|

市場調查報告書

商品編碼

1851124

美國自助倉儲:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)United States Self-Storage - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

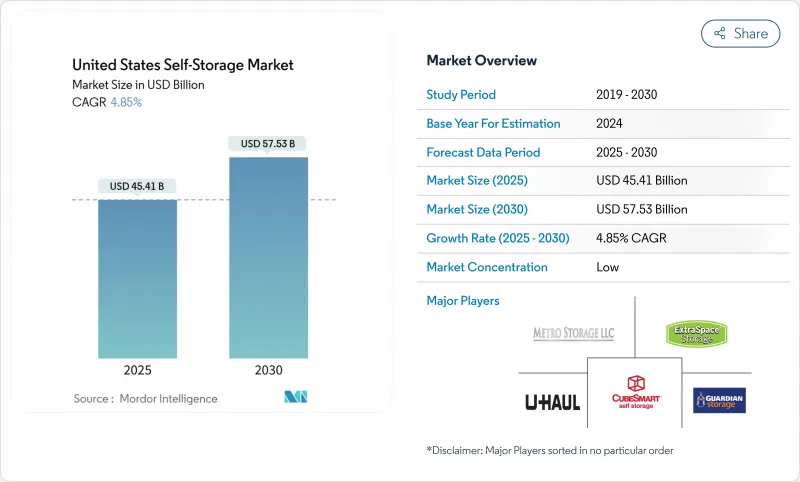

美國自助倉儲市場預計到 2025 年將達到 454.1 億美元,到 2030 年將達到 575.3 億美元,年複合成長率為 4.85%。

都市區成長、居住空間日益萎縮以及不斷發展的電子商務生態系統對微型履約以及數位化預訂平台的興起,增強了房地產市場的結構韌性和定價能力。隨著上市房地產投資信託基金(REITs)不斷深化市場滲透並規範技術應用,機構投資者持續重塑著市場競爭動態;同時,在人口密集地區,分區限制和建築成本上漲限制了新增供應。

美國自助倉儲市場趨勢與洞察

都市化加速和住房面積縮小

房屋供應缺口達385萬套,而都會區人口成長率僅1.1%,加劇了空間緊張的局面,促使居住者轉向外部儲存解決方案。相對於人口成長而言,住房供應有限,導致位於市中心的儲存設施租金居高不下,確保了其利用率在傳統搬遷高峰期之外也能持續成長。限制新建房屋的城市規劃無意中增加了長期儲存需求,並凸顯了高密度儲存設施對營運商的重要性。

電子商務對微型倉配的需求日益成長

電子商務營運商正日益將美國自助倉儲市場打造為經濟實惠的城市微型倉庫網路,推動該業務部門以5.8%的複合年成長率成長。基於貨櫃的倉儲設施為季節性庫存提供了靈活的存放空間,並能快速進入市場,滿足了擁擠都市區當日送達的需求。與純粹的個人使用模式相比,採用便於物流配送佈局和延長開放時間的倉儲設施能夠帶來更高的每平方英尺收益。

城市中心的分區與土地利用法規

像帕斯科縣這樣的城市製定了嚴格的設計和景觀標準,迫使開發人員轉向監管較為寬鬆的郊區。核准延誤增加了運輸成本,抑制了需求最高地區的供應成長,提高了現有設施的運轉率,但也降低了擴張潛力。

細分市場分析

2024年,個人用戶將占美國自助倉儲市場的73%,為市場提供可靠的收入來源,滿足人們應對人生大事的儲存需求。然而,隨著線上零售商利用都市區倉儲單位縮短配送距離,企業用戶正以5.8%的複合年成長率快速成長。預計到2030年,美國自助倉儲市場中由企業租戶佔據的佔有率將持續成長,這預示著市場將持續向商業用途轉變。

當日配送範圍的擴大,使得靠近消費者的庫存節點的重要性日益凸顯。那些能夠設計靈活的單元組合、整合全天候數位化服務並提供裝卸貨平台的營運商,更有可能從小型企業客戶那裡獲得更高的每平方英尺收益。

面積較小的儲物單位(小於100平方英尺)將在2024年佔總收入的44%,這得益於都市區高密度和高周轉率。所有尺寸的恆溫儲物櫃的複合年成長率將達到5.9%,優於非恆溫儲物櫃,因為租戶願意為溫濕度控制支付20%至50%的溢價。環境、社會和治理(ESG)要求將推動機構投資者對節能型、整合太陽能的暖通空調系統的需求,這可能會提高這些高階儲物單元在美國自助倉儲市場的佔有率。

能源管理技術的進步降低了營業成本,使營運商能夠在不損害利潤的情況下維持高價,而強調電子設備和文件保護的行銷宣傳活動進一步鞏固了家庭和企業的需求。

美國自助倉儲公司按使用者類型(個人和企業)、單元面積(小型,小於100平方英尺;中型,101-200平方英尺;其他)、物業類型(專用設施、改造後的商業建築;其他)、預訂管道(線下、線上聚合平台和營運商入口網站)、租期(短期、長期)和地區進行細分。市場預測以美元計價。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 都市化進程與居住空間萎縮

- 電子商務中對微型倉配的需求日益成長

- 居民流動性和移民率不斷上升

- 對不良零售/辦公資產進行適應性再利用

- 按需儲存平台的興起

- 倉儲需要減少因天氣原因造成的損失。

- 市場限制

- 城市中心的分區與土地利用管制

- 土地和建築成本上漲

- 對能源密集型氣候單元的ESG審查

- REIT整合帶來的利潤率壓力

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 競爭對手之間的競爭

- 替代品的威脅

- 價格分析(租金/平方英尺)

- 基準化分析營運指標

第5章 市場規模與成長預測

- 依使用者類型

- 個人

- 商業

- 按單位大小

- 小於100平方英尺(小型)

- 101-200平方英尺(中等大小)

- 超過 200 平方英尺(大型/車輛)

- 空調儲物櫃

- 按屬性類型

- 專用設施

- 商業建築改建

- 容器/行動網站

- 透過預訂管道

- 線下(到店/打電話)

- 線上聚合商和營運商入口網站

- 按使用期限

- 短期(少於6個月)

- 長期(6個月或以上)

- 按地區

- 東北

- 中西部

- 南部

- 西

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Metro Storage LLC

- Guardian Storage Solutions

- CubeSmart LP

- Extra Space Storage Inc.

- U-Haul International Inc.

- Life Storage Inc.

- National Storage Affiliates Trust

- Public Storage

- StorageMart

- Simply Self Storage Management LLC

- KO Storage

- Global Self Storage Inc.

- Prime Storage Group

- Storage Asset Management LLC

- SmartStop Self Storage REIT Inc.

- A-American Self Storage

- StorQuest Self Storage

- Safeguard Self Storage

- SpareBox Storage

- Mini U Storage

第7章 市場機會與未來展望

The United States self-storage market size generated USD 45.41 billion in 2025 and is projected to reach USD 57.53 billion by 2030, advancing at a 4.85% CAGR.

Sustained demand stems from urban population growth, shrinking living spaces, and the expanding e-commerce ecosystem that needs micro-fulfillment hubs. Rising adoption of climate-controlled units, adaptive reuse of vacant retail and office buildings, and digital booking platforms add structural resilience and pricing power. Institutional capital continues to reshape competitive dynamics as public REITs deepen market penetration and standardize technology adoption, while zoning constraints and construction-cost inflation temper new supply in densely populated corridors.

United States Self-Storage Market Trends and Insights

Increased Urbanization & Shrinking Dwelling Size

Housing underproduction of 3.85 million units and 1.1% metropolitan population growth magnify space constraints, pushing residents toward external storage solutions. Limited housing supply relative to population gains sustains premium rents for centrally located facilities, ensuring utilization beyond traditional moving spikes. Urban zoning that limits new housing inadvertently lifts long-term storage demand, reinforcing the importance of high-density footprints for operators.

Growth in E-commerce Micro-Fulfillment Demand

E-commerce businesses increasingly deploy the United States self-storage market as an affordable urban micro-warehouse network, driving the business segment's 5.8% CAGR. Container-based sites offer flexible staging for seasonal inventory and rapid market entry, complementing same-day delivery expectations in congested metro areas. Facilities that integrate fulfillment-friendly layouts and extended access hours achieve higher revenue per square foot compared with purely personal-use models.

Zoning & Land-Use Restrictions in Urban Cores

Cities such as Pasco County impose stringent design and landscaping standards, steering developers to less regulated suburbs. Approval delays inflate carrying costs and curb supply growth where demand is strongest, elevating occupancy in existing facilities but reducing incremental expansion potential.

Other drivers and restraints analyzed in the detailed report include:

- Rising Residential Mobility & Migration Rates

- Adaptive Reuse of Distressed Retail/Office Assets

- Escalating Land & Construction Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Personal customers accounted for 73% of the United States self-storage market in 2024, providing a dependable revenue floor rooted in life-event storage needs. Business users, however, are scaling at 5.8% CAGR as online retailers leverage urban units to shorten delivery distances. The United States self-storage market size attributable to business tenants is projected to expand by 2030, signaling a durable shift toward commercial utilization.

Expanding same-day delivery commitments elevate the importance of near-consumer inventory nodes. Operators that design flexible unit mixes, integrate 24/7 digital access, and provide loading docks position themselves to capture structurally higher revenue per square foot from small-business clients.

Small units (<=100 sq ft) captured 44% of 2024 revenue, benefiting from urban density and high turnover. Climate-controlled lockers-spanning all size bands-registered a 5.9% CAGR, outpacing non-conditioned counterparts due to tenant willingness to pay 20-50% premiums for temperature and humidity control. The United States self-storage market share for these premium units is set to climb as ESG mandates drive institutional investors toward energy-efficient, solar-integrated HVAC systems.

Energy management advancements moderate operating costs, allowing operators to maintain premium pricing without margin erosion. Marketing campaigns that highlight protection benefits for electronics and documents further solidify demand among both households and businesses.

United States Self Storage Companies is Segmented by User Type (Personal and Business), Unit Size (<= 100 Sq Ft (Small), 101-200 Sq Ft (Medium), and More), Property Type (Purpose-Built Facilities, Converted Commercial Buildings, and More), Booking Channel (Offline, Online Aggregators & Operator Portals), End-Use Duration (Short-Term, Long-Term), and by Region. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Metro Storage LLC

- Guardian Storage Solutions

- CubeSmart LP

- Extra Space Storage Inc.

- U-Haul International Inc.

- Life Storage Inc.

- National Storage Affiliates Trust

- Public Storage

- StorageMart

- Simply Self Storage Management LLC

- KO Storage

- Global Self Storage Inc.

- Prime Storage Group

- Storage Asset Management LLC

- SmartStop Self Storage REIT Inc.

- A-American Self Storage

- StorQuest Self Storage

- Safeguard Self Storage

- SpareBox Storage

- Mini U Storage

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increased urbanization and shrinking dwelling size

- 4.2.2 Growth in e-commerce micro-fulfilment demand

- 4.2.3 Rising residential mobility and migration rates

- 4.2.4 Adaptive reuse of distressed retail/office assets

- 4.2.5 Emergence of on-demand valet storage platforms

- 4.2.6 Weather-related loss-mitigation storage needs

- 4.3 Market Restraints

- 4.3.1 Zoning and land-use restrictions in urban cores

- 4.3.2 Escalating land and construction costs

- 4.3.3 ESG scrutiny on energy-intensive climate units

- 4.3.4 Margin pressure from REIT consolidation wave

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Intensity of Competitive Rivalry

- 4.7.5 Threat of Substitutes

- 4.8 Pricing Analysis (Rent / sq-ft)

- 4.9 Operational Metrics Benchmarking

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By User Type

- 5.1.1 Personal

- 5.1.2 Business

- 5.2 By Unit Size

- 5.2.1 ? 100 sq ft (Small)

- 5.2.2 101-200 sq ft (Medium)

- 5.2.3 > 200 sq ft (Large/Vehicle)

- 5.2.4 Climate-controlled lockers

- 5.3 By Property Type

- 5.3.1 Purpose-built facilities

- 5.3.2 Converted commercial buildings

- 5.3.3 Container-based/mobile sites

- 5.4 By Booking Channel

- 5.4.1 Offline (walk-in / phone)

- 5.4.2 Online aggregators and operator portals

- 5.5 By End-use Duration

- 5.5.1 Short-term (< 6 months)

- 5.5.2 Long-term (> 6 months)

- 5.6 By Region

- 5.6.1 Northeast

- 5.6.2 Midwest

- 5.6.3 South

- 5.6.4 West

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes global level overview, market level overview, core segments, financials as available, strategic information, market rank/share for key companies, products and services, and recent developments)

- 6.4.1 Metro Storage LLC

- 6.4.2 Guardian Storage Solutions

- 6.4.3 CubeSmart LP

- 6.4.4 Extra Space Storage Inc.

- 6.4.5 U-Haul International Inc.

- 6.4.6 Life Storage Inc.

- 6.4.7 National Storage Affiliates Trust

- 6.4.8 Public Storage

- 6.4.9 StorageMart

- 6.4.10 Simply Self Storage Management LLC

- 6.4.11 KO Storage

- 6.4.12 Global Self Storage Inc.

- 6.4.13 Prime Storage Group

- 6.4.14 Storage Asset Management LLC

- 6.4.15 SmartStop Self Storage REIT Inc.

- 6.4.16 A-American Self Storage

- 6.4.17 StorQuest Self Storage

- 6.4.18 Safeguard Self Storage

- 6.4.19 SpareBox Storage

- 6.4.20 Mini U Storage

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and unmet-need assessment

2026年全球自助倉儲市場報告

2026年全球自助倉儲市場報告 自助倉儲市場:2026-2032年全球市場預測(按單位類型、租賃期限、單位面積、存取方式及最終用戶分類)自助倉儲及搬家服務市場:自助倉儲、搬家服務、單位規模、應用、全球預測(2026-2032年)

自助倉儲市場:2026-2032年全球市場預測(按單位類型、租賃期限、單位面積、存取方式及最終用戶分類)自助倉儲及搬家服務市場:自助倉儲、搬家服務、單位規模、應用、全球預測(2026-2032年) 德國自助倉儲市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)歐洲自助倉儲:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

德國自助倉儲市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)歐洲自助倉儲:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 自助倉儲市場-全球產業規模、佔有率、趨勢、機會、預測:按應用、最終用戶、地區和競爭格局分類,2021-2031年

自助倉儲市場-全球產業規模、佔有率、趨勢、機會、預測:按應用、最終用戶、地區和競爭格局分類,2021-2031年 日本自助倉儲市場報告(按倉儲單元尺寸(小型倉儲單元、中型倉儲單元、大型倉儲單元)、最終用途(個人、商業)和地區分類,2026-2034年)

日本自助倉儲市場報告(按倉儲單元尺寸(小型倉儲單元、中型倉儲單元、大型倉儲單元)、最終用途(個人、商業)和地區分類,2026-2034年) 自助倉儲市場規模、佔有率、按類型、單位規模、最終用途和地區分類的成長分析 - 產業預測,2025 年至 2032 年亞太地區自助倉儲:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

自助倉儲市場規模、佔有率、按類型、單位規模、最終用途和地區分類的成長分析 - 產業預測,2025 年至 2032 年亞太地區自助倉儲:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 自助倉儲市場報告:2031 年趨勢、預測與競爭分析

自助倉儲市場報告:2031 年趨勢、預測與競爭分析