|

市場調查報告書

商品編碼

1851468

歐洲黏合劑和密封劑:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)Europe Adhesives And Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

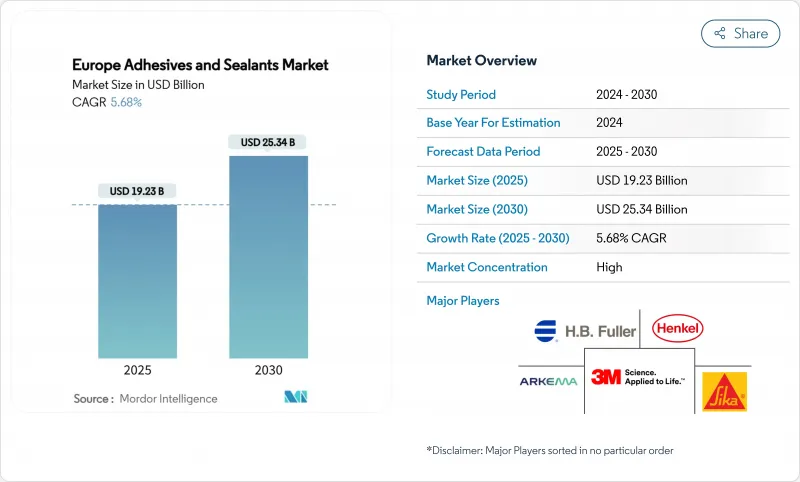

據估計,到 2025 年,歐洲黏合劑和密封劑市場規模將達到 192.3 億美元,預計到 2030 年將達到 253.4 億美元,在預測期(2025-2030 年)內複合年成長率為 5.68%。

這一發展軌跡反映了該產業在應對歐盟綠色協議嚴格法規的同時,充分利用建設業復甦、車輛輕量化強制令以及可再生能源擴張等機會的能力。隨著揮發性有機化合物(VOC)法規的日益嚴格,水性體係正獲得越來越多的關注;紫外光固化化學品則正在提升電子和汽車工廠的生產線速度。德國的綠色交易投資支撐著強勁的需求,而西班牙的可再生能源建設則是該地區結構膠合劑解決方案成長最快的買家。市場競爭依然溫和,大型企業正調整其產品組合,轉向生物基樹脂,並透過主導擴大產能,以應對原料價格波動和碳減排成本帶來的淨利率影響。

歐洲黏合劑和密封劑市場趨勢及洞察

房屋翻新需求不斷成長

受節能法規和後疫情時代生活方式改變的推動,歐洲的房屋翻新工程正蓬勃發展,隔熱材料、地板材料和門窗維修的支出不斷增加。歐盟的翻新浪潮旨在到2030年將建築維修率加倍,從而推動對能夠消除熱感橋的連續黏合系統的需求。德國每年500億歐元(約584.5億美元)的維修市場正日益青睞生物基產品,例如漢高的樂泰HB S ECO。北歐供應商率先研發用於預製外牆板的工廠預塗黏合劑,從而實現現場快速組裝,同時滿足嚴格的室內空氣品質標準。在這一維修趨勢的推動下,預計到2028年,歐洲建築幕牆和密封劑市場將保持銷售成長。

電子商務包裝量快速成長

小包裹運輸量的成長迫使加工商採用快速、無溶劑的黏合劑解決方案,以滿足歐洲包裝聯合會 (FEICA) 發布的紙張回收指南。軟包裝黏合劑必須在黏合強度和脫墨性之間取得平衡,同時還要支援單一材料設計,從而簡化歐盟塑膠戰略下的回收流程。德國和荷蘭的自動化生產線升級改造正在增加,這需要嚴格的黏度控制和快速固化。這些趨勢推動了歐洲黏合劑和密封劑市場的擴張,尤其是針對高產能的熱熔型和水性黏合劑。

日益成長的環境問題

REACH法規中關於二異氰酸酯的規定將於2023年8月生效,屆時將要求對聚氨酯體系進行改造或對工人進行培訓;而甲醛排放法規將於2026年8月生效,屆時將鼓勵轉向超低排放等級的產品。新增的247種高度關注物質(SVHC),包括八甲基三矽氧烷,將增加監管的不確定性。對永續性投資的需求將使歐洲化工產業的年度資本支出增加70%,這將壓縮淨利率,但也會刺激生物基原料的長期創新。

細分市場分析

由於丙烯酸樹脂用途廣泛且對多種基材具有良好的黏合性,預計到2024年,其在歐洲黏合劑和密封劑市場仍將佔據37.16%的佔有率。隨著碳減排需求的日益嚴格,包括生物基創新產品在內的其他樹脂預計將在2030年前以6.96%的複合年成長率成長。隨著BASF可再生丙烯酸乙酯的上市以及Xylan熱熔膠展現出30 MPa的搭接剪切強度並保持可重複使用性,歐洲生物基黏合劑和密封劑市場預計將進一步擴大。氰基丙烯酸酯在電子微型化領域獲得廣泛應用,而聚氨酯模塑製造商則致力於開發無需二異氰酸酯固化的濕固化系統。矽膠樹脂在高溫領域表現強勁,而VAE/EVA則持續保持其對成本敏感的細分市場地位。

到2024年,水性平台將佔總以銷售額為準的43.19%,這反映了其與現有生產線和VOC排放限制的契合度;但隨著組裝廠對即時粘合工藝的需求,UV固化系統到2030年將以6.54%的複合年成長率成長。 Panacol的黑色UV環氧樹脂可形成較厚的固化層,消除陰影區域,目前已被指定用於電動車馬達線束的應力消除接頭。

反應型熱熔膠兼具快速固化和牢固黏合的優點,尤其適用於高速包裝生產線。航太領域對溶劑型膠合劑的需求持續成長,因為該領域對較長的開放時間要求很高;同時,高固態膠合劑有助於滿足日益嚴格的排放法規。 LED-UV燈等設備的升級可降低能耗,進一步推動歐洲膠合劑和密封劑市場的技術轉型。

歐洲黏合劑和密封劑報告按黏合劑樹脂(丙烯酸、氰基丙烯酸酯、環氧樹脂、其他)、黏合劑技術(熱熔、反應型、溶劑型、其他)、密封劑樹脂(聚氨酯、環氧樹脂、丙烯酸、其他)、最終用戶產業(航太、汽車、建築、其他)和地區(德國、英國、法國、義大利、其他國家)

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 房屋翻新需求不斷成長

- 電子商務包裝量快速成長

- 加速歐洲汽車產業的輕量化進程

- 快速成長的風力發電機葉片黏接市場

- 預製模組化建築的興起

- 市場限制

- 日益成長的環境問題

- 原物料價格不穩定

- 機器人黏合劑應用勞動力技能缺口

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 通過粘合樹脂

- 丙烯酸纖維

- 氰基丙烯酸酯

- 環氧樹脂

- 聚氨酯

- 矽酮

- VAE/EVA

- 其他樹脂(矽烷改性聚合物(SMP)、生物基樹脂等)

- 透過黏合技術

- 熱熔膠

- 反應性

- 溶劑型

- 紫外線固化型

- 水溶液

- 通過密封樹脂

- 聚氨酯

- 環氧樹脂

- 丙烯酸纖維

- 矽酮

- 其他樹脂(聚硫化物、SMP混合樹脂等)

- 按最終用戶行業分類

- 航太

- 車

- 建築/施工

- 鞋類和皮革

- 衛生保健

- 包裝

- 木工和細木工

- 其他終端用戶產業(例如,可再生能源、電子產品和家電)

- 按地區

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- 3M

- Akzo Nobel NV

- Arkema

- Avery Dennison Corporation

- BASF

- Dow

- Dymax

- HB Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC.

- Jowat

- Mapei SpA

- Momentive

- Munzing

- PPG Industries, Inc.

- Sika AG

- Soudal Group

- Wacker Chemie AG

第7章 市場機會與未來展望

The Europe Adhesives And Sealants Market size is estimated at USD 19.23 billion in 2025, and is expected to reach USD 25.34 billion by 2030, at a CAGR of 5.68% during the forecast period (2025-2030).

This trajectory reflects the sector's ability to navigate stringent EU Green Deal regulations while capitalizing on construction recovery, automotive lightweighting mandates, and renewable-energy expansion. Water-borne systems gain traction as VOC limits tighten, and UV-cured chemistries accelerate line speeds in electronics and automotive plants. German infrastructure outlays underpin steady demand, while Spain's renewable build-out positions it as the region's quickest-growing buyer of structural bonding solutions. Competitive intensity remains moderate, with large incumbents refocusing portfolios on bio-based resins and acquisition-driven capability expansion to safeguard margins against feedstock price volatility and carbon-reduction costs.

Europe Adhesives And Sealants Market Trends and Insights

Rising Demand from Residential Renovation

European renovation activity is gathering momentum as energy-efficiency mandates and post-pandemic lifestyle shifts lift spending on insulation, flooring, and window upgrades. The EU Renovation Wave aims to double building refurbishment rates by 2030, bolstering demand for continuous-bonding systems that eliminate thermal bridging. Germany's EUR 50 billion (~USD 58.45 billion) annual renovation market increasingly specifies bio-based products such as Henkel's LOCTITE HB S ECO, which cuts embodied CO2 by more than 60% compared with fossil-based counterparts. Nordic suppliers pioneer factory-applied adhesives for prefabricated facade panels, allowing rapid site assembly while meeting stringent indoor-air-quality norms. This renovation push is set to sustain volume growth for the European adhesives and sealants market through 2028.

Surge in E-Commerce Packaging Volumes

Rising parcel shipments prompt converters to adopt high-speed, solvent-free bonding solutions compatible with paper-recycling guidelines published by FEICA. Flexible-packaging adhesives must balance bond strength and de-inkability while supporting mono-material designs that simplify recycling under the EU Plastics Strategy. Germany and the Netherlands are upgrading automated lines that require tight viscosity control and quick setting. These trends underpin incremental gains for the European adhesives and sealants market, especially in hot-melt and waterborne grades engineered for rapid throughput.

Rising Environmental Concerns

REACH diisocyanate restrictions effective August 2023 force reformulation of polyurethane systems or mandatory worker training, while formaldehyde emission ceilings effective August 2026 drive shifts to ultra-low-emission grades. The addition of 247 SVHCs, including octamethyltrisiloxane, extends regulatory uncertainty. Sustainability investment needs 70% higher annual capital outlays across Europe's chemical sector, compressing margins yet spurring long-run innovation in bio-based feedstocks.

Other drivers and restraints analyzed in the detailed report include:

- Accelerating Lightweighting in European Auto Industry

- Fast-Growing Wind-Turbine Blade Bonding Market

- Volatile Feedstock Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Acrylics retained 37.16% revenue share of the European adhesives and sealants market in 2024, thanks to versatility and adhesion to diverse substrates. Other resins, including bio-based innovations, are forecast to expand 6.96% CAGR to 2030 as carbon-reduction mandates intensify. Europe adhesives and sealants market size for bio-based grades is projected to widen as BASF's renewable ethyl acrylate rolls out and xylan hot-melts demonstrate 30 MPa lap-shear while remaining reusable. Cyanoacrylates gain traction in electronics miniaturization, and polyurethane formulators pursue moisture-curing systems that bypass diisocyanate training. Silicone chemistries grow in high-temperature segments, whereas VAE/EVA retains cost-driven niches.

Waterborne platforms accounted for 43.19% of the 2024 revenue base, reflecting entrenched production lines and alignment with VOC caps. UV-cured systems, however, will post a 6.54% CAGR through 2030 as assembly plants seek instant-bond processing. Panacol's black UV epoxies cure in thicker layers, eliminating shadow areas, and are now specified in EV motor wire stress-relief joints.

Reactive hot melts combine rapid set with strong final bonds, serving high-speed packaging lines. Solvent-borne demand persists in aerospace, where long open time is critical, but higher-solids versions help meet tightening emission norms. Equipment upgrades toward LED-UV lamps cut energy use and further incentivize technology switching in the European adhesives and sealants market.

The Europe Adhesives and Sealants Report is Segmented by Adhesive Resin (Acrylic, Cyanoacrylate, Epoxy, and More), Adhesive Technology (Hot-Melt, Reactive, Solvent-Borne, and More), Sealant Resin (Polyurethane, Epoxy, Acrylic, and More), End-User Industry (Aerospace, Automotive, Building and Construction, and More), and Geography (Germany, United Kingdom, France, Italy, Spain, Russia, NORDIC Countries, and Rest of Europe).

List of Companies Covered in this Report:

- 3M

- Akzo Nobel N.V.

- Arkema

- Avery Dennison Corporation

- BASF

- Dow

- Dymax

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC.

- Jowat

- Mapei S.p.A

- Momentive

- Munzing

- PPG Industries, Inc.

- Sika AG

- Soudal Group

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand from Residential-Renovation

- 4.2.2 Surge in E-Commerce Packaging Volumes

- 4.2.3 Accelerating Lightweighting in European Auto Industry

- 4.2.4 Fast-Growing Wind-Turbine Blade Bonding Market

- 4.2.5 Prefab Modular Construction Uptake

- 4.3 Market Restraints

- 4.3.1 Rising Environmental Concerns

- 4.3.2 Volatile Feedstock Prices

- 4.3.3 Skill Gap in Robotic Adhesive-Dispensing Workforce

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products and Services

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Adhesive Resin

- 5.1.1 Acrylic

- 5.1.2 Cyanoacrylate

- 5.1.3 Epoxy

- 5.1.4 Polyurethane

- 5.1.5 Silicone

- 5.1.6 VAE / EVA

- 5.1.7 Other Resins (Silane-Modified Polymer (SMP), Bio-based Resins, etc.)

- 5.2 By Adhesive Technology

- 5.2.1 Hot-Melt

- 5.2.2 Reactive

- 5.2.3 Solvent-Borne

- 5.2.4 UV-Cured

- 5.2.5 Water-Borne

- 5.3 By Sealant Resin

- 5.3.1 Polyurethane

- 5.3.2 Epoxy

- 5.3.3 Acrylic

- 5.3.4 Silicone

- 5.3.5 Other Resins (Polysulfide, SMP Hybrid, etc.)

- 5.4 By End-User Industry

- 5.4.1 Aerospace

- 5.4.2 Automotive

- 5.4.3 Building and Construction

- 5.4.4 Footwear and Leather

- 5.4.5 Healthcare

- 5.4.6 Packaging

- 5.4.7 Woodworking and Joinery

- 5.4.8 Other End-User Industries (Renewable Energy,Electronics and Appliances, etc.)

- 5.5 By Geography

- 5.5.1 Germany

- 5.5.2 United Kingdom

- 5.5.3 France

- 5.5.4 Italy

- 5.5.5 Spain

- 5.5.6 Russia

- 5.5.7 NORDIC Countries

- 5.5.8 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Akzo Nobel N.V.

- 6.4.3 Arkema

- 6.4.4 Avery Dennison Corporation

- 6.4.5 BASF

- 6.4.6 Dow

- 6.4.7 Dymax

- 6.4.8 H.B. Fuller Company

- 6.4.9 Henkel AG & Co. KGaA

- 6.4.10 Huntsman International LLC.

- 6.4.11 Jowat

- 6.4.12 Mapei S.p.A

- 6.4.13 Momentive

- 6.4.14 Munzing

- 6.4.15 PPG Industries, Inc.

- 6.4.16 Sika AG

- 6.4.17 Soudal Group

- 6.4.18 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 EU Green Deal push for low-VOC and circular materials

- 7.3 Innovation and Development of Bio-based Adhesives

黏合劑和密封劑市場:2026-2032年全球市場預測(按產品類型、技術、形態、最終用途產業、應用和分銷管道分類)

黏合劑和密封劑市場:2026-2032年全球市場預測(按產品類型、技術、形態、最終用途產業、應用和分銷管道分類) 全球黏合劑和密封劑市場,2026-2030年

全球黏合劑和密封劑市場,2026-2030年 黏合劑和密封劑市場報告:黏合劑類型、密封劑類型、技術、應用和地區分類(2026-2034 年)建築外牆黏合劑和密封劑市場:2026-2032年全球市場預測(按產品類型、技術、配方、分銷管道、最終用途行業和應用分類)彈性黏合劑和密封劑市場:2026-2032年全球市場預測(按樹脂類型、包裝、應用方法、終端用戶產業和分銷管道分類)

黏合劑和密封劑市場報告:黏合劑類型、密封劑類型、技術、應用和地區分類(2026-2034 年)建築外牆黏合劑和密封劑市場:2026-2032年全球市場預測(按產品類型、技術、配方、分銷管道、最終用途行業和應用分類)彈性黏合劑和密封劑市場:2026-2032年全球市場預測(按樹脂類型、包裝、應用方法、終端用戶產業和分銷管道分類) 消費性電子產品黏合劑市場預測至2034年:按黏合劑類型、應用、最終用戶和地區分類的全球分析電子設備以黏合劑、密封劑和填充物市場:按產品類型、技術、形式、應用和分銷管道分類-2026-2032年全球預測熱熔丁基黏合劑機械市場(按機器類型、黏合劑形式、噴嘴類型、功率等級、應用、終端用戶產業和分銷管道分類),全球預測,2026-2032年

消費性電子產品黏合劑市場預測至2034年:按黏合劑類型、應用、最終用戶和地區分類的全球分析電子設備以黏合劑、密封劑和填充物市場:按產品類型、技術、形式、應用和分銷管道分類-2026-2032年全球預測熱熔丁基黏合劑機械市場(按機器類型、黏合劑形式、噴嘴類型、功率等級、應用、終端用戶產業和分銷管道分類),全球預測,2026-2032年 2026-2034年全球雙層玻璃黏合劑和密封劑市場規模、佔有率、趨勢和成長分析報告全球黏合劑和密封劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

2026-2034年全球雙層玻璃黏合劑和密封劑市場規模、佔有率、趨勢和成長分析報告全球黏合劑和密封劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年)