|

市場調查報告書

商品編碼

1755206

微製造設備市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Micro-Manufacturing Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

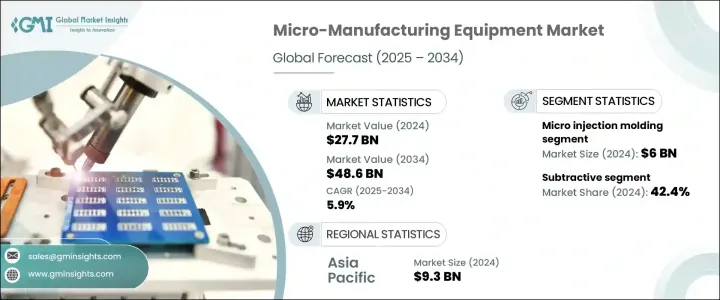

2024年,全球微製造設備市場規模達277億美元,預計2034年將以5.9%的複合年成長率成長,達到486億美元。這一成長主要源自於微型化技術的快速創新以及各行各業對高精度零件日益成長的需求。電子、汽車和醫療保健等行業對微尺度零件的需求強勁,即使是最小的偏差也會影響其整體性能。這些先進的應用需要具備卓越精度和可靠性的製造工具,從而推動了專業微製造系統在全球範圍內的快速普及。

儘管機會日益增多,但高昂的初始資本投入仍然是該市場面臨的一大障礙。購置微型製造設備(例如微型數控工具機、雷射微加工系統、精密測量工具和微型注塑機)通常每台設備的成本高達數十萬甚至數百萬美元。這些投資不僅限於設備本身,通常還包括先進的軟體、設施升級(例如無塵室或隔振系統)以及長期維護。這使得擁有成本相當高昂,尤其對於中小型企業而言。操作員培訓、零件品質驗證和定期維護等額外費用進一步挑戰了可擴展性,尤其是在早期階段。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 277億美元 |

| 預測值 | 486億美元 |

| 複合年成長率 | 5.9% |

2024年,微注塑成型市場規模達60億美元。這項技術對於製造精細且尺寸精確的零件至關重要,精度通常在微米級。它尤其適用於生產對精度要求極高的複雜組件。成型製程包括在嚴格控制的溫度和壓力條件下將熔融的聚合物注入精密的模具中。冷卻後,透過手動或自動化取出最終產品,以確保大量生產的一致性和可重複性。

減材製造流程領域在2024年佔了42.4%的市場。該領域包括微鑽、微銑削、微車削和電火花加工等材料去除技術,這些技術常用於製造精細的零件。微銑削透過使用超小型刀具逐步切削材料,可以實現複雜的形狀和光滑的表面光潔度。微車削是另一種重要的減材製造方法,它透過旋轉工件來加工圓柱形零件。這些技術對於生產電子、航太和汽車產業的零件至關重要,因為這些產業的尺寸精度至關重要。

2024年,亞太地區微製造設備市場規模達93億美元,佔33%的市佔率。這得益於強勁的工業擴張以及電子、航太、汽車和醫療設備等行業對精密製造日益成長的需求。日本、印度、中國和韓國等國家透過採用尖端微製造技術發揮關鍵作用。先進的微加工技術(包括微電火花加工、微銑削和雷射加工製程)的應用具有顯著的吸引力。這種轉變與半導體、感測器和植入物等應用領域對高性能微元件日益成長的需求密切相關。

塑造微製造設備市場競爭格局的關鍵公司包括 ARBURG GmbH + Co KG、FANUC、Oxford Instruments、Raith GmbH、ASML、Nanoscribe GmbH、Coherent Corp、日立高科技株式會社、住友(SHI)德馬格、應用材料、SUSS MicroTec、光電機械生產公司股庫法社、公司會股份公司。為了擴大市場地位,領導企業專注於策略性技術整合,例如自動化、人工智慧驅動的流程最佳化和混合製造技術。公司投資研發,以開發能夠在苛刻條件下進行高精度工作的緊湊、節能的機器。許多公司正在與終端行業建立合作,共同開發特定應用的解決方案,從而縮短產品上市時間並提高客製化程度。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 影響價值鏈的因素

- 利潤率分析

- 中斷

- 未來展望

- 製造商

- 經銷商

- 川普政府關稅分析

- 對貿易的影響

- 貿易量中斷

- 報復措施

- 對產業的影響

- 供應方影響(原料)

- 主要材料價格波動

- 供應鏈重組

- 生產成本影響

- 需求面影響(售價)

- 價格傳導至終端市場

- 市佔率動態

- 消費者反應模式

- 受影響的主要公司

- 策略產業反應

- 供應鏈重組

- 定價和產品策略

- 政策參與

- 展望與未來考慮

- 對貿易的影響

- 衝擊力

- 成長動力

- 製造技術的進步

- 工業自動化與智慧製造

- 蓬勃發展的醫療保健產業

- 小型電子設備需求不斷成長

- 產業陷阱與挑戰

- 初始投資高

- 材料限制

- 成長動力

- 成長潛力分析

- 技術概述

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 產業結構與集中度

- 競爭強度評估

- 公司市佔率分析

- 競爭定位矩陣

- 產品定位

- 性價比定位

- 地理分佈

- 創新能力

- 戰略儀表板

- Competitive benchmarking

- Strategic initiatives assessment

- SWOT analysis of key players

- Future competitive outlook

第5章:市場估計與預測:依類型,2021-2034

- 主要趨勢

- 微注塑成型

- 微切割

- 微加工

- 積層製造

- 其他

第6章:市場估計與預測:依製程類型,2021-2034 年

- 主要趨勢

- 添加劑

- 減法

- 其他

第7章:市場估計與預測:按應用,2021-2034

- 主要趨勢

- 汽車

- 半導體和電子

- 航太和國防

- 醫療的

- 電力和能源

- 其他

第8章:市場估計與預測:按配銷通路,2021-2034 年

- 主要趨勢

- 直銷

- 間接銷售

第9章:市場估計與預測:按地區,2021-2034

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- MEA

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

第10章:公司簡介

- Applied Materials

- ARBURG GmbH + Co KG

- ASML

- Coherent Corp

- FANUC

- Hikari Kikai Seisakusho Co Ltd

- Hitachi High-Tech Corporation

- KUKA AG

- Matsuura Machinery

- Nanoscribe GmbH

- Oxford Instruments

- Posalux

- Raith GmbH

- Sumitomo (SHI) Demag

- SUSS MicroTec

The Global Micro-Manufacturing Equipment Market was valued at USD 27.7 billion in 2024 and is estimated to grow at a CAGR of 5.9% to reach USD 48.6 billion by 2034. The growth is driven by rapid innovations in miniaturization and the growing need for high-precision components across a range of sectors. Industries such as electronics, automotive, and healthcare drive strong demand for micro-scale parts, where even the smallest variation can impact overall performance. These advanced applications require manufacturing tools that offer unmatched precision and reliability, contributing to the rapid uptake of specialized micro-manufacturing systems across the globe.

Despite the growing opportunities, high initial capital investment remains a major hurdle in this market. Acquiring micro-manufacturing equipment such as micro-CNC machines, laser micromachining systems, precision measurement tools, and micro injection molding units often runs into hundreds of thousands or even millions of dollars per unit. These investments go beyond just the equipment, they typically involve advanced software, facility upgrades such as cleanrooms or vibration isolation systems, and long-term maintenance. This makes the cost of ownership quite steep, especially for small to mid-sized enterprises. Additional expenses for operator training, part quality validation, and recurring maintenance further challenge scalability, especially in the early stages.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $27.7 Billion |

| Forecast Value | $48.6 billion |

| CAGR | 5.9% |

Micro injection molding segment generated USD 6 billion in 2024. This technology is essential for creating highly detailed and dimensionally accurate parts, often in the micrometer range. It is particularly suited for producing complex assemblies where high precision is critical. The molding process involves injecting molten polymers into precise molds under tightly controlled temperature and pressure conditions. Once cooled, the final product is removed, either manually or via automation, to ensure consistency and repeatability in mass production.

The subtractive manufacturing processes segment held a 42.4% share in 2024. This segment includes material-removal techniques like micro-drilling, micro-milling, micro-turning, and electrical discharge machining, which are frequently used to manufacture finely detailed components. Micro-milling allows for intricate shapes and smooth surface finishes by progressively cutting material with ultra-small tools. Micro-turning, another key subtractive method, rotates the workpiece to shape cylindrical parts. These techniques are vital in producing components used in electronics, aerospace, and automotive sectors, where dimensional accuracy is paramount.

Asia Pacific Micro-Manufacturing Equipment Market generated USD 9.3 billion holding a 33% share in 2024 driven by the robust industrial expansion and rising demand for precise manufacturing across sectors like electronics, aerospace, automotive, and medical devices. Countries such as Japan, India, China, and South Korea play a pivotal role by adopting cutting-edge micromanufacturing techniques. There is significant traction in the use of advanced micromachining technologies, including micro-EDM, micro-milling, and laser-based processes. This shift is closely tied to the rising demand for high-performance microcomponents in applications such as semiconductors, sensors, and implants.

Key companies shaping the competitive landscape of the Micro-Manufacturing Equipment Market include ARBURG GmbH + Co KG, FANUC, Oxford Instruments, Raith GmbH, ASML, Nanoscribe GmbH, Coherent Corp, Hitachi High-Tech Corporation, Sumitomo (SHI) Demag, Applied Materials, SUSS MicroTec, Hikari Kikai Seisakusho Co Ltd, Matsuura Machinery, KUKA AG, and Posalux. To expand their market position, leading players focus on strategic technology integrations such as automation, AI-driven process optimization, and hybrid manufacturing techniques. Companies invest in R&D to develop compact, energy-efficient machines capable of high-precision work under demanding conditions. Many are forging collaborations with end-use industries to co-develop application-specific solutions, reducing time-to-market and improving customization.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.4.2.1 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factors affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.2 Price volatility in key materials

- 3.2.2.3 Supply chain restructuring

- 3.2.2.4 Production cost implications

- 3.2.2.5 Demand-side impact (selling price)

- 3.2.2.6 Price transmission to end markets

- 3.2.2.7 Market share dynamics

- 3.2.2.8 Consumer response patterns

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Advancements in Manufacturing Technologies

- 3.3.1.2 Industrial Automation & Smart Manufacturing

- 3.3.1.3 Booming Medical and Healthcare Industry

- 3.3.1.4 Rising Demand for Miniaturized Electronic Devices

- 3.3.2 Industry pitfalls & challenges

- 3.3.2.1 High Initial Investment

- 3.3.2.2 Material Limitations

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Technological overview

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Industry structure and concentration

- 4.3 Competitive intensity assessment

- 4.4 Company market share analysis

- 4.5 Competitive positioning matrix

- 4.5.1 Product positioning

- 4.5.2 Price-performance positioning

- 4.5.3 Geographic presence

- 4.5.4 Innovation capabilities

- 4.6 Strategic dashboard

- 4.6.1 Competitive benchmarking

- 4.6.1.1 Manufacturing capabilities

- 4.6.1.2 Product portfolio strength

- 4.6.1.3 Distribution network

- 4.6.1.4 R&D investments

- 4.6.2 Strategic initiatives assessment

- 4.6.3 SWOT analysis of key players

- 4.6.4 Future competitive outlook

- 4.6.1 Competitive benchmarking

Chapter 5 Market Estimates & Forecast, By Type, 2021-2034 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Micro injection molding

- 5.3 Micro-cutting

- 5.4 Micromachining

- 5.5 Additive manufacturing

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Process Type, 2021-2034 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Additive

- 6.3 Subtractive

- 6.4 Others

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Automotive

- 7.3 Semiconductor and Electronics

- 7.4 Aerospace and Defense

- 7.5 Medical

- 7.6 Power and Energy

- 7.7 Others

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Direct sales

- 8.3 Indirect sales

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Applied Materials

- 10.2 ARBURG GmbH + Co KG

- 10.3 ASML

- 10.4 Coherent Corp

- 10.5 FANUC

- 10.6 Hikari Kikai Seisakusho Co Ltd

- 10.7 Hitachi High-Tech Corporation

- 10.8 KUKA AG

- 10.9 Matsuura Machinery

- 10.10 Nanoscribe GmbH

- 10.11 Oxford Instruments

- 10.12 Posalux

- 10.13 Raith GmbH

- 10.14 Sumitomo (SHI) Demag

- 10.15 SUSS MicroTec

奈米機電系統市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

奈米機電系統市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測 2025年MEMS(電子機械系統)全球市場報告2025年電子機械系統(MEMS)振盪器全球市場報告2025年電子機械(MEM)系統揚聲器全球市場報告

2025年MEMS(電子機械系統)全球市場報告2025年電子機械系統(MEMS)振盪器全球市場報告2025年電子機械(MEM)系統揚聲器全球市場報告 電子機械系統市場(按設備類型、製造材料、最終用戶和分銷管道)—2025-2030 年全球預測全球行動裝置MEMS市場

電子機械系統市場(按設備類型、製造材料、最終用戶和分銷管道)—2025-2030 年全球預測全球行動裝置MEMS市場 全球電子機械系統 (MEMS) 市場(至 2030 年)按感測器類型(慣性感測器、壓力感測器、環境感測器、光學感測器)、致動器類型(光學、微流體、噴墨頭、高頻)、產業和地區分類電子機械系統 (MEMS) 振盪器全球市場機會與策略(至 2034 年)

全球電子機械系統 (MEMS) 市場(至 2030 年)按感測器類型(慣性感測器、壓力感測器、環境感測器、光學感測器)、致動器類型(光學、微流體、噴墨頭、高頻)、產業和地區分類電子機械系統 (MEMS) 振盪器全球市場機會與策略(至 2034 年) MEMS:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)電子機械系統市場:2034 年的機會與策略

MEMS:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)電子機械系統市場:2034 年的機會與策略