|

市場調查報告書

商品編碼

1852178

二手卡車:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)Used Truck - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

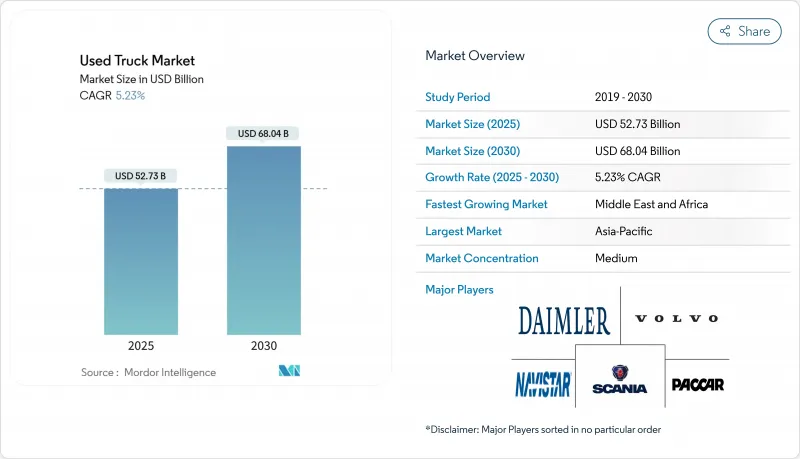

預計到 2025 年,二手卡車市場規模將達到 527.3 億美元,到 2030 年將達到 680.4 億美元。

由於車隊管理者更重視整體擁有成本,市場對高品質二手8級卡車的需求強勁。雖然大型卡車仍保持著定價權,但隨著電子商務加速最後一公里配送,小型卡車也越來越受歡迎。柴油卡車在動力系統方面佔據主導地位,但隨著競標動力傳動系統正在促進跨國交易,並降低小型企業的資訊取得門檻。

全球二手卡車市場趨勢與洞察

印度和東協的主導設施建設熱潮推動了重型二手卡車的流通。

印度和東南亞的大型企劃建設項目正在加速車隊更新換代,促使承包商採購更大、車齡四至七年的車輛,以兼顧可靠性和可控的資本支出。隨著計劃於2025年5月開工,敞篷貨車運力趨緊,迫使托運人在競標週期早期就鎖定設備。儘管2024年輕型商用車銷售量大幅下滑,但由於基礎建設投資保障了貨運量,商用車需求依然強勁。買家越來越重視車輛的檢驗記錄,擁有完整遠端資訊處理資料的車輛價格更高,這凸顯了透明的車輛認證對二手卡車市場的重要性。

北美最後一公里電子商務的擴張正在推動對二手輕型卡車的需求。

小包裹量的快速成長正促使零售商和第三方物流供應商轉向更適合狹窄都市區走廊且負載容量更大的3-5級新型貨車。由於營運商既能避免不斷上漲的新車價格,又能滿足服務水準協議的要求,二手卡車市場從中受益。沿著州際公路環線建設的都市區倉庫也支援縮短配送半徑。環境研究表明,電動貨車的碳排放強度更低,隨著二手電動車型逐漸退出主力車隊,其殘值也更高。

歐盟VII/第三階段:更嚴格的氮氧化物排放法規限制了老舊柴油引擎進口到歐盟

更嚴格的廢氣排放法規使歐洲二次性車市場分化:一部分是符合歐六排放標準的牽引車,另一部分則是需要進行成本高昂維修的老舊車輛。國際清潔交通委員會已確認,在不斷擴大的低排放氣體區,車齡超過七年的車輛將受到准入限制。出口商正將不符合歐六排放標準的車輛轉運至中亞和北非,這暫時增加了這些地區的供應量,同時也加劇了歐盟內部來自低里程歐六排放標準車輛的競爭。

細分市場分析

由於重型卡車在遠距貨運和基礎設施運輸中發揮至關重要的作用,即使在景氣衰退時期,其需求依然旺盛,預計2024年將佔總銷售量的43.05%。受包裹物流的推動,輕型卡車預計將在二手卡車市場實現最快成長,到2030年複合年成長率將達到7.69%。輕型卡車的機動性使其非常適合繁忙的城市道路,而且與新貨車相比,其較低的購買成本也更受車隊買家的青睞。

中型卡車(6-7級)佔據戰略性的中間位置,市場表現好壞參半。該細分市場庫存激增,而要價卻有所下降,顯示其市場狀況較為微妙。正在進行的自動駕駛測試,例如在2025年國際消費電子展(CES 2025)上展出的鉸接式自動卸貨卡車,預示著未來將出現一些專用的重型應用,一旦這些車輛進入二手車市場,可能會重新定義殘值曲線。

2024年,柴油資產佔車隊總資產的92.25%,顯示柴油車擁有完善的基礎設施、成熟的維護體係以及車隊管理者信賴的燃油效率記錄。柴油車市場持續成長的動力源於其久經考驗的可靠性、燃油效率和廣泛的服務網路,使其成為優先考慮營運穩定性的二手車買家的首選。

混合動力車和純電動車雖然目前絕對數量仍然較小,但預計到2030年將以22.55%的複合年成長率成長。由康明斯、戴姆勒卡車和帕卡集團合資成立的Accellera公司(投資額20億至30億美元)將建造一座年產能21吉瓦時的電池工廠,從而增強未來二手電動車的供應。電氣化聯盟計算得出,電動卡車的運作成本比柴油卡車低三分之二,這意味著完善的充電基礎設施將提升其在次市場的吸引力。天然氣和液化石油氣(LPG)車型目前仍屬於小眾市場,主要集中在燃料供應充足且有市政獎勵的地區。

區域分析

亞洲擁有全球最大的區域車隊規模,佔全球市場佔有率的47.35%,基礎設施計劃和電子商務的興起持續擴大卡車運輸需求。受嚴格的電氣化目標驅動,中國正在加速減少柴油車隊,並將高品質的歐V排放標準牽引車投放到鄰近的發展中市場。印度快速發展的數位零售業預計到2030會計年度商品總值將成長兩倍,該產業高度依賴中重型運輸,從而推動了設備的持續更新換代。

北美市場將與全球成長趨勢保持一致,預計到2030年複合年成長率將達到5.2%,這得益於完善的二手車市場網路和數據主導的估值工具能夠維持市場流動性。即將實施的重型皮卡和廂型車企業平均燃油經濟性標準(CAFE)可能會促使車隊選擇更新、更有效率的車型,這可能會為二手卡車市場增加更多新車型。

中東和非洲是成長最快的地區,預計到2030年複合年成長率將達到7.41%,這得益於數位競標的流動性,該地區能夠獲得價格合理的資產。南美洲也經歷了強勁成長,經濟穩定和財政獎勵推動了車隊現代化。巴西GDP的復甦帶動了卡車購買量的回升,而二手車稅收優惠政策也鼓勵自僱人士進行投資。跨境運輸便利化措施,例如TIR系統,可望為南美洲運輸商開闢新的出口通道,間接提升改裝二手牽引車的需求。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 印度和東協基礎設施建設熱潮主導了重型二手卡車的周轉率。

- 北美最後一公里電子商務的擴張正在推動對二手輕型卡車的需求。

- 歐洲原廠認證二手車專案提升可靠性與殘值

- 數位批發競標擴大了買家群體,尤其是在中東地區。

- 中國汽車電氣化目標推動柴油車產業結構調整

- 巴西二手商用車稅收優惠政策支持自營商

- 市場限制

- 更嚴格的歐VII/第三階段氮氧化物排放法規限制了歐盟老舊柴油引擎的進口。

- 中國新型低成本卡車降低了非洲二手車的溢價。

- 東協農村地區大型老舊資產的融資選擇有限

- 晶片短缺縮短了新車的前置作業時間,使得二手車不再那麼稀缺。

- 價值/供應鏈分析

- 監理與技術展望

- 排放氣體法規過渡時程

- 利用數位產權和遠端資訊處理技術的檢測技術

- 波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 按車輛類型

- 輕型卡車(3-5級)

- 中型卡車(6-7級)

- 大型卡車(8級以上,15噸以上)

- 按燃料類型

- 柴油引擎

- 汽油

- 天然氣和液化石油氣

- 混合動力和純電動

- 按年齡層

- 3歲以下

- 4至7歲

- 8至12歲

- 12歲以上

- 按汽車等級

- 三年級

- 四年級

- 五年級

- 六年級

- 七年級

- 八年級

- 按最終用途行業分類

- 建築和基礎設施

- 物流與電子商務配送

- 採礦和採石

- 農業/林業

- 地方政府與公共產業

- 其他

- 按銷售管道

- 獨立經銷商

- 特許經銷商

- 經原廠認證的二手車

- 在線P2P交易和競標

- 按地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 南美洲

- 巴西

- 阿根廷

- 智利

- 其他南美洲國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 亞太其他地區

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 卡達

- 南非

- 其他中東和非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Daimler AG(SelecTrucks)

- PACCAR Inc.

- Volvo Group

- Scania AB

- MAN Truck and Bus SE

- Navistar International Corp.

- Tata Motors

- Ashok Leyland

- Isuzu Motors

- Hino Motors

- Mitsubishi Fuso Truck and Bus Corp.

- Eicher Motors(VECV)

- Iveco Group NV

- Ford Otosan

- Sinotruk(CNHTC)

- FAW Jiefang

- Dongfeng Commercial Vehicles

- UD Trucks

- Penske Used Trucks

- Enterprise Truck Rental

- Ryder Used Vehicle Sales

- AmeriQuest Used Trucks

- Copart Inc.

- Ritchie Bros. Auctioneers

- Mascus

- TruckPlanet(IronPlanet)

- AutoNation USA

- OLX Autos Commercial

第7章 市場機會與未來展望

The used trucks market stands at USD 52.73 billion in 2025 and is forecast to reach USD 68.04 billion by 2030, advancing at a 5.23% CAGR despite uneven economic signals and tightening emissions rules.

Fleet managers concentrate on total cost of ownership, prompting robust demand for quality pre-owned Class 8 units. Heavy-duty models retain pricing power, yet light trucks are gaining traction as e-commerce accelerates last-mile activity. Diesel assets dominate the powertrain mix, but first-generation battery-electric trucks are beginning to influence residual-value expectations as charging networks widen. Digital auction platforms are broadening cross-border trade, lowering information frictions for small operators.

Global Used Truck Market Trends and Insights

Infrastructure-Led Construction Booms in India and ASEAN Stimulating Heavy Used-Truck Turnover

Construction megaprojects across India and Southeast Asia are accelerating fleet replacement cycles, prompting contractors to source 4-7-year-old heavy-duty units that balance reliability with manageable capital outlay. Open-deck capacity tightened in May 2025 as projects commenced, forcing shippers to secure equipment earlier in tender cycles. Even with a significant dip in 2024 light-vehicle sales, commercial demand remained firm because infrastructure spending shielded haulage volumes. Buyers increasingly request verified maintenance histories, and units with documented telematics data command premiums, reinforcing the importance of transparent vehicle provenance for the used trucks market.

E-commerce Last-Mile Expansion in North America Triggering Demand for Used Light-Duty Trucks

Rapid parcel-volume growth is pushing retailers and third-party logistics providers toward late-model Class 3-5 vehicles that fit tight urban corridors yet carry sizable payloads. The used trucks market benefits as operators sidestep higher new-vehicle prices while still meeting service-level agreements. Urban warehouse development along interstate rings supports shorter delivery radii. Environmental studies show that electric delivery vans lower carbon intensity, implying that lightly used electric models will secure strong residual values once they begin cycling out of primary fleets.

Tightening Euro-VII/Phase-3 NOx Rules Discouraging Older Diesel Imports in EU

Stricter tail-pipe limits split the European secondary market between compliant Euro VI tractors and legacy stock facing costly retrofits. The International Council on Clean Transportation confirms that access restrictions in growing low-emission zones penalize vehicles older than seven years. Exporters reroute pre-Euro VI units toward Central Asia and North Africa, temporarily inflating supply in those destinations while intensifying competition for low-mileage Euro VI assets within the EU.

Other drivers and restraints analyzed in the detailed report include:

- OEM Certified Pre-Owned Programs in Europe Enhancing Trust and Residual Values

- Digital Wholesale Auctions Broadening Buyer Pool, Especially in Middle East

- Low-Cost New Chinese Trucks Compressing Used Price Premiums in Africa

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Heavy-duty units commanded 43.05% of 2024 revenues as their pivotal role in long-haul freight and infrastructure haulage shielded demand during cyclical slowdowns. Light trucks, propelled by parcel logistics, are forecast to register a 7.69% CAGR to 2030, the quickest clip in the used trucks market. Their maneuverability suits congested inner-city routes, and fleet buyers value the lower acquisition cost relative to new vans.

Medium-duty trucks (Class 6-7) occupy a strategic middle ground, experiencing mixed market results. The segment witnessed a surge in inventory, while asking prices softened, signaling nuanced sub-segment conditions. Ongoing autonomous trials, such as an articulated dump truck showcased at CES 2025, foreshadow specialized heavy-duty applications that could redefine residual-value curves once these vehicles cycle into the used trucks industry.

Diesel assets held 92.25% of the 2024 pool, underlining the entrenched infrastructure, familiar maintenance regimes, and fuel-efficiency track record that fleet managers trust. The segment's staying power stems from diesel's proven reliability, fuel efficiency, and widespread service network, making it the default choice for secondary market buyers prioritizing operational certainty.

Hybrid and battery-electric entries, while small in absolute numbers, are projected to expand at a 22.55% CAGR through 2030. A USD 2-3 billion joint venture among Accelera by Cummins, Daimler Truck, and PACCAR will create a 21 GWh battery-cell plant, bolstering future used-EV supply. The Electrification Coalition calculates two-thirds lower running costs for electric trucks versus diesel, suggesting robust secondary-market appeal once adequate charging coverage emerges. Natural-gas and LPG variants remain niche, concentrated in regions with price-advantaged fuel supplies and municipal incentives.

The Used Truck Market Report is Segmented by Vehicle Type (Light Trucks, Medium-Duty Trucks, and More), Fuel Type (Diesel, Gasoline, and More), Age Bracket (Up To 3 Years, 4-7 Years, and More), Vehicle Class (Class 3 and More), End-Use Industry (Construction and Infrastructure and More), Sales Channel (Independent Dealer and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Geography Analysis

Asia retains the world's largest regional fleet base and accounts for 47.35% of the global market share, as infrastructure projects and e-commerce penetration continue to expand trucking demand. China's accelerated diesel-fleet liquidation, prompted by stringent electrification targets, releases high-quality Euro V tractors into neighboring developing markets. India's rapidly scaling digital retail sector, expected to triple in gross merchandise value by FY30, relies heavily on medium and heavy-duty haulage, reinforcing sustained equipment turnover.

North America mirrors global growth at a projected 5.2% CAGR to 2030 as sophisticated remarketing networks and data-driven valuation tools sustain liquidity. Forthcoming Corporate Average Fuel Economy standards for heavy-duty pickups and vans could nudge fleets toward newer, more efficient units, feeding additional late-model supply into the used trucks market.

The Middle East and Africa are the fastest-growing regions, posting a CAGR of 7.41% through 2030, capitalizing on digital-auction liquidity to source affordable assets, while Europe concentrates on tightening emissions compliance that skews demand toward newer Euro VI vehicles. South America is also growing significantly as economic stabilization and fiscal incentives spur fleet modernization. Brazil's GDP recovery supports renewed truck purchases, and tax breaks for used equipment encourage owner-operator investment. Cross-border transport facilitation measures such as the TIR system promise to open fresh export lanes for South American carriers, indirectly boosting demand for compliant used tractors.

- Daimler AG (SelecTrucks)

- PACCAR Inc.

- Volvo Group

- Scania AB

- MAN Truck and Bus SE

- Navistar International Corp.

- Tata Motors

- Ashok Leyland

- Isuzu Motors

- Hino Motors

- Mitsubishi Fuso Truck and Bus Corp.

- Eicher Motors (VECV)

- Iveco Group N.V.

- Ford Otosan

- Sinotruk (CNHTC)

- FAW Jiefang

- Dongfeng Commercial Vehicles

- UD Trucks

- Penske Used Trucks

- Enterprise Truck Rental

- Ryder Used Vehicle Sales

- AmeriQuest Used Trucks

- Copart Inc.

- Ritchie Bros. Auctioneers

- Mascus

- TruckPlanet (IronPlanet)

- AutoNation USA

- OLX Autos Commercial

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Infrastructure-Led Construction Booms in India and ASEAN Stimulating Heavy Used-Truck Turnover

- 4.2.2 E-commerce Last-Mile Expansion in North America Triggering Demand for Used Light-Duty Trucks

- 4.2.3 OEM Certified Pre-Owned Programs in Europe Enhancing Trust and Residual Values

- 4.2.4 Digital Wholesale Auctions Broadening Buyer Pool, Especially in Middle East

- 4.2.5 Fleet Electrification Targets in China Pushing Diesel Fleet Liquidation

- 4.2.6 Tax Incentives on Used Commercial Vehicles in Brazil Supporting Owner-Operators

- 4.3 Market Restraints

- 4.3.1 Tightening Euro-VII/Phase-3 NOx Rules Discouraging Older Diesel Imports in EU

- 4.3.2 Low-Cost New Chinese Trucks Compressing Used Price Premiums in Africa

- 4.3.3 Limited Financing Options for Aged Heavy-Duty Assets in ASEAN Rural Regions

- 4.3.4 Chip Shortages Easing New-Truck Lead Times, Reducing Used-Vehicle Scarcity

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory or Technological Outlook

- 4.5.1 Emission-Norm Transition Timelines

- 4.5.2 Digital Title and Telematics-Enabled Inspection Technologies

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts

- 5.1 By Vehicle Type

- 5.1.1 Light Trucks (Class 3-5)

- 5.1.2 Medium-Duty Trucks (Class 6-7)

- 5.1.3 Heavy-Duty Trucks (Class 8 and Over 15 t)

- 5.2 By Fuel Type

- 5.2.1 Diesel

- 5.2.2 Gasoline

- 5.2.3 Natural Gas and LPG

- 5.2.4 Hybrid and Battery-Electric

- 5.3 By Age Bracket

- 5.3.1 Up to 3 Years

- 5.3.2 4 to 7 Years

- 5.3.3 8 to 12 Years

- 5.3.4 Above 12 Years

- 5.4 By Vehicle Class

- 5.4.1 Class 3

- 5.4.2 Class 4

- 5.4.3 Class 5

- 5.4.4 Class 6

- 5.4.5 Class 7

- 5.4.6 Class 8

- 5.5 By End-use Industry

- 5.5.1 Construction and Infrastructure

- 5.5.2 Logistics and E-commerce Delivery

- 5.5.3 Mining and Quarrying

- 5.5.4 Agriculture and Forestry

- 5.5.5 Municipal and Utilities

- 5.5.6 Others

- 5.6 By Sales Channel

- 5.6.1 Independent Dealer

- 5.6.2 Franchised Dealer

- 5.6.3 OEM-Backed Certified Pre-Owned

- 5.6.4 Online Peer-to-Peer and Auction

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Rest of North America

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Chile

- 5.7.2.4 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 Germany

- 5.7.3.2 United Kingdom

- 5.7.3.3 France

- 5.7.3.4 Italy

- 5.7.3.5 Spain

- 5.7.3.6 Russia

- 5.7.3.7 Rest of Europe

- 5.7.4 Asia-Pacific

- 5.7.4.1 China

- 5.7.4.2 India

- 5.7.4.3 Japan

- 5.7.4.4 South Korea

- 5.7.4.5 Rest of Asia-Pacific

- 5.7.5 Middle East

- 5.7.5.1 United Arab Emirates

- 5.7.5.2 Saudi Arabia

- 5.7.5.3 Qatar

- 5.7.5.4 South Africa

- 5.7.5.5 Rest of Middle East and Africa

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Daimler AG (SelecTrucks)

- 6.4.2 PACCAR Inc.

- 6.4.3 Volvo Group

- 6.4.4 Scania AB

- 6.4.5 MAN Truck and Bus SE

- 6.4.6 Navistar International Corp.

- 6.4.7 Tata Motors

- 6.4.8 Ashok Leyland

- 6.4.9 Isuzu Motors

- 6.4.10 Hino Motors

- 6.4.11 Mitsubishi Fuso Truck and Bus Corp.

- 6.4.12 Eicher Motors (VECV)

- 6.4.13 Iveco Group N.V.

- 6.4.14 Ford Otosan

- 6.4.15 Sinotruk (CNHTC)

- 6.4.16 FAW Jiefang

- 6.4.17 Dongfeng Commercial Vehicles

- 6.4.18 UD Trucks

- 6.4.19 Penske Used Trucks

- 6.4.20 Enterprise Truck Rental

- 6.4.21 Ryder Used Vehicle Sales

- 6.4.22 AmeriQuest Used Trucks

- 6.4.23 Copart Inc.

- 6.4.24 Ritchie Bros. Auctioneers

- 6.4.25 Mascus

- 6.4.26 TruckPlanet (IronPlanet)

- 6.4.27 AutoNation USA

- 6.4.28 OLX Autos Commercial

7 Market Opportunities and Future Outlook

- 7.1 Digital Inspection-as-a-Service for Cross-Border Buyers

- 7.2 Subscription and Pay-per-mile Financing Models for SMEs

- 7.3 Electrified Truck After-market and Second-life Batteries