifting toward ethical and sustainable options, particularly among younger demographics who emphasize environmental impact and animal welfare. The competition intensifies as vegan collagen alternatives achieve functional equivalence with animal-derived products while offering better consistency and regulatory benefits. In response, European manufacturers are investing in fermentation-based production technologies and creating hybrid formulations that integrate traditional and alternative protein sources to retain their market position while addressing ethical concerns.

Other drivers and restraints analyzed in the detailed report include:

- Expansion in the Beauty and Personal Care Sector

- Increasing Applications in Dietary Supplements

- Stringent Regulatory Compliance and Certification Requirements

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Animal-based collagen maintains market leadership with a 65.05% share in 2025, reflecting established supply chains and consumer familiarity with bovine and porcine sources. However, marine-based collagen demonstrates superior growth dynamics at 10.11% CAGR through 2031, driven by sustainability advantages and regulatory preferences that favor traceable marine sources over traditional animal derivatives. The marine segment benefits from technological advances in extraction methods and growing consumer awareness of bioavailability advantages, with fish collagen demonstrating 1.5 times higher absorption rates than mammalian alternatives.

European regulatory frameworks increasingly favor marine sources due to reduced BSE risk and clearer traceability requirements, with EFSA assessments confirming safety advantages over ruminant-derived collagen. Innovation in marine collagen extraction from fish processing by-products addresses sustainability concerns while creating economic value from waste streams, with research demonstrating potential annual production exceeding 6,500 tons from European fisheries alone. The competitive landscape evolves as traditional animal collagen producers invest in marine processing capabilities while specialized marine biotechnology companies gain market share through premium positioning and sustainability credentials.

The Europe Collagen Market Report is Segmented by Source (Animal-Based, Marine-Based), End User/Application (Food & Beverages, Dietary Supplements, Personal Care & Cosmetics, Pharmaceuticals, Animal Nutrition), and Geography (Germany, United Kingdom, Italy, France, Spain, Netherlands, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Gelita AG

- Darling Ingredients Inc. (Rousselot)

- PB Leiner (Tessenderlo Group)

- Italgel S.r.l.

- Nippi, Incorporated

- Lapi Gelatine S.p.A.

- Collagen Solutions Plc

- DSM-Firmenich

- Symrise AG

- Weishardt Group

- Gelnex

- Lonza Group Ltd.

- BioCell Technology LLC

- Jellagen Ltd

- CollaSwiss (Swiss Nutrivalor)

- Medichema GmbH

- Evonik Industries AG

- Essentia Protein Solutions

- PB Gelatins

- NovaColl (Geltor)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing consumer demand for health and wellness products,

- 4.2.2 Ageing population seeking joint-care solutions

- 4.2.3 Expansion in the beauty and personal care sector

- 4.2.4 Increasing Applications in Dietary Supplements

- 4.2.5 Shift toward sustainable marine collagen sources

- 4.2.6 Rising Innovation in research and production

- 4.3 Market Restraints

- 4.3.1 Rise of vegan protein alternatives

- 4.3.2 Stringent regulatory compliance and certification requirements

- 4.3.3 Ethical and allergenic concerns related to animal-derived collagen

- 4.3.4 High costs of sourcing and processing high-quality collagen raw materials

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECAST

- 5.1 By Source

- 5.1.1 Animal-based

- 5.1.2 Marine-based

- 5.2 By End User / Application

- 5.2.1 Food & Beverages

- 5.2.2 Dietary Supplements

- 5.2.3 Personal Care & Cosmetics

- 5.2.4 Pharmaceuticals

- 5.2.5 Animal Nutrition

- 5.3 By Geography

- 5.3.1 Germany

- 5.3.2 United Kingdom

- 5.3.3 Italy

- 5.3.4 France

- 5.3.5 Spain

- 5.3.6 Netherlands

- 5.3.7 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials (if available), Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 Gelita AG

- 6.4.2 Darling Ingredients Inc. (Rousselot)

- 6.4.3 PB Leiner (Tessenderlo Group)

- 6.4.4 Italgel S.r.l.

- 6.4.5 Nippi, Incorporated

- 6.4.6 Lapi Gelatine S.p.A.

- 6.4.7 Collagen Solutions Plc

- 6.4.8 DSM-Firmenich

- 6.4.9 Symrise AG

- 6.4.10 Weishardt Group

- 6.4.11 Gelnex

- 6.4.12 Lonza Group Ltd.

- 6.4.13 BioCell Technology LLC

- 6.4.14 Jellagen Ltd

- 6.4.15 CollaSwiss (Swiss Nutrivalor)

- 6.4.16 Medichema GmbH

- 6.4.17 Evonik Industries AG

- 6.4.18 Essentia Protein Solutions

- 6.4.19 PB Gelatins

- 6.4.20 NovaColl (Geltor)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

膠原蛋白市場:2026-2032年全球市場預測(依膠原蛋白類型、原料、形態、萃取製程、等級、應用及銷售管道)

膠原蛋白市場:2026-2032年全球市場預測(依膠原蛋白類型、原料、形態、萃取製程、等級、應用及銷售管道) 2026年全球膠原蛋白市場報告

2026年全球膠原蛋白市場報告 膠原蛋白市場規模、佔有率、趨勢和預測:按原料、產品、應用和地區分類,2026-2034年

膠原蛋白市場規模、佔有率、趨勢和預測:按原料、產品、應用和地區分類,2026-2034年 膠原蛋白原料市場規模、佔有率及成長分析(依原料來源、產品類型、應用、形態及地區分類)-產業預測(2026-2033 年)未變性 II 型膠原蛋白市場按來源、形式、劑量、最終用途、分銷管道和應用分類——全球預測,2026-2032 年食品級尿石素A市場按應用、形態、最終用戶、來源和通路分類-2026-2032年全球預測日本膠原蛋白市場報告(按來源、產品、應用和地區分類,2026-2034年)

膠原蛋白原料市場規模、佔有率及成長分析(依原料來源、產品類型、應用、形態及地區分類)-產業預測(2026-2033 年)未變性 II 型膠原蛋白市場按來源、形式、劑量、最終用途、分銷管道和應用分類——全球預測,2026-2032 年食品級尿石素A市場按應用、形態、最終用戶、來源和通路分類-2026-2032年全球預測日本膠原蛋白市場報告(按來源、產品、應用和地區分類,2026-2034年) 膠原蛋白市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)

膠原蛋白市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年) 膠原蛋白市場規模、佔有率和趨勢分析報告:按原料、產品、應用、地區和細分市場預測(2025-2033 年)

膠原蛋白市場規模、佔有率和趨勢分析報告:按原料、產品、應用、地區和細分市場預測(2025-2033 年) 膠原蛋白:全球市場佔有率和排名、總收入和需求預測(2025-2031年)

膠原蛋白:全球市場佔有率和排名、總收入和需求預測(2025-2031年)