|

市場調查報告書

商品編碼

1892755

二手車融資市場機會、成長促進因素、產業趨勢分析及預測(2026-2035年)Used Car Financing Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

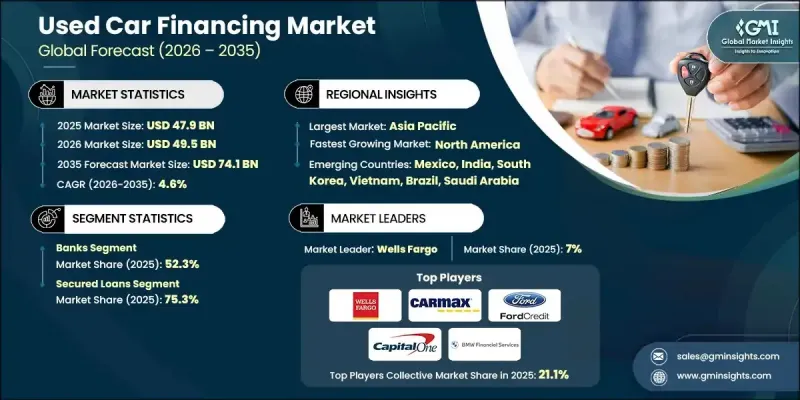

2025年全球二手車融資市場價值為479億美元,預計2035年將以4.6%的複合年成長率成長至741億美元。

可支配收入的成長推動了汽車需求,但新車的高昂價格仍然令購車者猶豫不決。二手車銷售已成為一種切實可行的替代方案,使消費者能夠以更低的價格購買汽車。包括分期付款在內的融資方案正在彌合這一差距,使汽車擁有變得更加容易和方便。貸款機構提供靈活的利率以適應不同的貸款期限,據行業協會稱,目前12-36個月的平均利率約為4.79%,37-60個月的平均利率約為5.29%。亞太地區約佔全球市場佔有率的一半,這主要得益於中國的經濟規模、印度快速的汽車普及以及有組織的零售網路的擴張。北美和歐洲市場雖然仍較為成熟,但透過數位化融資平台、創新的保險解決方案以及針對電動車的專項融資,仍蘊藏著巨大的發展機遇,從而支持著全球市場的穩步擴張。

| 市場範圍 | |

|---|---|

| 起始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 479億美元 |

| 預測值 | 741億美元 |

| 複合年成長率 | 4.6% |

2024年,銀行類股佔據52.3%的市佔率。其主導地位源自於低成本的存款能力、廣泛的網點和線上管道,以及在低風險貸款方面的專業知識。借款人通常可獲得80%至90%的貸款價值比,期限為36至72個月。抵押貸款佔市場收入的75.3%,因為有抵押貸款既能降低貸款人的風險,又能為借款人提供優惠的利率和更長的還款期限。

到2025年,擔保貸款市場將佔據75.3%的佔有率。擔保貸款之所以備受青睞,是因為車輛本身即可作為抵押品,從而降低了貸款機構的風險。信用良好的借款人可以享受更長的還款期限和更低的利率。從貸款機構的角度來看,這些貸款提供了保障,因為在必要時可以選擇收回抵押物;而藉款人則可以獲得優惠的融資方案。這種風險管理結構使擔保貸款成為二手車融資市場的基石。

預計2025年,美國二手車融資市場規模將達83億美元。新車價格高漲使得二手車成為許多人的首選,從而維持了融資需求。銀行、信用社和附屬金融公司積極為各類信用等級的消費者提供服務,包括優質、次優和次級信用借款人。

目錄

第1章:方法論

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 利潤率

- 成本結構

- 每個階段的價值增加

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 成長促進因素

- 二手車價格上漲擴大了潛在市場

- 數位化預審可減少摩擦並提高轉換率

- 延長貸款期限,提高貸款負擔能力及取得途徑。

- 嵌入式金融合作關係擴大分銷

- 產業陷阱與挑戰

- 利率上升導致借貸成本增加。

- 汽車價格正常化可能導致利潤空間壓縮

- 市場機遇

- 嵌入式金融夥伴關係

- 電動汽車二手車融資這一新興細分市場

- 小型企業和車隊融資成長

- 信用合作社-銀行合作模式

- 成長促進因素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 技術與創新格局

- 當前技術趨勢

- 新興技術

- 技術路線圖與演進

- 技術採納生命週期分析

- 價格趨勢

- 按地區

- 依產品

- 專利分析

- 投資與融資分析

- 汽車金融科技領域的創投

- 私募股權在次級貸款領域的活動

- 銀行對數位化能力的投資

- 證券化市場趨勢

- 定價與利率分析

- 利率基準

- 歷史利率趨勢

- 經銷商加價經濟學

- 附加產品定價

- 費用結構分析

- 信用分析總成本

- 宏觀經濟和市場週期敏感性

- 影響二手車融資需求的宏觀經濟因素

- 汽車市場動態

- 信貸週期動態

- 經濟衰退和經濟低迷敏感性

- 擴張與復甦動態

- 車輛擁有率

- 消費者信用評分分佈分析

- 信用評分隨時間變化的趨勢

- 按人口統計資料分類的信用評分分佈

- 信用評分對貸款期限的影響

- 信用評分提升與修復

- 客戶行為分析

- 車輛購買決策過程

- 融資管道選擇

- 貸款期限選擇行為

- 首付行為

- 附加產品購買行為

- 支付行為與績效

- 風險評估與緩解框架

- 信用風險

- 抵押品風險

- 營運風險

- 合規與監理風險

- 市場和經濟風險

- 永續發展與ESG趨勢

- 環境因素

- 社會因素

- 治理方面的考慮

- 將ESG因素納入貸款實踐

- 投資者和貸款機構的ESG承諾

- 未來展望與機遇

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新產品發布

- 擴張計劃和資金

- 供應商選擇標準

第5章:市場估價與預測:依貸款機構分類,2022-2035年

- 銀行

- 私人的

- 民眾

- 非銀行金融公司

- OEM專屬融資公司

- 其他

第6章:市場估計與預測:依貸款類型分類,2022-2035年

- 擔保貸款

- 無擔保貸款

- 租賃融資

第7章:市場估價與預測:依車輛類別分類,2022-2035年

- 經濟型轎車

- 中檔

- 豪華轎車

第8章:市場估算與預測:依車輛類型分類,2022-2035年

- 轎車

- 掀背車

- SUV

第9章:市場估計與預測:依貸款期限分類,2022-2035年

- 短期(12-36個月)

- 中期(37-60個月)

- 長期(超過 60 個月)

第10章:市場估價與預測:依車齡分類,2022-2035年

- 較新的(不超過3年)

- 年齡較大(3歲以上)

第11章:市場估計與預測:依用途分類,2022-2035年

- 個人/消費者

- 企業/商業

第12章:市場估算與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐

- 比荷盧經濟聯盟

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳新銀行

- 新加坡

- 馬來西亞

- 印尼

- 越南

- 泰國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 哥倫比亞

- MEA

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第13章:公司簡介

- 全球公司

- Ally Financial

- Capital One Financial Corporation

- JPMorgan Chase

- Bank of America

- Wells Fargo

- Santander Consumer

- TD Auto Finance

- GM Financial

- Ford Motor Credit Company

- Toyota Financial Services

- Honda Financial Services

- Volkswagen Credit

- BMW Financial Services

- Mercedes-Benz Financial Services

- 區域公司

- Navy Federal Credit Union

- First Tech Federal Credit Union

- Truist Financial

- KeyBank

- Huntington National Bank

- PenFed Credit Union

- 新興公司

- Carvana

- LendingClub

- Upstart Holdings

- AutoFi

- Exeter Finance

The Global Used Car Financing Market was valued at USD 47.9 billion in 2025 and is estimated to grow at a CAGR of 4.6% to reach USD 74.1 billion by 2035.

Rising disposable income has fueled automotive demand, yet the high cost of new vehicles continues to make buyers hesitant. Used car sales have emerged as a practical alternative, enabling consumers to access vehicles at lower price points. Financing solutions, including EMIs, are bridging this gap, making car ownership more attainable and convenient. Lenders are offering flexible interest rates to accommodate varying loan tenures, with rates currently averaging around 4.79% for 12-36 months and 5.29% for 37-60 months, according to industry associations. The Asia-Pacific region accounts for roughly half of the market, driven by China's scale and India's rapid motorization alongside the growth of organized retail networks. North America and Europe remain mature markets but continue to present opportunities through digital financing platforms, innovative insurance solutions, and specialized financing for electric vehicles, supporting steady market expansion globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $47.9 Billion |

| Forecast Value | $74.1 Billion |

| CAGR | 4.6% |

The banks segment held a 52.3% share in 2024. Their dominance stems from low-cost deposit capabilities, wide branch and online networks, and expertise in low-risk lending. Borrowers typically secure 80-90% loan-to-value ratios over 36-72 months. Secured loans accounted for 75.3% of the market revenue, as collateralized loans reduce lender risk while offering borrowers favorable rates and longer tenures.

The secured loans segment held a 75.3% share in 2025. Secured loans are highly preferred because the vehicle itself serves as collateral, reducing risk for lenders. Borrowers with strong credit profiles can benefit from longer repayment terms and lower interest rates. From the lender's perspective, these loans provide assurance through the option to repossess the asset if needed, while borrowers gain access to favorable financing solutions. This risk-managed structure makes secured loans the cornerstone of the used car financing market.

U.S. Used Car Financing Market reached USD 8.3 billion in 2025. High new car prices have made used vehicles the preferred choice for many, sustaining demand for financing. Banks, credit unions, and captive finance companies actively serve consumers across credit categories, including prime, near-prime, and subprime borrowers.

Key players in the Used Car Financing Market include CarMax Auto Finance, Capital One Auto Finance, Ally Financial, Ford Motor Credit Company, Carvana, BMW Financial Services, JPMorgan Chase, GM Financial, Wells Fargo, and Toyota Financial Services. Companies in the Used Car Financing Market are leveraging flexible financing structures, including variable interest rates and customizable EMI plans, to attract a broader customer base. Many are investing in digital platforms and mobile applications to simplify loan applications, approvals, and repayments, increasing convenience for borrowers. Partnerships with dealerships, online marketplaces, and financial institutions allow lenders to expand distribution channels and tap into new regional markets. Risk assessment and credit scoring technologies are being enhanced to accommodate prime, near-prime, and subprime borrowers while minimizing defaults. Additionally, marketing initiatives emphasize affordability, convenience, and vehicle accessibility, strengthening brand presence.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Lender

- 2.2.3 Loan Type

- 2.2.4 Vehicle Class

- 2.2.5 Vehicle Type

- 2.2.6 Loan Duration

- 2.2.7 Vehicle Age

- 2.2.8 User

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising used vehicle prices expanding addressable market

- 3.2.1.2 Digital pre-qualification reducing friction & improving conversion

- 3.2.1.3 Extended loan terms improving affordability & access

- 3.2.1.4 Embedded finance partnerships expanding distribution

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Rising interest rates increasing borrowing costs

- 3.2.2.2 Vehicle price normalization risk compressing margins

- 3.2.3 Market opportunities

- 3.2.3.1 Embedded finance partnerships

- 3.2.3.2 EV used car financing emerging niche

- 3.2.3.3 Small business & fleet financing growth

- 3.2.3.4 Credit union-bank partnership models

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.7.3 Technology roadmaps & evolution

- 3.7.4 Technology adoption lifecycle analysis

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Patent analysis

- 3.10 Investment & Funding Analysis

- 3.10.1 Venture capital in auto fintech

- 3.10.2 Private equity activity in subprime lending

- 3.10.3 Bank investment in digital capabilities

- 3.10.4 Securitization market trends

- 3.11 Pricing & interest rate analysis

- 3.11.1 Interest rate benchmarking

- 3.11.2 Historical interest rate trends

- 3.11.3 Dealer markup economics

- 3.11.4 Add-on product pricing

- 3.11.5 Fee structure analysis

- 3.11.6 Total cost of credit analysis

- 3.12 Macroeconomic & market cycle sensitivity

- 3.12.1 Macroeconomic drivers of used car financing demand

- 3.12.2 Vehicle market dynamics

- 3.12.3 Credit cycle dynamics

- 3.12.4 Recession & economic downturn sensitivity

- 3.12.5 Expansion & recovery dynamics

- 3.12.6 Vehicle ownership rates

- 3.13 Consumer credit score distribution analysis

- 3.13.1 Credit score trends over time

- 3.13.2 Credit score distribution by demographics

- 3.13.3 Credit score impact on loan terms

- 3.13.4 Credit score improvement & rehabilitation

- 3.14 Customer behavior analysis

- 3.14.1 Vehicle purchase decision process

- 3.14.2 Financing channel selection

- 3.14.3 Loan term selection behavior

- 3.14.4 Down payment behavior

- 3.14.5 Add-on product purchase behavior

- 3.14.6 Payment behavior & performance

- 3.15 Risk assessment & mitigation framework

- 3.15.1 Credit risk

- 3.15.2 Collateral risk

- 3.15.3 Operational risk

- 3.15.4 Compliance & regulatory risk

- 3.15.5 Market & economic risk

- 3.16 Sustainability & ESG trends

- 3.16.1 Environmental considerations

- 3.16.2 Social considerations

- 3.16.3 Governance considerations

- 3.16.4 ESG integration in lending practices

- 3.16.5 Investor & lender ESG commitments

- 3.17 Future outlook & opportunities

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

- 4.7 Vendor selection criteria

Chapter 5 Market Estimates & Forecast, By Lender, 2022 - 2035 ($Mn)

- 5.1 Key trends

- 5.2 Banks

- 5.2.1 Private

- 5.2.2 Public

- 5.3 NBFCs

- 5.4 OEM captive finance companies

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Loan Type, 2022 - 2035 ($Mn)

- 6.1 Key trends

- 6.2 Secured Loans

- 6.3 Unsecured Loans

- 6.4 Lease Financing

Chapter 7 Market Estimates & Forecast, By Vehicle Class, 2022 - 2035 ($Mn)

- 7.1 Key trends

- 7.2 Economy Cars

- 7.3 Mid-range

- 7.4 Luxury Cars

Chapter 8 Market Estimates & Forecast, By Vehicle Type, 2022 - 2035 ($Mn)

- 8.1 Key trends

- 8.2 Sedan

- 8.3 Hatchbacks

- 8.4 SUVs

Chapter 9 Market Estimates & Forecast, By Loan Duration, 2022 - 2035 ($Mn)

- 9.1 Key trends

- 9.2 Short-term (12-36 months)

- 9.3 Medium-term (37-60 months)

- 9.4 Long-term (Above 60 months)

Chapter 10 Market Estimates & Forecast, By Vehicle Age, 2022 - 2035 ($Mn)

- 10.1 Key trends

- 10.2 Newer (Upto 3 years)

- 10.3 Older (Above 3 years)

Chapter 11 Market Estimates & Forecast, By Use, 2022 - 2035 ($Mn)

- 11.1 Key trends

- 11.2 Individuals/consumers

- 11.3 Businesses/commercial

Chapter 12 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 US

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 UK

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.3.6 Russia

- 12.3.7 Nordics

- 12.3.8 Benelux

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 South Korea

- 12.4.5 ANZ

- 12.4.6 Singapore

- 12.4.7 Malaysia

- 12.4.8 Indonesia

- 12.4.9 Vietnam

- 12.4.10 Thailand

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.5.4 Colombia

- 12.6 MEA

- 12.6.1 South Africa

- 12.6.2 Saudi Arabia

- 12.6.3 UAE

Chapter 13 Company Profiles

- 13.1 Global companies

- 13.1.1 Ally Financial

- 13.1.2 Capital One Financial Corporation

- 13.1.3 JPMorgan Chase

- 13.1.4 Bank of America

- 13.1.5 Wells Fargo

- 13.1.6 Santander Consumer

- 13.1.7 TD Auto Finance

- 13.1.8 GM Financial

- 13.1.9 Ford Motor Credit Company

- 13.1.10 Toyota Financial Services

- 13.1.11 Honda Financial Services

- 13.1.12 Volkswagen Credit

- 13.1.13 BMW Financial Services

- 13.1.14 Mercedes-Benz Financial Services

- 13.2 Regional companies

- 13.2.1 Navy Federal Credit Union

- 13.2.2 First Tech Federal Credit Union

- 13.2.3 Truist Financial

- 13.2.4 KeyBank

- 13.2.5 Huntington National Bank

- 13.2.6 PenFed Credit Union

- 13.3 Emerging companies

- 13.3.1 Carvana

- 13.3.2 LendingClub

- 13.3.3 Upstart Holdings

- 13.3.4 AutoFi

- 13.3.5 Exeter Finance

二手半拖車市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、流程及最終用戶二手

二手半拖車市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、流程及最終用戶二手 東南亞二手車市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)越南二手車市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)非洲二手車市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)

東南亞二手車市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)越南二手車市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)非洲二手車市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年) 二手拖車市場-全球產業規模、佔有率、趨勢、機會和預測:按車輛類型、動力類型、銷售管道、地區和競爭格局分類,2021-2031年二手車市場 - 全球產業規模、佔有率、趨勢、競爭格局、機會、預測(按車輛類型、動力類型、銷售管道、最終用途、地區和競爭情況分類),2021-2031年印尼二手車市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印尼二手車融資:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)德國二手車市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)歐洲二手車市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

二手拖車市場-全球產業規模、佔有率、趨勢、機會和預測:按車輛類型、動力類型、銷售管道、地區和競爭格局分類,2021-2031年二手車市場 - 全球產業規模、佔有率、趨勢、競爭格局、機會、預測(按車輛類型、動力類型、銷售管道、最終用途、地區和競爭情況分類),2021-2031年印尼二手車市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印尼二手車融資:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)德國二手車市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)歐洲二手車市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)