|

市場調查報告書

商品編碼

1850357

人力資本管理軟體:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)Human Capital Management Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

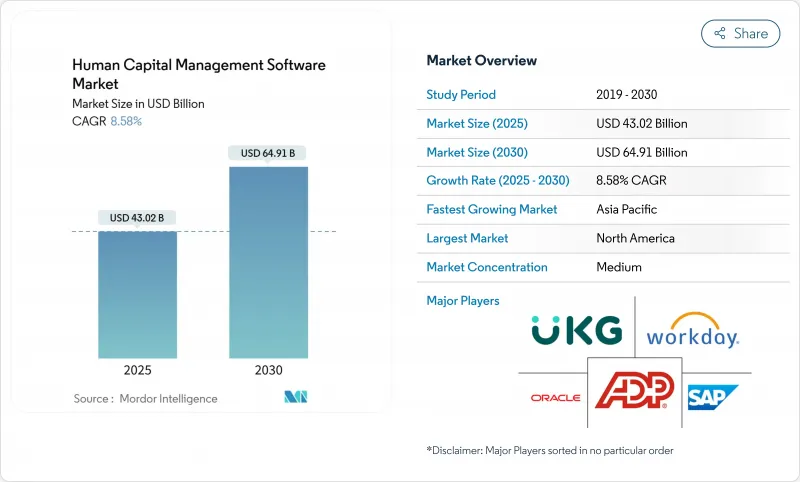

預計到 2025 年,人力資本管理軟體市場規模將達到 430.2 億美元,到 2030 年將達到 649.1 億美元,年複合成長率為 8.6%。

雲端遷移、嵌入式人工智慧和運作全球合規自動化正在再形成採購週期的每個階段,從招標書設計到合約續簽,沒有例外。董事會現在將整合式雲端原生人力資源套件視為重要的風險緩解工具,這些套件能夠自動處理薪酬公平性調整、稅務變更和隱私義務,同時提供即時勞動力分析,從而提高生產力和員工留存率。中小企業正在加速採用這些方案,因為基於訂閱的部署方式消除了傳統本地部署人力資源系統所需的資本成本和IT人員配置。能夠提供通用資料模型、行動優先工作流程和透明人工智慧管道的供應商正在獲得不成比例的市場佔有率,而那些仍然固守傳統架構的後起之秀則正在失去續約機會。超過三分之一的北美擴張交易將機器學習主導的目標設定、流失風險評分和技能匹配作為預設權益捆綁在一起,這表明人工智慧不再是可選項,而是基本要求。

全球人力資本管理軟體市場趨勢與洞察

向雲端原生HCM平台的轉變

雲端遷移已從硬體更新升級到董事會層級的強制性要求。超過90%的人力資源主管計劃為雲端分析和自動化更新合規引擎分配或增加預算。即時推播稅表和特定司法管轄區的薪資平等規則只需一行程式碼即可實現,從而消除季度補丁積壓。然而,只有22%的雇主表示他們已做好充分準備來利用這些功能,這造成了執行上的差距,而實施合作夥伴和專業服務團隊正努力從中收益。中階市場買家佔據了新客戶數量的主導地位,因為他們無需維護資料中心即可獲得企業級分析功能,而大型企業現在正在發布分階段遷移的RFP,這些RFP採用容器化微服務,同時保留原有的自訂邏輯。在人力資本管理軟體市場,所有供應商都將解決長期存在的安全問題放在藍圖的核心位置,提供多租戶擴展、自主雲端選項和零停機升級服務。

整合式人力資源和薪資核算系統越來越受歡迎

使用獨立的人才或薪資名冊引擎會導致成本高昂的資料核對和不準確的分析。目前,85% 的雇主至少授權合約了兩款付費人力資源產品,並在商業條件允許的情況下進行整合。在亞太地區,快速成長的公司在其第一階段數位化中就採用了整合套件,從而避免了技術債務,並超越了西方國家的採用曲線。融合還能帶來更豐富的洞見。薪資數據可以即時反映預算限制,人才模組可以揭示技能差距,並實現與學習成果相關的演算法薪酬提案。投資於涵蓋薪酬、技能、資格和績效的統一對像模型的供應商,其表現優於那些拼湊收購代碼庫的同行,這一趨勢也體現在人力資本管理軟體市場的續訂價格中。

網路安全和資料隱私問題

GDPR、CCPA、CPRA 和巴西的 LGPD 對資料保留、居住和員工同意施加了嚴格的限制。包含銀行詳細資訊、社保號碼和績效考核記錄的人力資源資料庫是撞人員編制攻擊的主要目標。因此,買家將 ISO 27001 認證、零信任網路設計和持續滲透測試作為優先選擇標準。新的挑戰在於如何證明個人識別資訊在傳輸和儲存過程中均已加密,同時還要保持分析效能。供應商正在透過記憶體內標記化和基於屬性的存取控制來應對這些挑戰,但這些改進會延長部署時間並增加整體擁有成本,從而限制人力資本管理軟體市場的成長。

細分市場分析

薪資核算仍是人力資源技術的核心支柱,預計到2024年將佔人力資本管理軟體市場收入的38.0%。其重要性源於法律要求企業必須準確、及時地支付員工薪資,這意味著外包造成的任何延誤都是不可接受的。然而,到2030年,學習與發展領域的複合年成長率將達到9.5%。面臨技能短缺的管理者更傾向於提升內部人才的技能,以避免不斷上漲的招募成本和長期職缺。將學習目錄、認證追蹤和導師制工作流程與薪資核算整合到同一平台,可以創建一個閉迴路回饋機制:人工智慧可以將微證書的取得與封閉式連結起來,在提高員工敬業度的同時,滿足薪資公平性報告的要求。

人才和人力資源管理、薪資核算和學習管理等模組的需求仍然強勁,這主要源自於雇主希望獲得統一的績效數據,以輔助排班、加班核准和提高薪資。核心人力資源管理仍然是必備模組,但除非與增值分析功能捆綁,否則很少會影響供應商的選擇。在不斷發展的人力資本管理軟體市場中,供應商正在整合課程市場、技能本體和內部零工市場模組,將學習從一項合規義務提升為策略生產力引擎。隨著客戶將預算轉向以結果為導向的應用,未能調整策略的供應商將面臨市場佔有率下降的困境。

到2024年,本地部署仍將佔總收入的68.4%,這是十年前ERP決策遺留下來的產物。許多公共部門和受嚴格監管的客戶由於資料主權條款和複雜的整合問題而抵制遷移。然而,雲端採用率正以10.1%的複合年成長率成長,推動人力資本管理軟體市場邁入訂閱模式時代。買家看重的是,他們能夠將資本支出轉化為可觀的收益,同時還能獲得季度功能更新和安全補丁,且無需停機。如今的合約還包括亞小時級的合規性推送和即時分析沙箱,這些都是靜態本地部署架構所無法提供的優勢。

我們也看到混合模式的出現,個人資訊和薪資核算運行在私有雲端上,而前端分析則運行在超大規模執行個體上。提供容器化服務和基礎設施即程式碼藍圖的供應商正在獲得市場預算,以緩解用戶的遷移焦慮。最終,我們預計會出現曲折點,屆時人工智慧的快速發展將迫使即使是較為保守的行業也重新評估其本地部署資產,從而進一步推動人力資本管理軟體市場向雲端傾斜。

人力資本管理軟體市場報告按解決方案類型(薪資管理、人才管理、勞動力管理等)、部署類型(本地部署、雲端部署)、組織規模(大型企業、中小企業)、垂直行業(IT 和通訊、銀行、金融服務和保險等)和地區進行細分。

區域分析

2024年,北美將佔人力資本管理軟體市場收入的43.1%。長期以來對SaaS的熟悉、強大的創業投資資金以及完善的實施合作夥伴生態系統正在推動升級週期。薪酬公平立法正在加速報告模組的普及。僅加州就強制要求按性別和種族類別披露工資中位數,獎勵即時分析。供應商正透過人工智慧驅動的可解釋性和工作流程擴充性來脫穎而出。儘管轉換成本仍然很高,但承諾提供消費級行動用戶體驗和透明定價的新興參與企業正在快速擴張員工隊伍的新創公司中找到立足之地。

德國、法國和北歐國家各自製定了不同的職工委員會工作流程。 GDPR 推動了嚴格的資料主權審查,許多買家要求資料中心設在本國境內。敏感的人事檔案保存在當地,機器學習工作負載運行在歐盟認證的公共雲端上。永續性認證和對負責任人工智慧的承諾正日益影響採購決策,供應商強調其節能資料中心和偏差緩解框架,以期在競標評分中獲得通過。

亞太地區是成長最快的區域,複合年成長率高達9.6%。從印度到印尼,各國政府都在津貼中小企業的數位化,推動了第一代薪資核算和時間管理軟體的採購。行動優先功能十分普遍,滿足了外勤員工的需求。區域供應商透過整合法定申報、電子錢包支付和本地語言聊天機器人支援等功能取得了成功,但他們也經常與全球套件供應商合作,以獲得更高級的分析功能。跨國公司正在尋求在中國、日本和東南亞地區實現流程統一,這促使供應商擴展語言包和本地稅務內容。在人力資本管理軟體市場,該地區呈現層級構造:掌握監管細微差別的本地領導企業和提供人工智慧強大分析功能的全球巨頭。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 遷移到雲端原生 HCM 平台

- 整合的人力資源和薪資核算系統正變得越來越普遍。

- 人才分析與人工智慧在策略性人力資源管理的應用

- 全球薪資核算和稅務合規義務

- 薪酬公平法推動薪酬工具的發展

- 無固定辦公人員及零工人員的行動優先型人力資本管理

- 市場限制

- 網路安全和資料隱私問題

- 傳統系統遷移的成本與複雜性

- 複雜套件的最終用戶接受度較低。

- 人工智慧偏見訴訟風險限制了其部署

- 價值鏈分析

- 技術展望

- 波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

- 評估宏觀經濟趨勢對市場的影響

第5章 市場規模與成長預測

- 透過解決方案

- 薪資管理

- 人才管理

- 人力資源管理

- 核心人力資源管理

- 學習與發展

- 透過部署

- 本地部署

- 雲

- 按組織規模

- 主要企業

- 小型企業

- 按行業

- 資訊科技和通訊

- BFSI

- 製造業

- 衛生保健

- 零售與電子商務

- 政府和公共部門

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- ASEAN

- 澳洲和紐西蘭

- 其他亞太地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略舉措與發展

- 市佔率分析

- 公司簡介

- SAP SE

- Oracle Corporation

- Workday Inc.

- ADP LLC

- Ceridian HCM Holding Inc.

- UKG(Ultimate Kronos Group)

- Infor

- Cornerstone OnDemand Inc.

- IBM Corporation

- Ramco Systems

- BambooHR LLC

- Zoho Corporation(Zoho People)

- Namely Inc.

- Gusto Inc.

- Paycom Software Inc.

- Sage Group plc

- Epicor Software Corporation

- SumTotal Systems LLC

- PeopleFluent Inc.

- Meta4(Cegid)

- Talentia Software

- OrangeHRM Inc.

- Rippling

- Deel Inc.

第7章 市場機會與未來展望

The human capital management software market size is valued at USD 43.02 billion in 2025 and is projected to reach USD 64.91 billion by 2030, expanding at an 8.6% CAGR.

Cloud migration, embedded artificial intelligence, and always-on global compliance automation are the structural forces reshaping every stage of the purchase cycle, from RFP design to contract renewal. Boards now view integrated, cloud-native HR suites as essential risk-mitigation tools that automate pay-equity adjustments, tax changes, and privacy obligations, while simultaneously delivering real-time workforce analytics that lift productivity and retention. Small and medium enterprises are accelerating adoption because subscription-based deployments eliminate the capital costs and IT headcount traditionally associated with on-premise HRIS, creating a two-speed environment inside the human capital management software market where SME agility meets large-enterprise complexity. Vendors that can deliver universal data models, mobile-first workflows, and transparent AI pipelines are capturing a disproportionate share, whereas laggards tethered to legacy architectures are losing renewals. Over one-third of North American expansion deals already bundle machine-learning-driven goal-setting, attrition risk scoring, and skills matching as default entitlements, signaling that AI is no longer an optional add-on but a baseline requirement.

Global Human Capital Management Software Market Trends and Insights

Shift to Cloud-Native HCM Platforms

Cloud migration has progressed from hardware refresh to board-level mandate. Over 90% of HR leaders plan to protect or increase budgets specifically to unlock cloud analytics and auto-updated compliance engines. Real-time tax table pushes and jurisdiction-specific pay-equity rules arrive inside a single code line, eliminating quarterly patch backlogs. Yet only 22% of employers report full readiness to harness those capabilities, leaving an execution gap that implementation partners and professional-services teams are keen to monetize. Mid-market buyers dominate new-logo counts because they gain enterprise-class analytics without maintaining data centers, but large enterprises are now issuing phased migration RFPs that preserve prior custom logic while adopting containerized microservices. Within the human capital management software market, every provider's roadmap now centers on delivering multi-tenant scale, sovereign-cloud options, and zero-downtime upgrades to neutralize lingering security objections.

Integrated Talent and Payroll Suites Gain Traction

Stand-alone talent or payroll engines create costly data reconciliations that impede analytics accuracy. Eighty-five percent of employers currently license at least two paid HR products and are consolidating wherever commercial terms allow. In Asia-Pacific, fast-growing organizations deploy unified suites during first-generation digitization, avoiding technical debt and leapfrogging Western adoption curves. Convergence also unlocks richer insights: payroll data surfaces real-time budget constraints, while talent modules expose skills gaps, enabling algorithmic compensation recommendations linked to learning achievements. Vendors that invest in a unified object model-covering wages, skills, credentials, and performance-outperform peers still stitching together acquired codebases, a dynamic increasingly visible in renewal pricing inside the human capital management software market.

Cyber-Security and Data-Privacy Concerns

GDPR, CCPA, CPRA, and Brazil's LGPD impose strict constraints on data retention, residency, and employee consent. HR databases contain bank details, social-security numbers, and performance notes-prime targets for credential-stuffing attacks. Buyers, therefore, elevate ISO 27001 certification, zero-trust network designs, and continuous penetration testing to top selection criteria. The new hurdle is proving encryption of personally identifiable information both in transit and at rest while maintaining analytics performance. Vendors are responding with in-memory tokenization and attribute-based access controls, but those enhancements lengthen rollout timelines and raise total cost of ownership, tempering growth inside the human capital management software market.

Other drivers and restraints analyzed in the detailed report include:

- Workforce Analytics and AI for Strategic HR

- Compliance Mandates for Global Payroll and Taxation

- Legacy Migration Cost and Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Payroll remains the backbone of HR technology, accounting for 38.0% of 2024 revenue in the human capital management software market. Its criticality stems from legal requirements to pay employees accurately and on time, leaving little room for outsourcing delays. However, Learning and Development is advancing at a 9.5% CAGR toward 2030. Executives battling skill shortages prefer upskilling internal talent to avoid escalating recruiting costs and protracted vacancy periods. Incorporating learning catalogues, credential tracking, and mentorship workflows into the same platform that runs payroll unlocks a closed feedback loop: AI can correlate micro-credential completion with wage progression, boosting engagement while satisfying pay-equity reporting.

Beyond payroll and learning, demand for talent-management and workforce-management cubes remains steady, driven by employers seeking unified performance data that informs scheduling, overtime approval, and compensation bumps. Core HR Administration persists as a table-stakes module but rarely influences vendor selection unless bundled with value-add analytics. In the evolving human capital management software market, providers are embedding course marketplaces, skills ontologies, and internal gig-market modules to elevate learning from a compliance obligation to a strategic productivity engine. Those failing to retool will see wallet share erode as clients shift budget toward outcome-oriented applications.

On-premise still controls 68.4% of revenue in 2024, a legacy of decade-old ERP decisions. Many public-sector and highly regulated customers resist migration because of data-sovereignty clauses and integration tangles. Yet cloud implementations are climbing at a 10.1% CAGR, propelling the human capital management software market into a subscription-first era. Buyers appreciate converting capex to opex while gaining quarterly feature drops and security patches without downtime. Contracts now bundle sub-hour compliance pushes and real-time analytics sandboxes, benefits unattainable in static on-premise stacks.

A hybrid pattern is emerging: personal information and payroll calculations often remain on private or sovereign clouds, whereas front-end analytics run on hyperscaler instances for elasticity. Vendors offering containerized services and infrastructure-as-code blueprints capture implementation budgets because they reduce migration anxiety. Eventually, an inflection point will arise where artificial-intelligence feature velocity compels even conservative sectors to re-evaluate on-premise holdings, further tipping the human capital management software market toward cloud dominance.

The Human Capital Management Software Market Report is Segmented by Solution (Payroll Management, Talent Management, Workforce Management, and More), Deployment (On-Premise and Cloud), Organization Size (Large Enterprises and Small and Medium Enterprises), Industry Vertical (IT and Telecom, BFSI, and More), and Geography.

Geography Analysis

North America controls 43.1% of 2024 revenue inside the human capital management software market. Longstanding SaaS familiarity, strong venture funding, and dense implementation-partner ecosystems fuel upgrade cycles. Pay-equity legislation accelerates reporting module adoption; California alone mandates median-pay disclosure across gender and race categories, incentivizing real-time analytics. Vendors differentiate on AI explainability and workflow extensibility because functionality parity exists across payroll, benefits, and learning. Switching costs remain high, yet new entrants that promise consumer-grade mobile UX and transparent pricing still find footholds among venture-backed firms scaling headcount rapidly.

Europe presents a mosaic of labor codes; Germany, France, and the Nordics each impose unique works-council consultation workflows. GDPR drives strict data-sovereignty reviews; many buyers demand data centers within national borders. Hybrid deployments lead: sensitive HR files stay local, while machine-learning workloads run on EU-accredited public clouds. Sustainability credentials and responsible-AI commitments increasingly influence procurement; vendors highlight energy-efficient data centers and bias-mitigation frameworks to pass tender scoring.

Asia-Pacific is the fastest-growing region at 9.6% CAGR. Governments from India to Indonesia subsidize SME digitization, driving first-generation payroll and attendance purchases. Mobile-first features dominate, catering to field-based workforces. Regional providers thrive by integrating statutory returns, e-wallet disbursements, and chatbot support in local languages, yet often partner with global suites for advanced analytics. Multinational corporations seek unified processes across China, Japan, and Southeast Asia, pushing vendors to expand language packs and in-country tax content. Within the human capital management software market, this region showcases a two-tier structure: local champions owning regulatory nuance and global giants supplying AI-rich analytics.

- SAP SE

- Oracle Corporation

- Workday Inc.

- ADP LLC

- Ceridian HCM Holding Inc.

- UKG (Ultimate Kronos Group)

- Infor

- Cornerstone OnDemand Inc.

- IBM Corporation

- Ramco Systems

- BambooHR LLC

- Zoho Corporation (Zoho People)

- Namely Inc.

- Gusto Inc.

- Paycom Software Inc.

- Sage Group plc

- Epicor Software Corporation

- SumTotal Systems LLC

- PeopleFluent Inc.

- Meta4 (Cegid)

- Talentia Software

- OrangeHRM Inc.

- Rippling

- Deel Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shift to cloud-native HCM platforms

- 4.2.2 Integrated talent and payroll suites gain traction

- 4.2.3 Workforce analytics and AI for strategic HR

- 4.2.4 Compliance mandates for global payroll and taxation

- 4.2.5 Pay-equity legislation spurs compensation tools

- 4.2.6 Mobile-first HCM for deskless and gig workforce

- 4.3 Market Restraints

- 4.3.1 Cyber-security and data-privacy concerns

- 4.3.2 Legacy migration cost and complexity

- 4.3.3 Low end-user adoption of complex suites

- 4.3.4 AI bias litigation risk restricts roll-outs

- 4.4 Value Chain Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Assessment of the Impact of Macroeconomic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Solution

- 5.1.1 Payroll Management

- 5.1.2 Talent Management

- 5.1.3 Workforce Management

- 5.1.4 Core HR Administration

- 5.1.5 Learning and Development

- 5.2 By Deployment

- 5.2.1 On-Premise

- 5.2.2 Cloud

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By Industry Vertical

- 5.4.1 IT and Telecom

- 5.4.2 BFSI

- 5.4.3 Manufacturing

- 5.4.4 Healthcare

- 5.4.5 Retail and E-Commerce

- 5.4.6 Government and Public Sector

- 5.4.7 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 ASEAN

- 5.5.3.6 Australia and New Zealand

- 5.5.3.7 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 UAE

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves and Developments

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Oracle Corporation

- 6.4.3 Workday Inc.

- 6.4.4 ADP LLC

- 6.4.5 Ceridian HCM Holding Inc.

- 6.4.6 UKG (Ultimate Kronos Group)

- 6.4.7 Infor

- 6.4.8 Cornerstone OnDemand Inc.

- 6.4.9 IBM Corporation

- 6.4.10 Ramco Systems

- 6.4.11 BambooHR LLC

- 6.4.12 Zoho Corporation (Zoho People)

- 6.4.13 Namely Inc.

- 6.4.14 Gusto Inc.

- 6.4.15 Paycom Software Inc.

- 6.4.16 Sage Group plc

- 6.4.17 Epicor Software Corporation

- 6.4.18 SumTotal Systems LLC

- 6.4.19 PeopleFluent Inc.

- 6.4.20 Meta4 (Cegid)

- 6.4.21 Talentia Software

- 6.4.22 OrangeHRM Inc.

- 6.4.23 Rippling

- 6.4.24 Deel Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

2026年全球人力資本管理軟體市場報告2026年全球人才管理軟體市場報告2026年全球目標與關鍵成果(OKR)軟體市場報告

2026年全球人力資本管理軟體市場報告2026年全球人才管理軟體市場報告2026年全球目標與關鍵成果(OKR)軟體市場報告 2026-2030年全球人力資源管理軟體市場

2026-2030年全球人力資源管理軟體市場 人力資源管理軟體市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、模組及功能分類

人力資源管理軟體市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、模組及功能分類 亞太地區人力資本管理軟體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

亞太地區人力資本管理軟體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 全球人力資源管理軟體市場規模、佔有率、趨勢和成長分析報告(2026-2034年)人才管理軟體市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察與預測(2026-2034)

全球人力資源管理軟體市場規模、佔有率、趨勢和成長分析報告(2026-2034年)人才管理軟體市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察與預測(2026-2034) 人力資本管理軟體市場報告:按組件、部署類型、最終用戶、垂直行業和地區分類,2026-2034 年

人力資本管理軟體市場報告:按組件、部署類型、最終用戶、垂直行業和地區分類,2026-2034 年 人力資本管理軟體市場-全球產業規模、佔有率、趨勢、機會和預測:按部署模式、組織規模、產業、服務、軟體、地區和競爭對手分類,2021-2031年

人力資本管理軟體市場-全球產業規模、佔有率、趨勢、機會和預測:按部署模式、組織規模、產業、服務、軟體、地區和競爭對手分類,2021-2031年