|

市場調查報告書

商品編碼

1850327

產品資訊管理(PIM):市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)Product Information Management (PIM) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

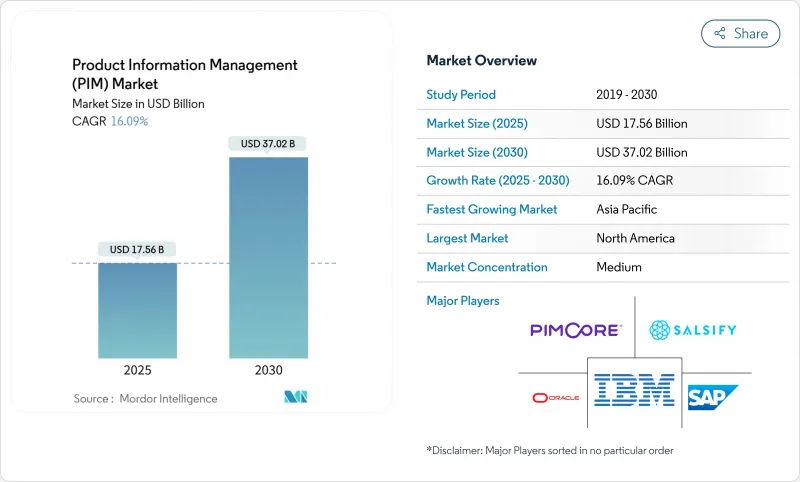

預計到 2025 年,產品資訊管理市場價值將達到 175.6 億美元,預計到 2030 年將達到 370.2 億美元,年複合成長率為 16.09%。

產品資訊管理 (PIM) 日益被視為數位商務的基石,這得益於人工智慧驅動的內容生成和全通路體驗的迫切需求。企業正迅速轉向雲端訂閱模式,以降低整體擁有成本、加速產品推出並確保功能自動更新。零售商、製造商和串流媒體平台如今產生大量複雜的產品數據,促使他們投資於集中式系統,以維護網站、市場、門市和社群媒體等各個管道的數據一致性。諸如計劃於 2026 年實施的歐盟數位產品護照等監管舉措,加劇了合規壓力;而生成式人工智慧工具則提升了 PIM 在快速內容在地化和搜尋引擎最佳化 (SEO) 方面的戰略價值。

全球產品資訊管理 (PIM) 市場趨勢與洞察

電子商務的蓬勃發展和SKU的激增

如今的零售商在2020年需要管理的產品種類是之前的3倍,這給電子表格和傳統工具帶來了巨大壓力。集中式產品資訊管理(PIM)平台需要編配數百萬個屬性,以同步亞馬遜、沃爾瑪和本地市場平台上的產品資訊。季節性時尚系列需要數百種顏色和尺寸組合,並在15個以上的管道上保持一致的展示,而國際擴張則增加了語言在地化和監管標籤方面的負擔。

透過採用雲端運算降低總體擁有成本

遷移到雲端 PIM 系統,透過消除伺服器維護和提供自動升級,可將整體擁有成本降低 45-55%。系統可動態擴展以應對假日尖峰時段流量,而無需過度配置硬體。 SAP 報告稱,2025 年第一季雲端收入成長 27%,證實了企業對 SaaS 資料管理的需求。

網路安全與資料外洩問題

擁有專有配方和價格表的公司不願將敏感資料儲存在多租戶雲端環境中。在資料遷移過程中,資料外洩的風險會增加 40%,這促使製藥和金融公司轉向採用更嚴格加密和零信任存取控制的專用基礎設施。

細分市場分析

預計到2024年,雲端技術將佔產品資訊管理市場63.5%的佔有率,並在2030年之前以18.2%的複合年成長率成長。集中式SaaS平台消除了地理基礎設施的限制,並可自動更新人工智慧功能,而無需企業內部IT資源。本地部署在嚴格監管的領域仍佔有一席之地,但隨著合規框架採用認證的雲端架構,其市場佔有率正在萎縮。

在對系統彈性和全球可用性的需求驅動下,雲端仍然是綠地計畫的主要選擇。 SAP 的雲端收益飆升 27%,凸顯了客戶對訂閱模式的偏好,這種模式能夠提供可預測的成本和強大的服務等級協定 (SLA)。跨國零售商優先考慮 3-6 個月的較短部署週期,而不是 12 個月以上的周期,以便快速實現季節性商品的收益。

到2024年,解決方案將佔總收入的65.9%,但隨著越來越多的公司尋求整合、資料清洗和變更管理的幫助,服務收入將以17.5%的複合年成長率超過解決方案。企業級產品資訊管理(PIM)部署目前包括人工智慧模型調優、全通路分發以及數位產品護照的資料層,所有這些都需要專業技能。

隨著客戶不斷應對架構變更和內容豐富化,培訓和託管服務需求日益成長。諮詢合作夥伴指導客戶完成分類法設計、機器學習管道建置和KPI儀表板構建,確保客戶從核心軟體授權中獲得長期價值。

產品資訊管理市場按部署類型(雲端、本地部署)、交付類型(解決方案/服務)、組織規模(大型企業、中小企業)、最終用戶行業(零售/電子商務、銀行、金融服務和保險 (BFSI)、其他)和地區進行細分。市場預測以美元計價。

區域分析

北美地區以24.5%的市佔率領跑,預計2024年將維持穩定成長,這得益於各公司在成熟的產品資訊管理(PIM)基礎架構之上疊加人工智慧內容功能。美國零售商投資於與核心PIM直接關聯的數位化貨架分析,加拿大製造商為整個北美大陸的貿易數位化做好準備,而墨西哥汽車供應商則採用PIM以滿足美墨加協定(USMCA)的文件要求。

亞太地區是成長最快的地區,年複合成長率達 16.7%。中國製造商正在將 PIM 與 MES 和出口門戶網站整合,以滿足全球標籤要求;印度製藥和汽車出口商正在採用基於 SaaS 的 PIM 來實現多市場合規;日本公司正在將 PIM 擴展到支援物聯網的工廠,以支援自動化品質檢測系統;澳洲零售商正在利用雲端技術快速推出全通路推出。

在歐洲,計劃引入數位產品護照,允許進口商和生產商集中管理永續性和來源數據,這一舉措正引起強烈的需求:德國工業公司正在實施產品資訊管理 (PIM) 來管理多語言技術文件,英國出口商正在透過統一的目錄來處理脫歐後的文件工作,法國奢侈品牌正在使用產品資訊管理 (PIM) 來保持跨語言的品牌形象。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 電子商務的蓬勃發展和SKU的激增

- 透過雲端採用降低總體擁有成本

- 全通路客戶體驗勢在必行

- 符合歐盟數位產品護照要求

- 人工智慧賦能的產品內容管道

- 市場「快速商務」API要求

- 市場限制

- 網路安全與資料外洩問題

- 與傳統ERP系統整合的複雜性

- ESG數據審核成本不斷上升

- 具備產品資訊管理 (PIM) 技能的資料管理員短缺

- 供應鏈分析

- 監管格局

- 技術展望

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

- 評估市場中的宏觀經濟因素

第5章 市場規模與成長預測

- 按部署模式

- 雲

- 本地部署

- 報價

- 解決方案

- 服務

- 按組織規模

- 主要企業

- 小型企業

- 按最終用戶產業

- 零售與電子商務

- BFSI

- 製造業

- 媒體與娛樂

- 資訊科技和通訊

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲和紐西蘭

- 其他亞太地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 埃及

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介{包括全球概覽、市場層級概覽、核心業務板塊、財務資訊、策略資訊、主要企業的市場排名/佔有率、產品和服務、近期發展等。 }

- SAP SE

- IBM Corp.

- Oracle Corp.

- Pimcore GmbH

- Salsify Inc.

- Syndigo LLC

- Stibo Systems A/S

- inRiver AB

- Akeneo SAS

- Contentserv AG

- Bluestone PIM AS

- Precisely Holdings LLC

- Plytix Ltd.

- InsightSoftware LLC

- Riversand(Syndigo)

- Informatica LLC

- Pimberly Ltd.

- Adobe(Experience Manager Assets)

- Acquia Inc.

- Ergonode Sp. z oo

第7章 市場機會與未來展望

The product information management market size is estimated at USD 17.56 billion in 2025 and is forecast to reach USD 37.02 billion by 2030, advancing at a 16.09% CAGR.

Rising recognition of PIM as the digital-commerce backbone, combined with AI-powered content generation and omnichannel experience imperatives, underpins this expansion. Enterprises shift quickly to cloud subscription models to reduce total cost of ownership, speed product launches, and secure automatic feature updates. Retailers, manufacturers, and streaming platforms now generate vast volumes of complex product data, prompting investments in centralized systems that maintain consistency across websites, marketplaces, stores, and social media. Regulatory momentum-most notably the EU Digital Product Passport due in 2026-adds compliance pressure, while generative-AI tooling increases the strategic value of PIM for rapid content localization and SEO optimization.

Global Product Information Management (PIM) Market Trends and Insights

E-commerce boom and SKU proliferation

Retailers today handle triple the product variants managed in 2020, straining spreadsheets and legacy tools. Centralized PIM platforms now orchestrate millions of attributes to keep Amazon, Walmart, and regional marketplace listings synchronized. Seasonal fashion lines present hundreds of color-size combinations that must appear consistently across 15-plus channels, and international rollouts add the burden of language localization and regulatory labeling.

Cloud adoption lowering TCO

Migrating to cloud PIM trims 45-55% in ownership costs by eliminating server upkeep and delivering automatic upgrades. Dynamic scaling fits peak holiday traffic without over-provisioning hardware. For mid-market firms, subscription pricing removes large capital outlays, while SAP recorded 27% cloud revenue growth in Q1 2025, underscoring enterprise appetite for SaaS data management.

Cyber-security and data-breach concerns

Firms handling proprietary formulas or price books hesitate to place sensitive data in multitenant clouds. Breach risk spikes 40% during migration phases, pushing pharmaceuticals and finance toward dedicated infrastructure with stricter encryption and zero-trust access controls.

Other drivers and restraints analyzed in the detailed report include:

- Omnichannel customer-experience mandates

- Gen-AI-ready product-content pipelines

- Integration complexity with legacy ERPs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud installations accounted for 63.5% of the product information management market in 2024, and the segment is set to grow at 18.2% CAGR to 2030. Centralized SaaS platforms remove geographic infrastructure constraints and push automatic AI feature updates without internal IT resourcing. On-premise retains a foothold in highly regulated fields, yet its share inches downward as compliance frameworks now accept certified cloud architectures.

Demand for elasticity and global availability ensures cloud remains the primary route for greenfield projects. SAP's 27% cloud revenue spike highlights customer preference for subscription models that deliver predictable spend and robust SLAs. Multinational retailers cite faster rollouts-three to six months instead of 12-plus-as pivotal to monetizing seasonal assortments swiftly.

Solutions held 65.9% revenue in 2024, but Services will outpace at 17.5% CAGR as firms seek integration, data-cleansing, and change-management assistance. Enterprise PIM rollouts now include AI model tuning, omnichannel syndication, and Digital Product Passport data layers, all requiring specialist skills.

Training and managed-service contracts rise as clients grapple with ongoing schema changes and content enrichment. Consulting partners guide taxonomy design, machine-learning pipeline setup, and KPI dashboards, ensuring long-term value extraction from core software licenses.

Product Information Management Market is Segmented by Deployment Mode (Cloud, On-Premises), Offering (Solutions Services), Organization Size (Large Enterprises, Small and Medium Enterprises (SMEs)), End User Industry (Retail and E-Commerce, BFSI, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led with 24.5% share in 2024 and will maintain steady growth as enterprises layer AI content capabilities atop mature PIM foundations. United States retailers invest in digital shelf analytics that link directly into core PIM, and Canadian manufacturers prepare for continent-wide trade digitization. Mexico's automotive suppliers adopt PIM to meet USMCA documentation rules.

Asia-Pacific is the fastest-growing region at 16.7% CAGR. Chinese manufacturers integrate PIM with MES and export portals to satisfy global labeling mandates, while Indian pharma and auto exporters adopt SaaS PIM for multi-market compliance. Japanese firms extend PIM into IoT-enabled factories to feed automated quality-inspection systems, and Australian retailers leverage cloud deployments for rapid omnichannel launches.

Europe enjoys entrenched demand thanks to the upcoming Digital Product Passport, compelling every importer and producer to centralize sustainability and provenance data. German industrials deploy PIM for multilingual technical files, UK exporters tackle post-Brexit paperwork through unified catalogs, and French luxury houses rely on PIM to preserve brand voice across languages.

- SAP SE

- IBM Corp.

- Oracle Corp.

- Pimcore GmbH

- Salsify Inc.

- Syndigo LLC

- Stibo Systems A/S

- inRiver AB

- Akeneo SAS

- Contentserv AG

- Bluestone PIM AS

- Precisely Holdings LLC

- Plytix Ltd.

- InsightSoftware LLC

- Riversand (Syndigo)

- Informatica LLC

- Pimberly Ltd.

- Adobe (Experience Manager Assets)

- Acquia Inc.

- Ergonode Sp. z o.o.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-commerce boom and SKU proliferation

- 4.2.2 Cloud adoption lowering TCO

- 4.2.3 Omnichannel customer-experience mandates

- 4.2.4 EU Digital Product Passport compliance

- 4.2.5 Gen-AI-ready product-content pipelines

- 4.2.6 Marketplace "quick-commerce" API requirements

- 4.3 Market Restraints

- 4.3.1 Cyber-security and data-breach concerns

- 4.3.2 Integration complexity with legacy ERPs

- 4.3.3 Rising ESG data-audit costs

- 4.3.4 Shortage of PIM-skilled data stewards

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Degree of Competition

- 4.8 Assesment of Macroeconomic Factors on the market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Model

- 5.1.1 Cloud

- 5.1.2 On-premise

- 5.2 By Offering

- 5.2.1 Solutions

- 5.2.2 Services

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises (SMEs)

- 5.4 By End-user Industry

- 5.4.1 Retail and E-commerce

- 5.4.2 BFSI

- 5.4.3 Manufacturing

- 5.4.4 Media and Entertainment

- 5.4.5 IT and Telecom

- 5.4.6 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Egypt

- 5.5.5.2.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments}

- 6.4.1 SAP SE

- 6.4.2 IBM Corp.

- 6.4.3 Oracle Corp.

- 6.4.4 Pimcore GmbH

- 6.4.5 Salsify Inc.

- 6.4.6 Syndigo LLC

- 6.4.7 Stibo Systems A/S

- 6.4.8 inRiver AB

- 6.4.9 Akeneo SAS

- 6.4.10 Contentserv AG

- 6.4.11 Bluestone PIM AS

- 6.4.12 Precisely Holdings LLC

- 6.4.13 Plytix Ltd.

- 6.4.14 InsightSoftware LLC

- 6.4.15 Riversand (Syndigo)

- 6.4.16 Informatica LLC

- 6.4.17 Pimberly Ltd.

- 6.4.18 Adobe (Experience Manager Assets)

- 6.4.19 Acquia Inc.

- 6.4.20 Ergonode Sp. z o.o.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

產品資訊管理市場:按組件、應用、產業和部署模式分類-2026年至2032年全球市場預測

產品資訊管理市場:按組件、應用、產業和部署模式分類-2026年至2032年全球市場預測 產品資訊管理市場報告:按部署類型、組件類型、作業系統、組織規模、產業和地區分類(2026-2034 年)

產品資訊管理市場報告:按部署類型、組件類型、作業系統、組織規模、產業和地區分類(2026-2034 年) 產品資訊管理市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測

產品資訊管理市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測 2026年全球產品資訊管理市場報告全球產品資訊管理市場規模、佔有率、趨勢和成長分析報告(2026-2034年)日本產品資訊管理市場報告:依部署類型、組件類型、組織規模、產業垂直領域及地區分類,2026-2034年

2026年全球產品資訊管理市場報告全球產品資訊管理市場規模、佔有率、趨勢和成長分析報告(2026-2034年)日本產品資訊管理市場報告:依部署類型、組件類型、組織規模、產業垂直領域及地區分類,2026-2034年 產品資訊管理市場規模、佔有率和成長分析(按組件、部署類型、組織規模、最終用戶產業和地區分類)-2026-2033年產業預測

產品資訊管理市場規模、佔有率和成長分析(按組件、部署類型、組織規模、最終用戶產業和地區分類)-2026-2033年產業預測 2025-2029年全球產品資訊管理市場全球產品資訊管理 (PIM) 市場(按組件、部署類型、組織規模、垂直產業、地區分類)預測 - 2020 年

2025-2029年全球產品資訊管理市場全球產品資訊管理 (PIM) 市場(按組件、部署類型、組織規模、垂直產業、地區分類)預測 - 2020 年 PIM 軟體市場報告:2031 年趨勢、預測與競爭分析

PIM 軟體市場報告:2031 年趨勢、預測與競爭分析