|

市場調查報告書

商品編碼

1851092

MEMS:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)MEMS - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

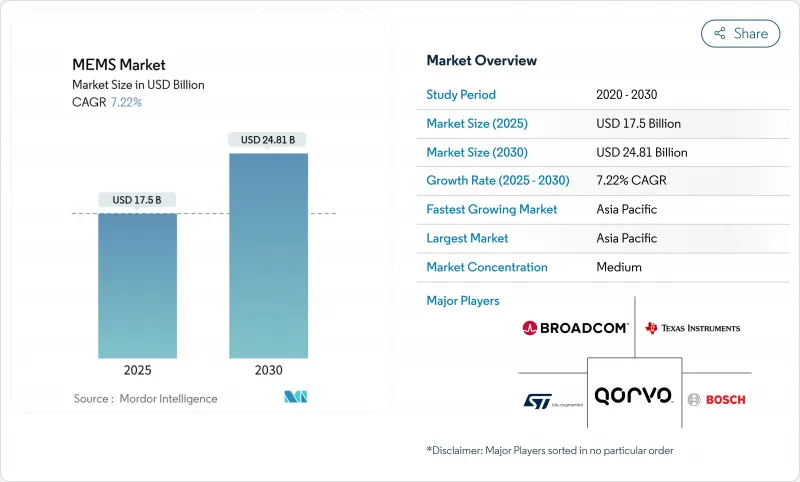

全球 MEMS 市場預計到 2025 年將達到 175 億美元,到 2030 年將達到 248.1 億美元,複合年成長率高達 7.22%。

這一發展勢頭主要得益於智慧型手機、電動車、醫療穿戴式裝置和工業IoT節點中感測器數量的日益成長,這些設備需要耐用、低功耗和小型化的組件。汽車電氣化推動了每輛車壓力、溫度和慣性感測器數量的增加,而照護現場技術則推動微流體晶片從試驗生產線走向量產。 5G基礎設施的建設將進一步增加對能夠在不斷擴展的頻寬內保持低插入損耗的射頻濾波器的需求。雖然美國300毫米晶圓試生產啟動提高了供應的穩定性,但市場競爭仍然分散,一些專注於特定領域的專家在新興應用場景(例如邊緣人工智慧感測器融合)中贏得了設計訂單。

全球MEMS市場趨勢與洞察

物聯網和邊緣設備的普及應用日益廣泛

互聯終端的激增要求工廠、建築和物流中心在每個資產上整合數十個感測器,其中低功耗加速計、陀螺儀和環境監測器正成為標準組件。半導體公司正在將MEMS感測器與微控制器封裝在一起,以提供本地化分析,從而降低回程傳輸頻寬和雲端延遲。邊緣AI晶片直接在感測器節點上運行決定架構和輕量級神經網路,這促使供應商重新思考低於50µW功耗預算的設計規則,從而推動持續的重新設計週期,擴大MEMS市場。

電動車和高級駕駛輔助系統(ADAS)中感測器數量的擴展

電動車所配備的壓力感測器、慣性感測器和環境感測器數量是內燃機汽車的兩到三倍。村田製作所新推出的國產汽車慣性感測器產品線表明,在傳統行動裝置銷售低迷的情況下,日本供應商正轉向行動出行領域尋求收入成長。 TDK 的光學 MEMS 反射鏡可用於主動式轉向頭燈和固態雷射雷達,並為每個車型提供差異化的介面。LiDAR供應商 RoboSense 預測,到 2024 年,其將佔據全球汽車雷射雷達市場 33.5% 的佔有率,這凸顯了高級駕駛輔助系統和高精度感測技術之間相互關聯的成長趨勢。

複雜且資本密集型製造業

向300毫米晶圓過渡雖然降低了晶圓成本,但需要新的光刻、鍵合和計量設備,每條生產線的購買成本超過5億美元。 SEMI預測,2025年第一季300毫米晶圓出貨量將成長6%,但中小型MEMS晶圓廠卻難以獲得升級所需的資金籌措。美國《晶片製造和整合法案》(CHIPS Act)的激勵措施為少數國內計劃提供了資金籌措便利,其中包括Rogue Valley Microdevices位於佛羅裡達州的晶圓廠,該廠計劃於2025年投產。沒有300毫米產能的供應商面臨日益擴大的成本差距,利潤空間受到擠壓。

細分市場分析

到2024年,隨著行動電話OEM廠商、汽車一級供應商和工業自動化公司對慣性、壓力和環境封裝的標準化,感測器將佔MEMS市場收入的57%。這個MEMS市場的主導地位表明,成熟的製造流程能夠提高成本效益,同時在嚴苛環境下保持可靠性。智慧型手機整合多達六個獨立的運動和音訊感測器,以及汽車整合三重冗餘加速計用於安全氣囊、穩定性控制和ADAS功能,都推動了這一領域的發展。相較之下,與光學影像穩定馬達和用於雷射雷達光束控制的微鏡陣列相關的致動器,則呈現穩定但增速放緩的成長態勢。振盪器正在取代汽車動力傳動系統中的石英晶體,隨著電氣化進程的加速,預計其應用將更加廣泛。

微流體晶片代表著一項前沿技術,其複合年成長率高達 9.8%。晶片實驗室整合了毛細管流動控制、電化學感測和板載試劑,將診斷週期從數天縮短至數分鐘。醫院採購負責人優先考慮簡化的樣本製備流程和盡可能減少微流體。這一新的市場格局有助於實現持續差異化,將擁有表面化學專業知識的供應商定位為優質合作夥伴,並將 MEMS 市場拓展到傳統電子機械領域之外。

慣性感測器將佔2024年營收的24.5%,用於智慧型手機方向偵測、汽車防翻和工業追蹤模組。其在振動和極端溫度下的可靠性已得到驗證,鞏固了該類別在MEMS市場中的重要性。持續的性能提升,例如低於1°/h的偏置漂移,正在拓展其應用範圍,使其應用於精密農業和倉儲自動化機器人等領域。同時,射頻MEMS組件的複合年成長率將達到10.4%,因為5G部署需要靈活的頻譜調諧,而固定陶瓷濾波器無法實現這一點。代工廠正在投資晶圓級氣密封裝,以保護高Q值諧振腔免受潮氣侵蝕,從而提高產量比率並提昇平均售價。

MEMS麥克風、壓力感測器和環境檢測器的銷售持續穩定成長。意法半導體(STMicroelectronics)計劃於2024年發布一款整合有限狀態機邏輯的自主工業級IMU,該IMU強調了邊緣智慧技術,只需少量程式碼即可在傳輸前過濾事件。光學MEMS反射鏡的出現,使得固態雷射雷達(LiDAR)的運動品質與抗機械疲勞性能大幅提升。

區域分析

亞太地區預計到2024年將維持45%的營收佔有率,並在2030年前以10.7%的複合年成長率成長。中國本土廠商正加速推動射頻前端專利申請,旨在實現5G和衛星通訊的在地化供應。日本TDK和村田製作所將提高汽車慣性感測器的產能,以滿足全球電氣化需求。韓國將利用其先進的記憶體無塵室技術,實現MEMS時序元件的多元化發展;而新加坡和馬來西亞則將擴大測試和組裝叢集,以降低人事費用。

北美受益於強大的航太和國防項目以及醫療設備創新管道。晶片專案辦公室(CHIPS)為採用微機電系統(MEMS)試點生產線的晶圓廠爭取到了數十億美元的津貼,從而縮短了國內供應鏈。 2025年第一季矽晶圓出貨量年增2.2%,對300毫米晶圓的需求顯示大規模生產的準備工作已經就緒。隨著佛羅裡達州一家新的MEMS晶圓廠於2025年開始量產,該地區的韌性將會提升。

歐洲正著力發展汽車安全、工業自動化和醫療穿戴設備。強制推行高階駕駛輔助功能的法律規範將加速感測器的普及,進而提升該地區對微機電系統(MEMS)市場的貢獻。意法半導體(STMicroelectronics)的自主工業慣性測量單元(IMU)滿足了德國和義大利設備製造商對長使用壽命的嚴格要求。中東和非洲仍在發展中,但海灣國家的智慧城市試點計畫為分散式空氣品質感測和智慧照明樹立了標竿。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 物聯網和邊緣設備的普及應用日益廣泛

- 電動車和高級駕駛輔助系統(ADAS)中感測器數量的擴展

- 5G的普及將推動射頻MEMS濾波器的發展。

- 將MEMS技術轉移到300毫米晶圓製造

- 異質整合和晶片封裝

- 微射流微機電在即時診斷的應用激增

- 市場限制

- 複雜且資本密集型製造業

- 設計標準化與流程標準化之間的差距

- 供應鏈對特殊材料的依賴性

- 射頻微機電系統專利叢林推高授權成本

- 價值/供應鏈分析

- 技術展望

- 監管環境

- 波特五力模型

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 按設備類別

- 感應器

- 致動器

- 振盪器和定時

- 微流體晶片

- 動力/運動微型發電機

- 按下感測器/致動器類型

- 慣性感測器

- 壓力感測器

- RF MEMS

- 光學MEMS

- 環境感測器

- MEMS麥克風

- 微測輻射熱計和紅外線檢測器

- 噴墨印字頭

- 其他

- 透過使用

- 消費性電子產品

- 車

- 工業與機器人

- 醫療保健和醫療設備

- 通訊基礎設施

- 航太/國防

- 其他

- 透過製造程序

- 大量微機械加工

- 表面微加工

- 高回火矽蝕刻/深反應離子蝕刻

- 絕緣體上矽(SOI)微機電系統

- LIGA和X光微影術

- 先進的3D列印MEMS

- 材料

- 矽

- 聚合物

- 壓電(氮化鋁、壓電陶瓷)

- 金屬

- 化合物半導體

- 石英和玻璃

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 歐洲

- 德國

- 法國

- 英國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 東南亞

- 澳洲、紐西蘭

- 亞太其他地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Robert Bosch GmbH

- Broadcom Inc.

- STMicroelectronics NV

- Texas Instruments Inc.

- TDK Corporation(InvenSense)

- Qorvo Inc.

- Infineon Technologies AG

- NXP Semiconductors NV

- Knowles Electronics LLC

- Panasonic Corporation

- GoerTek Inc.

- Honeywell International Inc.

- Murata Manufacturing Co., Ltd.

- Analog Devices Inc.

- Alps Alpine Co., Ltd.

- Omron Corporation

- Sensata Technologies

- Silex Microsystems AB

- Teledyne MEMS

- Rogue Valley Microdevices Inc.

第7章 市場機會與未來展望

The global MEMS market size stands at USD 17.50 billion in 2025 and is projected to reach USD 24.81 billion by 2030, reflecting a steady 7.22% CAGR.

Momentum stems from rising sensor penetration in smartphones, electric vehicles, medical wearables, and industrial IoT nodes that demand durable, low-power, and miniaturized components. Automotive electrification multiplies pressure, temperature, and inertial sensor counts per vehicle, while point-of-care diagnostics pull microfluidic chips from pilot lines into mass production. Advancing 5G infrastructure further amplifies demand for RF MEMS filters that sustain low insertion loss across expanding frequency bands. Supply resilience improves as 300 mm wafer processing enters pilot runs in the United States, yet competition remains fragmented, letting niche specialists capture design wins in emerging use-cases such as edge AI sensor fusion.

Global MEMS Market Trends and Insights

Rising adoption of IoT & edge devices

The climb in connected endpoints obliges factories, buildings, and logistics hubs to embed dozens of sensors per asset, turning low-power accelerometers, gyroscopes, and environmental monitors into standard bill-of-materials components. Semiconductor companies increasingly package MEMS sensors with microcontrollers to deliver localized analytics that cut backhaul bandwidth and cloud latency. Edge AI chips that run decision trees or lightweight neural networks directly on sensor nodes push suppliers to rethink design rules for power budgets below 50 µW, prompting sustained redesign cycles that enlarge the MEMS market.

Expanding sensor content in EV & ADAS

Electric vehicles contain 2-3 X more pressure, inertial, and environmental sensors than internal-combustion cars. Murata's new domestic line for automotive-grade inertial sensors underlines how Japanese suppliers pivot to mobility revenue as legacy handset volumes plateau newswitch. Optical MEMS mirrors from TDK enable adaptive headlights and solid-state LiDAR, adding differentiated sockets per vehicle. LiDAR vendor RoboSense captured 33.5% global automotive LiDAR revenue in 2024, underscoring the intertwined growth of advanced driver assistance and high-precision sensing.

Complex & capital-intensive manufacturing

Transitioning to 300 mm wafers cuts die cost but demands new lithography, bonding, and metrology tools whose acquisition can exceed USD 500 million per line. SEMI projects 6% growth in 300 mm wafer shipments in Q1 2025, yet smaller MEMS fabs struggle to raise capital for the upgrade.U.S. CHIPS Act incentives ease financing for a handful of domestic projects, including Rogue Valley Microdevices' Florida fab slated for 2025 production. Suppliers without -300 mm capacity face widening cost gaps that compress margins.

Other drivers and restraints analyzed in the detailed report include:

- Proliferation of 5G driving RF MEMS filters

- Surge in microfluidic MEMS for PoC diagnostics

- RF MEMS patent thickets raising licensing costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Sensors generated 57% of 2024 revenue as handset OEMs, automotive Tier-1 suppliers, and industrial automation houses all standardize inertial, pressure, and environmental packages. This dominant slice of the MEMS market underlines how mature manufacturing nodes deliver cost efficiency while maintaining reliability in harsh environments. The segment benefits from smartphones that embed up to six discrete motion and audio sensors, and vehicles that now integrate triple-redundant accelerometers for airbag, stability, and ADAS functions. In contrast, actuators deliver stable but slower growth tied to optical image-stabilization motors and micro-mirror arrays for LiDAR beam steering. Oscillators displace quartz timing in automotive powertrains, foreseeing rising attach rates as electrification accelerates.

Microfluidic chips, at 9.8% CAGR, represent the technology frontier. Lab-on-a-chip cartridges combine capillary flow control, electrochemical sensing, and on-board reagents, cutting diagnostic cycle time from days to minutes. Hospital procurement managers value simplified sample prep and minimal operator training, pushing device makers toward fully disposable units that rely on polymer-based MEMS flow channels. Pharmaceutical firms explore organ-on-chip platforms to model human tissue response, creating additional pull for high-precision microfluidic fabrication. This emerging basket supports sustained differentiation and positions suppliers that master surface chemistry as premium partners, expanding the MEMS market beyond traditional electromechanical spheres.

Inertial sensors secured 24.5% of 2024 revenue, underpinning smartphone orientation detection, automotive rollover protection, and industrial track-and-trace modules. Their proven reliability under vibration and temperature extremes cements the category's relevance within the MEMS market. Continuous performance improvements, such as bias drift under 1°/h, extend use-cases into precision agriculture and warehouse automation robotics. Meanwhile, RF MEMS components deliver 10.4% CAGR as 5G deployments request agile spectrum tuning unattainable with fixed ceramic filters. Foundries invest in hermetic wafer-level packaging to guard high-Q cavities against moisture ingress, safeguarding yield and elevating average selling prices.

MEMS microphones, pressure sensors, and environmental detectors sustain steady volume growth. STMicroelectronics' 2024 release of an autonomous industrial IMU that integrates finite-state-machine logic underscores the pivot toward edge intelligence where small code snippets filter events before transmission. Optical MEMS mirrors advance solid-state LiDAR, benefiting from minimal moving mass and mechanical fatigue resistance.

The MEMS Market is Segmented by Device Class (Sensors, Actuators, and More), Sensor/Actuator Type (Inertial Sensors, Pressure Sensors, and More), Application (Consumer Electronics, Automotive, and More), Fabrication Process (Bulk Micromachining, Surface Micromachining, and More), Material (Silicon, Polymers, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific retained 45% revenue share in 2024 and is tracking a 10.7% CAGR through 2030. China's domestic vendors accelerate patent filings in RF front-ends, aiming to localize supply for 5G and satellite communications. Japanese champions TDK and Murata extend capacity for automotive-grade inertial sensors to capture global electrification demand. South Korea leverages advanced memory cleanrooms to diversify into MEMS timing devices, while Singapore and Malaysia expand test-and-assembly clusters that offer lower labor cost structures.

North America benefits from strong aerospace and defense programs as well as medical device innovation pipelines. The CHIPS Program Office awarded multi-billion-dollar grant negotiations to fabs that incorporate MEMS pilot lines, encouraging shorter domestic supply chains. Silicon wafer shipments rose 2.2% year-on-year in Q1 2025, with 300 mm category demand signalling readiness for high-volume production. Florida's new MEMS foundry will add regional resilience when it enters volume production in 2025.

Europe concentrates on automotive safety, industrial automation, and medical wearables. Regulatory frameworks mandating advanced driver assistance functions accelerate sensor penetration, boosting the region's contribution to the MEMS market. STMicroelectronics' autonomous industrial IMU caters to stringent long-lifecycle demands from German and Italian equipment makers. The Middle East and Africa remain nascent, yet smart-city pilots in Gulf states create lighthouse references for distributed air-quality sensing and intelligent lighting.

- Robert Bosch GmbH

- Broadcom Inc.

- STMicroelectronics N.V.

- Texas Instruments Inc.

- TDK Corporation (InvenSense)

- Qorvo Inc.

- Infineon Technologies AG

- NXP Semiconductors N.V.

- Knowles Electronics LLC

- Panasonic Corporation

- GoerTek Inc.

- Honeywell International Inc.

- Murata Manufacturing Co., Ltd.

- Analog Devices Inc.

- Alps Alpine Co., Ltd.

- Omron Corporation

- Sensata Technologies

- Silex Microsystems AB

- Teledyne MEMS

- Rogue Valley Microdevices Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising adoption of IoT and edge devices

- 4.2.2 Expanding sensor content in EV and ADAS

- 4.2.3 Proliferation of 5G driving RF MEMS filters

- 4.2.4 Shift to 300 mm MEMS wafer fabrication

- 4.2.5 Heterogeneous integration and chiplet packaging

- 4.2.6 Surge in microfluidic MEMS for PoC diagnostics

- 4.3 Market Restraints

- 4.3.1 Complex and capital-intensive manufacturing

- 4.3.2 Design and process standardization gaps

- 4.3.3 Supply-chain dependence on specialty materials

- 4.3.4 RF MEMS patent thickets raising licensing costs

- 4.4 Value / Supply-Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Landscape

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Device Class

- 5.1.1 Sensors

- 5.1.2 Actuators

- 5.1.3 Oscillators and Timing

- 5.1.4 Microfluidic Chips

- 5.1.5 Power/Motion Micro-generators

- 5.2 By Sensor / Actuator Type

- 5.2.1 Inertial Sensors

- 5.2.2 Pressure Sensors

- 5.2.3 RF MEMS

- 5.2.4 Optical MEMS

- 5.2.5 Environmental Sensors

- 5.2.6 MEMS Microphones

- 5.2.7 Microbolometers and IR Detectors

- 5.2.8 Ink-jet Heads

- 5.2.9 Others

- 5.3 By Application

- 5.3.1 Consumer Electronics

- 5.3.2 Automotive

- 5.3.3 Industrial and Robotics

- 5.3.4 Healthcare and Medical Devices

- 5.3.5 Telecom Infrastructure

- 5.3.6 Aerospace and Defense

- 5.3.7 Others

- 5.4 By Fabrication Process

- 5.4.1 Bulk Micromachining

- 5.4.2 Surface Micromachining

- 5.4.3 HAR Silicon Etching / DRIE

- 5.4.4 Silicon-on-Insulator (SOI) MEMS

- 5.4.5 LIGA and X-ray Lithography

- 5.4.6 Advanced 3D-Printed MEMS

- 5.5 By Material

- 5.5.1 Silicon

- 5.5.2 Polymers

- 5.5.3 Piezoelectric (AlN, PZT)

- 5.5.4 Metals

- 5.5.5 Compound Semiconductors

- 5.5.6 Quartz and Glass

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 France

- 5.6.3.3 United Kingdom

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 APAC

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 South Korea

- 5.6.4.4 India

- 5.6.4.5 Southeast Asia

- 5.6.4.6 Australia and New Zealand

- 5.6.4.7 Rest of APAC

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 UAE

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Robert Bosch GmbH

- 6.4.2 Broadcom Inc.

- 6.4.3 STMicroelectronics N.V.

- 6.4.4 Texas Instruments Inc.

- 6.4.5 TDK Corporation (InvenSense)

- 6.4.6 Qorvo Inc.

- 6.4.7 Infineon Technologies AG

- 6.4.8 NXP Semiconductors N.V.

- 6.4.9 Knowles Electronics LLC

- 6.4.10 Panasonic Corporation

- 6.4.11 GoerTek Inc.

- 6.4.12 Honeywell International Inc.

- 6.4.13 Murata Manufacturing Co., Ltd.

- 6.4.14 Analog Devices Inc.

- 6.4.15 Alps Alpine Co., Ltd.

- 6.4.16 Omron Corporation

- 6.4.17 Sensata Technologies

- 6.4.18 Silex Microsystems AB

- 6.4.19 Teledyne MEMS

- 6.4.20 Rogue Valley Microdevices Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

MEMS冷卻系統-2026年至2034年全球市佔率及排名、總收入及需求預測

MEMS冷卻系統-2026年至2034年全球市佔率及排名、總收入及需求預測 全球微機電系統(MEMS)市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球微機電系統(MEMS)市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 電子機械系統(NEMS)市場分析及至2035年預測:類型、產品類型、技術、組件、應用、材料類型、裝置、最終用戶、功能微機電系統 (MEMS) 市場分析及預測(至 2035 年):按類型、產品、服務、技術、組件、應用、材料類型、裝置和最終用戶分類

電子機械系統(NEMS)市場分析及至2035年預測:類型、產品類型、技術、組件、應用、材料類型、裝置、最終用戶、功能微機電系統 (MEMS) 市場分析及預測(至 2035 年):按類型、產品、服務、技術、組件、應用、材料類型、裝置和最終用戶分類 2026年全球電子機械系統(MEMS)振盪器市場報告2026年微機電系統(MEMS)全球市場報告2026年微機電系統(MEMS)全球市場報告

2026年全球電子機械系統(MEMS)振盪器市場報告2026年微機電系統(MEMS)全球市場報告2026年微機電系統(MEMS)全球市場報告 電子機械系統市場-全球產業規模、佔有率、趨勢、機會及預測(依產品類型、材料、應用、地區及競爭格局分類,2021-2031年)

電子機械系統市場-全球產業規模、佔有率、趨勢、機會及預測(依產品類型、材料、應用、地區及競爭格局分類,2021-2031年) 全球電子機械系統(NEMS)市場,2026-2030年

全球電子機械系統(NEMS)市場,2026-2030年 MEMS射頻濾波器市場按濾波器類型、技術類型、頻率範圍、應用和最終用戶產業分類,全球預測(2026-2032年)

MEMS射頻濾波器市場按濾波器類型、技術類型、頻率範圍、應用和最終用戶產業分類,全球預測(2026-2032年)