|

市場調查報告書

商品編碼

1940563

歐洲自助倉儲:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Europe Self-storage - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

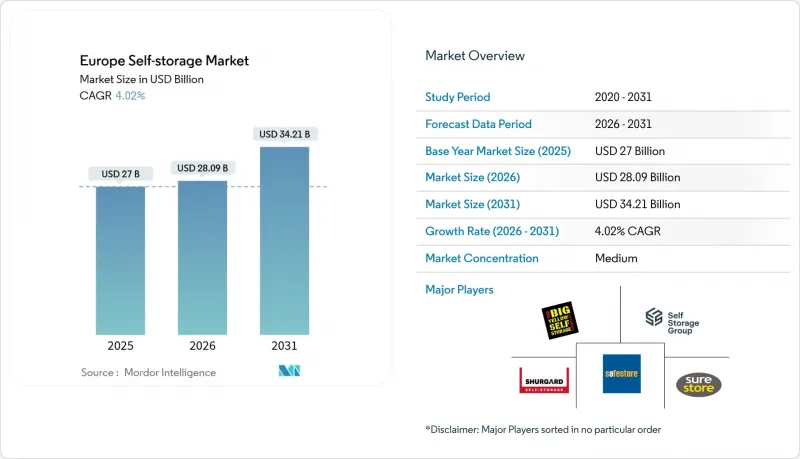

2025年歐洲自助倉儲市場價值270億美元,預計2031年將達到342.1億美元,高於2026年的280.9億美元。

預計在預測期(2026-2031 年)內,複合年成長率將達到 4.02%。

持續的都市區成長、住宅流動性的提高以及將倉儲資產視為基礎設施而非邊緣房地產投資的機構投資者的湧入,都支撐著這一擴張趨勢。倫敦、巴黎和柏林等主要城市的城市密度不斷增加,加上人口老化導致住房規模縮小,使得倉儲運轉率率和租金水準在各個經濟週期中都保持穩定。中小電商企業擴大採用微型倉庫策略,而學生和外籍人士的流動也帶來了可預測的季節性需求。氣候政策驅動的維修雖然成本高昂,但卻創造了一個高階市場,提高了能源效率,並提升了符合標準的設施的獲利能力。

歐洲自助倉儲市場趨勢與洞察

城市高密度化和微型居住

地價上漲導致都市區平均居住面積縮水,迫使他們利用本地倉儲設施作為戶外「房間」。三年來,英國新增了100多家倉儲設施,每年為用戶帶來10億英鎊的收入,用於存放家具和季節性物品。混合租賃模式和全天候數位化服務意味著這項服務正日益融入城市生活。

因老化而從大型住宅搬離,縮小居住面積

隨著德國、義大利和英國的老年住宅搬進小規模的住宅,對臨時存放傳家寶和大型家具的需求日益成長。經合組織預測,到2050年,七國集團居住者中將有25%超過65歲,這將形成一個永續的、以需求為導向的基本客群。

嚴格的消防安全標準

北歐法規要求採用先進的消防系統和檢驗的風險評估,這將使維修預算增加高達 25%,並減緩市場准入。

細分市場分析

截至2025年,個人用戶將佔歐洲自助倉儲市場收入的69.35%。家庭搬遷、微型居住和退休縮減住房規模等因素將確保長期合約的簽訂,即使在宏觀經濟衝擊下也能維持運轉率的穩定。企業用戶群雖然規模較小,但正以每年7.42%的速度成長,這主要得益於中小企業對計量型倉儲空間的日益成長的需求。營運商目前正在建立雙品牌策略,例如針對個人用戶的生活方式通訊和針對企業的承包物流服務,以有效實現兩個細分市場的收入成長。

歐洲自助倉儲市場規模(主要指個人租賃市場)預計將在2031年之前保持主導地位,這主要得益於簡化短期預訂流程的數位化預訂平台的普及。同時,隨著電子商務在區域城市的滲透率不斷提高,宅配代收、貨架安裝和保險等交叉銷售服務正在提升企業客戶的平均收入。

由於前期投入成本較低,到2025年,非空調自助倉儲單位將佔歐洲自助倉儲市場59.35%的佔有率。然而,配備感測器、空調和嚴格門禁系統的空調自助倉儲單元,由於其租金比標準間高出25%至40%,將以8.82%的複合年成長率成長,從而帶來更高的利潤率。

日益嚴格的監管正在加速這一轉變,而達到E級標準的設施可以透過更高的租金和更低的客戶流失率來收回維修成本。預計到2031年,歐洲空調市場規模將超過142億美元,這將支撐對電子產品、藝術品和檔案等專業保險產品的需求。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 歐洲主要城市的城市壓縮與微型生活趨勢

- 德國、義大利和英國的居民因房屋老化而搬離大型住宅。

- 中小企業在電子商務領域的快速成長推動了對靈活的小規模倉庫的需求。

- 申根區內學生和外籍人士流動迅速增加

- 混合辦公模式的普及導致了在家工作環境的零碎化。

- 機構投資者對另類房地產收入的興趣

- 市場限制

- 北歐國家嚴格的消防安全法規限制了設施改造。

- 歷史城區中心缺乏適當的工業用地

- 法國和西班牙的通膨掛鉤租金指數上限

- 日益嚴格的能源效率法規增加了維修成本。

- 消費者分析

- 監理展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 投資分析

第5章 市場規模與成長預測

- 依使用者類型

- 個人

- 商業

- 依儲存類型

- 空調管理

- 非空調管理

- 按空間大小

- 90平方英尺或更少

- 91-150平方英尺

- 151-300平方英尺

- 超過300平方英尺

- 透過使用

- 家居用品

- 電子商務小包裹配送中心

- 文件和檔案存儲

- 車輛存放

- 按國家/地區

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Shurgard Self Storage SA

- Safestore Holdings PLC

- Big Yellow Group PLC

- Self Storage Group ASA

- Lok'nStore Group PLC

- SureStore Ltd

- Access Self Storage Ltd

- Lagerboks

- Nettolager

- Pelican Self Storage

- 24Storage AB

- Casaforte(SMC Self-Storage Management)

- W Wiedmer AG

- MyPlace SelfStorage GmbH

- BlueSpace Self-Storage SL

- Space Station Ltd

第7章 市場機會與未來展望

The Europe self-storage market was valued at USD 27 billion in 2025 and estimated to grow from USD 28.09 billion in 2026 to reach USD 34.21 billion by 2031, at a CAGR of 4.02% during the forecast period (2026-2031).

Expansion rests on steady urban population growth, rising residential mobility, and institutional capital inflows that treat storage assets as infrastructure rather than peripheral real-estate plays. Urban compression in London, Paris, Berlin, and similar Tier-1 cities, coupled with ageing populations downsizing, keeps occupancy and rental levels resilient across economic cycles. Small and medium e-commerce businesses increasingly adopt micro-warehousing strategies, while student and expatriate mobility supplies predictable seasonal demand. Climate-policy-driven retrofits, although costly, improve energy efficiency and create a premium segment that lifts yields for compliant facilities

Europe Self-storage Market Trends and Insights

Urban compression and micro-living

Intensifying land prices have shrunk average city dwellings, prompting residents to treat local storage facilities as an external "room." Over 100 new complexes opened in the UK in three years, earning operators GBP 1 billion annually as renters off-load furniture and seasonal goods. Hybrid leases and 24/7 digital access further embed the service into day-to-day urban living.

Ageing population downsizing from larger homes

Older homeowners in Germany, Italy, and the UK are shifting to smaller dwellings, creating interim storage demand for heirlooms and bulky furniture. OECD projections show the 65+ cohort reaching 25% of G7 city dwellers by 2050, locking in a durable, needs-based customer base

Stringent fire-safety codes

Nordic rules require advanced suppression systems and verified risk assessments, adding up to 25% to conversion budgets and delaying market entry

Other drivers and restraints analyzed in the detailed report include:

- E-commerce SMB boom driving flexible micro-warehousing

- Student & expat mobility

- Heightened energy-efficiency mandates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Personal users accounted for 69.35% of Europe self-storage market revenue in 2025. Household moves, micro-living, and retirement downsizing secure long-tenure contracts that stabilise occupancy during macro shocks. The business cohort, while smaller, is expanding at 7.42% annually as SMEs embrace pay-as-you-go inventory space. Operators now tailor dual-branding strategies-lifestyle messaging for individuals and turnkey logistics features for corporations-to monetise both streams effectively.

The Europe self-storage market size attached to personal tenancy is forecast to maintain a dominant share through 2031, helped by digital reservation platforms that simplify short-cycle booking. Meanwhile, cross-selling services such as courier pick-up, racking, and insurance lift average revenue per business customer as e-commerce penetration deepens in peripheral cities.

Non-climate units delivered 59.35% of Europe self-storage market share in 2025 thanks to lower fit-out costs. Yet climate-controlled stock, growing at 8.82% CAGR, underpins margin expansion because sensors, HVAC, and stricter access controls command fees 25-40% above standard rooms.

Regulatory upgrades accelerate the pivot: facilities that already meet class E standards recoup retrofit spending via higher rents and lower churn. The Europe self-storage market size for climate-controlled units is on track to surpass USD 14.2 billion by 2031, supporting specialised insurance offerings for electronics, art, and archival documents.

Europe Self Storage Market Report is Segmented by User Type (Personal and Business), Storage Type (Climate-Controlled, Non-Climate-Controlled), Space Size (Up To 90 Sq Ft, 91-150 Sq Ft, and More), Application (Household Goods, E-Commerce Micro-Fulfilment, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Shurgard Self Storage SA

- Safestore Holdings PLC

- Big Yellow Group PLC

- Self Storage Group ASA

- Lok'nStore Group PLC

- SureStore Ltd

- Access Self Storage Ltd

- Lagerboks

- Nettolager

- Pelican Self Storage

- 24Storage AB

- Casaforte (SMC Self-Storage Management)

- W Wiedmer AG

- MyPlace SelfStorage GmbH

- BlueSpace Self-Storage S.L.

- Space Station Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Urban Compression and Micro-Living Trends in Tier-1 European Cities

- 4.2.2 Aging Population Downsizing from Larger Homes in Germany, Italy and UK'

- 4.2.3 E-commerce SMB Boom Driving Need for Flexible Micro-Warehousing

- 4.2.4 Surging Student & Expat Mobility Within the Schengen Region

- 4.2.5 Rise of Hybrid Work Creating Home Office Clutter

- 4.2.6 Institutional Investor Appetite for Alternative Real-Estate Yields

- 4.3 Market Restraints

- 4.3.1 Stringent Fire-Safety Codes Limiting Facility Conversions in Nordics

- 4.3.2 Scarcity of Suitable Zoned Industrial Stock in Historic City Centres

- 4.3.3 Inflation-Linked Rental Index Caps in France and Spain

- 4.3.4 Heightened Energy-Efficiency Mandates Increasing Retrofit Costs

- 4.4 Consumer Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By User Type

- 5.1.1 Personal

- 5.1.2 Business

- 5.2 By Storage Type

- 5.2.1 Climate-Controlled

- 5.2.2 Non-Climate-Controlled

- 5.3 By Space Size

- 5.3.1 Up to 90 sq ft

- 5.3.2 91-150 sq ft

- 5.3.3 151-300 sq ft

- 5.3.4 Above 300 sq ft

- 5.4 By Application

- 5.4.1 Household Goods

- 5.4.2 E-commerce Micro-Fulfilment

- 5.4.3 Document & Archive Storage

- 5.4.4 Vehicle Storage

- 5.5 By Country

- 5.5.1 Germany

- 5.5.2 United Kingdom

- 5.5.3 France

- 5.5.4 Italy

- 5.5.5 Spain

- 5.5.6 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Shurgard Self Storage SA

- 6.4.2 Safestore Holdings PLC

- 6.4.3 Big Yellow Group PLC

- 6.4.4 Self Storage Group ASA

- 6.4.5 Lok'nStore Group PLC

- 6.4.6 SureStore Ltd

- 6.4.7 Access Self Storage Ltd

- 6.4.8 Lagerboks

- 6.4.9 Nettolager

- 6.4.10 Pelican Self Storage

- 6.4.11 24Storage AB

- 6.4.12 Casaforte (SMC Self-Storage Management)

- 6.4.13 W Wiedmer AG

- 6.4.14 MyPlace SelfStorage GmbH

- 6.4.15 BlueSpace Self-Storage S.L.

- 6.4.16 Space Station Ltd

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

德國自助倉儲市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

德國自助倉儲市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 自助倉儲市場-全球產業規模、佔有率、趨勢、機會、預測:按應用、最終用戶、地區和競爭格局分類,2021-2031年

自助倉儲市場-全球產業規模、佔有率、趨勢、機會、預測:按應用、最終用戶、地區和競爭格局分類,2021-2031年 日本自助倉儲市場報告(按倉儲單元尺寸(小型倉儲單元、中型倉儲單元、大型倉儲單元)、最終用途(個人、商業)和地區分類,2026-2034年)

日本自助倉儲市場報告(按倉儲單元尺寸(小型倉儲單元、中型倉儲單元、大型倉儲單元)、最終用途(個人、商業)和地區分類,2026-2034年) 自助倉儲市場規模、佔有率、按類型、單位規模、最終用途和地區分類的成長分析 - 產業預測,2025 年至 2032 年

自助倉儲市場規模、佔有率、按類型、單位規模、最終用途和地區分類的成長分析 - 產業預測,2025 年至 2032 年 2025年全球自助倉儲市場報告美國自助倉儲:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)2025 年至 2033 年自助儲存市場規模、佔有率、趨勢及預測(按儲存單元大小、最終用途和地區)亞太地區自助倉儲:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

2025年全球自助倉儲市場報告美國自助倉儲:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)2025 年至 2033 年自助儲存市場規模、佔有率、趨勢及預測(按儲存單元大小、最終用途和地區)亞太地區自助倉儲:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 自助倉儲市場報告:2031 年趨勢、預測與競爭分析新加坡自助倉儲:市場佔有率分析、產業趨勢和成長預測(2025-2030 年)

自助倉儲市場報告:2031 年趨勢、預測與競爭分析新加坡自助倉儲:市場佔有率分析、產業趨勢和成長預測(2025-2030 年)